July 20, 2010

The state of U.S. coins and currency

Louise L. Roseman, Director, Division of Reserve Bank Operations and Payment Systems

Before the Subcommittee on Domestic Monetary Policy and Technology, Committee on Financial Services, U.S. House of Representatives, Washington, D.C.

Chairman Watt, Ranking Member Paul, and members of the Subcommittee, I am pleased to appear before you on behalf of the Board of Governors of the Federal Reserve System to discuss Federal Reserve activities related to currency and coin. I plan to touch on currency developments and management of coin distribution.

Roles in Currency and Coin Distribution

First, it may be helpful to describe briefly the Federal Reserve's role in currency and coin distribution. The Board issues the nation's currency in the form of Federal Reserve notes. The Federal Reserve Banks distribute currency and coin for general circulation through depository institutions. The Reserve Banks also receive deposits of currency and coin from these institutions. Currently, thirty Reserve Bank cash offices provide cash services to approximately 9,200 banks, savings and loans, and credit unions in the United States. The remaining depository institutions obtain currency and coin from correspondent banks rather than directly from the Federal Reserve.

Each year, the Board projects the need for new currency, which it acquires from the Department of the Treasury's Bureau of Engraving and Printing (BEP) at approximately the cost of production. Our new-currency budget for 2010 is $703 million. The Federal Reserve issues notes at face value, which are recorded as liabilities on the Reserve Banks' balance sheets. The Reserve Banks, as required by law, pledge collateral (principally U.S. Treasury, federal agency, and government-sponsored enterprise securities) equal to the value of currency in circulation. This collateral produces a substantial portion of the earnings that Reserve Banks distribute to the Treasury each year. In the years preceding the recent increases to the Reserve Bank balance sheets, when currency represented the large majority of Reserve Bank liabilities, the annual distributions to the Treasury generally ranged from $20 to $30 billion. In 2009, the Reserve Banks distributed $47.4 billion to the Treasury.

The Federal Reserve monitors trends in and publishes statistics on noncash transactions such as checks, credit and debit cards, and other electronic payments, but it does not publish statistics on individuals' use of cash.1 Obtaining reliable data on cash transactions is more difficult because, unlike noncash payment methods, cash transactions do not flow through centralized systems at institutions that specialize in payments processing such as depository institutions and payment networks. Data on cash transactions would have to come from alternative sources, such as consumers or businesses, from whom representative data may be difficult to collect. Despite the difficulty of direct measurement of cash transactions, the Federal Reserve does monitor and study cash use in the United States through the information it collects in its role as currency processor, and from consumers and businesses. Although there is no direct information on trends in cash use, statistics on the growth in the use of noncash payment methods suggest some substitution away from cash in recent years. In addition, discussions Federal Reserve officials have had with select retailers suggest that cash transactions continue to grow although at a much slower rate than electronic forms of payment.

The Federal Reserve's role in coin operations is more limited than its role in currency operations. The United States Mint issues circulating coins that the Reserve Banks purchase at face value and record as assets on their balance sheets.2 The Reserve Banks distribute new and circulated coin to depository institutions to meet the public's demand and take as deposits coin that exceeds the public's needs. The United States Mint determines annual coin production; however, the Reserve Banks influence the process by providing the Mint with monthly coin orders and a 12-month, rolling coin-order forecast. The Mint transports the coin from its production facilities for circulating coin in Philadelphia and Denver to the Reserve Banks' offices and offsite locations. While the Reserve Banks store some coin in their vaults, they also contract with coin terminals to store, process, and distribute coin on their behalf.3 Armored carrier companies generally operate the coin terminals, which have improved the efficiency of the coin-distribution system. Today, 174 coin terminals store about 37 percent of the Federal Reserve's coin inventory volume, but account for about 88 percent of Reserve Bank daily distributional activity.4 The value of U.S. coins in circulation as of May 31, 2010, was approximately $40.4 billion, or about 4.3 percent of total currency and coin in circulation.

