FEDS Notes

March 25, 2022

(Don't Fear) The Yield Curve, Reprise

Eric C. Engstrom and Steven A. Sharpe1

Introduction

In recent months, financial market perceptions about the future path of short-term interest rates have evolved amidst signals from policymakers suggesting that reduced monetary policy accommodation is in the offing. As with previous episodes of policy tightening, most recently in 2018, one can hear an attendant rise in the volume of commentary about a decline in the slope of the yield curve and the risk of "inversion," whereby long-term yields fall below shorter-maturity yields. And echoing previous episodes, one measure of the yield curve that seems to draw inordinate attention is the difference between yields on the 10-year and 2-year Treasury bonds, often referred to as the "2-10 spread".

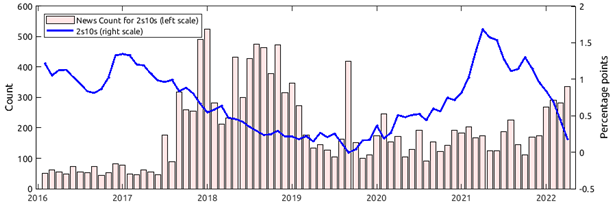

Notes: News count data for March 2022 is estimated using available daily data through 3/18. 2-10 spread data for March corresponds to 3/18.

Sources: Federal Reserve Bank of New York, Bloomberg, author calculations.

The attention garnered by the 2-10 spread in recent years is illustrated in Figure 1, where vertical bars plot the number of financial news articles mentioning the 2-10 spread. The decline in the level of the 2-10 spread itself, illustrated by the blue line, to less than 0.5 percent in recent months appears to be sparking interest in the financial press of late, though apparently still modest compared to the crescendo of attention in 2018. Is such attention warranted? It may seem so in light of the academic literature pioneered by Campbell Harvey in his 1986 dissertation, which documents that recession prediction models linked to the term structure of interest rates have substantial empirical success. The financial press maintains a particularly wary eye on inversions of the 2-10 spread. For instance, Investopedia claims that that "[inversion of] the 10-year to two-year Treasury spread is one of the most reliable leading indicators of a recession within the following year."

To the contrary, we have provided statistical evidence indicating that the perceived omniscience of the 2-10 spread that pervades market commentary is probably spurious. In particular, our similarly titled white paper (Engstrom and Sharpe, 2018) demonstrated that, historically, the 2-10 spread and its inversions would have provided no incremental information about future economic conditions if one were monitoring a very different measure of the Treasury yield curve, one with a much more transparent interpretation. This measure, which we named the "near-term forward spread," is based entirely on yields from Treasury bonds with maturities shorter than two years. We subsequently expanded the analysis in an article published in the Financial Analysts' Journal3 (Engstrom and Sharpe, 2019), showing that our near-term forward spread had substantial predictive power not only for the chances of recession, but also for both the pace of GDP growth and the returns earned on stocks over the subsequent four-quarter period, whereas the 10-2 spread again conveyed no incremental information for any of these outcomes.

Perhaps the more interesting insight from this analysis was, unlike for the 2-10 yield spread, there is an obvious interpretation for why the near-term forward spread has predictive power. This spread closely mirrors—and can be interpreted as—a measure of market participants' expectations for the trajectory of Federal Reserve interest rate policy over the coming year and a half. Indeed, it is very similar to the "market-implied path (of the expected Fed policy rate)" drawn from federal funds futures rates, which is widely monitored by investors and Fed watchers. When investors (perhaps appropriately) fear an economic slowdown or especially a downturn within the next year or so, they likewise tend to expect the Federal Reserve to begin lowering its target policy rate in the not-too-distant future. This generates a low, sometimes even negative, value of the near term forward spread. Although the 2-10 spread is influenced by these dynamics as well, that measure is also buffeted by other significant factors such as risk premiums on long-term bonds.

