FEDS Notes

September 20, 2019

Collateralized Loan Obligations in the Financial Accounts of the United States

Matthew Guse, Woojung Park, Zack Saravay, and Youngsuk Yook1

Introduction

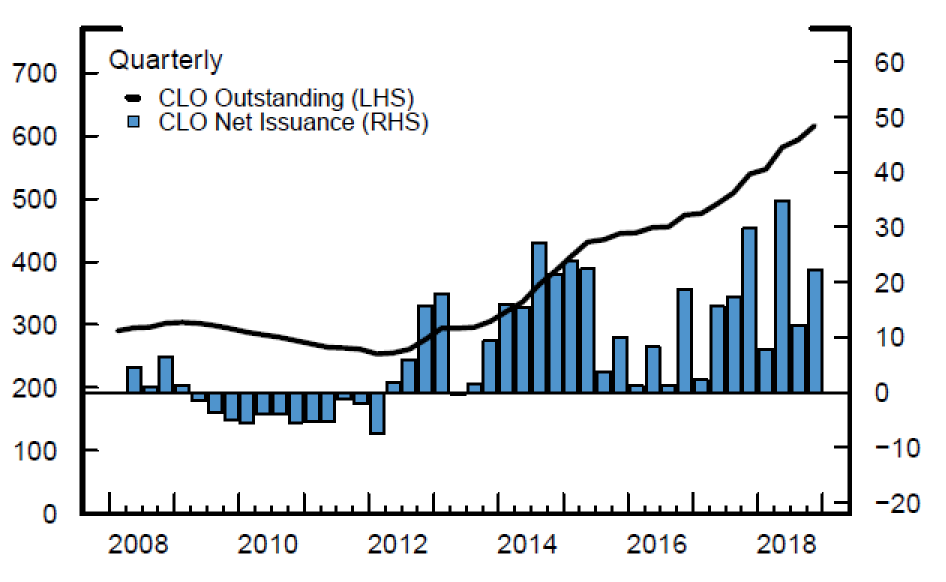

Collateralized Loan Obligations (CLOs) are structured securities backed primarily by pools of leveraged loans to businesses.2 CLOs have grown notably in recent years, from $264 billion in 2011 to $617 billion in 2018 (figure 1), drawing the attention of market participants and policymakers. This note describes how the Federal Reserve's Financial Accounts of the United States account for CLOs and discusses two new data series on CLOs that are introduced in the September 2019 publication of the Financial Accounts.

(Billions of dollars)

Source:Securities Industry and Financial Markets Association.

