June 01, 2015

What have we learned from the crises of the last 20 years?

Vice Chairman Stanley Fischer

At the International Monetary Conference, Toronto, Canada

There have been many economic and financial crises since the Mexican crisis that began in December 1994. Michel Camdessus, then Managing Director of the IMF, called the Mexican crisis "the first economic crisis of the twenty first century"--by which he meant that it was the first emerging market country crisis whose immediate roots were more in the capital account than in the current account of the balance of payments.

The Mexican crisis was followed by the crises of East Asia, including Thailand, Indonesia and Korea that started in the second half of 1997. The crisis also affected Malaysia, which by imposing capital controls and other measures avoided having to enter an IMF program. The current Japanese crisis began in the 1990s, but was not then seen as a possible forerunner of crises among the industrialized countries of North America and Europe.

The problems of East Asia were followed by crises in Russia, Brazil, Turkey and Argentina. All these took place during the Great Moderation, the moderation being the decline in inflation and greater stability of output that occurred in much of the industrialized world. The Great Moderation was ascribed primarily to the switch in many countries to an inflation targeting approach to monetary policy.

The Mexican crisis began within four months of my joining the IMF. I left the Fund at the end of August 2001, and a few months later the string of crises seemed to be drawing to its close after Argentina abandoned the peg of its peso to the dollar. For a few years it seemed that whatever measures had been put in place to deal with the myriad crises had been successful, as the frequency and intensity of crises declined in the first half of the aughts.

And then, in 2008, came the Great Recession and the Great Financial Crisis in the United States--a once-in-a-century event (one hopes), with deep worldwide repercussions. Nearly seven years after the failure of Lehman Brothers, the economies of the United States, Japan, countries within the Euro zone and other European countries who continue to use their own currencies, among them the United Kingdom, are still struggling to return to sustained growth, two percent inflation rates, and positive real central bank interest rates, and thus to leave behind the imprint of the Great Recession.

I. Learning from Crises

Folk wisdom, policymakers and researchers see opportunities in crises. Everyone is familiar with the notion that one should never waste a crisis. Jean Monnet, among the founders of the European Union, said that "Europe will be forged in crises, and will be the sum of the solutions adopted for those crises."1 European Union and EMU decision-makers have made similar statements in each of their crises, including the present one. And when talking about the present situation, they often conclude by saying "And we will emerge stronger this time too."

Policy economists seek to learn from crises, so that they can do better next time. During the thirty years from 1985 to 2015, I have been involved in a variety of roles in the management of crises, starting from the successful Israeli stabilization program of 1985, during which I was part of a small team advising then Secretary of State, George Shultz, and through the ongoing management of monetary policy in the United States today, where we are engaged in managing the expected exit from the policies adopted by the Fed to deal with the Great Recession.

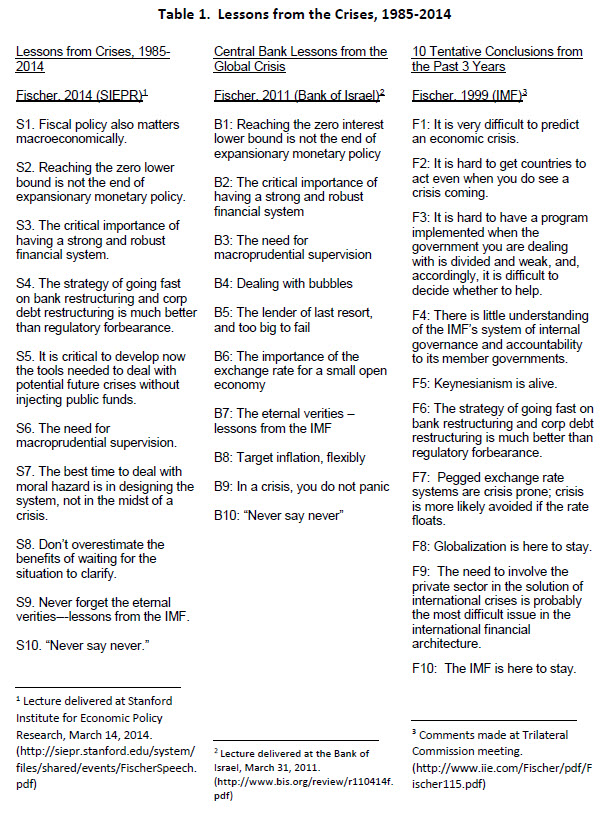

This morning I want to talk about major lessons learned from the economic crises of the last twenty years, many of them crises in which I was involved. I draw on three papers on lessons of crises that I wrote at different stages during that period. The three papers were written in 1999 (when I was at the IMF), 2011 (when I was Governor of the Bank of Israel), and 2014 (when I had been nominated but not yet confirmed as Vice-Chairman of the Fed.)

