May 12, 2023

On the Assessment of Current Monetary Policy

At the "How to Get Back on Track: A Policy Conference," Hoover Institution, Stanford, California

Good afternoon, everyone. Thank you to the organizers for inviting me to speak. It is a pleasure to be here. I welcome hearing diverse views on how to best conduct monetary policy, and this conference is certainly providing an invigorating debate on that topic.

Before I begin, I want to address quickly some news from this morning. I am deeply honored by the trust President Biden and Vice President Harris have shown me with the nomination to be the next Vice Chair of the Board. I am humbled by this extraordinary opportunity and thankful to my colleagues, friends, and family for their support.

Turning back to the conference, as I join this debate, let me remind you that the views I will express today are my own and are not necessarily those of my colleagues in the Federal Reserve System.

Introduction

The title of the conference "How to Get Back on Track: A Policy Conference" is potent. Its intent and ambiguity are striking. First, the title presupposes that U.S. monetary policy is currently on the wrong track. Second, the webpage for this conference advances a puzzling definition of the phrase "on track." How so? According to the Hoover webpage, "A key goal of the conference is to examine how to get back on track and, thereby, how to reduce the inflation rate without slowing down economic growth" (emphasis added).1 As this audience knows, there are macroeconomic models that permit disinflation with no slowdown in economic growth, but the assumptions underlying these models are very strong.2 It's not clear, at least to me, why such a strict metric would be used to assess real-world monetary policymaking. Third, the definition of "on track" in the title contrasts with more commonplace definitions such as "achieving or doing what is necessary or expected," as offered by a standard reference such as the Merriam-Webster dictionary.3 My view is that this commonplace definition provides a more practical lens through which to assess real-world policymaking.

Against this semantic backdrop, I will begin my remarks with my perspective on the current inflation and economic situation. Then, I will consider credit conditions in response to the recent bank stress events. Next, I will offer some normative thoughts about strategic monetary policymaking in highly uncertain environments. Finally, I will argue that if you are willing to widen your lens to include a more commonplace definition, then it is possible to conclude that current monetary policy is, in fact, "on track."

Current Inflation in the U.S.

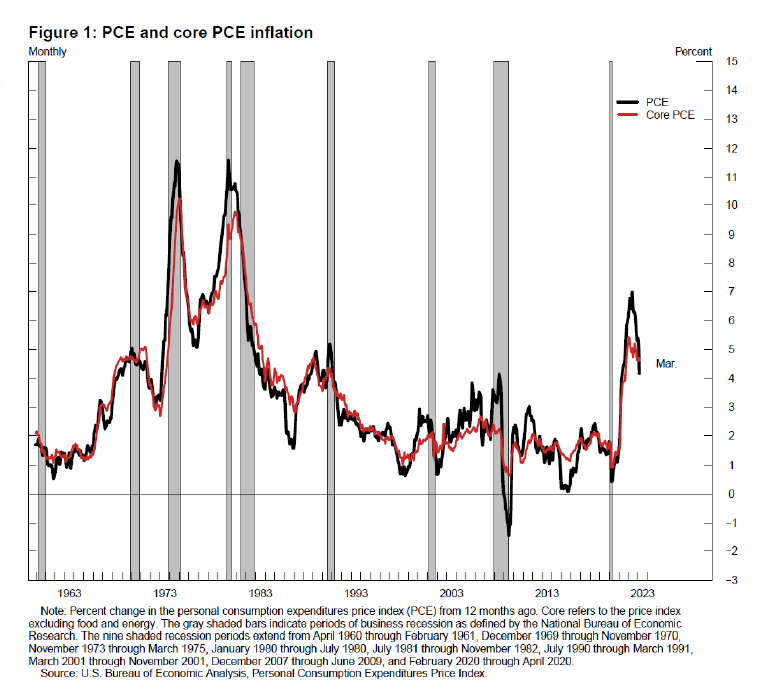

Current inflation is still high. Figure 1 illustrates this point. Personal consumption expenditures (PCE) inflation, the black line, stands at 4.2 percent, and core PCE inflation, the red line, stands at 4.6 percent for year-end March 2023.

{kind=link}

Overall, news on inflation so far this year has been mixed. The good news is that food and energy prices both fell in March, and total PCE inflation slowed to 4.2 percent from 5 percent in February. Since peaking last June, inflation has declined about 2.75 percentage points—with nearly all the step-down explained by falling energy prices and slowing food prices. The bad news is that there has been little progress on core inflation.

