FEDS Notes

March 08, 2019

The Green Dividend Dilemma: Carbon Dividends Versus Double-Dividends

Stephie Fried, Kevin Novan, and William Peterman

There is broad consensus that the most efficient way to reduce the flow of carbon into the atmosphere is by taxing carbon emissions.1 By raising the price of carbon-emitting energy sources, a carbon tax would flexibly incentivize households and businesses to reduce fossil fuel consumption and substitute towards cleaner energy sources. Importantly, a carbon tax would also generate a substantial stream of government revenue.2 This raises an important question – how should this revenue be used? In this note, we summarize findings from our recent research (Fried et al. (2018)) that examine this question.

One proposal garnering support from a number of economists is the Carbon Dividend proposal put forward by the Climate Leadership Council (CLC).3 The Carbon Dividend proposal calls for the U.S. federal government to institute a carbon tax and return the revenue "directly to U.S. citizens through equal lump-sum rebates." In contrast, the economic literature has consistently argued against the use of lump-sum rebates. Instead, previous academic studies suggest that it would be better to use the new stream of revenue to reduce pre-existing distortionary taxes on labor or capital income – a result referred to as the 'weak double-dividend hypothesis.'4

Do the insights from the existing double-dividend literature reveal that the CLC's Carbon Dividend proposal is misguided? In our recent research (Fried et al. (2018)) we find that the answer is no, lump-sum rebates can play an important role in reducing the costs incurred when adopting a carbon tax. In particular, we stress that the double-dividend literature has focused on the long-run welfare consequences of revenue-neutral carbon tax policies. While these studies can inform us about how future generations who are born into an economy with the carbon-tax policy in place will be affected, we find that they serve as poor guides for how the policy affects the current living generations (i.e. those who must institute the policy). Ultimately, we find that, compared to returning the carbon tax revenues by reducing labor or capital income taxes, lump-sum rebates would be far less welfare reducing among the current living population.

In Fried et al. (2018), we highlight that there are two key reasons why the welfare effect of a carbon tax policy on living generations and the effect on future generations in the long-run can differ. First, it takes time for the macroeconomy – and in particular, the capital stock – to adjust to a new tax policy. Second, the welfare effects of the policy can vary substantially over an individual's lifetime. The variation in the welfare impacts over the life-cycle plays a particularly important role for understanding how the current living population would be affected by a carbon tax policy. For example, consider a carbon tax policy in which the revenue is returned through a reduction in the labor income tax. An individual would directly benefit from the tax rebate while they are working, but not after they stop paying labor income taxes. Thus, individuals who are already retired when the tax policy is implemented – which represents a sizable share of the current living population – will not receive the direct benefits of the labor tax reduction.

To compare the effects on the living population versus the long-run welfare consequences of adopting alternative carbon tax policies, Fried et al. (2018) constructs a quantitative, overlapping generations model (OLG) that captures not only how an agent's labor, consumption, and savings decisions vary over their life-cycle, but also how these decisions differ across agents with different lifetime incomes. Using the model we study the welfare consequences of a 35 dollar per ton carbon tax combined with three different revenue recycling options. In particular, the revenue from this tax is either (1) returned in the form of uniform, lump-sum payments (consistent with the CLC proposal), (2) used to reduce the capital tax rate, or (3) used to lower the labor tax rate. We focus exclusively on the non-environmental welfare impacts – e.g., excluding any benefits stemming from improved air quality or reductions in the risks posed by climate change.

Table 1 reports the welfare consequences of the carbon-tax policy, measured by the consumption equivalent variation (CEV). The CEV measure reflects how much future consumption (in percentage terms) an agent is willing to give up, in expectation, in order to live in the economy with the carbon tax in place. Thus, a positive value of the CEV implies that agents are better off under the policy while a negative value implies that they are worse off. The first row indicates the average welfare effect of each policy among the current generations alive when the tax change is adopted.5 The second row reports the average long-run welfare effect of the policy for agents born in the future, after the policy is adopted. The first column of Table 1 summarizes the welfare effects if the carbon tax revenue is returned through equal, lump-sum rebate (consistent with the Carbon Dividend proposal). The second and third column report the effects if the revenue is used to lower the distortionary capital or labor tax rates (consistent with the recommendation from the double-dividend literature).

