November 13, 2012

Revolution and Evolution in Central Bank Communications

Vice Chair Janet L. Yellen

At the Haas School of Business, University of California, Berkeley, Berkeley, California

Thank you. I'm delighted to be back at Haas, which I've been proud to call home for much of my career. I'd like to thank Dean Lyons for inviting me to speak to you this afternoon.1

My subject is the recent revolution and continuing evolution in communication by central banks. All of us, of course, live in an era of revolutionary advances in communication: If I succeed in saying anything interesting this afternoon, those words may be posted, tweeted, and blogged about even before I've left this podium. So, it might seem unsurprising that the Federal Reserve, too, is bolstering its efforts at communication.

But the revolution in central bank communication is not driven by technological advances. Rather, it is the product of advances in our understanding of how to make monetary policy most effective. A growing body of research and experience demonstrates that clear communication is itself a vital tool for increasing the efficacy and reliability of monetary policy. In fact, the challenges facing our economy in the wake of the financial crisis have made clear communication more important than ever before. Today I'll discuss the revolution in thinking about central bank transparency and how, pushed by the unique situation precipitated by the financial crisis, the Federal Reserve has responded with fundamental advances in communication. Indeed, I hope that one of the legacies of this difficult period is a permanent and substantial advance in Federal Reserve transparency, building on the policies I'll talk about shortly.

As you all know, the Federal Reserve is actively promoting a faster recovery. Our efforts are hampered by the fact that our standard policy tool, the federal funds rate, is near zero and cannot be reduced much further. In this extraordinary environment, the Federal Reserve is employing two unconventional policy tools to spur job creation and growth: large-scale asset purchases, which some people call quantitative easing, and communications about the future course of monetary policy, also known as forward guidance.

At the Federal Open Market Committee's (FOMC) meeting in September, the FOMC--the Federal Reserve's principal monetary policymaking body--employed both of these unconventional tools. The Committee initiated a new large-scale asset purchase program to buy mortgage-backed securities (MBS). In addition, with regard to forward guidance, the Committee said that, first, it intends to continue buying MBS and other assets until it sees a substantial improvement in the outlook for the labor market.2 Second, the Committee stated that it expects a highly accommodative stance of monetary policy to remain appropriate for a considerable time after the economic recovery strengthens. And third, the Committee noted that it currently expects to hold the federal funds rate at exceptionally low levels at least through mid-2015, about a half-year longer than previously announced.

The three elements of forward guidance that were adopted by the FOMC in September 2012 would have been unthinkable in 1992 and greatly surprising in 2002, but they have, in my view, become a centerpiece of appropriate monetary policy. To better explain my views regarding the FOMC's forward guidance, I will first discuss how it fits into the Committee's broader thinking and communication about monetary policy. The FOMC took a major step to explain this thinking last January when it issued for the first time a "Statement of Longer-Run Goals and Policy Strategy."3 This statement provides a concise description of the FOMC's objectives in conducting monetary policy and the approach the Committee considers appropriate to achieve them. I will present my views on the implications of this statement for monetary policy in current circumstances. I will then discuss several approaches the FOMC has recently considered to enhance its communications to make its policy more effective in this challenging situation. Let me emphasize that the views I express here are my own and do not necessarily represent those of my colleagues in the Federal Reserve System.

The Case for Central Bank Transparency

To fully appreciate the recent revolution in central bank communication and its implications for current policy, it is useful to recall that for decades, the conventional wisdom was that secrecy about the central bank's goals and actions actually makes monetary policy more effective. In 1977, when I started my first job at the Federal Reserve Board as a staff economist in the Division of International Finance, it was an article of faith in central banking that secrecy about monetary policy decisions was the best policy: Central banks, as a rule, did not discuss these decisions, let alone their future policy intentions. While the Federal Reserve is required by the Congress to promote stable prices and maximum employment, Federal Reserve officials at that time avoided discussing how policy would be used to pursue both sides of this mandate. Indeed, mere mention of the employment side of the mandate, even by the mid-1990s, was described in a New York Times article as the equivalent of "sticking needles in the eyes of central bankers."4

This secretiveness regarding monetary policy decisions clashed with the openness regarding government decisions expected in a democracy, especially since Federal Reserve decisions influence the lives of every American. And there were critics within the economics profession. James Tobin and Milton Friedman, both Nobel laureates, disagreed on almost every aspect of monetary policy, but they were united in arguing that transparency regarding central bank decisions is vital in a democracy to lend legitimacy to policy decisions.5 Surely only some important societal interest requiring opacity could justify the traditional practice. Indeed, in 1975 a citizen demanding greater openness sued the FOMC to obtain immediate release of the policy directive upon its adoption, and in 1981 the case was resolved in favor of deferred disclosure.6

Ironically, while this transparency lawsuit was wending its way through the courts, Robert Lucas and others were publishing research that would garner several Nobel prizes and ultimately overturn the traditional wisdom that secrecy regarding policy actions was the best policy.7 A key insight of these scholars was that monetary policy affects employment, incomes, and inflation to a large extent through its effects on the public's expectations about future policy. Many spending decisions, such as financing the purchase of a home or businesses' capital expenditures, depend on longer-term interest rates that are connected to monetary policy through expectations of short-term interest rates over the lifetime of a mortgage or an investment project. In other words, the effect of monetary policy on the economy today depends not only, or even primarily, on the FOMC's current target for the federal funds rate or the quantity of assets on its balance sheet, but rather on how the public expects the Federal Reserve to set the paths of these variables in the future. These expectations influence longer-term interest rates and asset prices as well as the public's views concerning the likely future paths of income and inflation.