Background

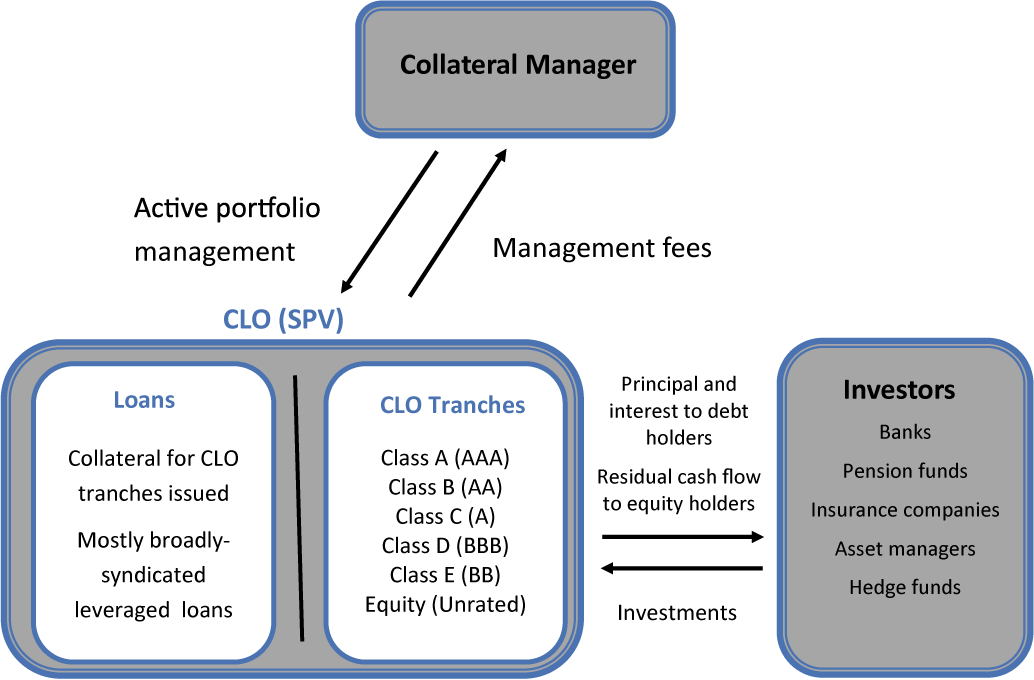

CLO securities are issued by special-purpose vehicles (SPVs) established to hold diversified portfolios of leveraged loans. Loans held in CLO issuers' portfolios are funded by the issuance of CLO securities, which are rated notes and unrated equity with varying degrees of credit risk, called "tranches," and are actively managed by third-party asset managers (figure 2).3 Investors in rated CLO debt tranches receive principal and interest payments, and investors in unrated subordinated tranches receive any residual cash flows after deal fees and the principal and interest payments to debt tranches are paid. U.S. investors in CLO securities are typically financial institutions such as banks, mutual funds, insurance companies, pension funds, and hedge funds.

Collateralized Loan Obligations in the Financial Accounts

CLOs typically involve two issuers--primary issuers incorporated in offshore tax havens, mainly the Cayman Islands, and domestic issuers incorporated in Delaware. The offshore incorporation allows CLOs to avoid being subject to income taxes at the corporate level, while co-issuance with a domestic issuer helps broaden the domestic investor base. Because CLO notes are typically co-issued, the Financial Accounts allocate part of CLO holdings of leveraged loans to domestic issuers of asset-backed securities (ABS) (table L.127), and the remainder to the rest of the world sector (table L.133). The next two sections further discuss how these are measured in the Financial Accounts.

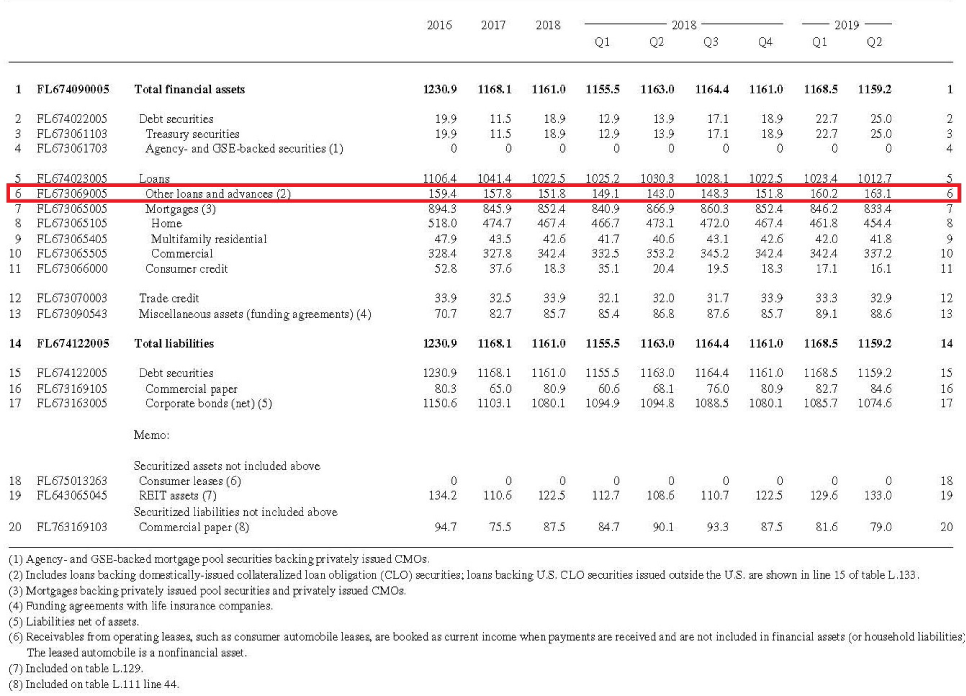

Collateralized Loan Obligations in Table L.127 ("Issuers of Asset-Backed Securities")

Leveraged loans held by domestic CLO issuers are shown on line 6 of table L.127. Federal Reserve Board staff use the lender and loan information in the Shared National Credit database to estimate the amount of loans held by domestic CLO issuers.4 As of 2019:Q2, domestic CLO issuers are estimated to hold about $163 billion of leveraged loans. An interactive guide to the Financial Accounts data on the Board's website provides more information on the sources and methodology used for these estimates and the others described in this note.