Table 1: Aggregate Welfare Effects (CEV, percent)

| Lump-sum Rebate | Capital Rebate | Labor Rebate | |

|---|---|---|---|

| Current generations | 0.26 | 0.06 | -0.63 |

| Future generations (steady state) | -1.26 | 0.29 | -0.33 |

The table reveals that the non-environmental welfare consequences of the policies differ meaningfully over time. Among agents born in the future steady state, the average welfare costs are minimized by using carbon tax revenues to reduce one of the pre-existing distortionary taxes. In fact, we find that using the carbon tax revenue to offset revenue generated by the capital tax can even lead to a welfare gain.6 This result echoes the findings presented in the previous double-dividend literature. In contrast, among the agents alive when the carbon tax policy is adopted, we find a very different pattern. In particular, we find that, among the three policies considered, recycling the carbon tax revenue through uniform, lump-sum rebates results in the largest increase in welfare among the current living population.

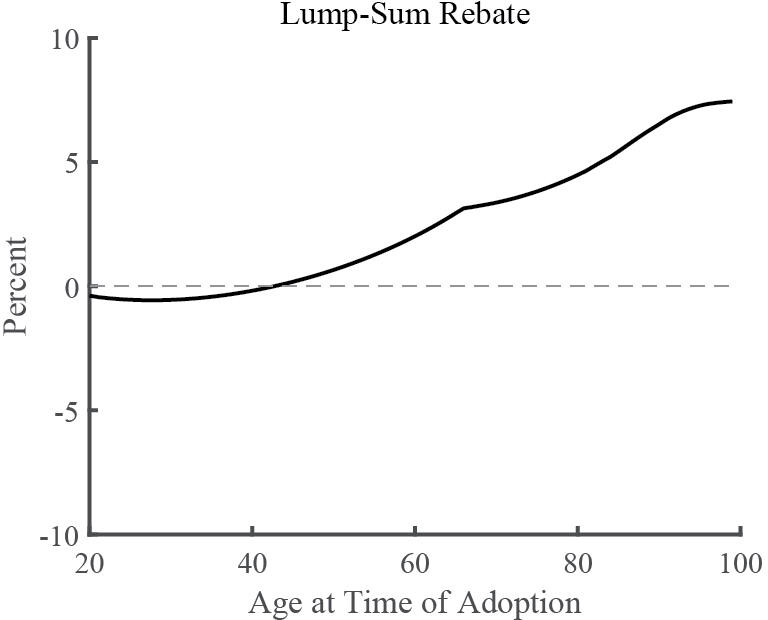

To highlight why the average welfare costs of the lump-sum rebate policy are so much lower among the current living agents, Figure 1 displays how the welfare impacts of the lump-sum rebate policy differ based on an agent's age at the time the policy is adopted. Similar to agents born in the future long-run steady state, agents that are very young (i.e., just entering the workforce) at the time the carbon tax and lump-sum rebate policy is adopted experience a small decrease in non-environmental welfare. In contrast, the policy increases the average welfare of agents older than 40 at the time of adoption. Ultimately, the sizable welfare gains achieved by the older living agents outweighs the small welfare costs incurred by the younger living agents. As a result, the lump-sum rebate policy increases the overall average welfare of the current living population along with increasing expected welfare for a majority of the living population.

Note: The figure displays the average non-environmental welfare effects of the carbon tax policy with the revenue returned through lump-sum rebates for each age cohort at the time the policy is adopted.

