September 27, 2017

Labor Market Disparities and Economic Performance

Governor Lael Brainard

At "Banking and the Economy: A Forum for Minority Bankers," a conference hosted by the Federal Reserve Bank of Kansas City, Kansas City, Missouri

I would like to thank President George and her staff at the Federal Reserve Bank of Kansas City for inviting me to participate in today's conference, which is a joint effort of the Federal Reserve Banks of Atlanta, Kansas City, Minneapolis, Philadelphia, Richmond, and St. Louis as well as the Federal Reserve Board.1

Diversity in Financial Services

As you may know, this is the second minority bankers forum hosted by the Federal Reserve System. Diversity and inclusion are important to the strength of the banking industry, and therefore I am pleased that the Federal Reserve System is sponsoring this conference. Among other benefits, diversity and inclusion strengthen organizations by improving deliberations and decisionmaking. Banks with more diverse workforces are also better able to reach broader groups of customers, especially customers who have historically been underbanked, when they show that serving those customers is a top priority. One of the most effective ways of showing a commitment to a diverse customer base is showing a commitment to a diverse workforce.

We now have substantial empirical evidence documenting the benefits of diversity in broadening the range of ideas and perspectives that are brought to bear on solving problems, and thereby contributing to better outcomes, in research, policy, and business. Studies suggest that increased diversity alters group dynamics and decisionmaking in positive ways. Microeconomic experiments and other research have confirmed these ideas. One experiment found that greater racial diversity helped groups of business students outperform other students in solving problems. And another found similar benefits from gender diversity. A study of 2.5 million research papers across the sciences found that those written by ethnically diverse research teams received more citations and had a greater influence than papers by authors with the same ethnicity.2

As a bank regulator, the Federal Reserve has an interest in promoting diversity in the financial services industry. For example, the Federal Reserve Bank of Chicago is actively engaged in developing diverse talent in the financial services industry as a key partner of the Financial Services Pipeline Initiative (FSP). The FSP is a collaborative of about 20 financial services organizations that are working together to increase the representation of Latinos and African Americans, at all levels, within the Chicago-area financial services industry. The members of this initiative recognize they have a collective interest in developing a diverse pipeline of talent. They are more likely to be more successful in achieving their internal pipeline goals if they succeed in improving diversity and inclusion in the finance workforce more broadly.

Another example of our work to promote diversity at banking institutions is the standards developed by the Board's Office of Minority and Women Inclusion to promote transparency and awareness of diversity policies and practices within banking institutions. The Board encourages banking institutions not only to provide their policies, practices, and self-assessment information to the Board, but also to disclose this information to the public. We hope that this new self-assessment tool will help individual banks achieve their own diversity and inclusion goals and contribute to greater diversity in the banking industry more generally.

I also want to take this opportunity to update you on what we are doing to preserve and promote Minority Depository Institutions (MDIs). Though I know that only some of you work for MDIs, the Federal Reserve recognizes their vital role in serving low- and moderate-income and minority communities as well as bringing diversity to the field of banking. I make a point of meeting with the leadership of MDIs as I travel around the country so I can hear firsthand about the challenges these institutions face and the important work they are doing to provide financial services to minority and historically underserved populations. I have heard from CEOs of MDIs about how challenging it can be to simultaneously serve their target market and be a bank of choice in a competitive banking market. Some have managed to thread that needle successfully by remaining firmly rooted and accessible in the communities they serve as well as maintaining their focus on trust, loyalty, and personalized relationship banking, which is a particular strength and competitive advantage for MDIs.

The Federal Reserve has developed a national outreach program called the Partnership for Progress to assist MDIs in confronting business model challenges, cultivating safe banking practices, and competing more efficiently. Recently, the Board doubled its resources for this program to better support MDIs. We brought to bear the resources of our community development function, which promotes economic growth and financial stability in lower-income communities. Combining the resources of our banking and supervision staff with our community development staff allows us to be more creative in supporting MDIs around the country. Recognizing that there has been a dearth of MDI research in recent decades, last year, for the first time, we commissioned two external researchers to develop papers on MDIs. The resulting new papers, along with another written by economists at the Federal Reserve Bank of Chicago, were presented at the interagency biennial MDI conference this past April in Los Angeles. We are in the process of commissioning research for next year in an effort to deepen our understanding of these unique institutions.