The history of oil price shocks is a good example to illustrate this point. In the 1970s, two large oil price shocks led to sharp increases in general inflation that were not met with prompt inflation-fighting actions by the Federal Reserve. This delay left the public unsure whether the Federal Reserve would act to reverse the increase in inflation, and expectations of longer-term inflation ratcheted up. When the Federal Reserve eventually did act to bring inflation down from double-digit levels, the consequence was the painful recession of 1981 and 1982.

The effects of that policy shift were severe, but the decision helped change expectations of the Federal Reserve's commitment to price stability, and thereby ultimately led to longer-run inflation expectations becoming anchored at their current low levels. As a result, a series of large increases in oil prices starting in 2005 did not unleash a general rise in inflation or longer-term inflation expectations. The public seemed to correctly perceive that the Federal Reserve would not allow an oil price shock to precipitate a general rise in inflation. Longer-term inflation expectations remained well anchored, and hence no aggressive and recessionary disinflation action by the Federal Reserve was required. Thus, over the quarter century up to the mid-2000s, the Federal Reserve established a record of policymaking that allowed the public to predict monetary policy responses to unforeseen events such as an oil price shock with reasonable accuracy.

Unfortunately, recent events have made it harder for the public to predict the future course of monetary policy. Economic weakness since the financial crisis and the Great Recession has confounded hopes for a speedy recovery and has required unprecedented monetary policy actions. Shortly after the financial crisis erupted, the Federal Reserve reduced the federal funds rate to almost zero and launched a number of temporary liquidity and credit programs to keep the financial system operating. Even these aggressive policy responses, however, were not enough to halt the contraction, and further action was needed to stop the economy from falling into a second Great Depression. To this end, the Federal Reserve started to expand its balance sheet through purchases of longer-term Treasury securities and agency debt and MBS in an effort to put further downward pressure on long-term interest rates and so stimulate the economy.

With the federal funds rate near zero, and the Federal Reserve deploying the new tool of large-scale asset purchases, it became much more difficult for the public to anticipate how the FOMC would likely conduct policy over time, and how the overall stance of monetary policy would both affect and respond to economic conditions. In this situation, the FOMC began to rely heavily on forward guidance about both the likely future path of the federal funds rate and the Committee's intentions concerning asset purchases and sales.8 But, for this guidance to have its maximum effect, it must be understood and believed by the public, and therefore provide the public with a solid basis for forming their borrowing and spending decisions today.9 In my view, such credibility can be achieved only if the public understands the FOMC's objectives and intentions.

Communications after the Financial Crisis

Chairman Bernanke asked me to take up these challenges in 2010 as chair of a new FOMC communications subcommittee.10 Central bank transparency had long been an issue of great interest to both of us, and the Chairman had been an exceptionally strong voice for central bank transparency in his academic work and in his earlier service on the Board of Governors. Throughout the Chairman's term, the FOMC has made important strides in transparency through actions such as introducing the Committee's quarterly Summary of Economic Projections (SEP), which provides information about participants' forecasts for the economy under their individual views concerning appropriate policy and their longer-run assessments of potential output growth, the "normal" unemployment rate, and the most appropriate inflation rate.

A high priority for the Chairman was to further clarify the FOMC's interpretation of the long-term objectives implied by its dual mandate to promote maximum employment and stable prices. While we had made progress, as I just noted, during the years preceding the crisis, the FOMC as a body had never provided an explicit description of its policy goals beyond quoting its mandate. We saw further clarification of these objectives as important for the sake of transparency and accountability. But beyond that, an explicit statement of goals had become essential for the Committee to achieve its monetary policy objectives in the aftermath of the crisis, including allowing heavier reliance than in the past on forward guidance on the future path of policy.

A particular concern, given that the crisis had ushered in a prolonged period of elevated unemployment, was that the weakness in the economy might push inflation well below 2 percent, a level that many took to be an implicit target of the FOMC. There was even an ongoing risk that low inflation might turn to deflation and further hamper growth. These challenges led to legitimate questions among forecasters and the public about just what the FOMC meant by "maximum employment" and "stable prices."

