FEDS Notes

August 20, 2018

The Branch Puzzle: Why Are there Still Bank Branches?

Elliot Anenberg, Andrew C. Chang, Serafin Grundl, Kevin B. Moore, and Richard Windle*

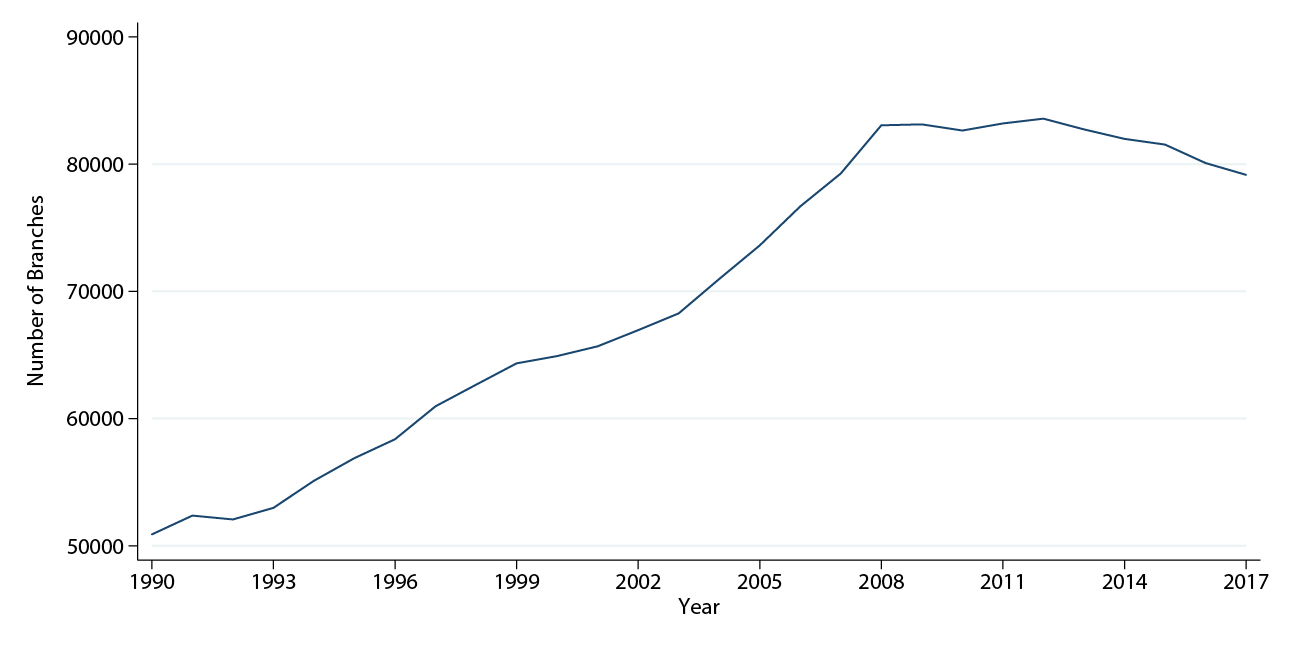

Over the past 25 years, advancements in information technology have allowed for many banking services to be conducted online instead of in a local bank branch. However, Figure 1 shows that the number of bank branches increased from 1990 to 2008, plateaued between 2008 and 2012, and decreased only slightly since 2013 as branch closures in some locations have been somewhat offset by openings in others. 1 The persistence of bank branches is puzzling because the presence of other types of establishments whose products or services are now available online has declined significantly, even for establishments that, unlike banks, sell physical goods.2 Even long before the Internet era, some observers predicted the death of the bank branch as electronic substitutes for branches began to emerge.3

We provide evidence that the persistence of the large number of local bank branches across the country--even in areas with expensive real estate and in the face of improving information technology--may be due to the fact that both depositors and small businesses continue to value local bank branches.

From the triennial Survey of Consumer Finances (SCF), we show that even though the majority of depositors now use online banking, a majority of depositors that use online banking still visit bank branches, which suggests that online banking is an imperfect substitute for bank branches. We also document broad-based reliance of depositors on bank branches, although this reliance varies with age, wealth, income, and occupation.

For small business lending, using Community Reinvestment Act (CRA) disclosures, we show that among banks that are CRA reporters the share of loans made by lenders without a local branch presence remains quite low. This finding suggests that local branch presence is still important for small business lending. However, we also find that among CRA reporters the non-local share has risen substantially since 2011, suggesting that local branch presence has lost some importance in recent years, at least for some businesses.4

This recent trend towards a growing role for non-local lenders could be caused by changes in underwriting technology or by changes in the composition of small businesses themselves. Underwriting technology is changing as credit scoring gains importance in small business lending, which could allow local lenders, who have access to soft information, to face increased competition from non-local lenders. At the same time, the nature of some types of small businesses themselves is changing, as more small businesses sell their goods and services online, and purchase their inputs online.5 This shift in the nature of small businesses also potentially reduces the advantage of local lenders in screening small businesses.

- Depositors

We use the SCF to provide three complementary pieces of evidence that households value local bank branches despite the rise of online banking services: (1) questions on the use of online banking, (2) new questions on the propensity for households to visit local branches, and (3) household subjective assessment of the importance of branch location for selecting their primary financial institution.

Who Uses Online Banking? Most people.

The 2016 SCF asked households whether they used online banking in the last 12 months, and over 70 percent of households reported using online banking. Thus, the persistence of bank branches does not appear to be simply explained by a low online banking take-up rate. In comparison, only 4 percent of households reported using online banking in 1995, suggesting that improvements in information technology have increased the availability and usage of online banking services.6

The 2016 SCF also contained new questions asking whether respondents visited a local bank branch. About 84 percent of households with a checking or savings account reported visiting the local branch of the institution of their main savings or their main checking account within the last year, and almost all households who visited their local branch did so to use banking services other than just the ATM.

Although online banking appears to substitute for services provided by local branches, the substitution is far from complete. Column 1 of Table 1 shows that among households with checking accounts, those who reported usage of online banking were only 2 percentage points less likely to report going to a local branch of the institution of their main checking account. Column 2 shows that among households with savings accounts, online banking usage is somewhat more substitutable with going to the local branch of the institution of their main savings account. For these households the difference is 12 percentage points. However, even among the households with savings accounts that reported using online banking, 70 percent of them still reported going to a local branch.