L.127 Issuers of Asset-Backed Securities (ABS)

Billions of dollars; amounts outstanding end of period, not seasonally adjusted

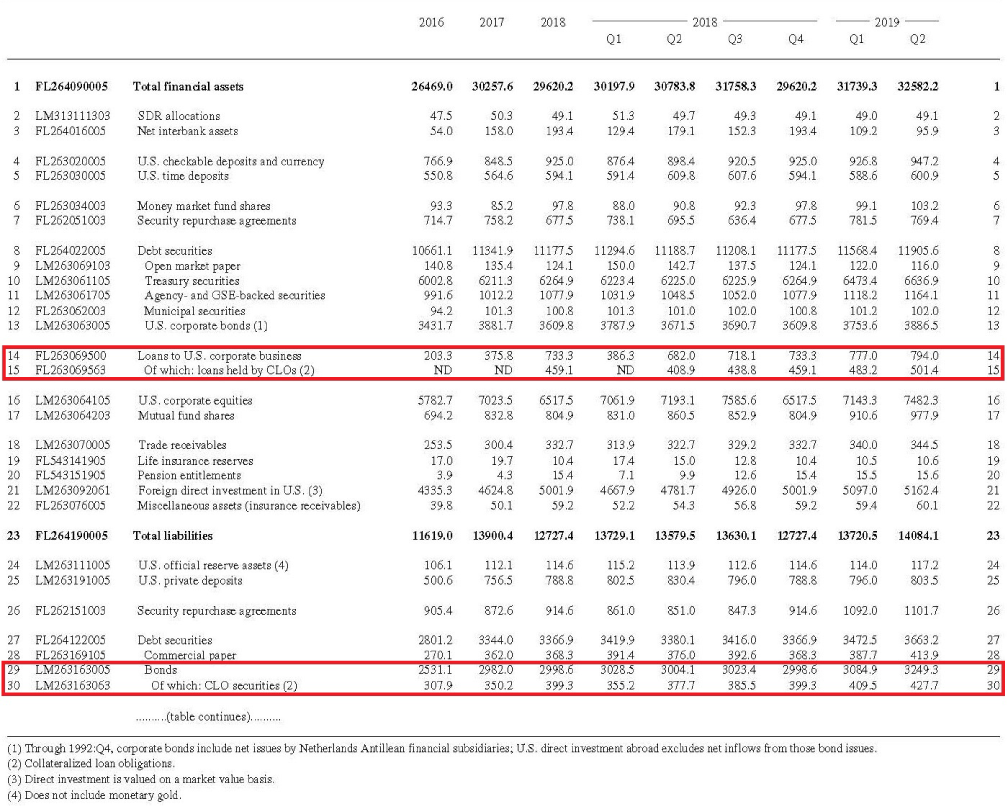

Collateralized Loan Obligations in Table L.133 ("Rest of the World")

Leveraged loans to U.S. firms held by foreign (e.g., Cayman) CLO issuers are included in line 14 of table L.133, along with other types of foreign loans to U.S. corporate business. Beginning with the September 2019 publication, table L.133 separately reports on line 15 the portion of the line-14 loans that are held by CLOs. This series, available from 2018:Q2 forward, is a staff estimate based on the Treasury International Capital (TIC) system's BL2 questionnaire, which covers foreign customers' U.S. dollar liabilities.5 For more information on CLOs in the TIC data, see the FEDS Notes article "Who Owns U.S. CLO Securities?"