The FOMC could have chosen to adopt an "inflation-targeting framework," in which it would have specified an objective solely for inflation, without any explicit reference to employment. Such an approach has been adopted by a large number of central banks since the 1990s. While the FOMC had debated adopting an inflation target on a number of occasions since the mid-1990s, some Committee members believed that stating an explicit target for inflation alone would undermine the maximum-employment side of the dual mandate. In fact, some central banks that have been assigned a single mandate of inflation stabilization have struggled to explain how the goals of growth and financial stability figure into their inflation-targeting framework.11

A Consensus on Monetary Policy Goals

Last January, the FOMC took a major step to clarify its interpretation of its dual mandate, issuing the "Statement of Longer-Run Goals and Monetary Policy Strategy" that I mentioned earlier. Unlike the regular postmeeting statements, which are intended to remain current only until the next FOMC meeting, this statement is meant to be a more enduring expression of the FOMC's policy objectives and how it plans to pursue them. The intention is that the public can count on the principles expressed in the statement to remain unchanged for some time to come, even as the economic outlook changes. For that reason, the Committee sought the endorsement of all its participants--the Board members and all 12 Reserve Bank presidents--not only the voting members. My expectation is that this "consensus statement" will be reaffirmed each January, perhaps with minor modifications but with the core principles intact.

Importantly, the consensus statement provides a numerical value--2 percent--for the Committee's longer-run inflation goal. But importantly, it pairs that inflation goal with a specific goal for maximum employment. In particular, the statement cites a range summarizing FOMC participants' estimates of the longer-run normal rate of unemployment. Finally, the statement says that the Committee will follow a "balanced approach" as it "seeks to mitigate deviations of inflation from its longer-run goal and deviations of employment from the Committee's assessments of its maximum level."12

The specification of 2 percent as the Committee's longer-run inflation goal, as measured by the annual change in the price index for personal consumption expenditures (PCE), reflected careful deliberation. The Committee judged that the PCE price index is the most reliable measure of prices that are relevant for households and, in choosing the 2 percent goal, balanced two main considerations. First, any rate of price inflation, whether positive or negative, imposes some costs on society, making planning more difficult and creating distortions in the economy. Second, were the FOMC to aim for zero inflation to eliminate these costs, it would face greater difficulty in providing sufficient monetary accommodation in response to large negative shocks. With inflation at zero, the zero lower bound on nominal interest rates implies that real short-term interest rates cannot be reduced below zero. In contrast, with low but positive inflation, they can be.13 History has shown that sustained periods of even mild deflation can impose immense costs in terms of slow growth and high unemployment.14 Thus, balancing the goal of maximum employment against the costs of modest inflation, the Committee chose 2 percent measured inflation as the value it judged likely to provide an adequate buffer against costly deflations while keeping the costs of inflation quite small.

Given that the rate of inflation over the longer run is determined solely by monetary policy, central banks can, and indeed must, determine the long-run level of inflation. In contrast, they cannot do much to affect the maximum sustainable level of employment. That level is determined by factors affecting the structure and dynamics of the labor market that are almost completely outside the control of the central bank. Nonetheless, the Committee felt strongly that it should provide some quantitative interpretation of economic conditions consistent with the maximum employment portion of the Fed's mandate. Failure to do so might be seen as elevating the inflation side of the dual mandate above the employment side. The Committee chose to couch the longer-run employment objective in terms of the rate of unemployment while indicating that other indicators may also be relevant in assessing the maximum level of employment. Unfortunately, there is a considerable range of disagreement in the economics profession and on the FOMC itself about what this longer-run normal rate of unemployment is. Moreover, there is widespread recognition that whatever the normal rate might be today, it can change over time. So the consensus statement notes that, as of January 2012, FOMC participants' estimates of this rate had a central tendency of 5.2 percent to 6.0 percent. I expect the FOMC to review its estimates of the longer-run normal rate of unemployment in its annual reaffirmation of the consensus statement on goals and strategy.

Setting Longer-Run Objectives and Minimizing Shorter-Run Fluctuations

As I mentioned before, stating longer-run goals is only one part of clarifying the dual mandate. The other part involves explaining how the FOMC will conduct policy to attain its longer-run objectives over time. Because shocks to the economy regularly push inflation and unemployment away from the Committee's objectives, the FOMC must adjust policy to mitigate such deviations from its goals. We can therefore think of two tasks for monetary policymakers: first, setting policy to pursue the longer-run objectives; and second, adjusting policy in response to shocks to minimize shorter-run fluctuations around those objectives.

Clarity on longer-run goals, due to the important role of expectations, can itself help reduce short-run fluctuations. In the words of the January consensus statement, "communicating this inflation goal clearly to the public helps keep longer-term inflation expectations firmly anchored, thereby fostering price stability and moderate long-term interest rates and enhancing the Committee's ability to promote maximum employment in the face of significant economic disturbances."15

Put differently, the purpose of providing greater clarity about the FOMC's longer-run inflation goal is to anchor inflation expectations more firmly. These more firmly anchored expectations in turn free the Committee's hand to more actively and effectively stabilize short-run fluctuations in economic activity. The Committee can act in this way because the FOMC can tolerate transitory deviations of inflation from its objective in order to more forcefully stabilize employment without needing to worry that the public will mistake these actions as the pursuit of a higher or lower long-run inflation objective. The instability of inflation, inflation expectations, and employment in response to the oil price increases of the 1970s vividly illustrates the threat posed by price shocks when longer-term inflation expectations are not well anchored.