Currency Developments

Trends in Currency Demand

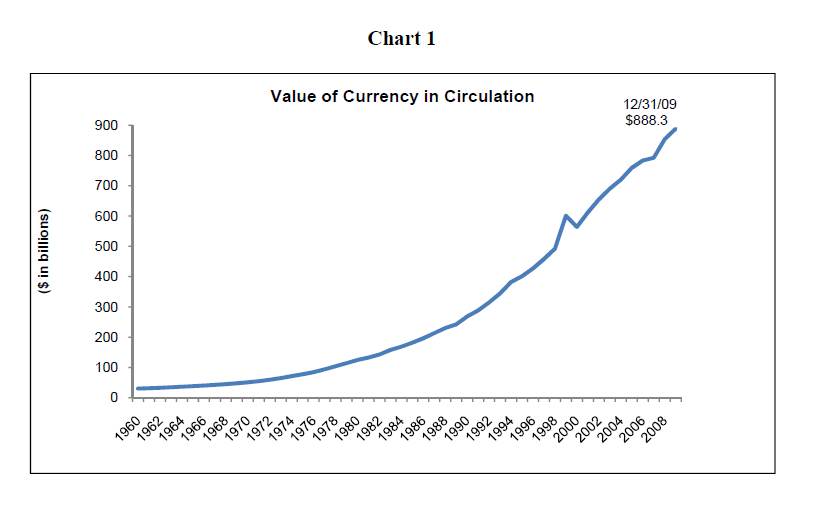

The Federal Reserve measures demand for U.S. currency by the amount of currency in circulation. From 1980 to 2009, currency in circulation increased an average of 7.0 percent per year from $124.8 billion to $888.3 billion, as shown in chart 1.5 Domestic demand for currency is largely based on the use of currency for transactions and is influenced primarily by income levels, prices of goods and services, the availability of alternative payment methods, and the opportunity cost of holding currency in lieu of an interest-bearing asset. In the United States, demand (in terms of number of notes) for smaller denominations ($1s through $20s) exceeds demand for larger denominations ($50s and $100s). Consumers frequently use smaller-denomination notes for small transactions and alternative payment methods (for example, debit and credit cards) for larger purchases. In contrast, foreign demand is influenced primarily by the political and economic uncertainties associated with certain foreign currencies, which contrast with the U.S. dollar's historically relatively high degree of stability. Because U.S. currency is held abroad primarily as savings, foreigners tend to hold high-denomination notes. The Federal Reserve estimates that as much as two-thirds of currency in circulation is held abroad.6