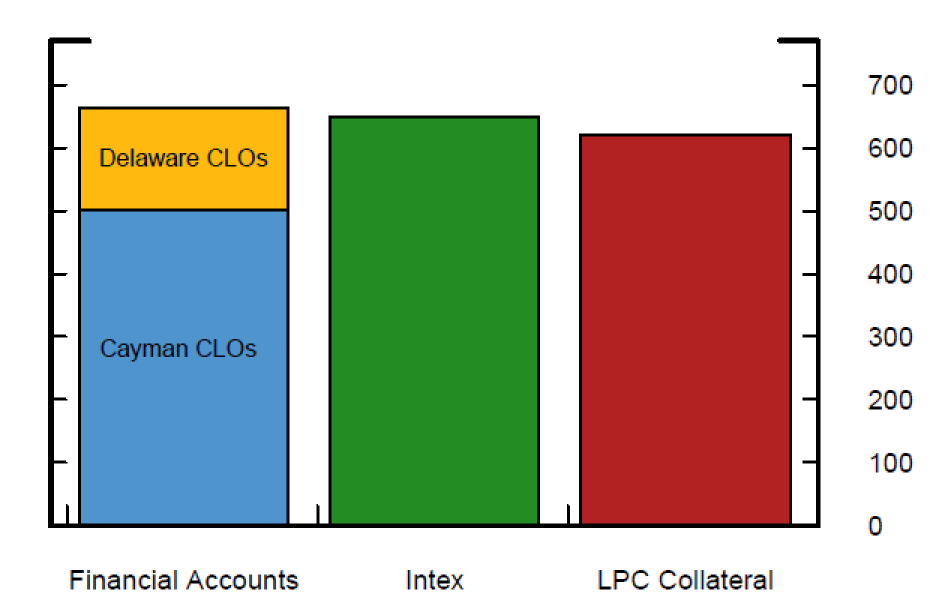

The new series on line 15 of table L.133 shows that Cayman CLO issuers held $501.4 billion of U.S. leveraged loans in 2019:Q2. This estimate, combined with the estimate of loans held by domestic CLO issuers (line 6 of L.127), indicates that together, domestic and foreign issuers of CLO securities held a total of $664.5 billion of leveraged loans in 2019:Q2. Figure 3 shows that this total is similar to estimates reported by other data vendors.6

L.133 Rest of World

Billions of dollars; amounts outstanding end of period, not seasonally adjusted

(Billions of dollars)

Source: Financial Accounts of the United States, Intex, Refinitiv LPC Collateral.