Table 1: Online Banking Users are Less Likely to Visit Branches

| (1) | (2) | |

|---|---|---|

|

Go to Checking Branch? |

Go to Savings Branch? |

|

| Use Online Banking? |

-0.02** (0.01) |

-0.12*** (0.02) |

| Constant |

0.84*** (0.01) |

0.82*** (0.01) |

Which Households Visit Local Bank Branches? Older, Wealthier, and Self-Employed.

While the 2016 SCF showed that 84 percent of households reported visiting a local bank branch, certain types of households were more likely to visit branches than others. To further explore these differences, we regress a dummy variable, VisitBranch, for whether a respondent's household visited a local branch, on a variety of household characteristics, shown in equation (1).

In equation (1) WealthPercentile is four dummies for whether respondent i's household was in the 25th-49th, 50th-74th, 75th-89th, or 90th+ percentile of wealth, IncomePercentile is five dummies for whether the respondent's household was in the 20th-39th, 40th-59th, 60th-79th, 80th-89th, or 90th+ percentile of income, AgeCategory is five dummies for whether the respondent was 35-44, 45-54, 55-64, 65-74, or 75+ at the time of the survey, OccupationCategory is three dummies for whether the respondent was Self-Employed, Retired/Disabled/Student/Homemaker, or otherwise out of the labor force (the omitted category is working for someone else), and X is a variety of other control variables.7 We estimate equation (1) using the 2016 SCF after applying survey weights.

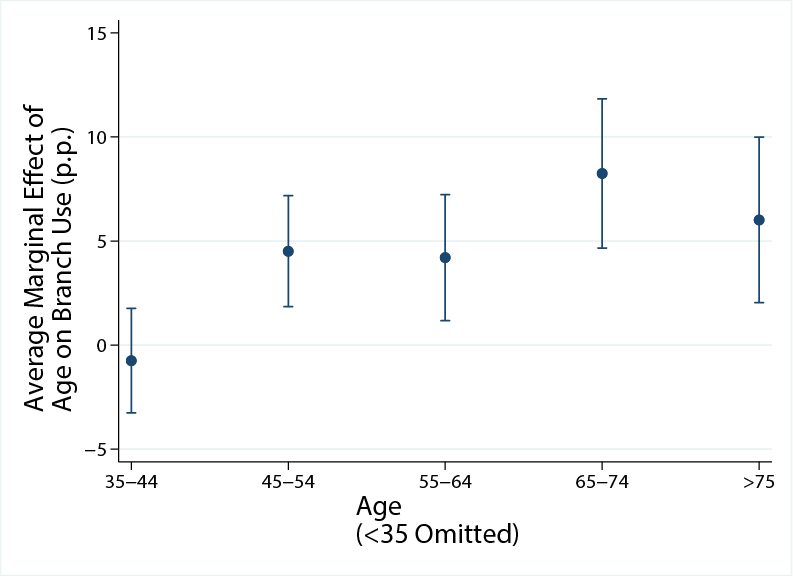

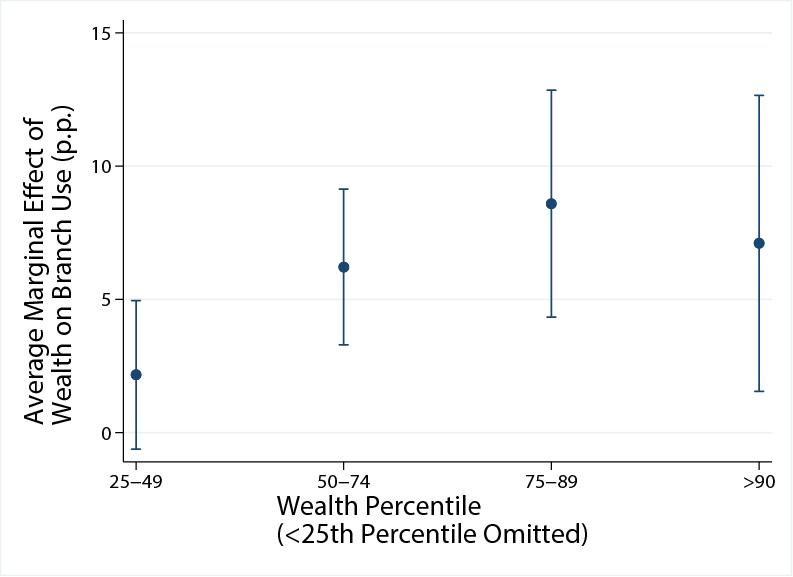

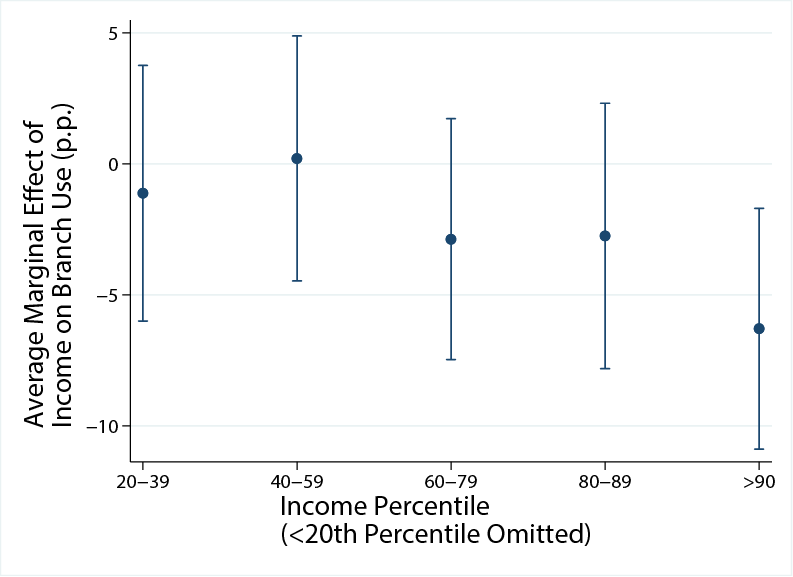

Figure 2: Effects of Depositor Characteristics on Branch Use.