Labor Market Disparities

Turning to the workforce more broadly, I want to spend some of my time today talking about disparities and share some findings from a conference we hosted yesterday at the Board titled "Disparities in the Labor Market: What Are We Missing?" In fulfilling its dual mandate, the Federal Open Market Committee (FOMC) has set a target of 2 percent for inflation but does not have a similarly fixed numerical goal for maximum employment. That is because the level of maximum employment depends on "nonmonetary factors that affect the structure and dynamics of the labor market," which "may change over time and may not be directly measurable."3 Understanding how close the labor market is to our full-employment goal requires consulting a variety of evidence along with a healthy dose of judgment. This approach to maximum employment has allowed the FOMC to navigate the current expansion in a way that has likely brought more people back into productive employment than might have been the case with a fixed unemployment rate target based on pre-crisis standards.

The Federal Reserve is also keenly interested in disparities in employment, labor force participation, income, and wealth because they may have implications for the growth capacity of the economy. When we consider appropriate monetary policy, we need to have a good sense of how fast the economy can grow without fueling excessive price inflation. At a time when the retirement of the baby-boom generation looks likely to be something of a drag on the growth of the labor force, it is especially important to consider whether relatively low levels of employment and labor force participation for some prime working-age groups represent slack that, if successfully tapped, could increase the labor force and boost economic activity.

More broadly, when a person who was previously unemployed or discouraged secures a job, not only does it boost the economy, but that person also may gain a greater sense of economic security, self-sufficiency, and self-worth and be better able to invest in their family's future. With a richer understanding of economic or social barriers that inhibit labor market success and prosperity for some groups, we may better grasp how much these individuals can be helped by broad economic expansion and how much targeted intervention is required through other policy means.4

There is also an important connection between the economy's potential growth rate and equality of opportunity. Large disparities in opportunity based on race, ethnicity, gender, or geography mean that the enterprise, exertion, and investments of households and businesses from different groups are not rewarded commensurately. To the extent that disparities in income and wealth across race, ethnicity, gender, or geography reflect such disparities in opportunity, families and small businesses from the disadvantaged groups will then underinvest in education or business endeavors, and potential growth will fall short of the levels it might otherwise attain.5

Aside from reducing the long-run productive potential of the economy, persistently high levels of income and wealth inequality may also have implications for the robustness of consumer spending, which accounts for roughly two-thirds of aggregate spending in the United States. The gaps in household income and wealth between the richest and poorest households are at historically high levels, as income and wealth have increasingly accrued to the very richest households. For example, results from the Federal Reserve's latest Survey of Consumer Finances (SCF), which is due to be released soon, indicate that the share of income held by the top 1 percent of households reached 24 percent in 2015, up from 17 percent in 1988. The share of wealth held by the top 1 percent rose to 39 percent in 2016, up from 30 percent in 1989.6 Some research suggests that widening income and wealth inequality may damp consumer spending in the aggregate, as the wealthiest households are likely to save a much larger proportion of any additional income they earn relative to households in lower income groups that are likely to spend a higher proportion on goods and services.7