{kind=link}

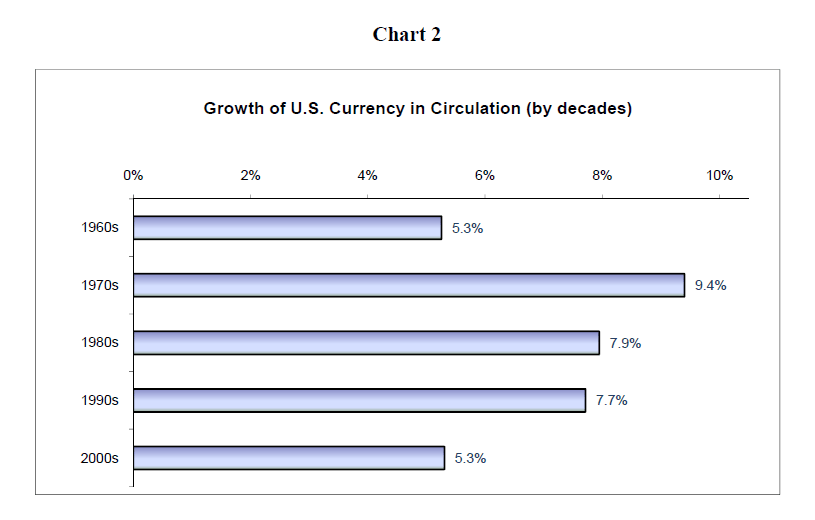

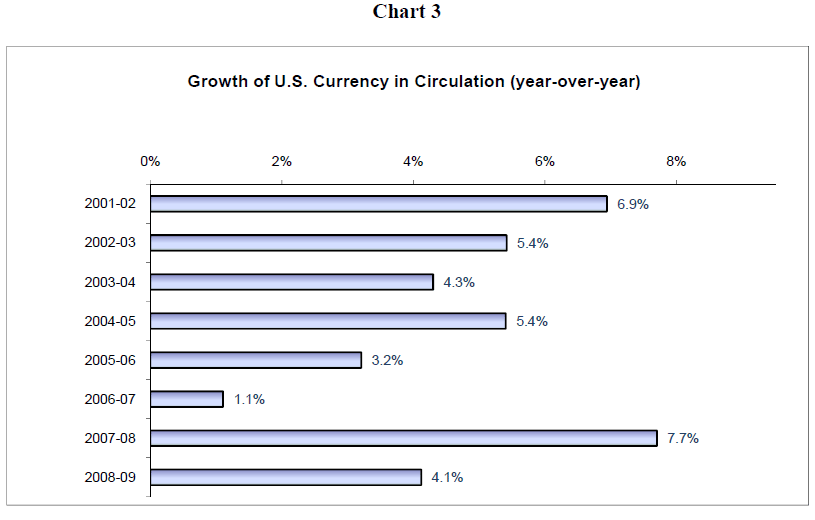

The foreign component of currency in circulation is estimated to have increased significantly beginning in the late 1980s and continues to grow today. In the 1990s, currency in circulation grew at an average annual growth rate of approximately 7.7 percent, resulting primarily from increases in foreign demand and a surge in demand at the end of the decade.7 As shown in chart 2, during the decade beginning in 2000, the average annual growth rate of currency in circulation moderated to about 5.3 percent (which is a rate consistent with growth during the 1960s). As reflected in chart 3, however, annual growth rates began to decline in 2001 and significantly declined to below one percent in 2008 (through August). Demand slowed over this period partly because the value of the dollar decreased against many other major currencies; international markets gained trust in their own economies and national currencies; electronic payments displaced some cash usage; and the effect of the recent recession. This decline was reversed, however, beginning in September 2008, as currency demand increased significantly as a result of the financial crisis. Currency growth increased substantially, from 0.8 percent year-to-date through August 2008 to 7.7 percent for full-year 2008. As the effects of the financial crisis persisted, strong growth continued in 2009; currency in circulation increased from $775 billion at the end of 2007 to almost $900 billion by year-end 2009. As of May 31, 2010, the value of currency in circulation was $902.2 billion, or about 95.7 percent of total currency and coin in circulation.

{kind=link}

{kind=link}

The effects of the financial crisis on currency in circulation domestically were less significant than on currency in circulation internationally. Although domestic demand appears to have increased briefly in the fall of 2008, the increase of the FDIC deposit insurance limit and other government actions to address the crisis allayed domestic concerns and demand seems to have returned quickly to normal levels. The majority of the growth rate increase was driven by demand for $100 notes internationally. The Federal Reserve requested that the BEP accelerate the Board's print order for $100 notes during this period so that the Reserve Banks could continue meeting international demand.8 Although payments of $100 notes abroad have returned to normal levels, most of the currency the Reserve Banks paid into circulation during the financial crisis remains in circulation as Reserve Bank receipts from circulation remain historically weak.

Evolving Currency Designs of Federal Reserve Notes

The U.S. government redesigns U.S. currency to improve its security and protect the public from counterfeiters. Through an interagency cooperative agreement of the Treasury Department and its Bureau of Engraving and Printing, the Federal Reserve System, and the United States Secret Service, the Board participates on the Advanced Counterfeit Deterrence Steering Committee (ACD) and recommends U.S. currency design changes to the Secretary of the Treasury, who has sole statutory authority to approve new currency designs. Decisions about the redesign of each denomination are guided by the ACD's evaluation of the range of ongoing counterfeit threats from digital technology and traditional printing processes, and advancements in banknote security features.9

Through this cooperative effort, in 1996, the United States produced the first significant redesign of U.S. currency in 65 years (the Series-1996 design family). This redesign began with the $100 note in March 1996 and concluded with the $5 and $10 notes issued together in May 2000. The 1996-design family incorporated portrait watermarks, embedded security threads, and color-shifting ink to combat the predominant threat of the traditional counterfeiter. To address a phenomenon known as "opportunistic counterfeiting," which is the use of digital technology available in the home by non-professional or casual counterfeiters, the ACD recommended another redesign of the currency, which began with the $20 note in October 2003, followed by the $50 note in 2004, the $10 note in 2006, and the $5 note in 2008.