Figure 2b: Wealthier People Use Branches More

Figure 2c: Highest Income People Use Branches Less

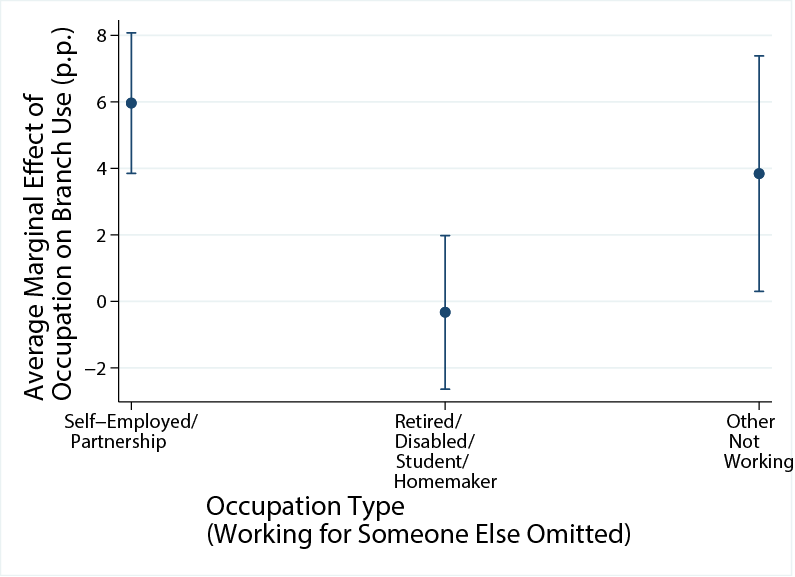

Figure 2d: Self-Employed People Use Branches More

This figure plots the estimated average marginal effects, in percentage points, of age, wealth, income, and occupation on the likelihood that a member of the household visited a local branch of the institution of their primary checking or savings account from equation (1). Whiskers denote 95% confidence intervals. Standard errors are bootstrapped.

Older households were more likely to use their local branch. Figure 2a shows that relative to respondents under the age of 35, respondents over the age of 75 were about six percentage points more likely to have visited a local bank branch in the last year. This pattern could reflect that older households have stronger preferences for visiting their local branch than younger households, but an alternative interpretation is that age is proxying for a year-of-birth effect (i.e. a cohort effect).

Higher wealth households were also more likely to visit their local branch. Figure 2b shows that on average, above-median wealth households were about 7.5 percentage points more likely to have visited their local branch. This finding could reflect higher demand for banking services among higher wealth households, as the SCF also shows that, among households with checking accounts, the number of services a household obtains from its main checking institution increases from 2.0 for the lowest wealth group to 3.6 for the top wealth group. This finding could also reflect that higher wealth households demand certain banking products that are better serviced through visiting a local branch.

While higher wealth households were more likely to use their local branch, higher income households were somewhat less likely to use their local branch, as shown in Figure 2c. Households in the top 10 percent of the income distribution were about 6 percentage points less likely to visit a branch than households in the bottom 20 percent. Visiting a branch is time consuming, and so perhaps the lower usage of local branches among higher income households reflects their higher opportunity cost of time.8

Finally, as shown in Figure 2d, we find that self-employed households were especially likely to use their local branch. They were about 6 percentage points more likely to visit a branch than households that work for someone else. This is perhaps because such households demand a set of banking products (e.g. depositing checks with large balances) that are best serviced through visiting a local branch. The 2016 SCF data show that about 35 percent of self-employed households used the same institution for their business as for their main checking account.

Do Households Place Subjective Value on Branches? Yes, and More Value With Age.

The SCF also asks respondents for the most important reason for choosing the financial institution for their main checking account, offering respondents a menu of options. This question is asked in the 2016 SCF, but also in previous survey years as well. Respondents have consistently said that the location of an institution's offices is the most important reason for choosing their financial institution. This reason accounts for over a third of responses to this question in each survey year.9

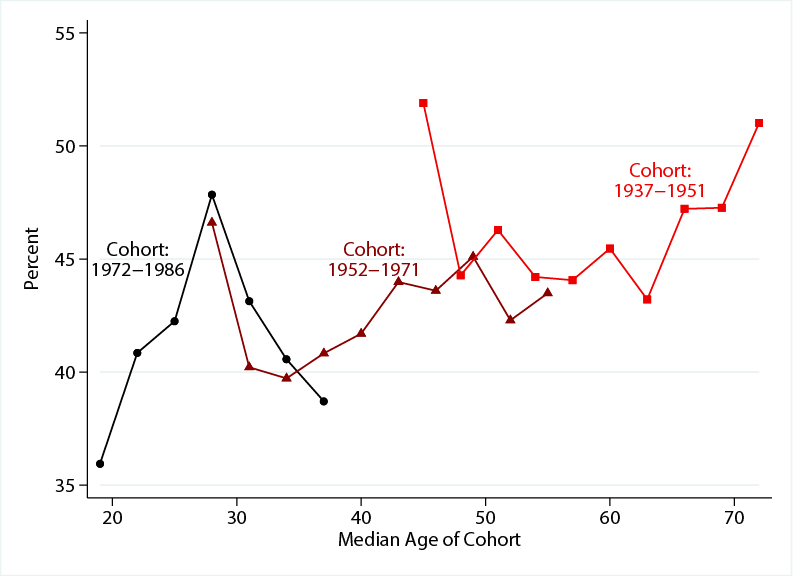

Figure 3 plots the fraction of SCF respondents that list the location of offices as the most important reason for choosing their main financial institution for their checking account, for three birth cohorts, against the median age of the cohort. Figure 3 shows that older households are much more likely to value brick and mortar locations, with an upward trend in the reported value of location of offices starting at around age 31, consistent with our findings in Figure 2a. However, the difference in responses between cohorts for a given age of the cohort, shown by the areas of Figure 3 where two cohorts overlap in age, are usually small. Thus, our results suggest that the increasing effect of age on branch importance reflects an age effect rather than a cohort effect. This interpretation implies that when currently young depositors transition into old age they will have a stronger preference for visiting their local branch, meaning that branches may remain important in the future. That said, our interpretation is based on comparisons of cohorts from decades ago, before the rapid advancements in information technology in recent years, and it is possible that the cohort effect has become more important.

Figure 3: Percent of SCF Households That List the "Location of Offices" as the Most Important Determinant for Selecting their Primary Financial Institution, By Birth Cohort

Cohorts are born from 1937-1951 (light red line with squares), 1952-1971 (dark red line with triangles), and 1972-1986 (black line with circles). Horizontal axis is the age of a household in the middle of the cohort birth range. Data from 1989-2016 SCF.