The ten lessons presented in each paper are summarized in Table 1. Each lesson is numbered, and each bears a letter: F for the 1999 paper (written when I was at the IMF); B for the 2011 paper, when I was at the Bank of Israel; and S for SIEPR2 , where the 2014 paper was presented.

{kind=link}

Each of the lists reflects the concerns of the times and circumstances in which it was written. The 1999 paper was written at a time when the IMF was under criticism for its handling of the many crises with which it had been confronted since 1994. It was a time of far less transparency than today. For instance, in May of 1997 when I paid a secret visit to Thailand to try to gauge the seriousness of their situation, and asked for data on their international reserves, I was told that I could get them--on condition I not pass them on to anyone else in the Fund. This was an offer I had no difficulty in refusing.

In addition to lessons in the 1999 paper relating to the Fund, it is clear from the conclusions presented in F5 (Keynesianism), F6 (bank and debt restructuring) and F7 (exchange rates) that the Fund had drawn the correct critical lessons on several of the central issues of economic policy. It is also clear from F8 that we were surprised--pleasantly so--that despite the pessimism of many that the Asian crisis spelled the beginning of the end of globalization, we had already concluded that very few countries, if any, intended to withdraw from the international economic system.

The 2011 paper reflects lessons both about policy--especially the critical role of the exchange rate for small open economies--and about crisis management, some of which I learned from my experience as Governor of the Bank of Israel. Both B9 (don't panic in a crisis) and B10 are rules of behavior for those managing economic crises, or indeed any crisis. I included B10, "Never say never" because in a crisis a decision-maker may sometimes find him- or herself having to undertake a policy action that they were sure they would never do and which, furthermore, they dislike doing.

The 2014 paper was written while I was focusing on joining the Fed, and thus includes in S5 and S7 issues that remain on the agenda today. I will return to the issues of moral hazard and too big to fail as I turn next to five major lessons that we should draw from the experiences that lie behind the three columns of Table 1.

II. The Main Lessons.

I will focus on five major issues, leaving the most important--lessons relating to the financial system and its regulation and supervision--to the last.3

Lesson T1: Monetary policy at the Zero Lower Bound.4 Before the Great Recession, textbooks used to say that once the central bank interest rate had reached zero, monetary policy could not be made more expansionary--otherwise known as the liquidity trap. The argument was that the central bank could not reduce the interest rate below zero, since at a zero interest rate people could hold currency, on which the nominal interest rate is zero--which implies that the nominal interest rate could not decline below zero.

Almost immediately after the collapse of Lehman Brothers, the Fed began to undertake policies of Quantitative Easing (QE), in two forms: first, by buying assets of longer duration on a large scale, thus lowering longer term rates and making monetary policy effectively more expansionary; and second, by operating as market maker of last resort in markets that in the panic had seemed to stop working--for example, the commercial paper market.

Did these policies work? The econometric evidence says yes. So does the evidence of one's eyes. For instance, the recent inauguration of the ECB's QE policy seemed to have an immediate effect not only on European interest rates, but also on longer-term rates in the United States.

More recently, policymakers in several jurisdictions have discovered that zero is not the lower bound on interest rates. The reason is that it is not costless to hold currency: there are costs of storage, and insurance costs to cover the potential for theft of or damage to the currency. We do not know how low the interest rate can go--but do know that it can go below zero. Whether it can be reduced much below minus one percent remains to be seen--and many would prefer that we don't go there.5

Lesson T2: Monetary policy in normal times.6 In normal times, monetary policy should continue to be targeted at inflation and at output or employment.7 Typically, central bank laws also include some mention of financial stability as a responsibility of the central bank. At this stage the institutional arrangements under which different central banks exercise their financial stability mandate vary across countries, and depend to a considerable extent on the tools that the central bank has at its command. It will take time for the advantages and disadvantages of different arrangements to be evaluated and recommendations on what works best to be developed. On paper, the British approach of setting up nearly parallel committees for monetary policy and for macroprudential financial supervision and regulation appears to be a leading model.

