FEDS Notes

August 18, 2022

Are Stocks Pricing in Recession Risks? Evidence from Dividend Futures1

Markus Ibert, Ben Knox, and Francisco Vazquez-Grande

Since the beginning of this year, broad equity price indexes around the world have declined significantly. In interpreting the declines, market commentaries have highlighted the risks to the economic outlook in the United States and other advanced economies. Given their significant declines, do equity prices now reflect the risks of an economic contraction? To shed light on this question, in this note we use dividend futures prices to derive high frequency market-implied growth expectations for 2022 and 2023 for four major advanced economies.

Dividend futures are claims to the dividends paid out by an equity index (e.g., the S&P 500 index) in a given year. As argued by the academic literature (see, e.g., Gormsen and Koijen 2020), these future contracts can be used to infer market-implied estimates of expected dividend and GDP growth. We document that, since the beginning of the year, expected dividends implied by dividend futures are about unchanged for 2022 and have modestly declined for 2023. In turn, these changes in expected dividends translate into moderate downward revisions to expected real GDP growth for this year and the next. We conclude that the declines in equity prices since the beginning of the year have been mostly driven by a revaluation of far-dated cash flows through a higher discount rate as opposed to changes in cash-flow expectations. Moreover, equity markets do not unequivocally price in a contraction in economic activity as of late June.

Extracting Dividend Expectations from Dividend Futures

We infer dividend growth expectations using dividend futures prices for the S&P 500 (the United States), the EuroStoxx 50 (the euro area), the FTSE 100 (the United Kingdom), and the Nikkei 225 (Japan). Similar to equity prices, dividend futures prices reflect both expectations about future dividends and equity risk premiums. However, in contrast to equity prices, which reflect expectations about dividends and risk premiums decades ahead, dividend futures reflect near-term expectations (see, e.g., Chen, Ibert, Vazquez-Grande 2020). To isolate the expected dividend component of dividend futures, we follow Martin (2017) and construct empirical measures of equity risk premiums. As these measures rely on the prices of index options, which are not actively traded for maturities longer than two years, we focus our analysis on expected dividends for 2022 and 2023 only.2

