October 01, 2019

Advancing Our Understanding of Community Banking

At "Community Banking in the 21st Century" 2019 Community Banking Research and Policy Conference sponsored by the Federal Reserve System, the Conference of State Bank Supervisors, and the Federal Deposit Insurance Corporation, St. Louis, Missouri

It is a special honor for me to be part of this conference and its tradition of advancing our understanding of how banking shapes our economy and our communities.1 As a community banker, I sought out actionable research that I could leverage to better serve my customers and my community. As a state bank regulator, I conducted my own research to answer questions about issues affecting the banks my agency regulated. I also appreciated learning what researchers thought would provide better insight into the industry. Today I am honored to be here as the first person to serve on the Federal Reserve Board in the role that the Congress designated for someone with community banking or state supervisory experience. My work at the Board has given me an even greater appreciation for how creative, insightful research informs and shapes policy decisions that support our economy. But it also tells me there is still much to be learned and many additional areas that deserve more exploration.

More than 10 years on, as the entire banking industry continues to evolve post-crisis, I would like to share with you some of my thoughts and observations on the forces influencing the future of banking, and community banking in particular. I will also suggest some areas where policymakers could use the help of researchers, bankers, and state supervisors to better understand how community banking is changing and how we can better provide a path for the continued viability of this sector and its business model.

I hardly need to tell this audience that community banks play a vital role in the financial services industry and in the economy. From my perspective, the Federal Reserve supports community banks as a central component of a strong, resilient, and stable financial system. Our system is made more resilient through a broad and varied range of institutions serving different types of customers, with community banks providing access to credit and other financial services in towns and cities across America. With the support of community bankers, these investments are the building blocks of a strong community and help support a vibrant economy across the country—from here in the Midwest to the coasts on either side.

Research on community banking and the accessibility of financial services is incredibly important. Community bankers and policymakers want to better understand how technology, competition, regulation, and other factors are driving decision making, consolidation, and the other challenges and opportunities that are shaping community banking. Existing research provides us with some answers to these questions, but there are many gaps. The lack of a full understanding of these institutions, their functionality, and their needs may limit our ability to identify important areas of focus for research.

This is where I would like to ask for your expertise and assistance. We need to challenge ourselves to tackle some questions and issues that have not been fully explored by researchers. If you are a community banker, are involved in economic development or city or county management, or live in a community served by a community bank, your own experiences likely provide anecdotal evidence regarding the answers to these questions, but research can provide more comprehensive and systematic evidence, leading to more definitive answers. So I need your help. To begin, let's look at the questions.

Community banks provide a variety of benefits to their communities, but these benefits can be difficult to quantify and measure. Therefore, economists and policymakers would like to be able to define and understand the full economic effects of a community bank in an area that relies on it and identify the different channels by which a community bank finances spending, investment, economic development, and job creation. In addition, what happens to a community when a bank headquartered or chartered in that community is acquired by a financial institution located elsewhere? Can we calculate the cumulative contribution of community banks to U.S. investment, employment, and economic output? I hope that presentations at future community banking research conferences can help answer some of these questions and provide a stronger foundation for policy development.

Perhaps as a baseline for this discussion, we can start by looking at what has happened to the structure of the banking industry since the financial crisis. While community banks face considerable challenges, in general they have emerged from the last decade as strong competitors: On average, they have grown somewhat larger and have expanded their geographic footprints. In other words, we have a more resilient, stronger community banking sector, but one with fewer locally headquartered banks.

