FEDS Notes

September 07, 2023

Analyzing State Resilience to Weather and Climate Disasters

Celso Brunetti, Benjamin Dennis, Gurubala Kotta, and Adam Smith1

The National Oceanic and Atmospheric Administration (NOAA) reports that climate change is increasing the frequency of extreme conditions that lead to disasters such as droughts, hurricanes, flooding, and wildfires.2 These climate-related physical risks are likely to disrupt local economic activity. Given these risks, it is unclear what impact these extreme events might have on local government finances in the medium to longer term. Against this backdrop, this note quantifies historical disaster damages relative to states' tax revenues and explores future cost-sharing dynamics between firms and households, insurers, and federal and local governments.

Billion-Dollar Weather and Climate Disasters

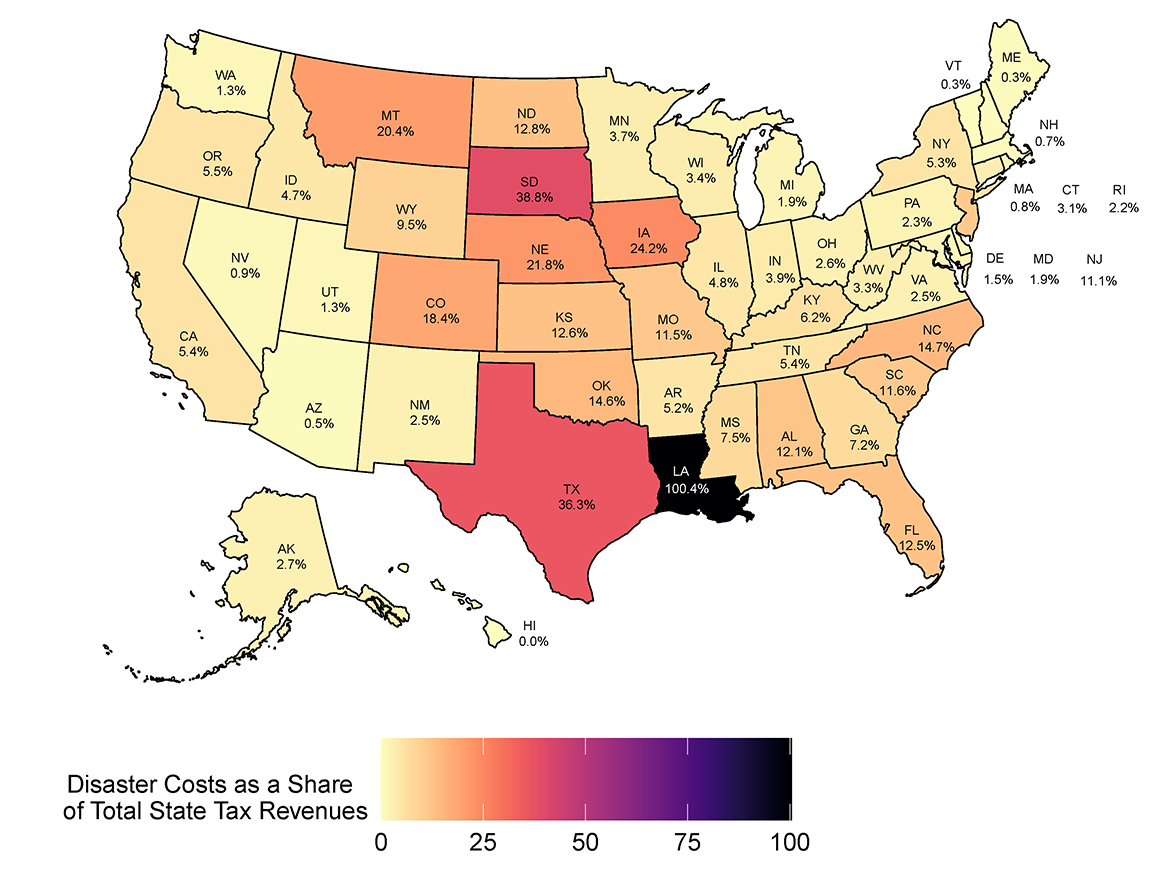

NOAA tracks disasters that cause damages in excess of $1 billion (inflation adjusted). Damages from these weather and climate disasters have increased significantly over the past 40 years. Nationally, the real cost of these disasters – which differ by type and relative cost across regions – has risen from $20 billion per year in the 1980s to nearly $95 billion per year during the period 2010–19. In 2021, damages increased to about $153 billion.3 Figure 1 shows the estimated cumulative cost of these disasters4 for the period 2012–21 across U.S. states as a percentage of cumulative state tax revenues, with the yellow shading indicating that disaster costs are a small share of a state's tax revenues and the purple shading indicating that such costs are a larger share of revenues. Note, we normalize damages by tax revenues5 to proxy for state fiscal vulnerability.6 Figure 1 has three main takeaways:

Figure 1. 2012-2021 Billion-Dollar Weather and Climate Disaster Costs as a Share of Total State Tax Revenues

Note: This figure omits costs associated with chronic climate phenomena such as low rainfall and higher average temperatures.

Source: National Oceanic and Atmospheric Administration, the Bureau of Labor Statistics, and the U.S. Census Bureau.

- The state most affected over this period is Louisiana, with damages amounting just over 100 percent of tax revenues. Even worse affected, a similar calculation for Puerto Rico (not included in Figure 1) shows that incurred damages are approximately double their revenues.7 By contrast, Maine and Vermont, among other states, have been much less affected.

- The clustered shading shows that damages in relation to tax revenues are particularly high in Midwestern and Southern states, possibly raising fiscal vulnerabilities in those states.

- Losses from damages are already large relative to tax revenues for some states, and these damages could rise as the frequency and/or severity of these disasters is projected to increase in many locations.8

Damages in Figure 1 reflect four factors: (1) frequency, or the number of extreme weather events; (2) hazard, or the intensity of the event; (3) exposure, or the number of firms and households affected by the event; and (4) vulnerability, or the resilience of each firm, household, or local economy to the event.9 Each of these factors is changing over time. The number of severe weather events is increasing, with multiple events occurring in the same area within a single year. The intensity of climate events is increasing due to climate change; for example, hurricanes appear to be strengthened by warmer oceans and increased moisture in the air.10 Exposure has risen as migration and growth have increased the share of population and economic activity in the South, which appears more vulnerable than other parts of the country. However, ongoing adaptation of infrastructure and continued improvements in building codes can be expected to reduce vulnerabilities with time.11 Projecting trends in these four dimensions is likely to provide valuable insights into future climate-related costs to the economy.

Who is Bearing the Costs?