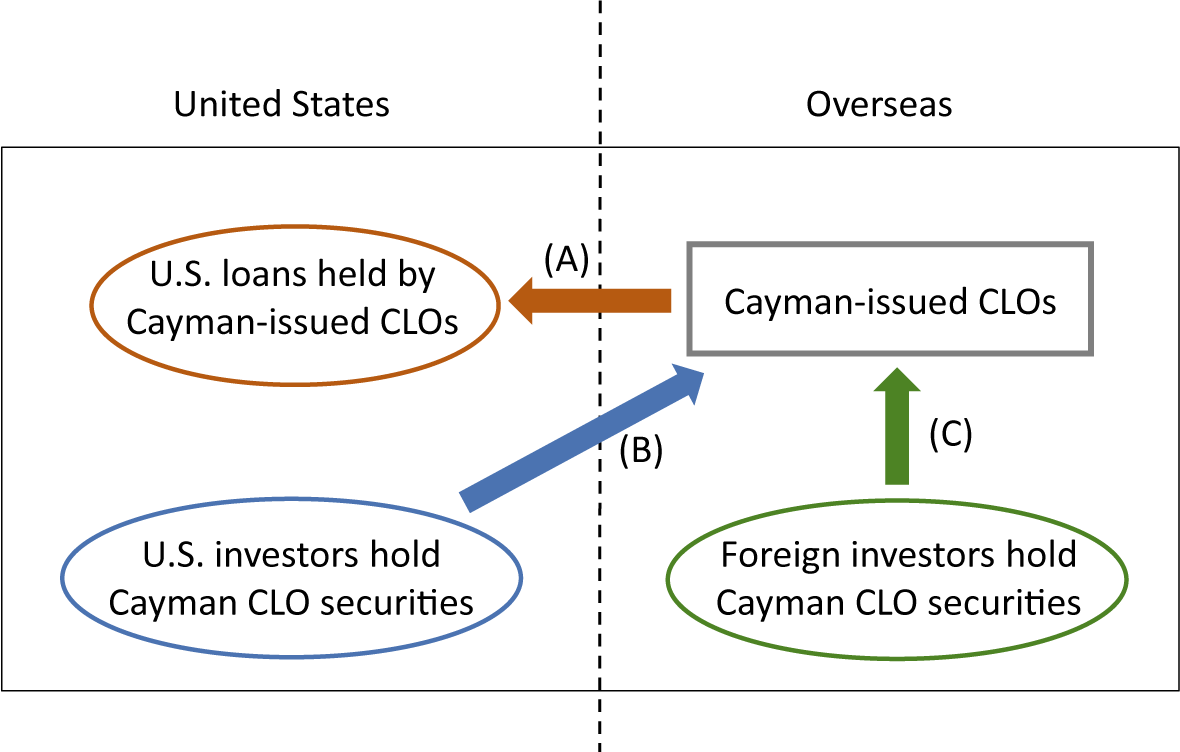

The majority of foreign-issued CLO securities are held by U.S. investors and thus are treated as liabilities of the rest of the world. These securities are included in line 29 of table L.133 as part of U.S. holdings of foreign bonds.7 Beginning with the September 2019 publication, Table L.133 separately reports in line 30 the portion of U.S. holdings of foreign bonds that are CLO securities. This series, available from 2014:Q4 forward, is a staff estimate based on information in TIC form SHC(A), which covers U.S. claims on foreign residents resulting from U.S. investment in foreign securities. The new series shows that of the $3,249.3 billion of foreign bonds held by U.S. residents in 2019:Q2, $427.7 billion were CLO securities. Note that CLO securities shown on table L.133's liability side ((B) in figure 4) are smaller than the CLOs' holding of leveraged loans in the table's asset side ((A) in figure 4) because foreign investors' holdings of Cayman-issued CLO securities ((C) in figure 4) are not a U.S. cross-border transaction and thus are not included in the Financial Accounts.

Conclusion

This note describes how CLOs are accounted for in the Financial Accounts of the United States. CLO issuers' holdings of leveraged loans are split based on their reported domiciles and shown in two separate tables: Those issued by domestic entities are shown in table L.127 and those issued by offshore entities are shown in table L.133. The note also highlights two new series that provide additional detail on CLO holdings and amounts outstanding in table L.133. An additional detail item in line 15 of the table reports how much of the rest of the world's loans to U.S. corporate business are held by offshore-issued CLOs, and another additional detail item in line 30 of the table reports how much of the offshore bonds are held by U.S. investors are CLO securities.

References

Liu, Emily, and Tim Schmidt-Eisenlohr (2019). "Who Owns U.S. CLO Securities?" FEDS Notes. Washington: Board of Governors of the Federal Reserve System, July 19, https://doi.org/10.17016/2380-7172.2423.

S&P Global Market Intelligence (2018). "S&P Global Ratings' CLO Primer," S&P Global Ratings, September 21.

1. Guse, Saravay, and Yook are at the Board of Governors of the Federal Reserve System, and Park is at the Federal Reserve Bank of New York. We thank Marco Cagetti, Elizabeth Caviness, Emily Liu, Susan McIntosh, Maria Perozek, Paul Smith, Kamila Sommer, and Bryce Turner for their helpful comments. Return to text

2. This FEDS Note only considers U.S. CLOs. Leveraged loans are secured loans typically provided to non-investment grade or unrated business borrowers. Return to text

3. See S&P Global Market Intelligence (2018) for additional information. Return to text

4. The Shared National Credit database contains supervisory data on syndicated loans and is governed by an interagency agreement among the Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency. Return to text

5. The TIC data reporting system is required by law and is designed to collect reliable information on cross-border portfolio capital. The BL2 questionnaire was revised in 2018:Q2, resulting in improved reporting of CLOs. Return to text

6. CLOs' holdings of leveraged loans are generally smaller than total CLO assets under management, which often include a small amount of cash and other securities in addition to leveraged loans. Return to text

7. Note that, despite the name, the so-called "equity" tranche of CLO securities is typically structured as a subordinated or income note security, so it is included along with other tranches of CLO securities under debt securities in Table L. 133. Return to text

Guse, Matthew, Woojung Park, Zack Saravay, and Youngsuk Yook (2019). "Collateralized Loan Obligations in the Financial Accounts of the United States," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, September 20, 2019, https://doi.org/10.17016/2380-7172.2447.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.