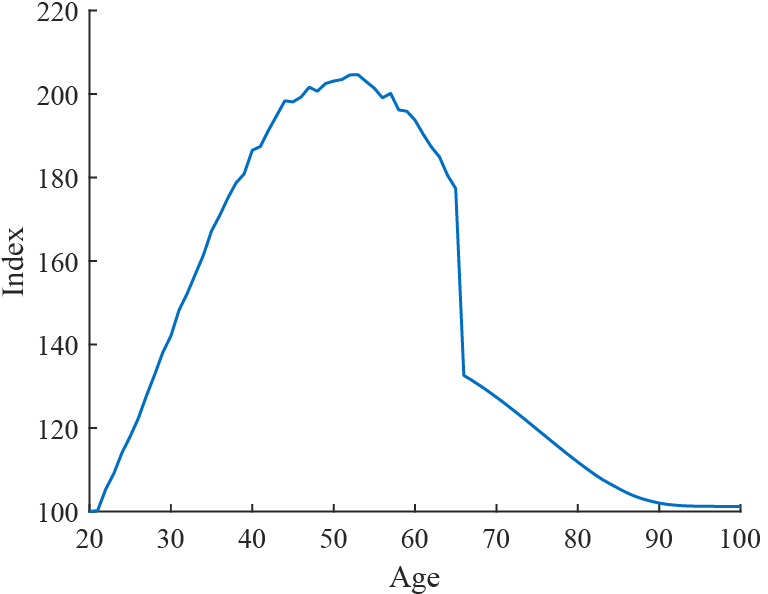

To understand why the welfare benefits from the lump-sum rebate policy increase with an agent's age, Figure 2 plots the total annual income an agent receives on average from all sources across different ages. Total income is humped shaped over the lifetime and falls sharply after retirement. By design, the lump-sum rebate provides cohorts the same payment regardless of income or age. Thus, for a young agent, the net present value of these lump-sum payments over their lifetime is relatively small compared to the net present value of agent's remaining lifetime income. In contrast, the lump-sum rebate represents a relatively larger windfall for older cohorts, who have lower total income over the remainder of their lifetime. Consequently, the lump-sum rebates lead to a sizable welfare increase for these older cohorts.

Note: The figure displays total income for agents of different ages, indexed to 100 for age 20. Total income is income from labor, returns to capital, Social Security, and accidental bequests.

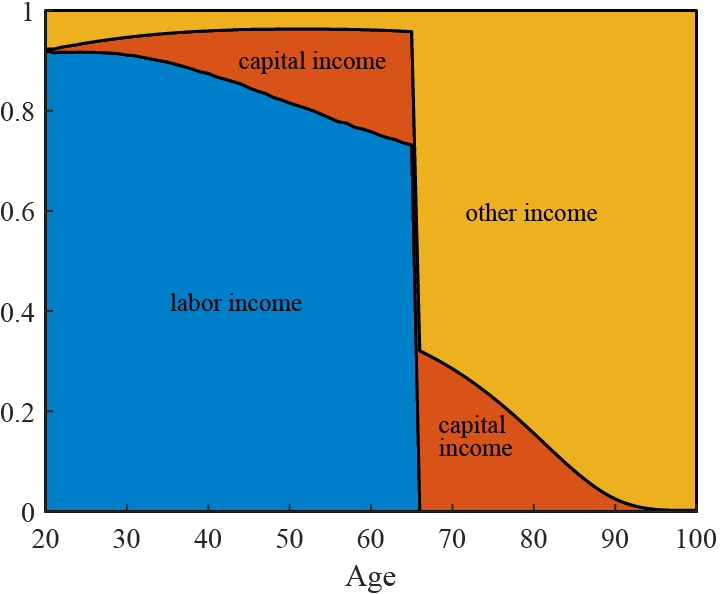

In contrast, the capital and labor tax rebates do not provide the same welfare benefits to the older living cohorts. To understand why, Figure 3 displays the average share of total income an agent receives from labor income, capital income, or other sources (e.g., Social Security) at different points in their lifetime. Importantly, the share of total income from labor declines as agents age and then falls to zero following retirement. Therefore, while a reduction in the labor tax rate would offset some of the burden a carbon tax imposes on young working agents, older agents would receive little to no benefit from a reduction in the labor tax rate. Similarly, Figure 3 highlights that, as agents age and deplete their savings, the share of income from capital steadily declines. Consequently, a reduction in the capital tax rate does not provide older living agents with a windfall as large as the lump-sum rebates.

Note: The figure displays the average share of total income agents of different ages receive from labor, capital, and other sources (e.g., Social Security).