Ultimately, we argue there is no need to fear the 2-10 spread, or any other spread measure for that matter. At best, the predictive power of term spreads is a case of "reverse causality." That is, term spreads predict recessions because they impound pessimistic—often accurately pessimistic—expectations that market participants have already formed about the economy, and thus an expected cessation in monetary policy tightening.4 Thus, term spreads could have little or no economic impact in and of themselves. Nevertheless, as FDR might have pointed out, it can only make things worse if investors not only fear the prospect of a recession, but at the same time, are spooked by that fear itself, which is mirrored in inverted term spreads.

In the remainder of this note, we review the historical pattern of yields spreads and recessions. In doing so, we provide a narrative on some key developments that followed the publication of our study, which also highlights how statistical regularities can be misleading. Finally, we briefly apply the implications of our analysis to observations about the current state of the yield curve.

The historical pattern of yield spreads and recessions

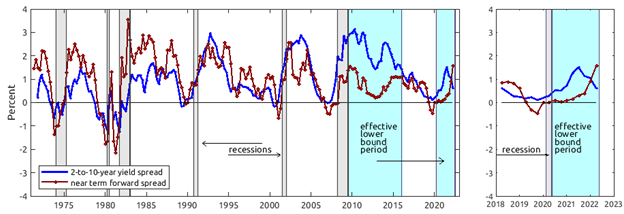

Figure 2 plots the long-term historical time series for both the 2-10 spread and the near-term forward spread. Concretely, we define the 2-10 spread in the usual manner:

$$$$ 2s10s_t = y^{40}_t – y^8_t $$$$

where $$2s10s_t$$ is the 2-10 spread and $$ y^{40}_t $$ and $$ y^8_t $$ are the zero-coupon yields on Treasury securities at 40- and 8-quarter horizons, respectively. 5 The near-term forward spread is defined as:

$$$$ ntfs_t = fwd^6_t – y^1_t $$$$

where $$ ntfs_t$$ is the near-term forward spread, $$ fwd^6_t$$ is the six-quarter ahead 1-quarter Treasury rate6 and $$y^1_t$$ is the 1-quarter Treasury yield.

Notes: The light gray shading represents recession dates, and the light blue shading represents the effective lower bound period.

Sources: Federal Reserve Bank of New York, NBER, author calculations.

The left panel of Figure 1 illustrates that the two measures have tended to move broadly in tandem over the past several decades. Both have regularly inverted, or nearly so, in advance of recessions, which are indicated by the gray shading. That said, the near-term forward spread has provided a demonstrably cleaner signal of recessions, which we first documented in Engstrom and Sharpe (2018).

What about 2019?

Shortly after that article went public, in early 2019, the near-term forward spread inverted, providing an instructive, even if misleading, example of the mechanism by which the near-term forward spread appears to forecast recessions. Magnified in the right panel of Figure 1, this episode will also forevermore provide an arguably spurious boost to the statistical evidence for the power of term spreads to prediction recessions.

During the first quarter of 2019, concern grew regarding the decelerating economy. For instance, the minutes from the March 2019 FOMC meeting stated, "… growth of economic activity had slowed from its solid rate in the fourth quarter… Participants cited various factors as likely to contribute to the step-down, including slower foreign growth and waning effects of fiscal stimulus."7 Unsurprisingly, market participants began to expect that more accommodative monetary policy could be in the offing. Such expectations, which caused the near-term forward spread to decline and eventually turn negative, were subsequently ratified in July 2019, when the FOMC lowered the target range for the federal funds rate. At the time, Chair Powell stated "[The lower target for the federal funds rate] is intended to insure against downside risks from weak global growth and trade policy uncertainty, to help offset the effects these factors are currently having on the economy…"8

Whether the incrementally more accommodative monetary policy that ensued would have been sufficient to prevent a recession in the face of those headwinds is unknowable because, soon after, the COVID-19 pandemic slammed the economy. Of course, that development was entirely unexpected as of mid-2019 and just as surely not predicted or caused by any term spread, but it produced the steepest contraction in economic activity since the Great Depression. Nonetheless, going forward, pure statistical analysis will give credit, where credit is not due, to the near-term yield spread, not to mention other spread measures including the 2-10 spread, for predicting the Covid recession.