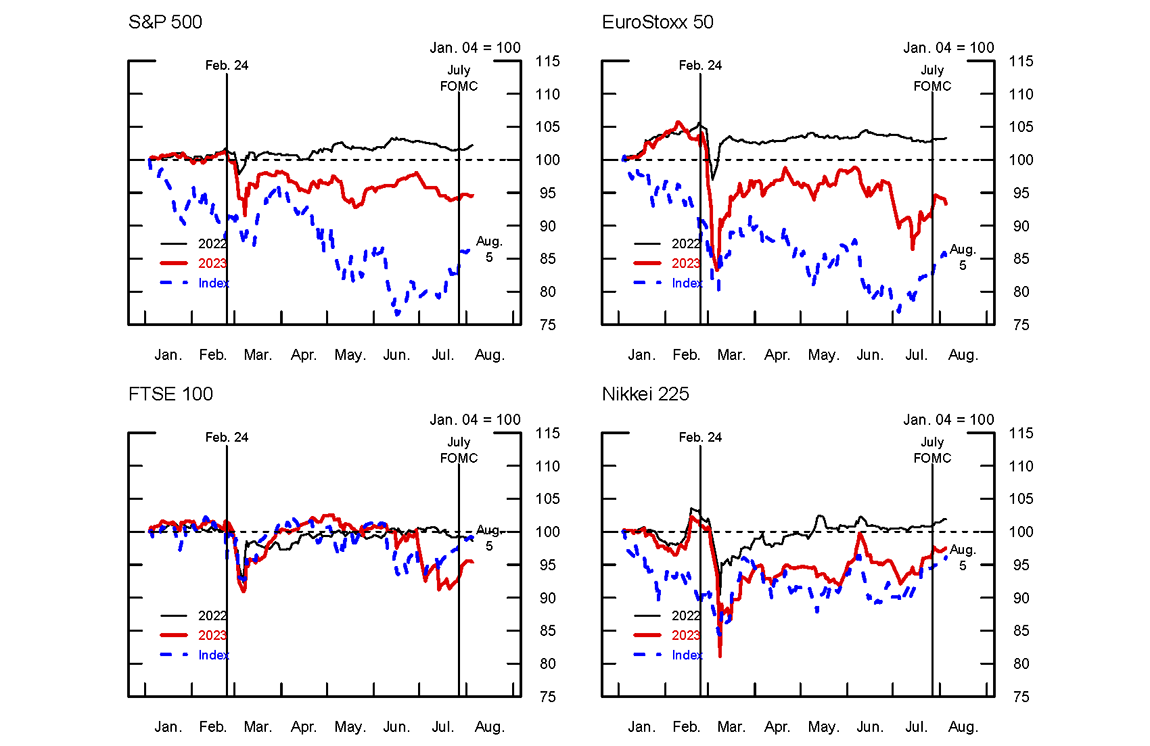

Figure 1 plots expected nominal dividends for 2022 and 2023 across advanced economies since the start of this year together with the corresponding broad equity indexes. Following Russia's invasion of Ukraine on February 24th, expected dividends fell significantly but recovered most of their losses soon thereafter. Expected dividends in the euro area suffered the largest declines, consistent with the euro area's greater exposure to the conflict. As of early August, expected nominal dividends for 2022 have increased or are about unchanged, while expected nominal dividends for 2023 have modestly declined on balance. Since expected inflation for 2022 and 2023 is elevated in most economies, expected real dividends have mostly declined. Meanwhile, broad equity price indexes in the United States and Europe have declined about 20 percent year-to-date. The significant declines in equity prices together with little changes to near-term expected dividends suggest that the declines in equity prices mostly reflect the significant rise in long-term interest rates since the beginning of the year as opposed to declining near-term growth expectations.

Source: Bloomberg; Board of Governors of the Federal Reserve System; Board staff calculations.

Inferring changes on GDP

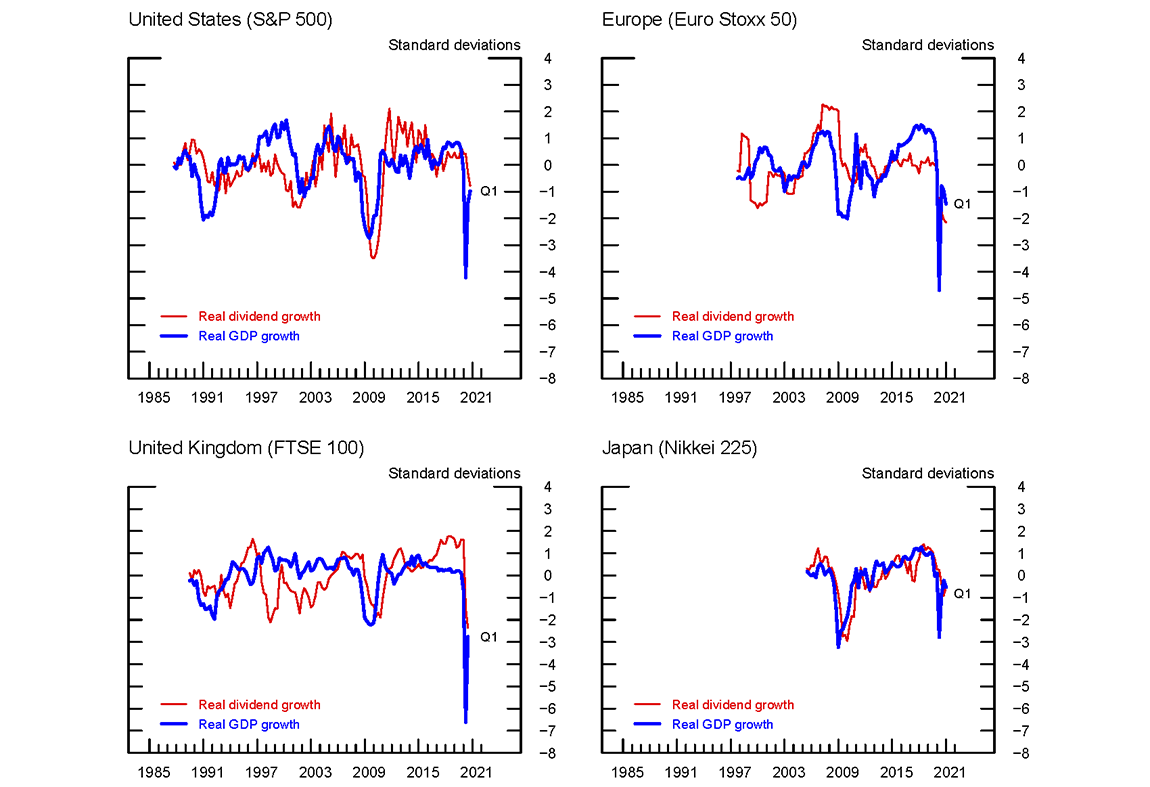

Expected dividends contain information about GDP, as they provide a signal about firms' profits, which in turn are an important component of GDP. Beyond this direct effect, they reveal information about firms' and investors' expectations of future economic conditions. Indeed, figure 2 shows a strong contemporaneous correlation between aggregate realized dividend and realized GDP growth across economies. To illustrate the relation between the two series at the business-cycle frequency, we have extracted the cyclical component of real dividends and real GDP using the methodology developed in Hamilton (2018). For our remaining analysis, we estimate the historical relationship between realized real dividend growth and real GDP growth using a simple regression model.3 We then map the estimated elasticities into changes in GDP growth expectations for this year and the next.4

Source: Bloomberg; Board of Governors of the Federal Reserve System; Board staff calculations.