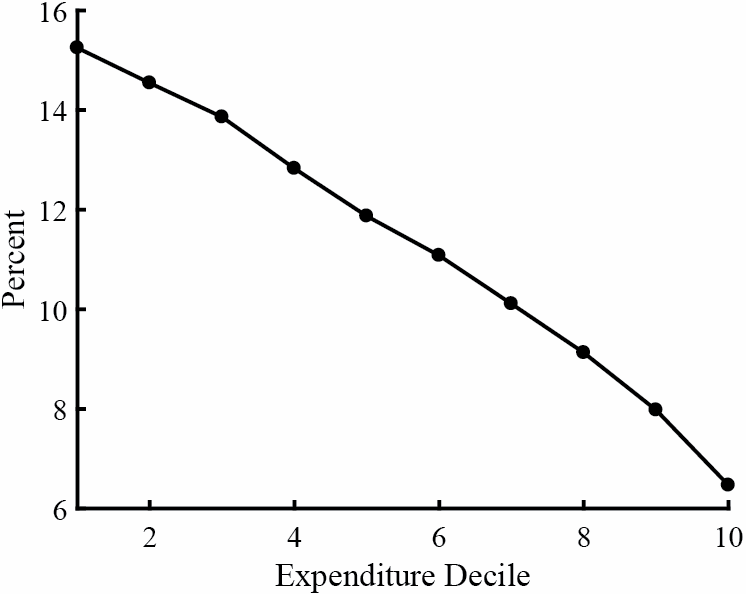

Aside from the average welfare impacts, another potentially important consideration is how the welfare costs of carbon tax policy are distributed across agents within a cohort. A carbon tax is generally thought to be regressive because low-income agents spend a larger share of their consumption on energy (Metcalf (2007), Mathur and Metcalf (2009)). Figure 4 plots the average energy budget share for each expenditure decile, within cohort, using data from the Consumer Expenditures Survey.7 Consistent with these previous findings, the average energy budget share falls considerably as average expenditures rise. At the extremes, energy expenditures are over 15 percent of total expenditures for the lowest decile but just over six percent for the highest decile. Thus, the carbon tax will be more burdensome for the households in the lower deciles. However, a uniform lump-sum rebate will be relatively larger compared to lifetime income for households who experience lower lifetime income. In Fried et al. (2018) we find that, while a carbon tax by itself would be regressive, when combined with a lump-sum rebate, the policy as a whole is progressive.

Note: Figure displays average energy budget shares by expenditure decile from the 1981-2003 Consumer Expenditures Survey. Energy expenditures include household expenditures on electricity, natural gas, gasoline, and coal and oil in the home. We determine the average energy budget share for each decile conditional on the household's age. Specifically, we first calculate the average energy budget share for each decile within each age bin. Second, for each decile, we calculate a population weighted average across the age bins where the weights are determined by the share of the population in each bin.

It is important to reiterate that our analysis abstracts from the potential environmental benefits achieved by implementing a carbon tax policy. However, the future generations will benefit from the reduction in carbon emissions taken by the current generations. The current generations, particularly the old, do not see these benefits. Thus, enacting a carbon tax policy with lump-sum rebates that are "best" for the living generations, but not "best" for the future generations, provides a channel through which the future agents can compensate the living agents for reducing their carbon emissions.

References

Baumol, William J. and Wallce E. Oates, The Theory of Environmental Policy, Cambridge University Press, 1988.

Bovenberg, Lans, "Green Tax Reforms and the Double Dividend: An Updated Reader's Guide," International Tax and Public Finance, 1999, 6(3), 421–443.

CBO, "Reducing the Deficit: Spending and Revenue Options," Technical Report, United States Congressional Budget Office March 2011.

Dales, John H., Pollution, Property, and Prices: An Essay in Policy-Making and Economics, Vol. 83, University of Toronto Press, 1968.

De Mooij, Ruud and Lans Bovenberg, "Environmental Taxes, International Capital Mobility and Inefficient Tax Systems: Tax Burden versus Tax Shifting," International Tax and Public Finance, 1998, 5(1), 7–39.

Dinan, Terry and Diane Rogers, "Distributional Effects of Carbon Allowance Trading: How Government Decisions Determine Winners and Losers," National Tax Journal, 2002, 199–222.

Fried, Stephie, Kevin Novan, and William B Peterman, "The Distributional Effects of a Carbon Tax on Current and Future Generations," Review of Economic Dynamics, 2018, 30, 30–46.