What about now?

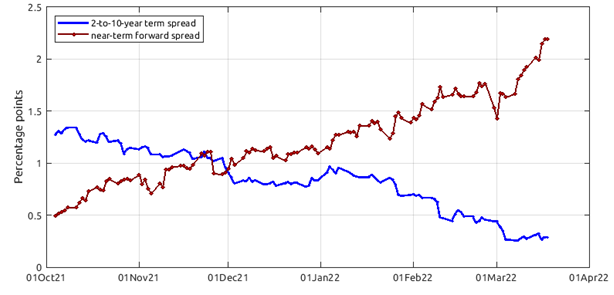

Figure 3 shows the recent evolution of the 2-10 spread and the near-term forward spread.

Sources: Federal Reserve Bank of New York, author calculations.

While both the 2-10 spread and the near-term forward spread were hovering at around 1 percentage point late last year, the near-term forwad spread has roughly doubled to over 2 percentage points while the 2-10 spread has fallen to a recent level around 1/4 percentage points. The monetary and macroeconomc narratives around the climb in the near-term forward spread are straightforward, and well reflected in the postmeeting statement from January 2022, which concluded "With inflation well above 2 percent and a strong labor market, the Committee expects it will soon be appropriate to raise the target range for the federal funds rate."9 Clearly, market participants have ancitipated the pivot towards removal of monetary policy accomodation and the near-term forward spread has moved up accordingly.

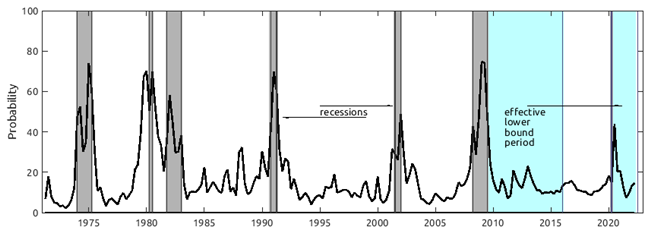

Of course, it is conceivable that market participants expect both policy tightening as well as an elevated probability of recession in the near term, but the Survey of Professional Forecasters, shown in Figure 4, suggests otherwise. Averaged across respondents, the mean probabilities that the economy will be in recession in the next quarter has edged up recently but it remains below 20 percent and close to its long-run median level.10

Notes: Recession probability is for the subsequent calendar quarter. The dark gray shading represents recession dates, and the light blue shading represents the effective lower bound period.

Sources: Survey of Processional Forecasters and NBER.

What of the recent decline in the 2-10 spread shown in Figure 3? One simple explanation for the decline is that market participants do not anticipate that the FOMC will seek to increase short term interest rates much beyond a horizon of around six quarters. (Again, in part this spread reflects the dynamics expected in near-term yields.) Another ingredient could be that the neutral short term interest rate is expected to be low by historical standards. A level of the 2-10 spread around zero is consistent with such expectations. Another explanation for a near inversion of the 2-10 spread is that inflation over the next two years is expected to be higher than during the subsequent eight.11 That naturally pushes up two-year (nominal) yields relative to ten-year (nominal) yields, compressing the spread. Neither of these two explanations require an elevated probability of recession.

Conclusion

It is not valid to interpret inverted term spreads as independent measures of impending recession. They largely reflect the expectations of market participants. Among various terms spreads to consider, the 2-10 spread offers a particularly muddled view. Especially in the present circumstancs when the 2-10 spread is very much out of step with the near-term forward spread, which offers a much more precise view of market expectations over the next year and a half, it is difficult to concoct a reason to be concerned about the flattening of the 2-10 spread. In contrast, if and when the near-term spread does contract, we know that investors will then be expecting a cessation in monetary policy tightening. While such a shift in expectations could well be precipitated by future concerns about a recession, that need not be the case. A more benign cause would be a marked easing in inflation and inflation expectations that allow for a cessation of policy firming.