To minimize short-run fluctuations, the FOMC also needs to decide how to respond to shocks that push the economy away from price stability and maximum employment. The goals of stable prices and maximum employment are often complementary: Policymakers need not sacrifice performance on one goal to pursue the other. However, the pursuit of the two sides of the dual mandate can temporarily conflict. For example, returning inflation to its longer-run goal might require, say, a tighter stance of monetary policy, whereas returning the economy to maximum employment might require just the opposite. The consensus statement explains that in such circumstances the FOMC will pursue a balanced approach, taking into account the magnitude of the deviation of each variable from its objective and allowing for the possibility that the deviations may not be eliminated over the same time horizon. The balanced-approach strategy endorsed by the FOMC is consistent with the view that maximum employment and price stability stand on an equal footing as objectives of monetary policy.

As I see it, such a balanced approach has two important implications that deserve emphasis. The first is that, if the FOMC is doing its best to minimize deviations from its objectives, then, over long periods, both unemployment and inflation will be about equally likely to fall on either side of those objectives. To put it simply, if 2 percent inflation is the Committee's goal, 2 percent cannot be viewed as a ceiling for inflation because that would result in deviations that are more frequently below 2 percent than above and thus not properly balanced with the goal of maximum employment. Instead, to balance the chances that inflation will sometimes deviate a bit above and a bit below the goal, 2 percent must be treated as a central tendency around which inflation fluctuates. The same holds true for fluctuations of unemployment around its longer-run normal rate.

The second property, which to me is the essence of the balanced approach, is that reducing the deviation of one variable from its objective must at times involve allowing the other variable to move away from its objective. In particular, reducing inflation may sometimes require a monetary tightening that will lead to a temporary rise in unemployment. And a policy that reduces unemployment may, at times, result in inflation that could temporarily rise above its target.

Communicating the Economic Outlook and Its Policy Implications

How can we translate the principles embodied in the Committee's consensus statement of longer-run goals and strategy into a concrete plan of action for the current situation? And, having done so, how can we make such a plan understandable to the public? I'll next illustrate a method I use to help me judge the best plan of action at a particular time. I will then describe the communications tools the Committee is now using to explain its strategy and discuss others it is considering to better explain its policy decisions to the public.

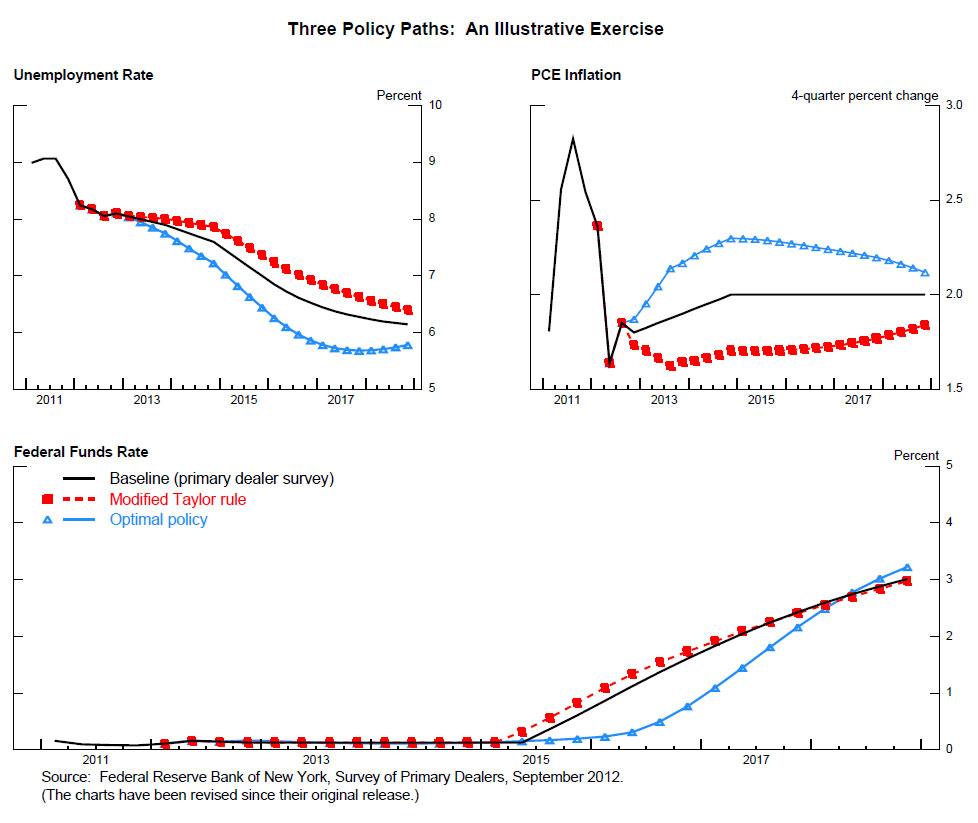

In addition to clearly specified goals, concrete recommendations about appropriate monetary policy require the specification of a baseline outlook for the economy and also a realistic, quantitative model of the economy to assess how monetary policy choices affect the likely paths of the FOMC's goal variables--namely, inflation and the unemployment rate. Figure 1 presents such an outlook, one based on a survey of the Federal Reserve's primary dealers conducted during the week prior to the September FOMC meeting. The baseline paths through 2015 of the unemployment rate and inflation shown by the solid black lines in the upper two panels track the median of the dealers' forecasts of these variables. Beyond 2015, the path assumes that the unemployment rate converges over time to 6 percent--the median forecast of the long-run unemployment rate, which is the upper end of the range of estimates of the longer-run normal unemployment rate cited in the FOMC consensus statement--while the inflation rate settles down at 2 percent, the FOMC's inflation objective and the median long-run forecast in the dealer survey.