The final denomination in the 2004-design family, the $100 note, was unveiled on April 21. The unveiling of the $100 note was the first step in a multi-agency program to educate consumers, businesses, banks, and governmental entities around the world about the new $100 note before it begins circulating. Under the auspices of the ACD, we conducted extensive qualitative and quantitative research to understand better how domestic and international users verify the authenticity of the $100 note. Through this research, three major points emerged: (1) those who use U.S. currency do not want drastic changes when we introduce new designs and prefer only a few security features that are easy to use; (2) the security features in the current-design $100 note are considered effective; and (3) it was important to some users that any new security features can be used discreetly.10 Building on the currency-design efforts that began in 2003, this note reflects what we learned from the research and includes new, state-of-the-art security features such as the 3-D security ribbon and the color-shifting bell in the ink well. The Federal Reserve will begin distributing the new $100 note on February 10, 2011.

Management of Coin Distribution

The Federal Reserve has been working for some time to improve the efficiency of the Reserve Banks' coin activities by implementing a program to manage coin distribution from a national perspective. Before the Federal Reserve moved to centralized management of coin distribution, each Reserve Bank made independent ordering and distributional decisions. Today, the Reserve Banks' national Cash Product Office (CPO) manages coin nationally for the Federal Reserve System, taking into account the Reserve Banks' input regarding local estimates of coin demand. The CPO produces a consolidated monthly coin order on behalf of the Reserve Banks for the United States Mint. Along with the order, the CPO provides the Mint with a rolling, 12-month order forecast for planning purposes. The key element of the CPO's forecast is predicting net payments to circulation--the difference between payments to and receipts from circulation. The order and forecast are based on expected net payments relative to Reserve Banks' inventory levels. The Reserve Banks ensure sufficient inventories are positioned at each office and coin terminal to meet the forecasted demand.

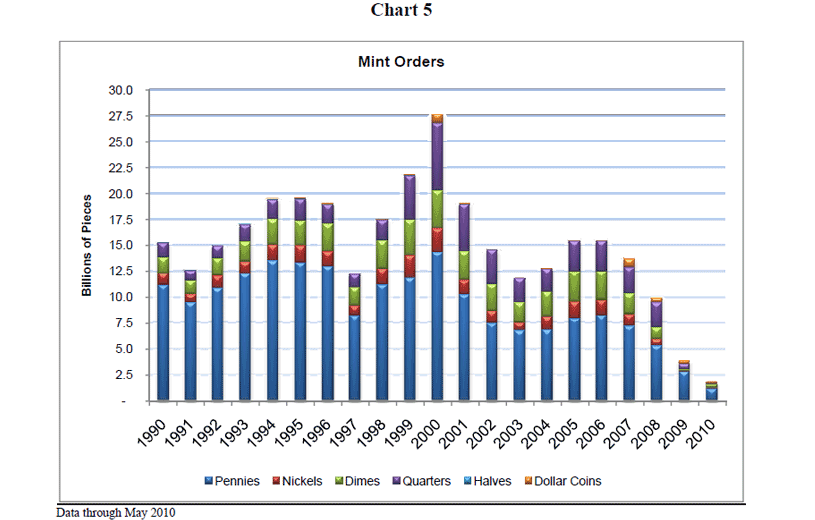

As a result of improved inventory management, over the past five years, the Reserve Banks have increasingly used previously circulated pennies, nickels, and dimes to fill orders from depository institutions while decreasing their orders for these coins from the United States Mint by almost 31 percent, compared with the average orders over the previous five years, as shown in chart 5. This has reduced Reserve Bank inventories of pennies, nickels, and dimes as of May 31, 2010, to their lowest levels since early 2000, although they are still sufficient to meet demand.11 The Reserve Banks have not experienced surpluses or shortages of pennies, nickels, or dimes since 1999 when they experienced a temporary shortage of pennies.

{kind=link}

Commemorative Circulating Coins

Demand for coin for transactional purposes can be met by any design of a denomination. For example, a retailer that orders quarters from its bank typically does not care what design(s) it receives. Demand for a commemorative circulating coin by collectors, however, is design-specific. In the early years of the 50 State Quarters program, the Reserve Banks ordered more new quarters than were necessary to meet demand in order to fill many depository institution orders with new coins rather than with available inventories of circulated quarters. The residual coins from each release, plus the excess quarters redeposited by depository institutions, created excessive inventories at the Reserve Banks. The Reserve Banks were able to reduce those inventories because of regular demand for quarters.12 Because of low transactional demand for $1 coins, however, the Federal Reserve's experience with commemorative circulating $1 coin programs has differed significantly. For previous $1 coin programs, the Reserve Banks have encountered large excess inventories for much longer periods, and our experience with the Presidential $1 Coin Program is consistent with those programs.13