References

English, William B., Skander Van den Heuvel and Egon Zakrajšek (2018), "Interest Rate Risk and Bank Valuations," Journal of Monetary Economics, vol. 98, issue C, ppg. 80-97.

Engstrom, Eric C. and Steven A. Sharpe (2018), "(Don't Fear) the Yield Curve," FEDS Notes (Washington: Board of Governors of the Federal Reserve System, June 28).

Engstrom, Eric C. and Steven A. Sharpe (2019), "The Near-Term Forward Yield Spread as a Leading Indicator: A Less Distorted Mirror," Financial Analysts Journal, vol. 75, no. 4, ppg. 37-49.

Gurkaynak, Refet, Sack, Brian, and Jonathan Wright (2007), "The U.S. Treasury Yield Curve: 1961 to the Present," Journal of Monetary Economics, vol. 54(8), pp. 2291-2304.

Harvey, Campbell, 1986, “Recovering Expectations of Consumption Growth from an Equilibrium Model of the Term Structure of Interest Rates,” Ph.D. dissertation, University of Chicago.

1. Staff working papers in the Finance and Economics Discussion Series (FEDS) are preliminary materials circulated to stimulate discussion and critical comment. The analysis and conclusions set forth are those of the authors and do not indicate concurrence by other members of the research staff or the Board of Governors. References in publications to the Finance and Economics Discussion Series (other than acknowledgement) should be cleared with the author(s) to protect the tentative character of these papers. Return to text

2. See, for instance, www.investopedia.com/terms/i/invertedyieldcurve.asp.Return to text

3. Full article hyperlink: The Near-Term Forward Yield Spread as a Leading Indicator: A Less Distorted Mirror (tandfonline.com) Return to text

4. Other authors have considered whether there may be a case for actual causality, under the hypothesis that inverted spreads could put pressure on the profits of banks, thereby tightening financial conditions and tilting the economy towards recession. English, Van den Heuvel, and Zakrajšek (2018) provide a comprehensive survey of the literature examining the link between bank profitability, bank equity valuation, and interest rates. They find evidence that increases in short-term interest rates or increases in the slope of the yield curve tend to depress bank stock prices, the latter effect seeming contrary to the notion that lower term slopes are bad for banks. Regarding the effects of shifts in the yield curve on measures of accounting profits for banks, they find some evidence that a steeper yield curve enhances bank interest margins, but the effect wanes after about two years. Return to text

5. All Treasury yield data are constructed from smoothed zero-coupon yield curves following the procedure of Gurkaynak, Sack, and Wright (2007). Return to text

6. The forward rate can be directly calculated from zero-coupon yields as $$fwd^{6}_t = 7yld^{7}_t – 6yld^{6}_t$$ Return to text

7. Board of Governors of the Federal Reserve System (2019). "Minutes of the Federal Open Market Committee, March 19–20, 2019," press release, April 10, https://www.federalreserve.gov/newsevents/pressreleases/monetary20190410a.htm. Return to text

8. Board of Governors of the Federal Reserve System (2019). "Federal Reserve Issues FOMC Statement," press release, July 31, https://www.federalreserve.gov/newsevents/pressreleases/monetary20190731a.htm. Return to text

9. Board of Governors of the Federal Reserve System (2022). "Federal Reserve Issues FOMC Statement," press release, January 26 https://www.federalreserve.gov/newsevents/pressreleases/monetary20220126a.htm. Return to text

10. Survey-based subjective probabilities of recession from the SPF remain low by historical standards at all horizons queried (up to four). Return to text

11. At the time of this writing TIPS-based inflation compensation is substantially greater at the 2-year horizon, around 4½ percentage points than at the 10-year horizon, around 3 percentage points. Return to text

Note: This Note was edited Aug. 5, 2022 to include complete attributions for several references to other research.

Engstrom, Eric C., and Steven A. Sharpe (2022). "(Don't Fear) The Yield Curve, Reprise," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, March 25, 2022, https://doi.org/10.17016/2380-7172.3099.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.