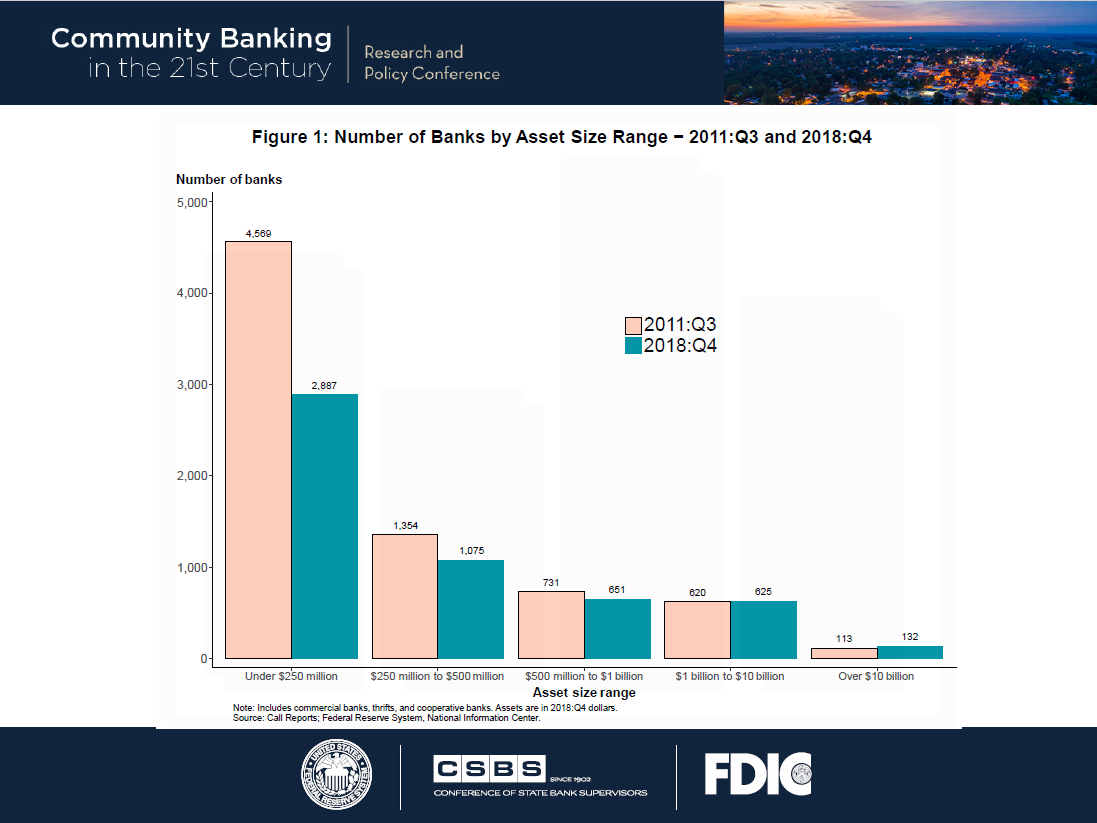

With that in mind, let's look at what leads me to these conclusions. As seen in figure 1, it is true that there are now many fewer small community banks—those with less than $250 million in assets—than there were in 2011.2 At the same time, the numbers of both large community banks and banks over $10 billion in assets (non-community banks) haven't changed much.