- Small Businesses

To study the importance of local branches for small businesses, we merge data on small business loans below $1 million, from CRA disclosures, with data on local branches from the Federal Deposit Insurance Corporation's (FDIC) Summary of Deposits.10 We define local markets either as a metropolitan statistical area (MSA) ("urban" market) or as a county for counties not contained in an MSA ("rural" market). In our merged data, we observe lending volume by bank (but not bank branch) and year for three loan size buckets, and the local market in which the small business is located. Our sample period is 2000 to 2016.11

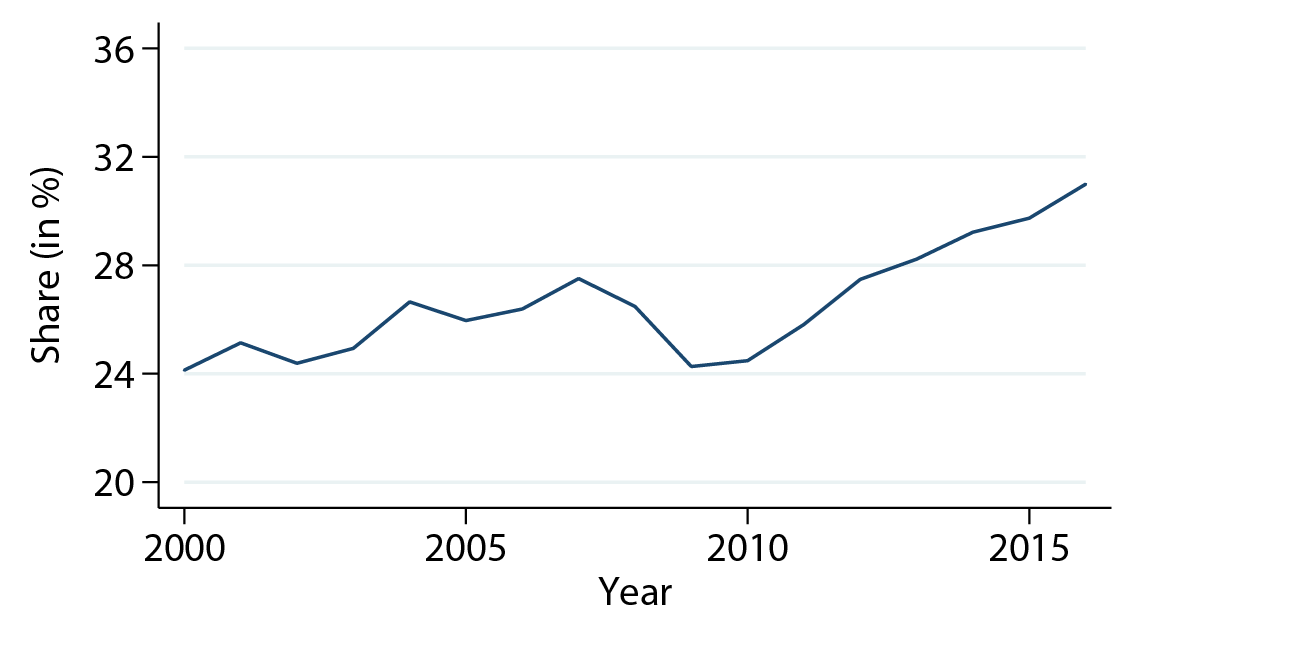

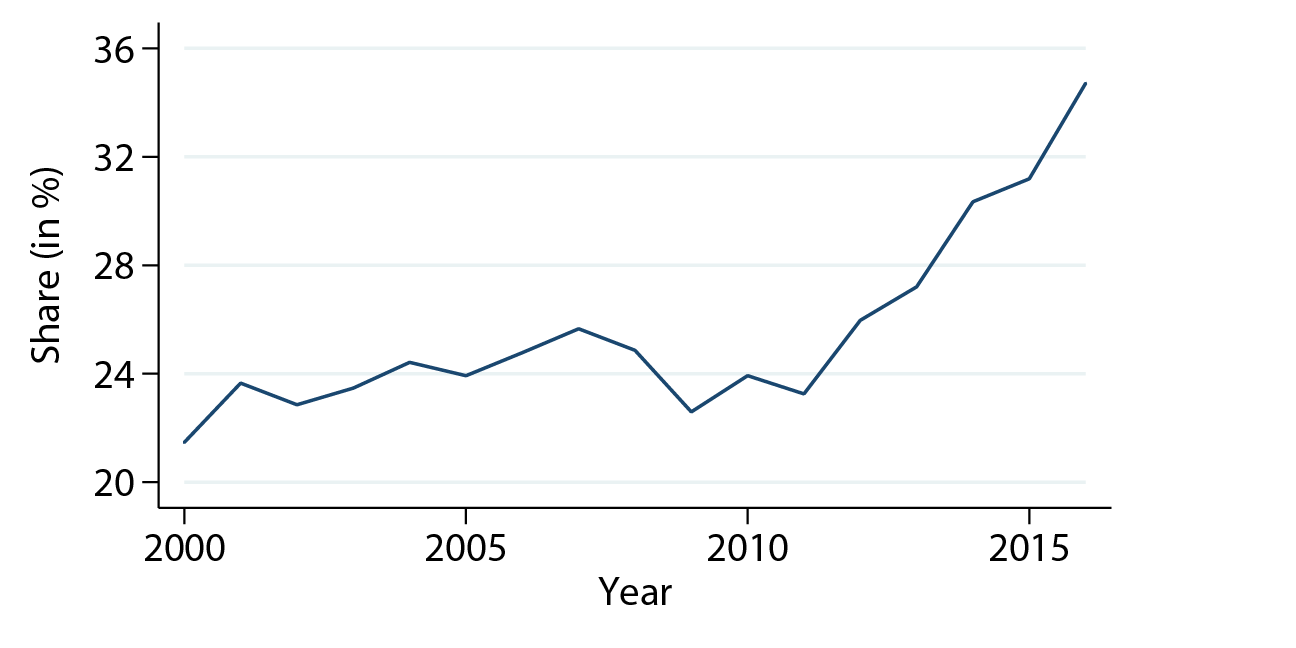

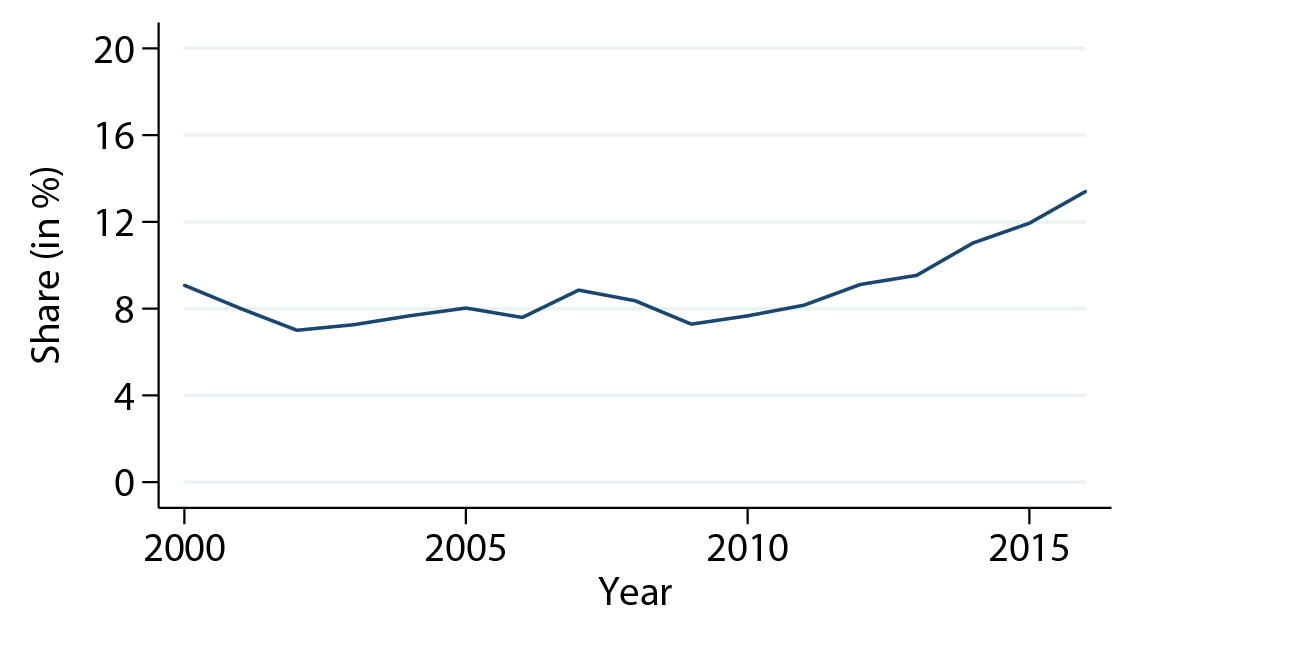

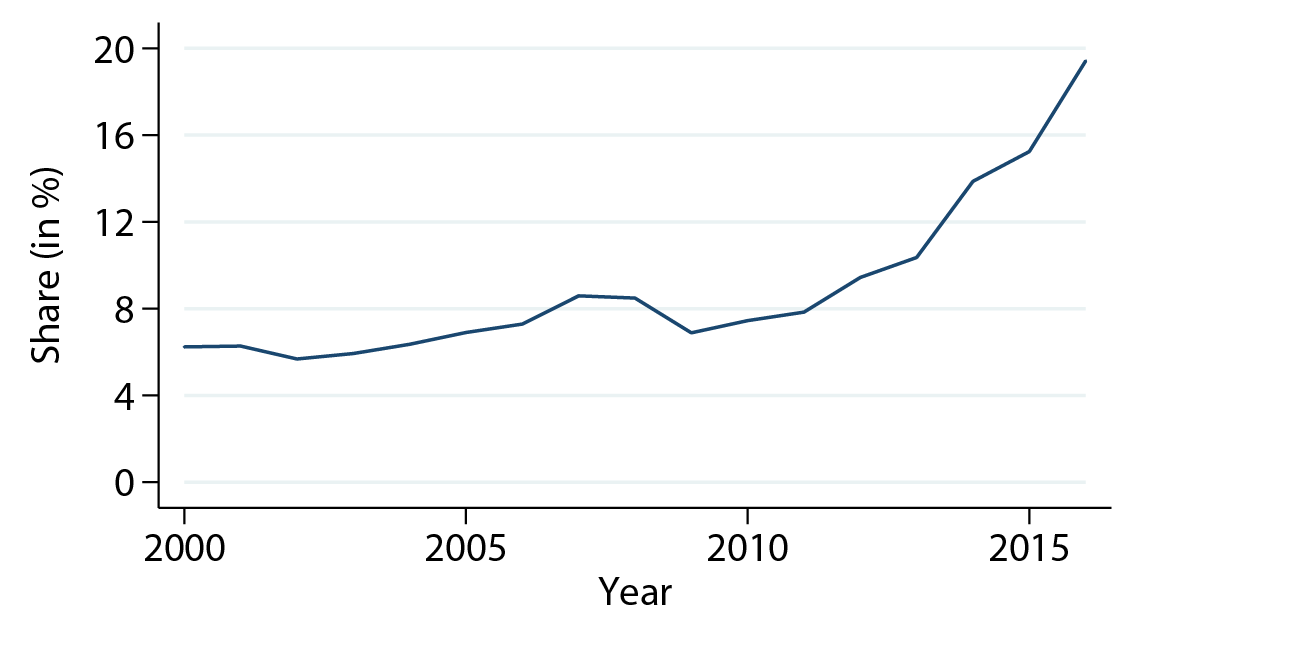

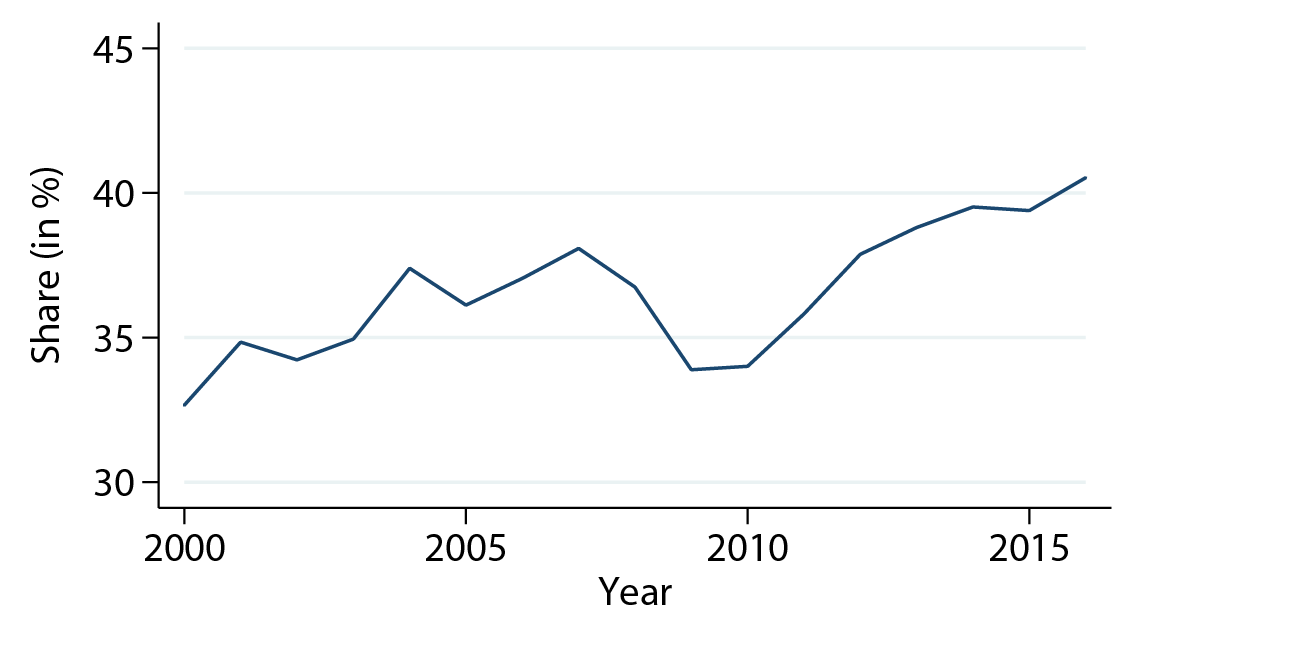

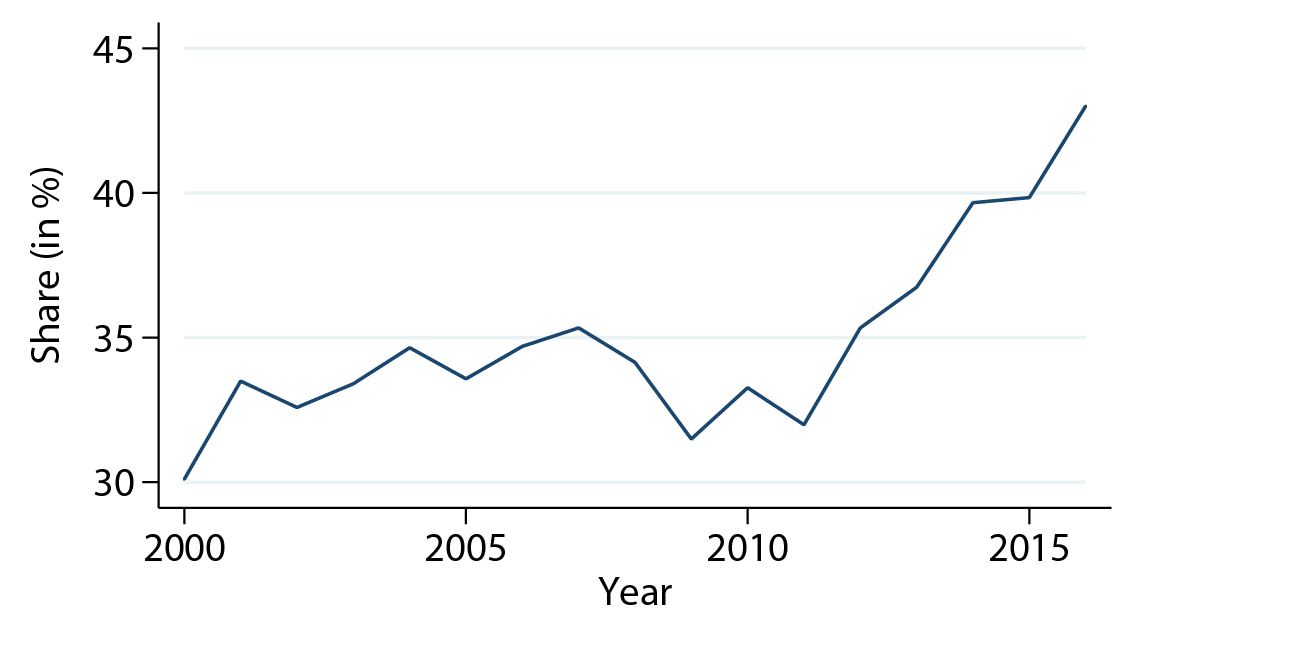

Figure 4: Average Share of Loans by Lenders Without Local Branch Presence Among CRA Reporters.

Figure 4a: All Markets, $100,000-$250,000

Figure 4b: All Markets, $250,000-$1 million