{kind=link}

The solid black line in the bottom panel of the figure shows the median of dealers' expectations for the path of the federal funds rate through the end of 2015. The dealers assumed it would remain near zero through the first half of 2015, consistent with the guidance the Committee subsequently provided. Beyond 2015, the federal funds rate is assumed to gradually rise to 4 percent, the long-run value expected by most dealers as well as most FOMC participants. I have assumed in the baseline that this process is largely completed within four years.16

The question I now want to address is whether this illustrative baseline path for the federal funds rate is one that reflects a balanced approach to attaining our longer-run objectives, consistent with our consensus statement. As I noted, this balanced approach means inflation and unemployment will sometimes temporarily deviate from longer-run objectives, but that these deviations would be minimized. To answer this question I need to rely, as I noted, on a specific macroeconomic model, and, for this purpose, I will employ the FRB/US model, one of the economic models commonly used at the Board. The model lets us analyze every possible policy path to see which one yields the best feasible outcome for the paths of unemployment and inflation. Although the exact numerical results of the exercises I am about to report depend on the specific model, the qualitative points that I'll highlight are fairly general.

To derive a path for the federal funds rate consistent with the Committee's enunciated longer-run goals and balanced approach, I assume that monetary policy aims to minimize the deviations of inflation from 2 percent and the deviations of the unemployment rate from 6 percent, with equal weight on both objectives.17 In computing the best, or "optimal policy," path for the federal funds rate to achieve these objectives, I will assume that the public fully anticipates that the FOMC will follow this optimal plan and is able to assess its effect on the economy.18

The blue lines with triangles labeled "Optimal policy" show the resulting paths. The optimal policy to implement this "balanced approach" to minimizing deviations from the inflation and unemployment goals involves keeping the federal funds rate close to zero until early 2016, about two quarters longer than in the illustrative baseline, and keeping the federal funds rate below the baseline path through 2018. This highly accommodative policy path generates a faster reduction in unemployment than in the baseline, while inflation slightly overshoots the Committee's 2 percent objective for several years.

This path illustrates one of the key features of optimal policy under a balanced approach to the dual mandate. Provided that long-term inflation expectations are firmly anchored, the federal funds rate is set to balance the benefits from a faster reduction of the unemployment rate against the losses from a temporary and modest increase of inflation above 2 percent. The more rapid reduction in unemployment along the optimal control path than in the baseline reflects the stimulus to demand provided by lower nominal and real interest rates, higher asset prices, and the expectation of more rapid growth in employment and income.19

The computation of an optimal path for monetary policy is obviously complicated, and, as I'll discuss, it's challenging to communicate. It rests on many assumptions about the outlook for the economy and its structure. An alternative and much simpler approach would entail setting the federal funds rate according to the prescriptions of a policy rule, such as the well-known Taylor rule or a variant. Many studies have shown that, in normal times, when the economy is buffeted by typical shocks--not the extraordinary shock resulting from the financial crisis--simple rules can come pretty close to approximating optimal policies. In fact, empirical research suggests that a modified version of the original Taylor rule fits the behavior of the Fed reasonably well from the late 1980s until the financial crisis. Given that participants in financial markets are familiar with both the FOMC's historical behavior and simple rules, the communications challenges might arguably be less severe if the FOMC followed such a strategy.20 To be sure, I would never advocate turning over monetary policy to a computer, but why shouldn't the FOMC adopt such a rule as a guidepost to policy?

The answer is that times are by no means normal now, and the simple rules that perform well under ordinary circumstances just won't perform well with persistently strong headwinds restraining recovery and with the federal funds rate constrained by the zero bound. A further simulation serves to illustrate that such rules would perform relatively poorly at the current time. The red lines with squares labeled "Modified Taylor rule" show the economic outcomes that would be expected if the federal funds rate were set according to the prescriptions of a rule that is similar to the original Taylor rule, with the only difference being that it responds equally to deviations of unemployment and inflation from their respective longer-run values.

The figure shows that this rule would raise the federal funds rate substantially earlier than the optimal path and thereby leads to more protracted deviations of the unemployment rate above its longer-run normal level without any measurable gains in keeping inflation closer to the 2 percent target. In contrast, the optimal policy results in better economic outcomes. In effect, it compensates for the period of economic weakness induced by both the zero lower bound and the unusual persistence and severity of the headwinds now buffeting the economy by holding the federal funds rate lower for longer than the modified Taylor rule, thereby maintaining greater accommodation as the economic recovery takes hold.21

The Future of FOMC Communications

The fact that simple rules aren't as useful in current circumstances as they would be for the FOMC at other times poses a significant challenge for FOMC communications, especially since private-sector Fed watchers have frequently relied on such rules to understand and predict the Committee's decisions on the federal funds rate.22 In particular, private-sector forecasters commonly use such rules to revise their expectations concerning the path of the federal funds rate in response to news that alters their views concerning the outlook for the economy.