As shown in table 1, revisions to expected real GDP growth in 2022 since the beginning of this year across advanced economies are about zero. This is because expected 2022 real dividends for broad equity indexes are, on net, about unchanged.5 In contrast, the moderate declines in expected real dividends for 2023 across the broad equity indexes we study translate into moderate downward revisions to real GDP growth for 2023 across advanced economies. For instance, the decline in expected 2023 real dividends translates into a 0.4-percentage-point and 0.9-percentage-point downward revision in 2023 GDP growth for the United States and the euro area, respectively.

Table 1: Changes in Expected Real GDP Growth

| Region | 2022 | 2023 |

|---|---|---|

| United States | 0 | -0.6 |

| Euro area | 0 | -1 |

| United Kingdom | -0.7 | -0.8 |

| Japan | 0.1 | -0.5 |

Note: All changes are from January 04, 2022 to August 05, 2022 and measured in percentage points. The elasticity between real dividend growth and real GDP growth is 0.06 for the United States, 0.08 for the euro area, 0.13 for the United Kingdom, and 0.10 for Japan. Changes refer to year-on-year growth rates.

Source: Board sta calculations, Bloomberg (dividend futures), Consensus Economics (survey inflation expectations).

Overall, these results indicate that equity markets price in only moderate downward revisions to expected dividend and GDP growth. By comparison, professional forecasters from Consensus Economics are less sanguine: they have on average marked their U.S. GDP growth forecasts downwards from 3.9% to 2.1% (1.8 percentage points) for 2022 and from 2.6% to 1.8% (0.8 percentage points) for 2023 since the beginning of this year.6 Should a recession materialize in 2022 or 2023, we suspect that expected dividends and equity prices have much further room to fall: as we have shown, dividends decline significantly whenever GDP declines.

References

Chen, Andrew Y. and Ibert, Markus and Vazquez-Grande, Francisco, The Stock Market–Real Economy "Disconnect": A Closer Look (October 14, 2020). FEDS Notes No. 2020-10-14-2.

Gormsen, Niels Joachim and Ralph S.J. Koijen, "Coronavirus: Impact on Stock Prices and Growth Expectations." Review of Asset Pricing Studies, 2020, 10 (4), 574-597.

Hamilton, James D., ''Why You Should Never Use the Hodrick-Prescott Filter'', The Review of Economics and Statistics, 2018, 100 (5), 831-843.

Knox, Benjamin and Vissing-Jorgensen, Annette, A Stock Return Decomposition Using Observables (March 1, 2022). FEDS Working Paper No. 2022-14

1. The authors work at the Board of Governors of the Federal Reserve System. We thank Nicholas von Turkovich, Jared Greufe and Salil Jajodia for excellent research assistance. All errors and omissions are our own responsibility. The views expressed in this note are solely those of the authors and should not be interpreted as reflecting the views of the Board of Governors of the Federal Reserve System or of anyone else associated with the Federal Reserve System. Return to text

2. The price of a n-period dividend strip is: $$$$P_{n,t} = \frac{E_t[D_{t+n}]}{(1+r^f_{n,t} + rp_{n,t})^n}$$$$

where $$ E_t[D_{t+n}]$$ is the expected n-period dividend, $$r^f_{n,t}$$, is the n-period risk-free rate, and $$rp_{n,t}$$ is the n-period dividend strip risk premium. The price of the n-period dividend futures contract is then $$$$ F_{n,t} = P_{n,t} \cdot (1+r^f_{n,t})^n $$$$,

where the present value of the n-period dividend strip is adjusted for the time value of money given that the futures price is a future value and not a present value. Rearranging, the expected dividend is approximately $$$$ E_t[D_{t+n}] = F_{n,t} \cdot (1+rp_{n,t}) $$$$.

To estimate this equation, we follow Knox and Vissing-Jorgensen (2022) and assume that the risk premium on a dividend strip is equal to the risk premium on the aggregate equity market. Return to text

3. Following Gormsen and Koijen (2020), we regress annual changes of real GDP growth on annual changes of real dividend growth using the following linear regression model $$$$ \Delta Y_t = \alpha + \beta \Delta D_t + \varepsilon_t $$$$.

We estimate this model for each country separately using OLS. The sample period for the US is from 1985-2021, for the EU from 1997-2021, for the UK from 1985-2021, and for Japan from 2005-2021. Return to text

4. We use the prevailing Consensus Economics inflation forecasts for each economy to convert changes in expected nominal dividends (observed from dividend futures prices and the risk premium adjustment) into changes in expected real dividend growth. Return to text

5. The exception is the United Kingdom for which we estimate a downward revision to GDP growth of 0.4 percentage points. This is because the estimated elasticity of real GDP growth to real dividend growth is largest for the United Kingdom, and because expected inflation for 2022 in the United Kingdom is elevated such that expected real dividends (as opposed to nominal dividends) have declined. Return to text

6. Change in survey forecast measured as the change from the January survey edition through to the July survey edition. Return to text

Ibert, Markus, Ben Knox, and Francisco Vazquez-Grande (2022). "Are Stocks Pricing in Recession Risks? Evidence from Dividend Futures," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, August 18, 2022, https://doi.org/10.17016/2380-7172.3176.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.