Figure 4c: Urban Markets, $100,000-$250,000

Figure 4d: Urban Markets, $250,000-$1 million

Figure 4e: Rural Markets, $100,000-$250,000

Figure 4f: Rural Markets, $250,000-$1 million

The share is measured by the number of loans in the size bucket. Urban markets are defined as MSAs and rural markets as non-MSA counties.

Figure 4 shows the evolution of the average share of loans made by lenders among CRA reporters without a local branch. The share is shown separately for loans between $100,000 to $250,000 and loans between $250,000 to $1 million.12 The share of lenders without a local branch increased slowly from 2000 to 2008, decreased somewhat during the financial crisis, and increased substantially after 2011. Despite the recent increase, the share of lenders without a branch presence remains below 20 percent for urban markets and below 45 percent for rural markets, which suggests that local branches still play an important role in small business lending.13

One interpretation of the recent increase in the non-local share among CRA reporters is that a local branch is becoming less important for acquiring soft information, possibly caused by changes in underwriting technology (e.g. credit scoring). Alternatively, it could be driven by changes in the nature of small businesses themselves. For example, loan officers in a local branch may have less of a comparative advantage in evaluating small businesses that sell their products online and purchase some of their inputs online.

An important caveat of our analysis is that we only observe banks that are CRA reporters. Small banks that are not CRA reporters might be lending less outside the area of their branch footprint. Therefore, the share of out-of-market lenders may be smaller than the numbers shown in Figure 4 if all banks are taken into consideration.14

As CRA reporters only account for 60-75 percent of small business lending over the sample period, it is possible that lending is more local than suggested by the graphs in Figure 4. However, as the CRA share increased during the sample period, it is unlikely that the recent increase of out-of-market lending among CRA reporters is driven by a shift towards non-CRA reporters.