Disparities by Race and Ethnicity

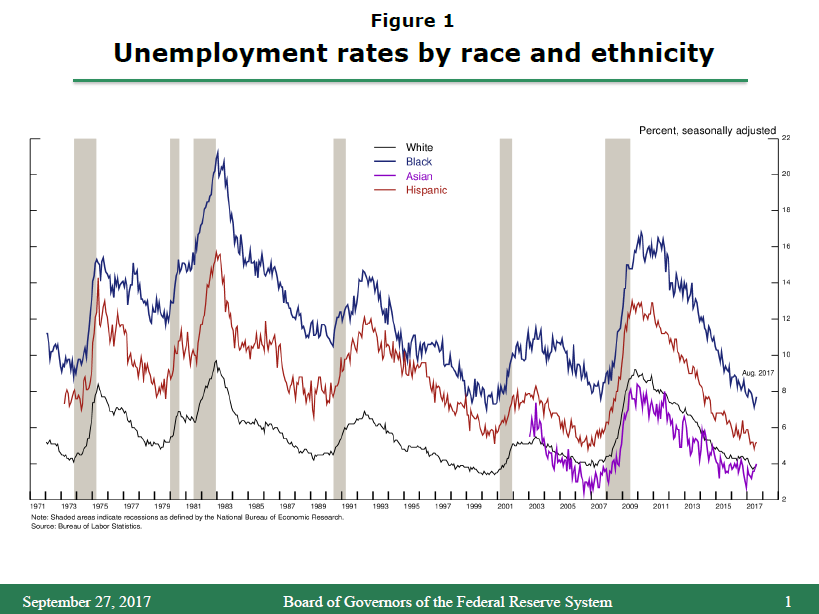

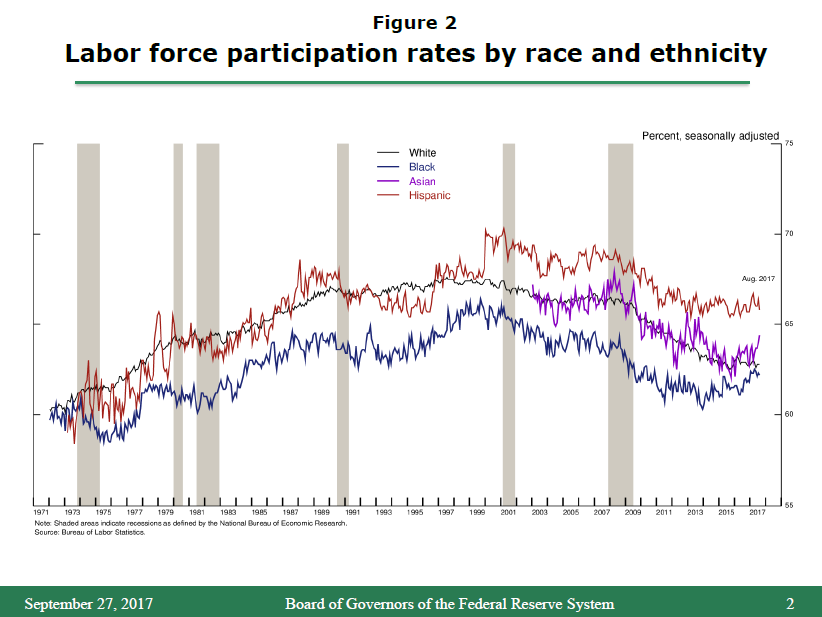

When we disaggregate the economy-wide labor market statistics, we find significant and persistent racial and ethnic disparities.8 In August, the national unemployment rate of 4.4 percent, which is low by historical standards, masked substantial differences across different demographic groups. As shown in figure 1, unemployment rates ranged from 3.9 percent for whites to 4 percent for Asians, 5.2 percent for Hispanics, and 7.7 percent for African Americans. Labor force participation rates, shown in figure 2, also differ substantially, although by less than unemployment rates, with the rate for African Americans lowest at 62.2 percent. These differences are not a recent development--similar differences across racial and ethnic dimensions have existed for as long as these data have been collected. Even more striking, a significant portion of the gaps in unemployment rates across racial and ethnic groups cannot be attributed to differences in their underlying characteristics, such as age and education levels.9

{kind=link}

{kind=link}

Although the differences in employment rates between racial and ethnic groups are still quite large, they have narrowed recently, after having widened considerably during the recession, and are near their lowest levels in decades. Differences in unemployment rates across racial and ethnic groups tend to widen sharply during recessions, as less advantaged groups shoulder an outsized share of total layoffs, and these differences shrink during recoveries. For example, in the second quarter of 2017, the unemployment rate for black adult men was a little more than 3 percentage points higher than for white adult men. This differential, while sizable, is nonetheless close to the smallest gap seen since comparable data became available in the mid-1970s. Differences in unemployment rates are similarly near historical lows for black women relative to white women, and for Hispanics relative to whites. Since racial disparities tend to get smaller throughout the course of an economic expansion, it seems likely that racial differences in unemployment rates will continue to shrink if the overall unemployment rate falls further.10