Presidential $1 Coin Program

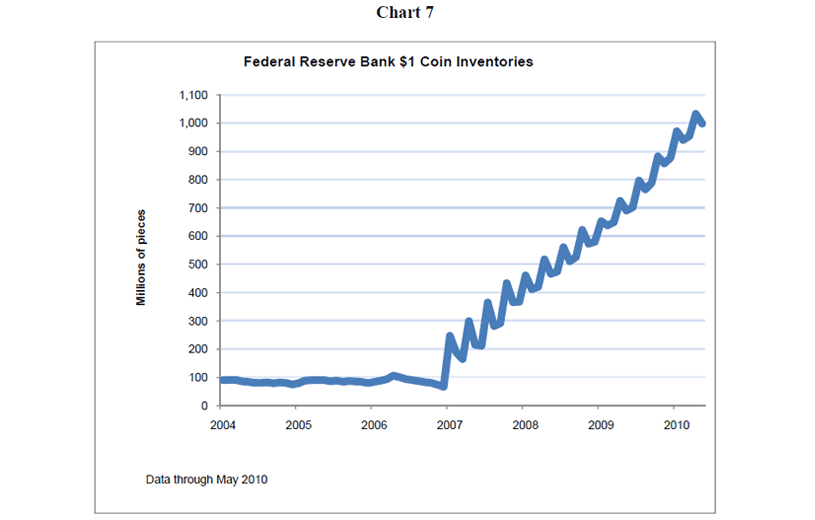

Before the Presidential $1 Coin Program began in 2007, demand for $1 coins, measured in Reserve Banks' net payments to circulation, was about $60 million per year (for comparison, net payments of $1 notes to circulation in 2006 were $289 million). Reserve Banks' payments to circulation increased significantly in the first year of the Presidential $1 Coin Program but have consistently declined since that time, while receipts from circulation have significantly increased.14 With Reserve Bank payments to circulation decreasing and receipts increasing each year of the program, Reserve Banks' inventories of $1 coins are growing substantially. As shown in chart 7, previous $1 coin supplies, plus the excess $1 coins returned by depository institutions, have elevated total Reserve Banks' inventories of all $1 coins to almost $1 billion as of May 31, 2010, compared with $67 million before the start of the program. At the current rate of inventory growth, the Federal Reserve estimates that it could hold as many as $2 billion by the time the program is expected to end.15 This inventory growth, in large part, is because a requirement in the Presidential $1 Coin Act requires the Federal Reserve to make each new design available to the public in unmixed quantities for an introductory period. Therefore, the Reserve Banks must order each new design from the Mint even though the Reserve Banks have ample inventories of $1 coins.

{kind=link}

Banking industry and armored carrier representatives have indicated that transactional demand for $1 coins has not increased materially since the start of the Presidential $1 Coin Program and that overall demand continues to come primarily from collectors. They have also indicated, however, that the program is working very well from their perspectives, that the coins are easy to order, and that our communication about program details is effective.16 Most representatives did not believe that demand would increase significantly for future coin releases, with the possible exception of the coins commemorating the most popular former Presidents.

Native American $1 Coin Program

The Native American $1 Coin Act requires that at least 20 percent of all $1 coins minted and issued in any year be Native American $1 coins. Because the Reserve Banks already have excessive inventories of $1 coins, the Reserve Banks do not plan to purchase Native American $1 coins unless needed to meet demand.17 As a result of the legislative requirement to issue these coins, the Mint began paying Native American $1 coins (and some Presidential $1 coins) directly to circulation through its Direct Ship program, which allows the public to order boxes of $1 coins in $250 increments. The Mint indicates that it paid to circulation $12 million $1 coins in 2008 and $121 million in 2009.18

Total Demand for $1 Coins

Taking into consideration the Reserve Banks' net payments to circulation and the Mint's direct payments to circulation, total demand for $1 coins in 2009 was nearly triple that of 2006, before the start of the Presidential $1 Coin Program. This increase, however, was from a very low base of only $60 million per year. Demand has declined by two-thirds since the initial year of the Presidential $1 Coin Program.19 It is unclear what portion of $1 coin demand is for transactional versus collector purposes, or where demand for $1 coins will ultimately stabilize. What is clear, however, is that the legislative requirements associated with these programs are resulting in steadily rising Reserve Bank inventories and the attendant costs of dealing with those inventories.