{kind=link}

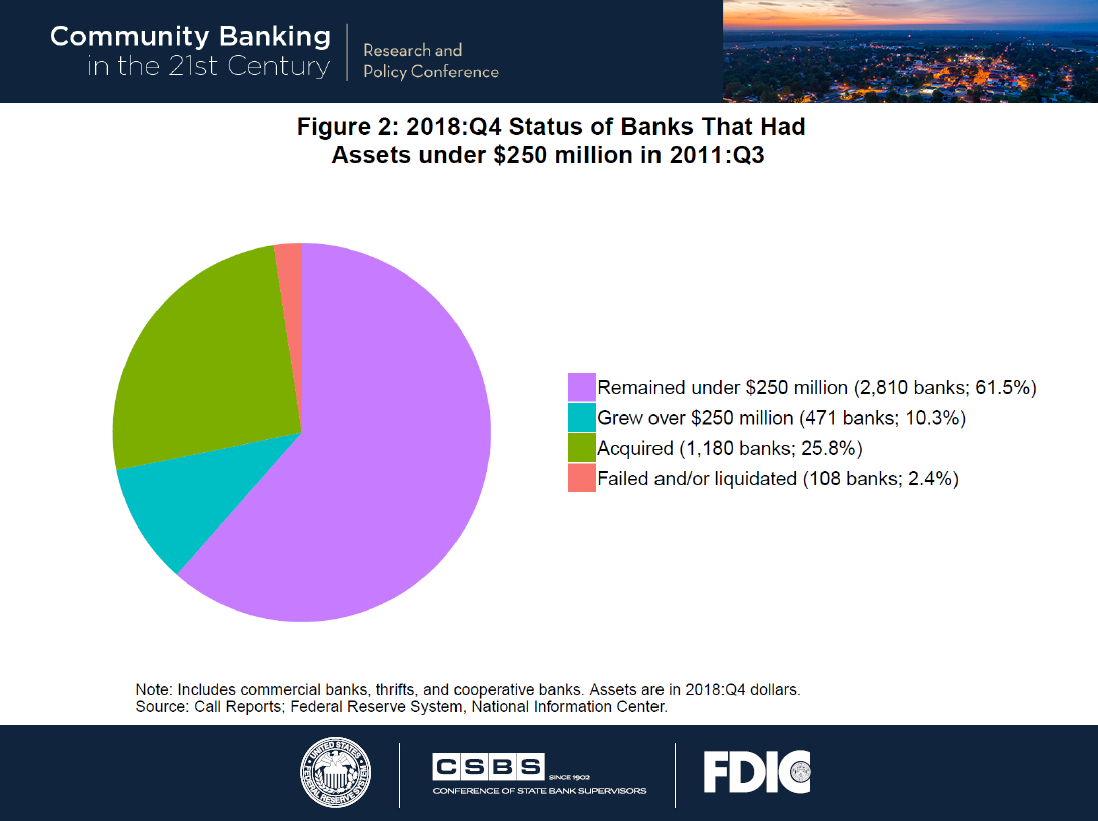

What do we find when we dig a little deeper? As shown in figure 2, very few small community banks failed or were liquidated in the past eight years—just over 100 banks, or 2 percent, of the total number in this size category as of 2011. About 2,800 banks, well over half of this original group, had no change in ownership and stayed below $250 million in assets. About 470 banks, or 10 percent of the initial number, had grown and are now above $250 million in assets.