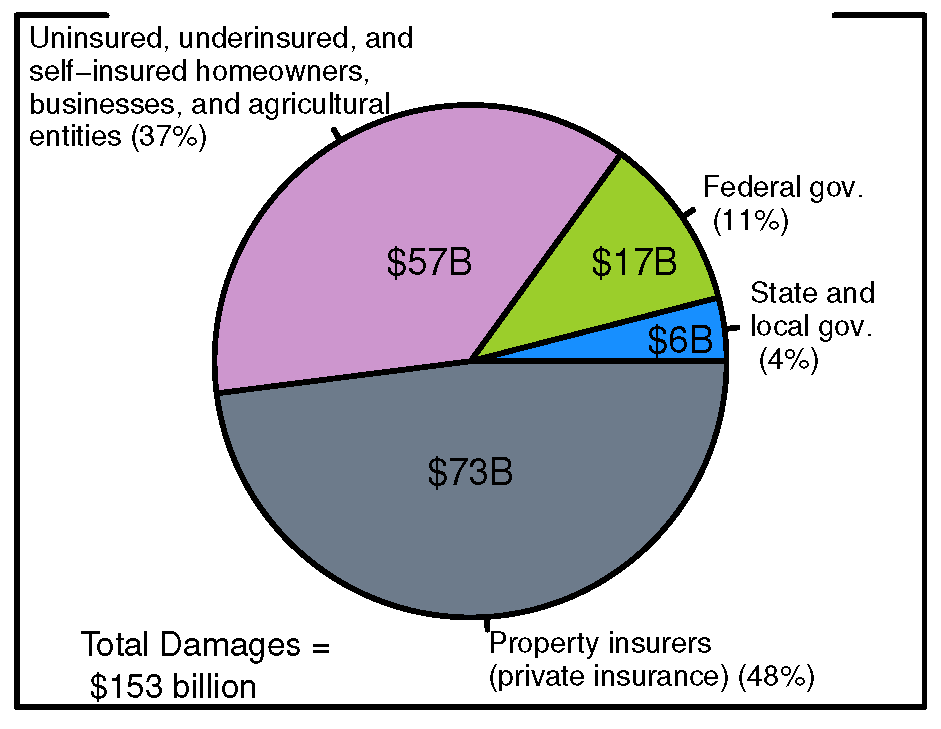

To better understand which entities are bearing the costs of such disasters, we use 2021 damages – which amounted to about $153 billion – as a case study. As shown by Figure 2, costs were absorbed by four entities: property insurers (48 percent), uninsured or underinsured homeowners, businesses, and agricultural entities (37 percent),12 the federal government (11 percent), and state and local governments (4 percent).13 Note, state and local governments incurred the smallest share in Figure 2, but as seen in Figure 1, such costs would already be overwhelming for certain states' budgets if there were no cost sharing mechanisms.

Source: National Ocean and Atmospheric Administration.

Importantly, the share of losses incurred by each of the entities shown in Figure 2 could shift over time. If property insurers were to exit certain markets or decrease coverage in states with greater exposure to physical risks due to decreased profitability, a larger share of damages would not be fully insured. Such structural shifts are already beginning to materialize – two major insurers recently announced that they will no longer accept new applications for business and personal property insurance coverage in California, citing increasing wildfire risk as a key factor in that decision.14 In addition, several major hurricanes (Ida, Laura, and Ian) during 2020-2022 forced numerous insurance companies into bankruptcy in Louisiana and Florida. Under such circumstances, homeowners, businesses, and agricultural entities may not be able to secure sufficient coverage to minimize their losses, and thus bear a larger share of costs. Additionally, given that the federal government can be regarded as the "final backstop" for disaster relief,15 its share of incurred losses could increase over time. Note, rapidly disbursing federal aid (and insurance payouts) in an accountable manner immediately after a disaster is difficult, and homeowners, businesses, and agricultural entities may face challenges in applying for aid and delays in receiving it. It is therefore common for affected individuals to bear a larger share of upfront costs until assistance arrives.

Conclusion

In coming decades, damages are likely to rise as disasters are projected to increase in frequency and/or severity. Such disasters may increase the incentive to shift economic resources away from locations troubled by clustered and increasing physical risk exposures. Indeed, other researchers predict that wealth is likely to transfer away from states in the South and Midwest toward less affected regions.16 Of course, whether such shifts will be visible in a straight read of data on employment, income, and wealth will depend upon a range of factors, including climate adaptations and the strength of the geographic preferences of households and businesses. Therefore, understanding whether and to what degree such shifts occur is necessarily a subject for future research. Additionally, closely sequential or coincident events appear to be occurring more frequently; for example, 1) in August 2021, California faced multiple wildfires at the same time that Hurricane Ida devastated Louisiana and caused widespread flooding in the Northeast, and 2) Texas experienced three sequential billion-dollar events in just one month in 2021.17 Between 2017-2021, there were just 18 days on average between U.S. billion-dollar disaster events compared to 82 days in the 1980s.18 Shorter time intervals between disasters can mean less time and resources available to respond, recover, and prepare for future events. This increased frequency of events produces cascading impacts that are particularly challenging to vulnerable socioeconomic populations that may lack property insurance or other recovery provisions. These co-occurring events may also potentially increase the cost of disaster mitigation and relief efforts while also possibly raising the cost of insuring against extreme weather events. Further research is needed to better understand the full scope of welfare and economic implications stemming from the physical risks of climate change and future cost sharing dynamics between firms and households, insurers, and federal and local governments.

1. We thank Diana Hancock and Matthias Paustian for helpful comments and suggestions. Adam Smith is an applied climatologist at the National Oceanic and Atmospheric Administration and the lead scientist for the U.S. Billion-Dollar Weather and Climate Disasters research. The views expressed are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Board of Governors of the Federal Reserve System or of any other person associated with the Federal Reserve System. Return to text

2. See National Oceanic and Atmospheric Administration, National Centers for Environmental Information (2022), "Billion-Dollar Weather and Climate Disasters: FAQ," webpage, https://www.ncei.noaa.gov/access/billions/faq. Weather events include droughts, flooding, freezes, severe storms, tropical cyclones, wildfires, and winter storms. Return to text

3. See National Oceanic and Atmospheric Administration, National Centers for Environmental information (2022), "Billion-Dollar Weather and Climate Disasters: Summary Stats," webpage, https://www.ncei.noaa.gov/access/billions/summary-stats/US/1980-2022. Return to text