To further explore the relationship between bank branches and small business lending, we regress a bank's lending market share against its share of branches in that market. This regression also uses year fixed effects and, therefore, we estimate the association of local branches with lending from bank-market-level differences in loan and branch shares. Our specification is:

LoanSharejmt is the amount of small business loans of bank j in market m in year t as a share of total amount of small business loans in market m in year t. BranchSharejmt is the number of bank branches of bank j in market m in year t as a share of total number of bank branches in market m and year t. The coefficient $$\beta_t$$ is allowed to vary by year and $$\mu_t$$ are year fixed effects. The loan share is the loan share among banks that are CRA reporters. The branch share is renormalized such that the branch shares of all banks that are CRA reporters also sum up to one. A higher value of $$\beta$$ implies a closer association between branch presence and small business lending.15 The number of observations is 32,585,004 as each bank-market-time triplet results is an observation.

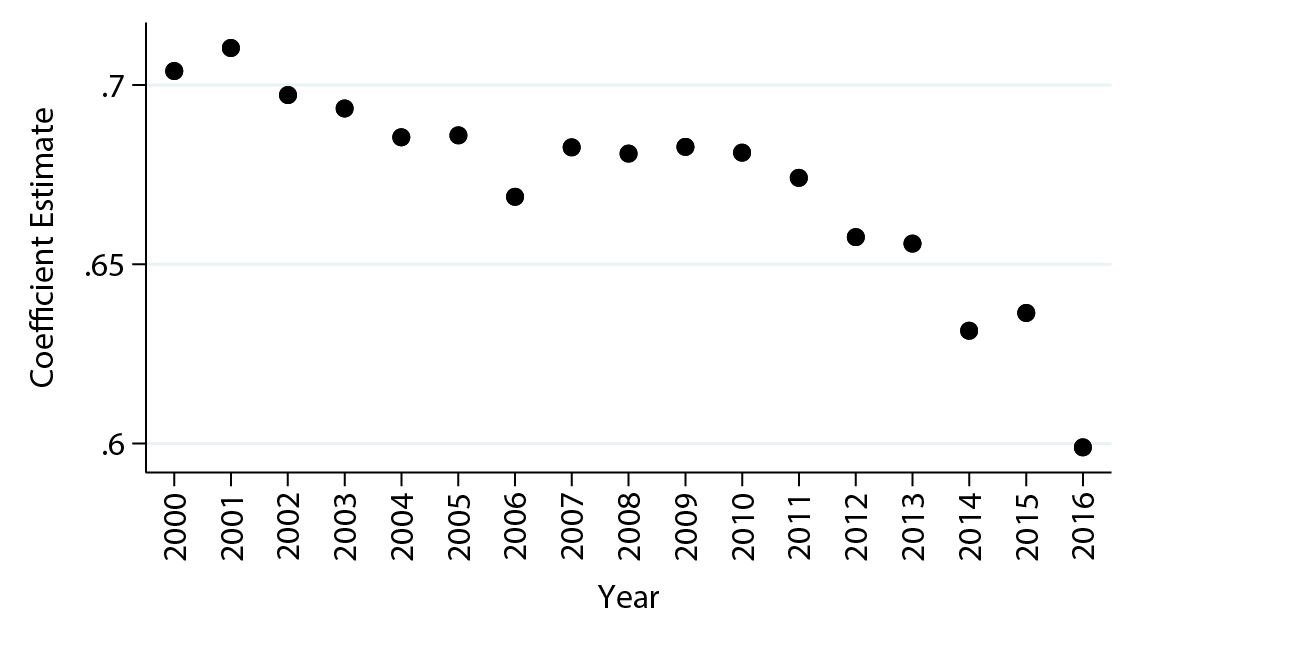

Figure 5 plots the coefficient estimates for $$\beta_t$$ for loans between $100,000 and $250,000. Since the end of the financial crisis, the association between the local branch share and the loan share has decreased. From 2000 to 2010, an increase in the local branch share by 1 percentage point was associated with an increase in the local loan share of 0.67-0.71 percentage points. Between 2011 and 2016, however, this number fell to about 0.60 percentage points. This corroborates the suggestive evidence from the graphs in Figure 4 that non-local lenders are becoming more important for small business lending.16

How does the increasing role of non-local lenders affect small businesses? If the increasing role is driven by improvements in underwriting technology that make non-local lenders more competitive with local ones (e.g. by making more information available at a distance), then small businesses could potentially benefit from increased competition and variety of lenders. However, if the improvements in underwriting technology are accompanied by branch closures, then those small businesses that still rely heavily on local branches, either for borrowing or for other purposes, could be harmed.

Figure 5: Correlation Between Branch Share and Loan Share

This graph shows estimated βt from equation (2). The confidence intervals are not shown because they are very tight and are indistinguishable from the point estimates.

Conclusion

Antitrust analysis of bank mergers currently defines banking markets to be geographically local, and our findings that depositors and small businesses still rely on bank branches support this market definition.17 However, our data also indicate that non-local lenders are gaining importance in small business lending.

References

[1] Sumit Agarwal, Robert Hauswald. Distance and private information in lending. The Review of Financial Studies, 23(7):2757—2788, 2010.

[2] Dean F Amel, Kenneth P Brevoort. The perceived size of small business banking markets. Journal of Competition Law and Economics, 1(4):771—784, 2005.

[3] Dean F Amel, Arthur B Kennickell, Kevin B Moore, others. Banking Market Definition: Evidence from the Survey of Consumer Finances. Divisions of Research & Statistics and Monetary Affairs, Federal Reserve Board, 2008.

[4] Dean F Amel, Martha Starr-McCluer. Market definition in banking: Recent evidence. The Antitrust Bulletin, 47(1):63—89, 2002.

[5] Kenneth P Brevoort, John D Wolken, John A Holmes. Distance still matters: the information revolution in small business lending and the persistent role of location, 1993-2003. , 2010.

[6] Jesse Bricker, Lisa J Dettling, Alice Henriques, Joanne W Hsu, Lindsay Jacobs, Kevin B Moore, Sarah Pack, John Sabelhaus, Jeffrey Thompson, Richard A Windle. Changes in US Family Finances from 2013 to 2016: Evidence from the Survey of Consumer Finances. Federal Reserve Bulletin, 103:1—41, 2017.

[7] Glenn B Canner, others. Evaluation of CRA data on small business lending. Business Access to Capital and Credit:8—9, 1999.

[8] Hans Degryse, Steven Ongena. Distance, lending relationships, and competition. The Journal of Finance, 60(1):231—266, 2005.

[9] Timothy E Dore, Traci L Mach. Recent Trends in Small Business Lending and the Community Reinvestment Act. 2018.