{kind=link}

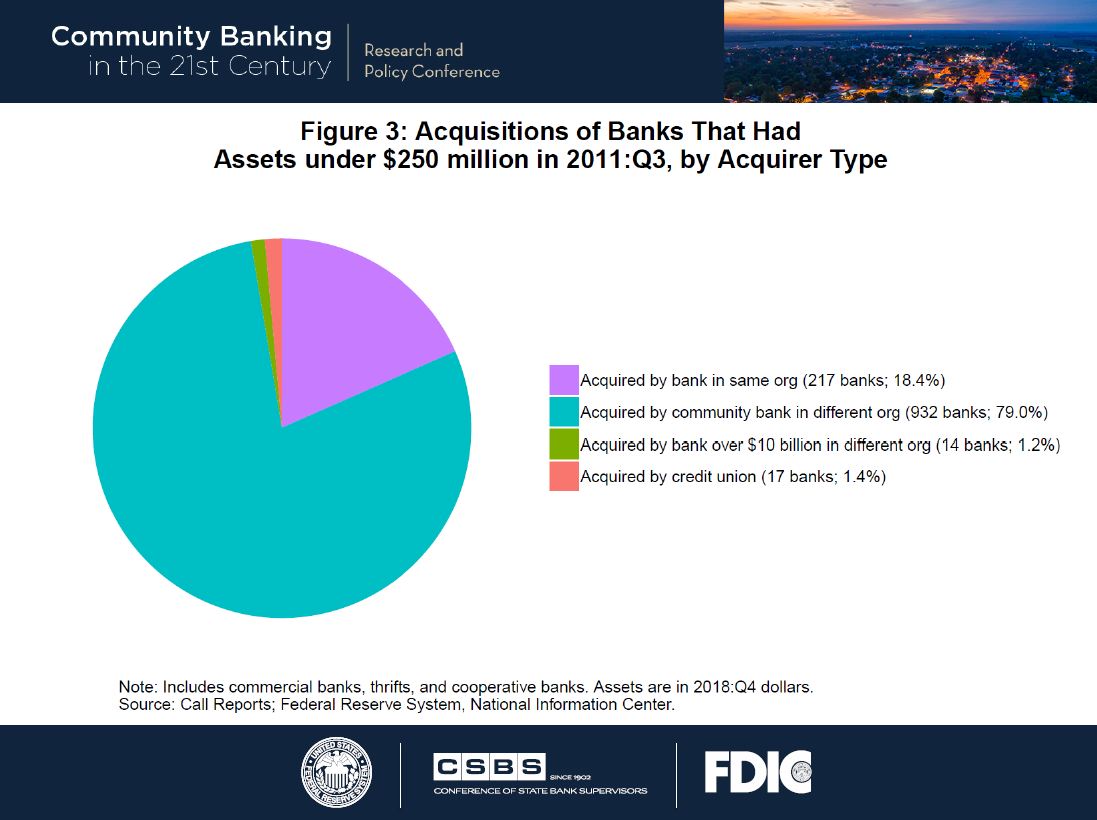

And over this time, just over one-fourth of the smallest community banks, nearly 1,200 of them, were acquired by other banks. That is certainly a large number of acquisitions. But, again, let's look a little deeper. A fair share of those acquired banks—one in five—were acquired by another bank within the same holding company (figure 3). You could consider that more of a reorganization at the holding company level rather than an acquisition by a competitor. The remaining banks—20 percent of the smallest banks operating in 2011—were acquired by another financial institution. Seventeen of the acquisitions, about one and a half percent, were acquisitions of a small community bank by a credit union, while 14, just over one percent, involved a non-community bank acquirer with over $10 billion in assets. In other words, approximately four out of five of the small banks that were acquired during this period, or about 930 banks, were acquired by another community bank.3

{kind=link}

To better understand what is happening with these institutions, we looked at several potential differences between small community banks that have been acquired and those that were not. Was it the smallest community banks, or those with the smallest markets, that were most likely to be acquired? It turns out that the key difference between these banks was not their geographic reach or their size, but rather their profitability. We find that small banks that were acquired by another institution were, on average, about the same size and geographic scope as other small banks but they were less profitable. This fact challenges the notion held by some that small scale or operating in a very limited geographic area is a disadvantage and it shows that many small, locally focused banks are performing well in a changing and challenging marketplace.

Bank regulators should understand how the evolving structure of community banking has affected customers and how regulations can be tailored to limit the extent to which consolidation is driven by unnecessary, ineffective, or excessive regulatory burden. Unfortunately, current research does not provide enough evidence to conclusively answer these questions. Earlier research has shown that technological change and the removal of regulatory restrictions on interstate banking in the 1980s and 1990s have played important roles in driving consolidation.4

We can gain more insight into the factors that underlie changes in community banking by asking community bankers. My former colleagues at the Conference of State Bank Supervisors (CSBS) have done that in their community bank survey and the companion "Five Questions for Five Bankers" interviews.5

Results of the 2019 survey will be revealed during the next session, but I don't think I am giving too much away to share that the factors mentioned as driving consolidation this year remain consistent with previous results. The 2018 survey shows that among banks indicating that they had received and seriously considered accepting an acquisition offer from another institution during the previous 12 months, a large majority say the cost of regulations or the lack of economies of scale at their current size are "important" or "very important" in their decision to consider the offer. About half mention succession issues. The survey did not ask which factor bankers consider most important, and there are many possible reasons a bank would consider selling. But it should not be surprising that the cost of regulation is cited as a leading factor by nearly 75 percent of these respondents.

What about those who made an offer to buy another bank during the past year? A majority, 8 out of 10, cite economies of scale as a factor in making an acquisition offer. Other common motivations include the desire to enter a new market, the ability to exploit underutilized potential at the target institution and the desire to expand within an existing market. I find these results very encouraging, reflecting an industry that believes in the future of community banking and is taking steps to invest in that future.

While it was not addressed in this part of the survey, it seems to me that the cost of regulation could have been a factor in making acquisition offers, possibly based on the theory that there could be efficiency gains by spreading fixed regulatory costs over a larger firm. It is possible these savings may have been a factor for the roughly 80 percent who cited "economies of scale." More detailed questions in future surveys could provide firmer evidence about the effect of regulatory costs on decisions related to consolidation.

The "Five Questions for Five Bankers" initiative provides many additional insights into the forces driving change in community banking. I find this initiative particularly valuable, because it is conducted by state banking commissioners who I know from my experience have deep insights into conditions in their states. Last year, 28 commissioners conducted structured interviews with a small number of community bankers in their states. The results show that bank consolidation is widely viewed as a trend that will continue into the future. Many bankers see that as a concern, but others see consolidation as an opportunity. Bankers from many states cited regulatory burden or compliance costs as major factors driving consolidation. Other frequently mentioned motives for consolidation were the costs of keeping up with technological change and the need to scale up in order to compete in a technology-focused landscape and with non-bank fintech firms in some service areas. Succession planning and finding employees were other common concerns, and bankers in a few states mentioned population decline in some rural areas as a significant issue driving the consolidation trend.