Now, however, the federal funds rate may well diverge for a number of years from the prescriptions of simple rules. Moreover, the FOMC announced an open-ended asset purchase program in September, and there is no historical record for the public to use in forming expectations on how the FOMC is likely to use this tool. Thus, the current situation makes it very important that the FOMC provide private-sector forecasters with the information they need to predict how the likely path of policy will change in response to changes in the outlook. While a clear statement of the Committee's goals and the strategy it will use to achieve them was an important and necessary step in this regard, the exercise we've just undertaken illustrates that a host of additional assumptions and information is needed to derive the concrete implications of the consensus statement for the FOMC's policy decisions.

The challenge facing the FOMC now is to devise ways to communicate its policy intentions during a period in which policy will most likely be constrained by the zero bound on short-term rates and asset purchases will be actively used to foster faster growth. I think the existing FOMC postmeeting statement already goes some way in this direction. With respect to the path of the federal funds rate, it offers a date--mid-2015--as the earliest time at which the Committee currently anticipates that liftoff might be warranted. As the simulations illustrate, this date is later than the modified Taylor rule would predict and closer to the predictions of the optimal policy simulation. This later liftoff date is consistent with the Committee's statement that "a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the economic recovery strengthens."23 Moreover, the simulations also suggest that, once liftoff from the zero lower bound occurs, it would be optimal for the federal funds rate to remain for some time below the prescriptions from a rule, such as the modified Taylor rule, that might in the past have provided a good guide to the Committee's action. Finally, with respect to asset purchases, the guidance indicates that, subject to ongoing evaluations of their efficacy and costs, purchases will continue until there is a substantial improvement in the outlook for the labor market in a context of price stability. Importantly, this open-ended plan reflects a goal-oriented approach in which the ultimate quantity of asset purchases will be geared to the attainment of sufficient progress toward the Committee's employment goal.

Could the FOMC go further in enhancing its communications? One logical possibility would be for the Committee to publish forecasts akin to those I've presented in figure 1. That is, the Committee could provide the public with its projections for inflation and the unemployment rate together with what it views as appropriate paths both for the federal funds rate and its asset holdings, conditional on its current outlook for the economy. Over time, these projections would be revised in response to incoming data that alters the Committee's economic outlook or, instead, because the Committee decides to alter its policy stance. Several inflation-targeting central banks, such as those in Sweden and Norway, publish forecasts of this type. Such a forecast could be highly informative, and, in recent months, the FOMC has explored whether it might be achievable. Not surprisingly perhaps, in a Committee of 19 participants with diverse views on the structure of the economy and appropriate policy, a detailed consensus forecast is exceptionally difficult to develop. As an alternative, the FOMC could try to build on the individual projections of macroeconomic variables and policy already included in its quarterly SEP to provide at least some further information about how these individual projections inform the Committee's collective policy judgment. Improvements along these lines are currently under active consideration.24

Another alternative that deserves serious consideration would be for the Committee to provide an explanation of how the calendar date guidance included in the statement--currently mid-2015--relates to the outlook for the economy, which can and surely will change over time. Going further, the Committee might eliminate the calendar date entirely and replace it with guidance on the economic conditions that would need to prevail before liftoff of the federal funds rate might be judged appropriate. Several of my FOMC colleagues have advocated such an approach, and I am also strongly supportive. The idea is to define a zone of combinations of the unemployment rate and inflation within which the FOMC would continue to hold the federal funds rate in its current, near-zero range. For example, Charles Evans, president of the Chicago Fed, suggests that the FOMC should commit to hold the federal funds rate in its current low range at least until unemployment has declined below 7 percent, provided that inflation over the medium term remains below 3 percent. Narayana Kocherlakota, president of the Minneapolis Fed, suggests thresholds of 5.5 percent for unemployment and 2.25 percent for the medium-term inflation outlook. Under such an approach, liftoff would not be automatic once a threshold is reached; that decision would require further Committee deliberation and judgment.

I support this approach because it would enable the public to immediately adjust its expectations concerning the timing of liftoff in response to new information affecting the economic outlook. This market response would serve as a kind of automatic stabilizer for the economy: Information suggesting a weaker outlook would automatically induce market participants to push out the anticipated date of tightening and vice versa.

Perhaps more importantly, the use of inflation and unemployment thresholds would help the public understand whether a shift in the calendar date, assuming that one is still included in the statement, reflects a change in the Committee's economic outlook or, alternatively, a change in its view concerning the appropriate degree of accommodation. Since monetary policy works in large part through the public's perceptions of the FOMC's systematic behavior, this distinction is critical.25

Conclusion

The past few years have seen important changes in the FOMC's communications‑‑innovations that promote the Federal Reserve's accountability to the public. Beyond that, I believe better communication serves to improve the efficacy of monetary policy at a time when the FOMC faces constraints on its ability to provide appropriate support to the economic recovery through the federal funds rate, its traditional policy tool. In my view, we've made progress, but much work remains to be done.