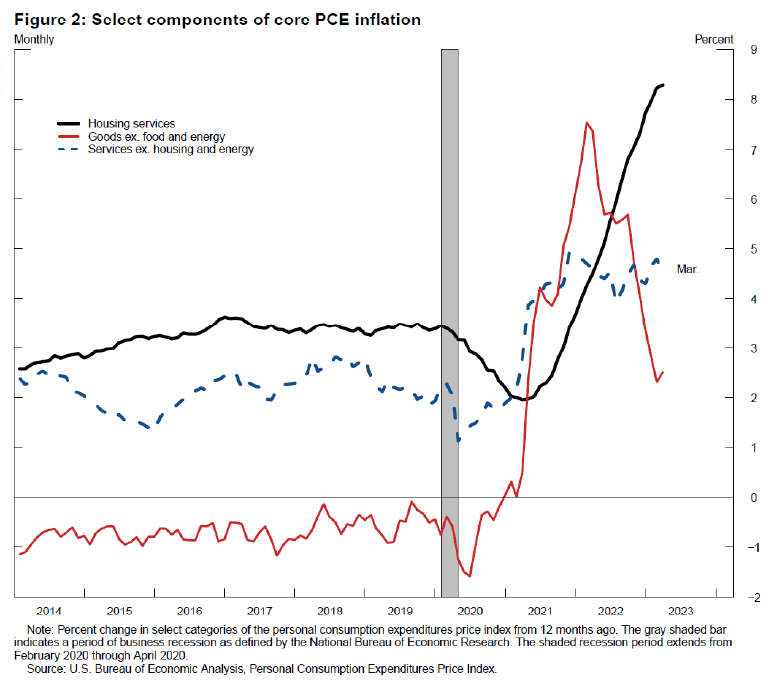

To understand why, I find it useful to separately analyze three large categories that together make up core PCE: goods excluding food and energy, the red line in figure 2; housing services, the black line; and services excluding housing and energy, the blue dashed line. The drivers of inflation in each of these sectors differ somewhat and understanding the different causes and how they affect the different components can help predict the future course of inflation.

Core goods inflation, the red line in figure 2, has come down since its peak of 7.6 percent in February 2022, but the most recent news has been discouraging. Outside of used motor vehicle prices, which fell unexpectedly in March, disinflation in core goods prices is occurring at a slower pace than expected. Supply and demand imbalances in the goods sector seem to be resolving less quickly than expected. Core housing services inflation, the black line in figure 2, surged over the past couple of years as demand in the housing sector underwent a major shift during the pandemic. The latest monthly readings have started to slow, though that is not yet evident in the 12-month changes shown in figure 2. The recent slowing was presaged by a flattening out of rents on new leases to new tenants since the middle of last year. In contrast, core services excluding housing inflation, the blue dashed line in figure 2, has not shown much sign of slowing.

{kind=link}

Labor Market and GDP Growth

Turning to labor markets, the April 2023 employment report data continue to point to a strong labor market amid improvements in labor supply, with the prime-age labor force participation rate exceeding its pre-pandemic level. Wage growth has continued to run ahead of the pace consistent with 2 percent inflation and current trends in productivity growth. Wage gains are welcome as long as they are consistent with price stability. Over the 12 months ended in March 2023, the employment cost index (ECI) for total hourly compensation for private-sector workers rose 4.8 percent, down only a little from its peak of 5.5 percent last June.

Despite strong growth in consumption spending, gross domestic product (GDP) grew modestly at an annual rate of 1.1 percent in the first quarter of 2023 as inventory investment slowed down substantially, similar to the below-trend pace of growth in 2022. Looking ahead, last quarter's growth in consumer spending seems unsustainable. Indeed, after rising very steeply in January 2023, consumer spending ticked down in February and was flat in March. Moreover, I expect slower consumer spending growth over the remainder of the year in response to tight financial conditions, depressed consumer sentiment, greater uncertainty, and declines in overall household wealth and excess savings.

Recent Stress in the Banking Sector

The tightening in financial conditions we have seen in response to our monetary policy actions is likely to be augmented by the effects on credit conditions from recent strains in the banking sector. The U.S. banking system is sound and resilient. The Federal Reserve, working with other agencies, has taken decisive actions to protect the U.S. economy. Nevertheless, it is reasonable to expect that recent stress events will lead banks to tighten credit standards further.4 Even though it is too early to tell, my view is that these incremental credit restraints will have a mild retardant effect on economic growth because the recent bank failures were isolated and addressed swiftly by aggressive macro- and micro-prudential policy actions.