The Five Questions interviews provide a wealth of anecdotes about industry trends, and I would encourage researchers to consider utilizing the detailed interview approach in exploring the causes and effects of community bank consolidation.

It is important to point out that many of the changes to community banking through consolidation that I have described, in a general sense, are a natural and often desirable consequence of competition in a vibrant market economy. However, consolidation is less desirable when it limits access and choice for customers without other benefits, or when it is an unintended effect of government regulation and the cost of that regulation rather than a result of vigorous competition.

This isn't news to community bankers or to community banking researchers. It is not news to many people who live in small towns or urban areas who have lost access to community banks with deep roots in the community. And it is a major challenge for those who live in areas that lack access to service from any bank.

Acquiring banks need to consider that when you purchase a community bank and enter into a new market, along with the new customers and opportunities come a responsibility to be a part of and to support that community. That is why I believe it is critical that we work together to find ways to preserve the benefits provided to communities by well-managed, strong financial institutions that are deeply grounded in the areas they serve—including the communities that they expand or merge into.

Now let's consider how the changes I have described in the banking industry have affected the benefits provided to local communities across the United States. One might expect that the decline in the number of banks over the past few decades would mean communities would see fewer banks operating within the average local banking market. In fact, when viewing the data in a national perspective, the number of banks per local market has been quite stable over time in both urban and rural areas. There may be two factors that explain this outcome. First, many bank mergers combine firms that do not operate in the same local area, so they don't reduce the number of competitors in any market. Second, many banks continue to expand their geographic scope by opening branches in new markets, leading to an increase in the number of banks in those local areas that offsets the decline from bank mergers in the same market.

Of course, stability in the average number of banks across a large number of markets does not imply stability locally within each market. Many local markets have seen declines in the number of banks, while others have experienced increases. And even if the number of banks in a community does not change, there is a difference for customers and communities between a branch of a bank with numerous locations and the headquarters of a bank that is strongly rooted in a community. For example, does bank consolidation influence the availability of credit to local small businesses?

A number of studies have addressed this question and have yielded mixed results. The effect of a merger on small business lending depends on a number of factors, including the size of the merging banks, whether the acquirer is focused on small business lending, and the response of other local banks to the merger.6 Studies have also shown that the post-merger bank tends to be healthier than the target institution was before the merger, which could to lead to an increase in the availability of credit in the community.7 The bottom line is that some studies find small business lending goes up after mergers, and others find it goes down. Given the wide range of results, this is another topic where policymakers and the public would benefit from further research and analysis.

One very clear trend in the United States is a decline in the number of bank headquarters. Acquisitions have resulted in the conversion of many bank headquarters into new branches of the acquiring institution. Unfortunately, some evidence suggests that these conversions may adversely affect the local communities that are no longer home to a headquarters. The impacts extend well beyond the availability of credit. Bank executives and staff who serve on the local chamber of commerce or on the boards of local hospitals or nonprofits may move to the new headquarters location, creating a leadership void in their old hometown.

Unfortunately, community involvement like this is difficult to measure. We turned to Community Reinvestment Act (CRA) performance evaluations in the hope that they would offer some insights into local involvement by banks. Because certain institutions are subject to community development tests, their performance evaluations include information on the bank's qualifying loans, investments (including donations) and services, grants, and certain community service activities.8

Comparing performance evaluations from CRA exam reports before and after an acquisition can provide some limited, case-specific evidence on the potential consequences of the loss of a bank headquarters. Several examples from the past decade show that local donations and community service activity decline in communities that lost a bank headquarters following a merger. Pre-merger CRA evaluations detailed donations to organizations targeting initiatives such as child care, job training, homeless shelters, and scholarship programs for low- and moderate-income (LMI) individuals. Other notable activities included in-kind donations of real estate to Habitat for Humanity and monetary contributions to food pantries, Meals on Wheels, and Big Brothers Big Sisters of America. Bank officers and employees also donated significant time to community service including through financial education to LMI individuals, mentoring programs, and service on the boards of local housing development agencies. Many of these benefits were lost after a merger. The wealth of information that supervisors include in the CRA reports offers a unique look into the type of involvement that communities potentially stand to lose when headquarters move or are eliminated. More research into the effects of losing a bank headquarters could help determine whether these examples are isolated or a predictable result of consolidation.