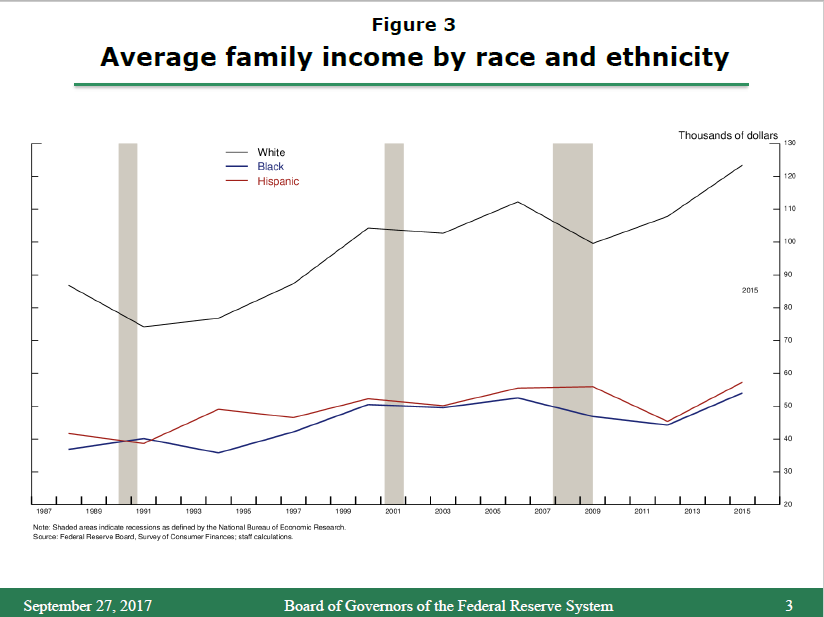

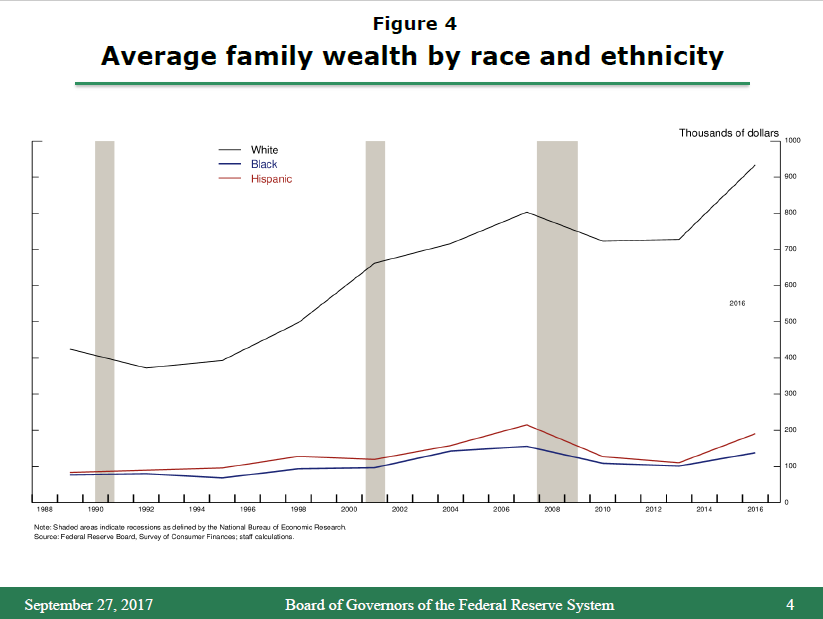

More broadly, the persistent disparities in employment outcomes are mirrored in significant and persistent racial and ethnic differences in families' income and wealth. According to forthcoming findings from the latest SCF and as shown in figure 3, the average income for white families in 2015 was about $123,000 per year, compared with $54,000 for black families and $57,000 for Hispanic families.11 Disparities in wealth, shown in figure 4, are even larger: Average wealth holdings for white families in 2016 were about $933,000, compared with $191,000 for Hispanic families and $138,000 for black families.12 Moreover, these racial and ethnic gaps in average family income and wealth have generally widened rather than narrowed over the past few decades. Based on SCF data, median family wealth has grown much more rapidly for white families than for other families over the past few decades, while median family incomes have risen by about the same amount for white, black, and Hispanic families.