[10] Roberto Felici, Marcello Pagnini. Distance, bank heterogeneity and entry in local banking markets. The Journal of Industrial Economics, 56(3):500—534, 2008.

[11] Stephan Hollander, Arnt Verriest. Bridging the gap: the design of bank loan contracts and distance. Journal of Financial Economics, 119(2):399—419, 2016.

[12] Mitchell A Petersen, Raghuram G Rajan. Does Distance Still Matter? The Information Revolution in Small Business Lending. The Journal of Finance, 57(6):2533—2570, 2002.

[13] Hirofumi Uchida, Gregory F Udell, Nobuyoshi Yamori. Loan officers and relationship lending to SMEs. Journal of Financial Intermediation, 21(1):97—122, 2012.

* We are grateful to Jacob Gramlich and Beth Kiser for helpful comments and to Dean Amel for making the note more entertaining. Thanks to Tim Dore for help with the CRA data. The analysis and conclusions set forth are those of the authors and do not indicate concurrence by other members of the staff, by the Board of Governors, or by the Federal Reserve System. Return to text

1. For example JP Morgan Chase recently announced that it plans to enter 15 to 20 regional markets around the United States by 2023, by opening new 400 branches. Similarly, Bank of America plans to open 500 new branches. Return to text

2. For example the number of book store locations declined from about 38,500 in 2004 to about 22,500 in 2018, according to Statista. In some industries that don't sell physical goods, like travel agencies, brick and mortar stores have disappeared almost entirely. Return to text

3. For example, in 1975, the Vice Chairman of the Federal Reserve George Mitchell said: "I have no doubt that some banks now continuously review their branching policies in light of the development of electronic substitutes for branches but the statistical evidence of such policies is hard to find… It appears to me that the continued growth of banking offices indicates a clear misreading of the trend in the banking technology climate, a misreading that is likely to prove costly for some banking enterprises." But since 1975, the number of bank branches more than doubled from about 30,000 to around 80,000 today. Return to text

4. Our analysis on small businesses relates to the literature on the importance of physical distance and soft information for lending relationships ([12, 5, 8, 10, 11, 13, 1]). Return to text

5. For example Amazon claims that more than 1 million small businesses with revenues below $7.5 million sell on its site. Return to text

6. This statistic is from the 1995 SCF. Prior to 2016, the SCF asked about online banking in a different way than in 2016. Online banking was one of the options for how a household interacted with a financial institution. Using that measure, the fraction of households using online banking increased from 4 percent in 1995 to 64 percent in 2013. Return to text

7. The control variables are: a dummy for being white non-hispanic, a dummy for living in a metropolitan statistical area, dummies for whether the respondent had a checking or a savings account for non-business use at any financial institution (not necessarily at their main financial institution), and a measure of financial literacy, as defined by [6]. Return to text

8. To examine the interaction between wealth and income's effect on the probability of visiting a branch, we re-run equation (1) by replacing WealthPercentile and IncomePercentile with a full WealthPercentile and IncomePercentile interaction set. This regression shows that the probability of visiting a branch conditioned on wealth falls with income for the top three wealth bins. The probability of visiting a branch conditioned on income rises with wealth for the bottom four income bins. Return to text

9. In contrast, less than five percent of respondents cite the location of an institution's offices as the most important reason for choosing their mortgage lender. The difference in these responses is consistent with evidence that markets for mortgages and other consumer loans are more national in scope than the market for depositors. Return to text

10. The Community Reinvestment Act mandates that banks that exceed an asset threshold of about $1 billion must report small business loans to the Federal Reserve Board. The data can be downloaded at https://www.ffiec.gov/cra/craflatfiles.htm. For a description of the data see [7]. See [9] for recent trends in small business lending and background on the Community Reinvestment Act. We estimate that CRA reporters account for about 60 percent of all small business loans as measured by outstanding loan balances. Return to text

11. An important caveat is that these data contain all loans with a small principal amount, not only loans to small businesses. These data are thought to be informative about lending to small businesses because about one half of loans below $1 million are taken out by small businesses with less than $1 million in revenue ([7]). In 2005 the reporting requirements for CRA loans were relaxed. We treat banks that were CRA reporters prior to 2005, but not afterwards, as non-reporters. Return to text

12. We calculate market shares as the fraction of loans to small businesses in the market by lenders without a local branch presence. The average market share is the simple average over all banking markets. We exclude loans below $100,000 because a large fraction of these loans are likely credit card loans. Return to text

13. The higher share for rural markets partly reflects that MSAs (urban markets) are typically comprised of multiple counties whereas we assume rural markets are single counties, and so it is more likely that we classify a lenders as local in an urban market. It may also reflect that local rural lenders are less likely to be required to file CRA disclosures. Return to text

14. To assess this we calculate the share of small business lending by CRA reporters using call report data, which is available for all banks. For loans between $100,000 and $250,000 the share of the CRA reporters increased somewhat from 64.9 percent in 2000 to 72.4 percent in 2016. For loans between $250,000 to $1 million their share also increased from 69.6 percent to 74.0 percent. These shares are based on dollar amounts. Shares based on number of loans are similar.

As CRA reporters only account for 60-75 percent of small business lending over the sample period, it is possible that lending is more local than suggested by the graphs in Figure 4. However, as the CRA share increased during the sample period, it is unlikely that the recent increase of out-of-market lending among CRA reporters is driven by a shift towards non-CRA reporters. Return to text

15. To see this relationship, consider that if all small businesses exclusively borrow locally, then when all loans are of common size and when small businesses are equally likely to choose from any of the local branches, β=1. Return to text

16. We also experimented with including various fixed effects in the specification (2). Including bank or market fixed effects does not change the general pattern of βt. Using loans between $250,000 and $1 million also yields similar results. Return to text

17. The Department of Justice defines geographic markets for the purposes of antitrust analysis such that a "hypothetical monopolist… in that region would profitably impose at least a 'small but significant and nontransitory' increase in price" (see https://www.justice.gov/atr/12-geographic-market-definition). Our results have implications for the geographic market definition in banking antitrust policy, because whether such a price increase would be profitable depends crucially on how many customers rely on local bank branches ([4], [2], and [3]). Return to text

Anenberg, Elliot, Andrew C. Chang, Serafin Grundl, Kevin B. Moore, and Richard Windle (2018). "The Branch Puzzle: Why Are there Still Bank Branches?," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, August 20, 2018, https://doi.org/10.17016/2380-7172.2206.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.