Fullerton, Don and Garth Heutel, "The General Equilibrium Incidence of Environmental Taxes," Journal of Public Economics, 2007, 91, 571–591.

Goulder, Lawrence, "Environmental Taxation and the Double Dividend: A Reader's Guide," International Tax and Public Finance, 1995, 2(2).

Hassett, Kevin, Aparna Mathur, and Gilbert Metcalf, "The Incidence of a U.S. Carbon Tax: A Lifetime and Regional Analysis," Energy Journal, 2009, 30(2), 157–180.

Horowitz, John, Julie-Anne Cronin, Hannah Hawkins, Laura Konda, and Alex Yuskavage, "Methodology for Analyzing a Carbon Tax," Technical Report, United States Department of the Treasury, Office of Tax Analysis, Washington D.C. 2017. Working Paper 115.

Metcalf, Gilbert, "A Proposal for a US Carbon Tax Swap: An Equitable Tax Reform to Address Global Climate Change," Hamilton Project, Brookings Institute, 2007.

Montgomery, David W., "Markets in Licenses and Efficient Pollution Control Programs," Journal of Economic Theory, 1972, 5 (3), 395–418.

Parry, Ian, "Are Emissions Permits Regressive?," Journal of Environmental Economics and Management, 2004, 47(2), 364–387.

Parry, Ian and Roberton Williams, "What Are the Costs of Meeting Distributional Objectives for Climate Policy?," B.E. Journal of Economic Analysis & Policy, 2010, 10(2).

Pigou, Arthur C., "The Economics of Welfare," London: Macnillam, 1920.

1. An efficient carbon price could be established directly through a carbon tax or through a cap-and-trade program. For examples see Pigou (1920), Dales (1968), Montgomery (1972), Baumol and Oates (1988). Return to text

2. A report from the U.S. Department of the Treasury (Horowitz et al. (2017)) estimates that a carbon tax starting at $49 per ton of CO2 in 2019, and rising to $70 by 2028, would generate $2.2 trillion over ten years. Similarly, estimates from the U.S. Congressional Budget Office suggest that setting a modest CO2 price of $20/ton would raise $1.2 trillion in revenue during the first decade the policy is in place (CBO (2011)). Return to text

3. See opinion piece, "Economists Statements' Statement on Carbon Dividends," January 16th, 2019 Wall Street Journal. Return to text

4. For example, Goulder (1995), de Mooij and Bovenberg (1998), and Bovenberg (1999) find that the most efficient way to use the revenue is to reduce these distortionary taxes. Previous studies also highlight that the revenue recycling method can substantially alter the distribution of the welfare changes across income groups (Fullerton and Heutal (2007), Dinan and Rogers (2002), Metcalf (2007), Parry (2004), Parry and Williams (2010)). Return to text

5. The CEV for the living population captures the effect of the policy over their remaining lifetimes, and thus, varies based on the cohort's age at the time the policy is adopted. Specifically, to calculate the CEV of the policy for a given age cohort, we compute the uniform percent change in consumption across all agents in the cohort that would be necessary, in every remaining period of their lifetimes, so that the cohort's average expected utility is the same as if they were to live the rest of their lives in the baseline steady state. The aggregate CEV among the living population is the weighted average of the CEVs for each living age cohort. Each cohort's weight is the share of the expected net present value of the remaining consumption for that cohort relative to the total remaining lifetime consumption for all living cohorts. Therefore, the weights account for the fact that the resources required to fund a one percent increase in a younger cohort's remaining lifetime consumption exceed the resources needed to fund a one percent increase in an older cohort's remaining lifetime consumption. Return to text

6. We find that in the steady state, rebating the revenue by lowering the labor tax leads to a small decrease in the welfare. These results indicate that, in this model, the capital tax is more distortionary than the labor tax. Return to text

7. See Fried et al. (2018) for discussion of how deciles were calculated. Return to text

Fried, Stephie, Kevin Novan, and William Peterman (2019). "The Green Dividend Dilemma: Carbon Dividends Versus Double-Dividends," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, March 8, 2019, https://doi.org/10.17016/2380-7172.2340.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.