{kind=link}

{kind=link}

As the economic expansion continues and brings more Americans off the sidelines and into productive employment, it seems likely that the positive trends in employment and participation rates for historically disadvantaged groups will continue. That said, the benefits of a lengthy recovery can only go so far, as the research points to some barriers to labor market outcomes for particular groups that appear to be structural. After controlling for sectoral and educational differences, the research suggests that these factors include discrimination as well as differences in access to quality education and informal social networks that may be an important source of information and support regarding employment opportunities.13

Federal Reserve Work on Labor Market Disparities

While the policy tools available to the Federal Reserve are not well suited to addressing the barriers that contribute to persistent disparities in labor market outcomes, understanding these barriers and efforts to address them is vital in assessing maximum employment as well as potential growth. The Federal Reserve is deeply engaged in understanding disparities through our data collection, research collaboration, and community development work. One way the Federal Reserve seeks to obtain a clearer picture is by collecting data ourselves. For instance, some of the data I have cited today come from the Federal Reserve's triennial Survey of Consumer Finances, which provides detailed information on income and wealth holdings by demographic groups. The Survey of Household Economics and Decisionmaking provides a portrait of household finances, employment, housing, and debt; the Survey of Young Workers provides insights into younger adults' employment experiences soon after entering the labor force; and the Enterprising and Informal Work Activities Survey provides information about income generating activities that are often outside the scope of other employment and income surveys.14

Each recent edition of the semiannual Monetary Policy Report (MPR) has focused on some aspect of the comparative economic experience of different racial and ethnic groups. In addition, as indicated in the minutes published after each meeting of the Federal Open Market Committee (FOMC), Federal Reserve staff regularly report on the differential labor experiences of different racial and ethnic groups as background for the FOMC's deliberations on monetary policy.

Across the Federal Reserve System, a variety of initiatives are aimed at understanding economic disparities and how to foster more-inclusive growth. The Opportunity and Inclusive Growth Institute at the Federal Reserve Bank of Minneapolis brings together researchers from a variety of fields to analyze barriers to economic opportunity and advancement. The Economic Growth and Mobility Project at the Federal Reserve Bank of Philadelphia aims to bring together researchers with community stakeholders to focus on differences in poverty and economic mobility across demographic characteristics. The Investing in America's Workforce Initiative is a collaboration between the Federal Reserve System and academic research institutions to promote investment in workforce skills that better align with employers' needs.15

In short, a deeper understanding of labor market disparities is central to the mission of the Federal Reserve because it may help us better assess full employment, where resources may be underutilized, and the likely evolution of the labor market and overall economic activity. Let me conclude by thanking you again for having me here today and allowing me the opportunity to explore some of the factors that influence labor market disparities.

References

Alichi, Ali, Kory Kantenga, and Juan Solè (2016). "Income Polarization in the United States (PDF)," IMF Working Paper 16/121. Washington: International Monetary Fund.

Bayer, Amanda, and Cecelia Elena Rouse (2016). "Diversity in the Economics Profession: A New Attack on an Old Problem," Journal of Economic Perspectives, vol. 30 (Fall), pp. 221-42.

Bernstein, Jared (2013). "The Impact of Inequality on Growth." Washington: Center for American Progress.

Bricker, Jesse, Lisa J. Dettling, Alice Henriques, Joanne W. Hsu, Lindsay Jacobs, Kevin B. Moore, Sarah Pack, John Sabelhaus, Jeffrey Thompson, and Richard A. Windle (forthcoming). "Changes in U.S. Family Finances from 2013 to 2016: Evidence from the Survey of Consumer Finances," Federal Reserve Bulletin.

Cajner, Tomaz, Tyler Radler, David Ratner, and Ivan Vidangos (2017). "Racial Gaps in Labor Market Outcomes in the Last Four Decades and over the Business Cycle (PDF)," Finance and Economics Discussion Series 2017-071. Washington: Board of Governors of the Federal Reserve System.