Metal Content of Coins

As the issuing authority for currency, the Federal Reserve appreciates the importance of identifying and incorporating cost-effective materials into the production of our nation's money. We commend the United States Mint for seeking solutions to the problem of higher raw material costs. Changing the metal content of pennies and nickels, even if doing so changes the weight and electronic signature, would not have a material adverse effect on the operations of the Reserve Banks. The Reserve Banks stopped routinely weighing penny and nickel deposits in 2003 after determining that the costs exceeded the benefits of doing so. Instead, the Reserve Banks give depository institutions credit on deposits of coin on a "said to contain" basis. As a result, we do not anticipate significant internal operational challenges associated with any such changes. Changing the metal content of dimes, quarters, half-dollars, and $1 coins, if it affects the respective weights, could affect Reserve Bank coin terminal operations. Coin terminal operators weigh incoming deposits of these denominations.

If a change in metal content changes a coin's weight or electronic signature, it could materially affect businesses that use coin-accepting machines, such as the vending industry, or other businesses that rely on these characteristics. While such a change probably would not be a material issue with respect to pennies, which are generally not accepted in vending equipment, it may be for larger-denomination coins. Those businesses are better placed to comment on the extent to which they would be required to make changes to their equipment to recognize coins of the same denomination that have different weights and electronic signatures.

Conclusion

The Federal Reserve will continue to work to meet demand for currency and coin efficiently and effectively. I appreciate the opportunity to discuss these issues with you and would be happy to answer your questions.

1. The Federal Reserve publishes currency in circulation data in its weekly H.4.1 report. In addition, the Federal Reserve also reports Reserve Banks' payments and receipts of currency and coin into and from circulation. Return to text

2. Coins held by the Reserve Banks are non-interest-earning assets on their books. Return to text

3. These armored carrier companies do not charge the Reserve Banks a fee for these services. In the 1990s, the Federal Reserve and the armored carrier companies reached a mutually beneficial agreement that the armored carriers would provide coin services on behalf of the Federal Reserve at no cost in exchange for access at the armored carrier terminals to Reserve Bank coin inventories, which significantly reduced the transportation expenses incurred by the armored carriers in obtaining the coin from Reserve Bank locations. Return to text

4. The armored carrier companies are most interested in storing coin that is routinely used in cash transactions (primarily pennies, nickels, dimes, and quarters) because they can charge fees to the depository institutions for providing coin services in preparing the coin for sale to their customers. Return to text

5. The value of currency in circulation was $242.3 billion at year-end 1989; $601.2 billion at year-end 1999; and $888.3 billion at year-end 2009. Return to text

6. In addition to being used as a store of value, U.S. currency is also used broadly for transactional purposes in officially dollarized countries, such as Panama, Ecuador, El Salvador, and East Timor, and in other countries where the U.S. dollar co-circulates with local currencies. Return to text

7. In preparation for the century date change, currency in circulation increased 22.1 percent from its December 1998 level. Uncertainty associated with the century date change increased the public's precautionary demand for cash, but as the event passed without incident, the public returned much of the currency it had amassed to depository institutions. Return to text

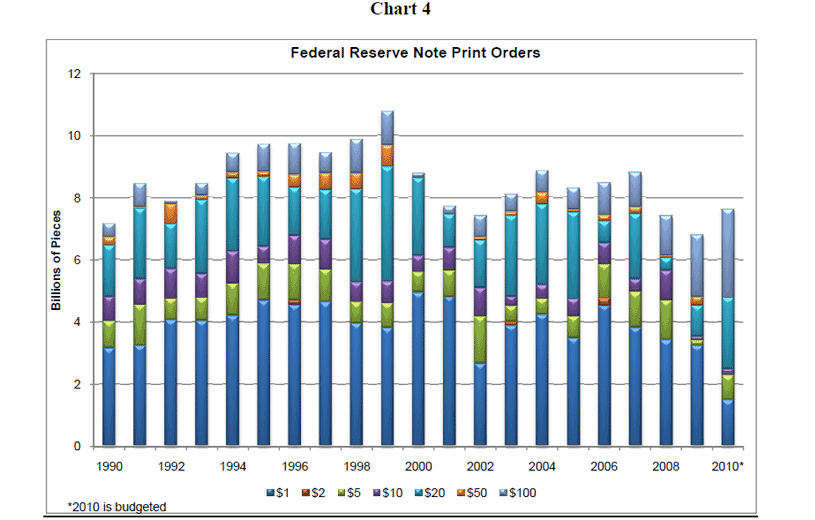

8. Chart 4 shows the Federal Reserve's annual currency print orders from the BEP from 1990 through 2010. Return to text

{kind=link}

9. The ACD has set as general policy guidance that currency will be redesigned every 7 to 10 years depending on specific counterfeiting threats and experience related to a particular denomination. The first Series-2004 design family of notes was issued about seven years after the first Series-1996 note was issued. Return to text