Another issue that remains to be settled is that of the possible use of monetary policy, i.e. the interest rate, to deal with financial stability. For instance, for some time several economists--including those working at the BIS--have been urging an increase in the interest rate to restore risk premia to more normal levels. Most central bankers say they would prefer to use macroprudential tools rather than the interest rate for this purpose. While such tools would have the advantage of being directly targeted at the problem that is to be solved, it is not clear that there are sufficiently strong macroprudential tools to deal with all financial instability problems, and it would make sense not to rule out the possible use of the interest rate for this purpose, particularly when other tools appear to be lacking.

Lesson T3: Active fiscal policy.8 There is a great deal of evidence that fiscal policy works well, almost everywhere, perhaps especially well when the interest rate is at its effective lower bound. Because the lags with which fiscal policy affects the economy may be relatively long (particularly the "decision lag", the lag between a situation developing in which fiscal policy should become more expansionary and the decision to undertake such a policy), automatic stabilizers can play an important stabilizing role.

Another important fiscal policy discussion is currently taking place in the United States. Infrastructure in the United States has been deteriorating, and government borrowing costs are exceptionally low. Many economists argue that this is a time at which fiscal policy can be made more expansionary at low real cost, by borrowing to finance a program to strengthen the physical infrastructure of the American economy. This would mean a temporary increase in the budget deficit while the spending takes place. That spending would have positive benefits--both an increase in aggregate demand as the infrastructure is built, and later an increase in aggregate supply as the positive impact of the increase in the capital stock due to the investment in infrastructure comes into effect--that under current circumstances would outweigh the costs of its financing.

More generally, the case for more expansionary fiscal policy has always to take into account the consequences of greater debt on future interest rates and on the flexibility of future fiscal policy. In this regard, government intervention to save banks has in some countries resulted in massive increases in the size of the government debt as a share of GDP, as in Ireland at the start of the Great Financial Crisis, when the Irish government stepped in to guarantee bank liabilities. This process is aptly known as a "doom loop".

Lesson T4: The lender of last resort, TBTF, and moral hazard.9 The role of the central bank as lender of last resort is a central theme in Walter Bagehot's 1873 classic on central banking, Lombard Street. The case for the central bank to be the lender of last resort is clear in the case of a liquidity crisis--one that arises from a temporary shortage of liquidity, typically in a financial panic--but less so in the case of solvency crises.10

In principle the distinction between liquidity and solvency problems should guide the actions of the central bank and the government in a financial crisis. But in a crisis, the distinction between illiquidity and insolvency is rarely clear-cut--and whether a company goes bankrupt will depend on how the authorities respond to the crisis.

Further, one has to be clear about which aspects of government actions are critical in this regard. If a firm is bankrupt, it may well be optimal for the firm to continue to operate while being reorganized, as typically happens in bankruptcies. In such a case, in which the firm's capital is negative, the ownership of the bankrupt firm should be changed--unless the owners succeed in mobilizing more capital, in which case the company was probably not bankrupt.

If the government is dealing with a bank, or other financial institution, with an extremely large balance sheet and multiple interactions with the rest of the financial system, putting the firm into bankruptcy without a plan to continue its most important activities from the viewpoint of the financial system and the economy, may induce a financial and economic crisis of the order of magnitude that followed the Lehman bankruptcy.

This is where the moral hazard issue arises. If the owners of a company are saved by official actions in circumstances where the company would otherwise have gone bankrupt, it will appear that the government is saving Wall Street at the expense of Main Street. One may argue that saving financial institutions would be good for Main Street. The lender of last resort may well be producing a result that is better for everyone in the economy when it intervenes in a financial crisis. But since the counterfactuals are difficult to establish, and the moral hazard argument is easy to deploy, the public sector may shy away from acting as lender of last resort except in extremis.

Hence the phenomenon of too big to fail. If policymakers reach a point at which they confront a choice between allowing a large and/or systemically interconnected bank to fail without their having reasonable assurance that its essential activities will continue, they may well step in to "save" the financial institution. By "save", I mean, allow the bank to continue to exist and to carry out the functions that are needed to prevent a financial crisis. It is essential to emphasize that this requires a resolution process that does not, and should not, preclude actions to ensure that equity and bond holders lose all or most of the value of their assets, to an extent that depends on circumstances. And the ability to do this depends on the resolution processes for insolvent financial institutions. In this context, the progress that has been made since 2008 in developing effective resolution mechanisms will play a key role in dealing with the too big to fail problem by significantly reducing the probability of a bank being too big to fail.

This is a good point at which to turn to the regulation and supervision of the financial system.