1. I am indebted to members of the Board staff--Jon Faust, Thomas Laubach, and John Maggs--who contributed to the preparation of these remarks. Return to text

2. The September FOMC meeting statement further indicates that the Committee will take account of the likely efficacy and costs of such purchases in determining the size, pace, and composition of its asset purchases. See Board of Governors of the Federal Reserve System (2012), "Federal Reserve Issues FOMC Statement," press release, September 13. Return to text

3. See Board of Governors of the Federal Reserve System (2012), "Federal Reserve Issues FOMC Statement of Longer-Run Goals and Policy Strategy," press release, January 25. I should note that this statement grew out of discussions within the FOMC that date back to the early 1990s. For a proposal from 2003 by the then Governor Bernanke, see Ben S. Bernanke (2003), "Panel Discussion," speech delivered at the 28th Annual Policy Conference: Inflation Targeting Prospects and Problems, Federal Reserve Bank of St. Louis, St. Louis, Missouri, October 17. My own thinking on the issue has evolved over the years; for a snapshot of its state in early 2006, see Janet L. Yellen (2006), "Enhancing Fed Credibility," speech delivered at the Annual Washington Policy Conference Sponsored by the National Association for Business Economics, Washington, March 13. Return to text

4. See Keith Bradsher (1994), "Tough-Decision Time for the Federal Reserve; New Vice Chairman Stirs the Board's Pot," New York Times, September 26, www.nytimes.com/1994/09/26/business/tough-decision-time-for-federal-reserve-new-vice-chairman-stirs-board-s-pot.html?pagewanted=all&src=pm. Return to text

5. See Milton Friedman (1962), "Should There Be an Independent Monetary Authority?" in Leland B. Yeager, ed., In Search of a Monetary Constitution (Cambridge, Mass.: Harvard University Press), pp.219-43; and James Tobin (1992), "Prepared Statement," in The Monetary Policy Reform Act of 1991, hearing before the Subcommittee on International Finance and Monetary Policy of the Committee on Banking, Housing, and Urban Affairs, U.S. Senate, November 13, 1991, S.1611, 102 Cong. (Washington: Government Printing Office), pp. 25-33. Return to text

6. See David R. Merrill and others v. Federal Open Market Committee of the Federal Reserve System, U.S. District Court of the District of Columbia, 443 U.S. 340 (1979). Disclosure of the directive adopted at a given FOMC meeting was deferred until after the following meeting, at which time the released directive would be superseded by a new directive. Return to text

7. While Robert Lucas mainly analyzed models in which only monetary surprises have any effect on real activity, his important insight in the present context was that the perceived monetary policy rule is critical in determining the effects of monetary policy actions, both anticipated and unanticipated. Return to text

8. The FOMC also provided information concerning its "exit strategy" in the minutes of its June 2011 meeting (see Board of Governors of the Federal Reserve System (2011), Minutes of the Federal Open Market Committee, June 21-22). The Committee indicated that it intends to normalize the size and composition of its balance sheet by selling off agency securities at a gradual pace after it begins the process of raising the federal funds rate. Return to text

9. Economic theory suggests that the public's expectations concerning the time path of the Federal Reserve's asset holdings--which includes both the ultimate size of those holdings and the length of time that these assets will be retained on the Fed's balance sheet--influence longer-term yields and the term premiums embedded in those yields today. For empirical estimates of these effects see, for example, Canlin Li and Min Wei (2012), "Term Structure Modeling with Supply Factors and the Federal Reserve's Large Scale Asset Purchase Programs," Finance and Economics Discussion Series 2012-37 (Washington: Board of Governors of the Federal Reserve System, May). Return to text

10. Similar subcommittees acting in the early 1990s dealt with FOMC policies concerning the disclosure of the minutes and transcripts of FOMC meetings. An FOMC subcommittee in 1999 laid the groundwork for the current FOMC postmeeting statements. And a subcommittee appointed in 2006, led by the then Vice Chairman Kohn, considered the adoption of a numerical inflation objective and recommended enhancements that were incorporated in the Summary of Economic Projections. Return to text

11. See, for example, the discussions in Lars E.O. Svensson (1999), "Inflation Targeting as a Monetary Policy Rule," Journal of Monetary Economics, vol. 43 (June), pp. 607-54; and in Jon Faust and Dale W. Henderson (2004), "Is Inflation Targeting Best-Practice Monetary Policy?" Federal Reserve Bank of St. Louis Review, vol. 86 (July/August), pp 117-44. Return to text

12. See Board of Governors, "FOMC Statement of Longer-Run Goals and Policy Strategy," in note 3. Return to text

13. Due to well-known upward biases in the PCE and other indexes of consumer prices as measures of the cost of living, zero inflation, properly measured, corresponds to a positive measured level of PCE inflation, most likely on the order of 1/2 percent. Return to text