In closing, let me return to the question of what we know and what we would like to know. We know that consolidation accelerated after the Congress removed barriers to interstate banking, and that it has proceeded more or less steadily since that time. We do not know if and to what extent other factors—such as achieving a desired level of economies of scale, for example—have been driving consolidation. We have recently seen a rising number of acquisitions by credit unions, and we do not fully understand the implications of this trend, which seems likely to continue to accelerate. We know that profitability is a more important factor in predicting acquisitions than bank size or geographic area, but more research on why some smaller banks are more profitable than others could be valuable. We know from the CSBS surveys that regulatory costs are motivating banks that are considering selling or merging, and we could learn more about what is motivating buyers.

Deeper and more creative research is certainly needed to understand how acquisitions affect many communities, small businesses, and consumers. One factor is the vital leadership and supporting role many small banks play in their communities. While that benefit may be hard to measure, I think it is essential that researchers try to do so. Communities need leaders and institutions that are deeply rooted in their cities, towns, and rural areas. Strong relationships and extensive experience are not easily replaced.

Finally, it is important that we understand why so few new banks have been created. Are asset thresholds too high? Are regulations too burdensome? Or have low interest rates meant that net interest rate margins are just too narrow? Understanding the lack of new bank formation is as important as understanding the extent of consolidation and competition.

I am sure you have noticed that I have given you more questions than answers today. That was one of my goals, because I am confident that as researchers you have the skills and creativity to focus on the best questions and find the most insightful answers. And when you do uncover new insights, my colleagues and I will always be eager to learn from and act on what you have found.

References

Avery, Robert B., and Katherine A. Samolyk (2004). "Bank Consolidation and Small Business Lending: The Role of Community Banks," Journal of Financial Services Research, vol. 25 (April), pp. 291–325.

Berger, Allen N., Rebecca S. Demsetz, and Philip E. Strahan (1999). "The Consolidation of the Financial Services Industry: Causes, Consequences, and Implications for the Future," Journal of Banking and Finance, vol. 23 (February), pp. 135–94.

Berger, Allen N., Anthony Saunders, Joseph M. Scalise, and Gregory F. Udell (1998). "The Effects of Bank Mergers and Acquisitions on Small Business Lending," Journal of Financial Economics, vol. 50 (November), pp. 187–229.

Focarelli, Dario, Fabio Panetta, and Carmelo Salleo (2002). "Why Do Banks Merge?" Journal of Money, Credit and Banking, vol. 34 (November), pp. 1047–66.

Jagtiani, Julapa, Ian Kotliar, and Raman Quinn Maingi (2016). "Community Bank Mergers and Their Impact on Small Business Lending," Journal of Financial Stability, vol. 27 (October), pp. 106–21.

Peek, Joe, and Eric S. Rosengren (1998). "Bank Consolidation and Small Business Lending: It's Not Just Bank Size That Matters," Journal of Banking and Finance, vol. 22 (August), pp. 799–819.

1. I would like to thank Robin Prager, John Kandrac, and Mark Wicks for their research and assistance in preparing this speech. Return to text

2. Assets are in constant 2018 dollars. Return to text

3. The pattern during the pre-crisis period is similar. The difference from the post-crisis period is that from the fourth quarter of 1998 to the third quarter of 2007, a larger share of the acquisitions involved an internal reorganization within a bank holding company. This period begins four years after the signing of the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994, which removed many restrictions on interstate banking. Return to text

4. See Berger, Demsetz, and Strahan (1999) and Focarelli, Panetta, and Salleo (2002). Return to text

5. A video on the results of the CSBS 2018 Survey of Community Banks is available on this conference's website at https://www.communitybanking.org/news; for more information on the survey, see the CSBS website at https://www.csbs.org. Return to text

6. For example, see Berger and others (1998), Peek and Rosengren (1998), and Avery and Samolyk (2004). Return to text

7. See Jagtiani, Kotliar, and Maingi (2016). Return to text

8. Under CRA, a small institution has assets of less than $321 million as of December 31 in both of the two prior calendar years. An intermediate small institution has at least $321 million in assets and less than $1.284 billion in assets under the same calendar rules. A large institution has greater than $1.284 billion in assets as of December 31 in both prior calendar years. Activities that qualify for community development tests must primarily focus on economic development, revitalization of low- and moderate-income (LMI) locales, affordable housing, and services that target to LMI individuals. Large and intermediate small banks are subject to review of their community development activities while some small banks voluntarily choose to have their community development activities reviewed. Return to text