4. To estimate the cost of disasters, we take the midpoint of a range of damage estimates provided by NOAA here: https://www.ncei.noaa.gov/access/billions/time-series Return to text

5. We find similar results if we normalize damages by gross state product (GSP). Return to text

6. Since other entities (such as private insurers and the federal government) currently cover a large share of disaster damages, states with high levels of "fiscal vulnerability" in Figure 1 may not necessarily be vulnerable in practice. However, a long-run reliance on non-state-government entities may not be fiscally sustainable; for example, insurance companies may exit certain markets due to decreased profitability. Thus, we highlight this ratio to demonstrate the fiscal challenges that states may face if they are to cover a larger share of damages in the future. Return to text

7. Puerto Rico's tax revenues are reported on a fiscal year basis, and we calculate the ratio based on the period 2013-2020. Return to text

8. See Sonia I. Seneviratne, Xuebin Zhang, Muhammad Adnan, Wafae Badi, Claudine Dereczynski, Alejandro Di Luca, Subimal Ghosh, Iskhaq Iskandar, James Kossin, Sophie Lewis, Friederike Otto, Izidine Pinto, Masaki Satoh, Sergio M. Vicente-Serrano, Michael Wehner, and Botao Zhou (2021), "Chapter 11: Weather and Climate Extreme Events in a Changing Climate," in Climate Change 2021: The Physical Science Basis (Geneva: Intergovernmental Panel on Climate Change, August). Return to text

9. See National Oceanic and Atmospheric Administration, National Centers for Environmental Information (2022), "Billion-Dollar Weather and Climate Disasters: FAQ," webpage, https://www.ncei.noaa.gov/access/billions/faq. Return to text

10. See, e.g., AghaKouchak et al. (2020), "Climate Extremes and Compound Hazards in a Warming World," Annual Review of Earth and Planetary Sciences, Vol. 48, pp. 519—48; and "A Force of Nature: Hurricanes in a Changing Climate," by Angela Colbert, NASA's Jet Propulsion Laboratory, June 1, 2022. Return to text

11. See, e.g., Federal Emergency Management Agency, "Building Codes Save: A Nationwide Study – Losses Avoided as a Result of Adopting Hazard-Resistant Building Codes," (2020). Return to text

12. Underinsured is defined as holding some level of private insurance coverage, but not full scope coverage. Self-insured is defined as maintaining a fund to cover possible losses rather than purchasing an insurance policy. Return to text

13. Federal government costs are from crop and flood insurance payouts, FEMA's public and individual assistance programs, and wildfire suppression costs. State and local government costs are from presidential disaster declaration matches, a reduced supply of hydropower energy, infrastructure damage, and wildfire suppression costs. Return to text

14. See "Climate change is fueling an insurance crisis. There's no easy fix." Washington Post - By Maxine Joselow, Vanessa Montalbano - 06/27/2023. Return to text

15. See McKinsey Global Institute, "Will mortgages and markets stay afloat in Florida?" (2020), https://www.mckinsey.com/~/media/mckinsey/business%20functions/sustainability/our%20insights/will%20mortgages%20and%20markets%20stay%20afloat%20in%20florida/mgi-will-mortgages-and-markets-stay-afloat-in-florida.pdf. Return to text

16. See Solomon Hsiang, Robert Kopp, Amir Jina, James Rising, Michael Delgado, Shashank Mohan, D.J. Rasmussen, Robert Muir-Wood, Paul Wilson, Michael Oppenheimer, Kate Larsen, and Trevor Houser (2017), "Estimating Economic Damage from Climate Change in the United States," Science, vol. 356 (June), pp. 1362–69. Return to text

17. From early April to early May, Texas was affected by hailstorms (April 12–15) as well as tornadoes and severe storms (April 27–28 and May 2–4). Return to text

18. See National Oceanic and Atmospheric Administration, National Centers for Environmental Information (2022), "Billion-Dollar Weather and Climate Disasters: Climatology," webpage, https://www.ncei.noaa.gov/access/billions/climatology. Return to text

Brunetti, Celso, Benjamin Dennis, Gurubala Kotta, and Adam Smith (2023). "Analyzing State Resilience to Climate Change," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, September, 07, 2023, https://doi.org/10.17016/2380-7172.3342.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.