14. The detrimental effects of unanticipated deflation are discussed in remarks by the then Governor Bernanke. See Ben S. Bernanke (2002), "Deflation: Making Sure ‘It' Doesn't Happen Here," speech delivered at the National Economists Club, Washington, November 21. Return to text

15. See Board of Governors, "FOMC Statement of Longer-Run Goals and Policy Strategy," in note 3. Return to text

16. It is worth noting that the dealer forecasts probably incorporate some effect from asset purchases that were only later announced by the FOMC. At the time of this survey, the median probability that the primary dealers assigned to the FOMC announcing a new program of asset purchases in September was 55% and the median probability assigned to further asset purchases within one year was 70%. The median value of asset purchases anticipated by the dealers under such a program was about $500 billion. In the simulations that follow, I treat the balance sheet as unchanged relative to its baseline path, and focus on the federal funds rate as the tool for conducting monetary policy even though the Committee is currently using both forward guidance concerning the funds rate path and the balance sheet to provide monetary accommodation. (The text of this footnote has been revised since its original release.) Return to text

17. More precisely, the loss function that the central bank is assumed to minimize is the discounted sum of current and future squared deviations of inflation from 2 percent, current and future squared deviations of the unemployment rate from 6 percent, and current and future quarterly changes in the federal funds rate. The last term is included to avoid unrealistically large quarterly movements in the "optimal" federal funds rate path. Return to text

18. This illustration takes the anticipated scale of asset purchases as fixed. The effect of these purchases, given that the modal expectation in the primary dealer survey was for $500 billion of purchases, is implicitly already incorporated into the baseline forecast. In principle, we could use the FRB/US model to perform a joint optimization exercise in which the optimal paths of asset purchases and the federal funds rate are simultaneously determined, but the results from such an exercise would be highly sensitive to assumptions about possible costs of asset purchases that are not well defined, such as the potential for market disruption. Return to text

19. It is also worth noting that the "Exit Strategy Principles" adopted by the FOMC in June 2011 indicate that the Committee intends to gradually sell off agency securities to normalize the size and composition of its portfolio after liftoff of the federal funds rate. This assumption pertaining to asset sales is incorporated into the FRB/US simulations, and provides a further reason why, along the optimal control path, the federal funds rate stays low for so long, rising only gradually after liftoff. Return to text

20. The rule is defined as Rt = 2 + πt + 0.5(πt - 2) + 1.0Yt. In this expression, R is the federal funds rate, π is the percent change in the headline PCE price index from four quarters earlier, and Y is the output gap. The output gap is approximated using Okun's law; specifically, Yt = 2.0(6‑Ut), where 2.0 is the estimated value of the Okun's law coefficient and 6 is the assumed value of the non-accelerating inflation rate of unemployment, or NAIRU. In a recent speech (see Janet L. Yellen (2012), "The Economic Outlook and Monetary Policy," speech delivered at the Money Marketeers of New York University, New York, April 11), I dubbed this rule "Taylor (1999)," as John Taylor described the rule in a paper published that year. See John B. Taylor (1999), "A Historical Analysis of Monetary Policy Rules," in John B. Taylor, ed., Monetary Policy Rules (Chicago: University of Chicago Press), pp. 319-41. As Taylor’s own strong preference is for his original rule--Taylor (1993)--I now refer to the later rule as the "modified Taylor rule." (The text of this footnote has been revised since its original release.) Return to text

21. I would note that the original Taylor rule, which places only one-half as much weight as the modified rule on unemployment deviations, would already have raised the federal funds rate above the zero bound, producing far worse outcomes than any illustrated in figure 1. Return to text

22. The baseline path, based through the end of 2015 on the primary dealer survey, assumes greater accommodation than would be consistent with the modified Taylor rule, suggesting that FOMC communications have had some success in conveying the desirability of such an approach. Return to text

23. See Board of Governors, "Federal Reserve Issues FOMC Statement," September 13, note 2. Return to text

24. In the SEP, participants provide paths for the unemployment rate, real GDP growth, and inflation that each expects under his or her own view of the policy that is most appropriate to achieve the Committee's dual mandate. But as is apparent in the SEP, participants have a great diversity of views on matters such as the expected timing and subsequent pace of federal funds rate increases. The SEP currently provides information about the separate distributions of the projections for inflation, real activity, and the federal funds rate over the next few years, but it does not provide the joint paths--that is, multivariate projections. The public cannot, for example, infer whether a projection for higher inflation in 2015 was made by a participant who expects real activity to be weak due to a more pessimistic view about the productive capacity of the economy, or by a participant who expects higher inflation in the context of a stronger recovery, perhaps judging, in the spirit of the optimal policy simulations, that somewhat higher inflation is warranted for some time to achieve faster progress in reducing unemployment. Return to text

25. The FOMC could also, potentially, provide additional information pertaining to the economic conditions it would expect to justify a decision to stop, or scale back, its asset purchases. However, this decision also depends on the Committee's assessment of efficacy and costs--matters on which the Committee is still gaining experience. Return to text