Nevertheless, I acknowledge that there is significant uncertainty around the amount of tightening of credit conditions in the coming year in response to the bank stress and the magnitude of the effect that tightening might have on the U.S. economy. Therefore, there is some downside risk that the incremental effect of the credit shock is larger than I expect.

Monetary Policymaking and Current Uncertainties

The pandemic aftermath, geopolitical instability, and banking-sector stress have contributed to a highly uncertain economic environment. Additionally, the numerous post-pandemic "surprises" in inflation, employment, and economic growth suggest that the underlying structure of the U.S. economy may be in flux. More simply, the data-generating process for the post-pandemic U.S. macroeconomy is less clear.

Due to the proximity of the pandemic and its unprecedented disruptions of economic and social activity, there are currently insufficient post-pandemic data to identify the parameters and stable relationships that characterize the possible new structure of the economy. Given this observation, what is a reasonable monetary policymaking strategy? The answer to this question is likely to be different for each monetary policymaker.

I want to share with you a few strategic principles that are important to me. First, policymakers should be ready to react to a wide range of economic conditions with respect to inflation, unemployment, economic growth, and financial stability. The unprecedented pandemic shock is a good reminder that under extraordinary circumstances it will be difficult to formulate precise forecasts in real time. Our dual mandate from the Congress is especially helpful here. It provides the foundation for all our policy decisions. Second, policymakers should clearly communicate monetary policy decisions to the public. Our commitment to transparency should be evident to the public, and monetary policy should be conducted in a way that anchors longer-term inflation expectations. Third—and this is where I am revealing my passion for econometrics—policymakers should continuously update their priors about how the economy works as new data become available. In other words, it is appropriate to change one's perspective as new facts emerge. In this sense, I am in favor of a Bayesian approach to information processing.

While these principles do not constitute a complete monetary policymaking framework, I think they are useful when thinking about features of such frameworks.

Conclusion

By way of concluding, I would like to return to the question of whether current monetary policy is "on track" but allow for the wider defining lens of "achieving or doing what is necessary or expected." The national unemployment rate was 3.6 percent in March 2022 when the current monetary policy tightening cycle began. Today, after 500 basis points of tightening of the policy rate, the national unemployment rate stands at a near-record low of 3.4 percent. At its recent peak, total PCE inflation was 7 percent in June 2022. Currently, it is 4.2 percent in March 2023. Is inflation still too high? Yes. Has the current disinflation been uneven and slower than any of us would like? Yes. But my reading of this evidence is that we are "doing what is necessary or expected" of us. Furthermore, monetary policy affects the economy and inflation with long and varied lags, and the full effects of our rapid tightening are still likely ahead of us. We are balancing the directives of the dual mandate given to us by the U.S. Congress. This is not an easy task in these uncertain times, but I can assure you that I and my colleagues on the FOMC take it quite seriously and with great humility. It is in this sense that I believe that we are well "on track."

Thank you.

References

Croushore, Dean (1992). "What Are the Costs of Disinflation?" (PDF) Federal Reserve Bank of Philadelphia, Business Review, May/June, pp. 3–15.

Goodfriend, Marvin, and Robert G. King (2005). "The Incredible Volcker Disinflation," Journal of Monetary Economics, vol. 52 (July), pp. 981–1015.

Sargent, Thomas J. (1982). "Stopping Moderate Inflations: The Methods of Poincare and Thatcher," in Rudiger Dornbusch and Mario Henrique Simonsen (eds.), Inflation, Debt, and Indexation (Cambridge, Mass.: MIT Press), pp. 54–96.

Tetlow, Robert J. (2022). "How Large Is the Output Cost of Disinflation?" Finance and Economics Discussion Series 2022-079 (Washington: Board of Governors of the Federal Reserve System, November).

1. See the conference's webpage at www.hoover.org/events/how-get-back-track-policy-conference. Return to text

2. Estimates of the cost of disinflation depend on the model used to measure it. Classical models, in which rational expectations play a dominant role in determining the cost of disinflation, show low cost, while Keynesian models, in which slack in the economy is needed to reduce inflation, show high cost. See, for example, Sargent (1982), Croushore (1992), Goodfriend and King (2005), and Tetlow (2022) for a comparison of the cost of disinflation across macroeconomic forecasting models. Return to text

3. See the definition for "track" at https://www.merriam-webster.com/dictionary/on%20track. Return to text

4. The April 2023 Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) shows that banks, especially small and midsize banks, reported further tightening in credit standards on loans to businesses and households over the past three months, following widespread tightening in previous quarters. The April 2023 SLOOS is available on the Board's website at https://www.federalreserve.gov/data/sloos/sloos-202304.htm. Return to text