10. The two primary security features (portrait watermark and embedded security thread) in the current-design $100 note require the user to hold the note up to light to check for authenticity. Although these features will remain in the new-design $100 note, new security features have been added that will require only slight movements of the note to authenticate. Return to text

11. As of May 31, 2010, the Reserve Banks held about 1.5 billion pennies, 343 million nickels, and 546 million dimes. Return to text

12. The Reserve Banks' quarter inventories reached a peak of 3.0 billion pieces in January 2003 and declined to 2.1 billion by year-end 2007. Inventories increased significantly in 2008 and 2009, however, because of considerably lower payments to circulation during the recession. The Reserve Banks expect to reduce those inventories once again, as demand improves. During 2010 through May, improved demand enabled the Reserve Banks to reduce inventories by almost 500 million pieces, or a 13 percent reduction since year-end 2009. As of May 31, 2010, the Reserve Banks held 3.3 billion quarters. Return to text

13. Because there is almost no transactional demand, Reserve Bank inventories of half-dollar coins also increase each year. Since 2001, Reserve Banks' inventories have increased by 110 million pieces even though the Reserve Banks have only ordered 24 million pieces over that time period. Return to text

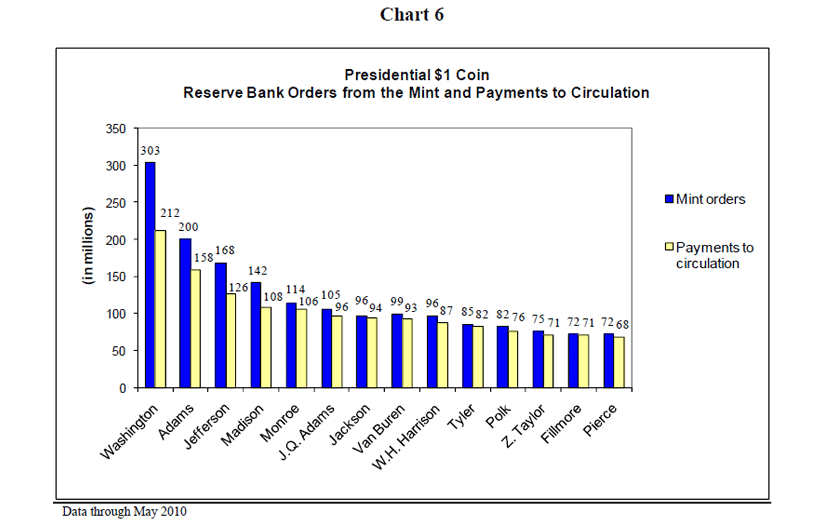

14. As chart 6 indicates, depository institution demand has decreased for each successive Presidential $1 coin design. About 70 percent of $1 coin payments to circulation occur during the special ordering periods for each new release. Return to text

{kind=link}

15. Because of the reluctance of most armored carrier companies to hold excess inventories of $1 coins that have low transactional demand and Reserve Banks' vault storage contraints, the Federal Reserve is investigating additional options to store these coins. The Reserve Banks have currently identified additional storage options at estimated one-time costs of about $6 million. Return to text

16. The Federal Reserve meets at least annually with representatives of depository institutions with the largest cash volumes, community bankers, and armored carriers to gather feedback about demand and potential obstacles to the circulation of $1 coins. Return to text

17. See 2007 Annual Report to the Congress on the Presidential $1 Coin Program, page 24. http://www.federalreserve.gov/boarddocs/RptCongress/dollarcoin/dollarcoin.htm. Return to text

18. The Mint is not currently charging shipping and handling fees for this program. Return to text

19. Considering both the Reserve Banks' net payments and the Mint's direct payments, total $1 coin demand was $513 million in 2007, $235 million in 2008, and $171 million in 2009. Return to text