Lesson T5: Regulation and supervision of the financial system.11 The natural and sensible reaction to the problem that the central bank and the government face when the dark clouds of a massive financial crisis appear on the horizon, is to make two sets of decisions. The first relates to its immediate actions and the short run, where the goal should be to intervene in a way that prevents the massive crisis, at minimum future cost to the economy and the society. The second is for the longer run, to rebuild the financial system in such a way that the probability of having to confront such a situation again is reduced to a very low level. Hence regulations should be strengthened, essentially as they have been recently, through the activities of governments, legislators, and regulators in most countries. In the case of the United States, most of the important changes have been introduced though the Dodd-Frank Act, and they have been supplemented by decisions of the regulators and the supervisors.

We are now at a difficult point. Regulations have been strengthened and the bankers' backlash is both evident and making headway. Of course, there should be feedback from the regulated to the regulators, and the regulated have the right to appeal to their legislators. But often when bankers complain about regulations, they give the impression that financial crises are now a thing of the past, and furthermore in many cases, that they played no role in the previous crisis.

We should not make the mistake of believing that we have put an end to financial crises. We can strengthen the financial system, and reduce the frequency and the severity of financial crises. But we lack the capacity of imagining, anticipating and preventing all future financial sector problems and crises. That given, we need to build a financial system that is strong enough to withstand the type of financial crisis we continue to battle. We can take some comfort--but not much--from the fact that this crisis was handled much better than the financial crisis of the Great Depression. But it still imposed massive costs on the people of the United States and those of other countries that were badly hit by the crisis.

No-one should underestimate the costs of the financial crisis to the United States and the world economies. We are in the seventh year of dealing with the consequences of that crisis, and the world economy is still growing very slowly. Confidence in the financial system and the growth of the economy has been profoundly shaken. There is a lively discussion going on at present as to whether we have entered a period of secular stagnation as Larry Summers argues, or whether we are seeing a more frequent phenomenon--that recessions accompanied by financial crises are typically deep and long, as Carmen Reinhart and Ken Rogoff's research implies. Ken Rogoff calls this a "debt supercycle".

It may take many years until we know the answer to the question of whether we are in a situation of secular stagnation or a debt supercycle. Either way, there is now growing evidence that recessions lead not only to a lower level of future output, but also to a persistently lower growth rate. Some argue that it was the growth slowdown that caused the financial crisis. This is a hard position to accept for anyone who has looked closely at the behavior of the financial system in the middle of the last decade.

We need to remind ourselves that the principle underlying Basel II was that the private sector would manage risk efficiently and effectively, since the last thing a bank would want would be to fail. That did not work out as predicted. A possible reason is that incentives are misaligned. One sees massive fines being imposed on banks. One does not see the individuals who were responsible for some of the worst aspects of bank behavior, for example in the Libor and foreign exchange scandals, being punished severely. Individuals should be punished for any misconduct they personally engaged in.

One reason we should worry about future crises is that successful reforms can breed complacency about risks. To the extent that the new regulatory and supervisory framework succeeds in making the financial system more stable, participants in the system will begin to believe that the world is more stable, that we suffered a once in a century crisis, and that the problems that led to it have been solved. And that will cause them to take more risks, to exercise less caution, and eventually, to forget the seriousness of the problems we are confronting today and will confront in the future.

This is a process that will one day lead to an unhappy result. You, the regulated, and we, the regulators, will have to work very hard, for a very long time, and then keep on working hard, to reduce the frequency and magnitude of those future crises.

Thank you.

1. See Jean Monnet (1976), Memoires, (Paris: Fayard). Return to text

2. Stanford Institute for Economic Policy Research. Return to text

3. The lesson numbers in this paper are preceded by the letter "T" for Toronto. Return to text

4. This appears in Table 1 as B1 and S2. Return to text

5. There are fascinating issues about how a hypothetical monetary system without currency would operate, and what interest rates the central bank should attempt to control in such a situation--but we will have to leave those issues for another occasion. Return to text

6. This is topic B8 in Table 1. Return to text

7. In most modern central bank laws, the central bank's policy goals include both inflation and a measure of economic activity, although more often than not, the inflation goal is defined as more important than the output or employment goal. By contrast, the Fed has a dual mandate that gives equal weight to both inflation and employment. I believe that in practice almost all central banks give approximately equal weight to their inflation and employment or output goals. Return to text

8. This issue appears in Table 1 as S1 and F5. Return to text

9. These issues are discussed in S5, S7 and B5. Return to text

10. I am quoting here from my 2011 paper, "Central bank lessons from the global crisis." (http://www.bis.org/review/r110414f.pdf ) Return to text

11. These issues are discussed in S3, S4, S6, B2, B3, and F6. Return to text