Carpenter, Seth, and William M. Rodgers (2004). "The Disparate Labor Market Impacts of Monetary Policy," Journal of Policy Analysis and Management, vol. 23 (Fall), pp. 813-30.

Fryer, Jr., Roland G. (2011). "Racial Inequality in the 21st Century: The Declining Significance of Discrimination," in David Card and Orley Ashenfelter, eds., Handbook of Labor Economics, vol. 4b. Amsterdam: North Holland, pp. 855‑971.

Marrero, Gustavo, and Juan Rodrìguez (2013). "Inequality of Opportunity and Growth," Journal of Development Economics, vol. 104 (September), pp. 107-22.

Ritter, Joseph A., and Lowell J. Taylor (2011). "Racial Disparity in Unemployment," Review of Economics and Statistics, vol. 93 (February), pp. 30-42.

Semega, Jessica L., Kayla R. Fontenot, and Melissa A. Kollar (2017). "Income and Poverty in the United States: 2016 (PDF)," Current Population Reports, pp. 60-259. Washington: U.S. Census Bureau, September.

Yellen, Janet L. (2015). "So We All Can Succeed: 125 Years of Women's Participation in the Economy," speech delivered at "125 Years of Women at Brown," a conference sponsored by Brown University, Providence, Rhode Island, May 5.

1. I am grateful to Amanda Roberts and Christopher Smith for their assistance in preparing this text. The remarks represent my own views, which do not necessarily represent those of the Federal Reserve Board or the Federal Open Market Committee. Return to text

2. See Bayer and Rouse (2016). Return to text

3. The FOMC's Statement on Longer-Run Goals and Monetary Policy Strategy is available on the Board's website at https://www.federalreserve.gov/monetarypolicy/files/fomc_longerrungoals.pdf. Return to text

4. For evidence on the relationship between monetary policy and labor market disparities between some demographic groups, see Carpenter and Rodgers (2004). Return to text

5. For more on inequality of opportunity see Marrero and Rodriquez (2013). Return to text

6. Staff calculations from forthcoming SCF data (to be released on September 27); for additional analysis of these data, see Bricker and others (forthcoming). Return to text

7. See Bernstein (2013) and Alichi, Kantenga, and Solè (2016) for more on the potential link between income and wealth inequality and consumer spending. Return to text

8. For a discussion of gender disparities, see Yellen (2015). Return to text

9. See Cajner and others (2017) for more on racial gaps and the labor market. Return to text

10. Data on recent estimates of unemployment rates for adult men (20 years and older) by race and ethnicity are available from the Bureau of Labor Statistics. Historical gaps are provided by Cajner and others (2017). Return to text

11. Staff calculations from forthcoming SCF data. Recent estimates of household income from Current Population Survey data and reported by the Census in Semega, Fontenot, and Kollar (2017) are qualitatively similar, in that between 2013 and 2016 for both sets of data, family income has increased for whites, blacks, and Hispanics (with greater increases, in percentage terms, for black and Hispanic families). Return to text

12. Racial and ethnic differences in median income and wealth are somewhat smaller. For example, in 2016 median income for white families was about $61,000, compared with $35,000 for black families and $39,000 for Hispanic families. Median wealth was about $171,000 for white families, compared with about $20,000 for black and Hispanic families. The larger gap in average income and wealth than median income and wealth reflects a greater concentration of income and wealth among the wealthiest white families than for other races and ethnicities. Return to text

13. For example, see Fryer (2011) and Ritter and Taylor (2011). Return to text

14. Further information on these surveys are found on the Board's website; see the Survey of Consumer Finances; the Survey of Household Economics and Decisionmaking; the Survey of Young Workers; and the Survey of Enterprising and Informal Work Activities (PDF). Return to text

15. For information about the Opportunity and Inclusive Growth Institute, see https://www.minneapolisfed.org/institute, for information about the Economic Growth and Mobility Project, see https://www.philadelphiafed.org/egmp, and for information about the America's Workforce Initiative, see https://www.investinwork.org. Return to text