FEDS Notes

September 08, 2023

Hedge Fund Treasury Exposures, Repo, and Margining

Ayelen Banegas and Phillip Monin1

Hedge funds have become among the most active participants in U.S. Treasury (UST) markets over the past decade. As a result, the financial stability vulnerabilities associated with their leveraged Treasury market exposures, which are facilitated by low or zero haircuts on their Treasury repo borrowing, have become more prominent. In this note, we use regulatory data from the SEC Form PF as of December 2022 to document recent trends in hedge funds' Treasury exposures and repo financing, and also to examine the implications for hedge fund repo borrowing and leverage of a hypothetical 200 basis point minimum haircut on Treasury repo.

Overall, we find that hedge funds' UST gross exposures and repo borrowing are elevated, though below the levels observed leading up to the COVID-19 pandemic. We document that UST and repo exposures are concentrated in a small group of highly leveraged funds, with the 50 funds with the largest Treasury exposure accounting for 83 percent of qualifying hedge funds' (QHFs) UST exposure and 89 percent of repo borrowing at the end of 2022.2 Also, we find that hedge funds face low haircuts on their repo financing transactions, with about 74 percent of total repo borrowing volume transacted at zero or negative haircuts. Furthermore, we document that average balance sheet leverage of funds transacting at zero or negative haircuts is significantly higher than that of the average QHF.

In addition, our analysis provides a first step estimate of how a floor on repo haircuts could affect hedge funds' activities in UST markets. We estimate that hedge funds had $553 billion in repo borrowing collateralized by UST securities as of December 2022, supported by $9.9 billion in hedge fund capital. Our empirical estimation shows that if haircuts on UST repo borrowing were subject to a hypothetical 200 basis points floor, funds in the aggregate would likely need an additional $12.4 billion in capital to support their existing repo borrowing levels, which most funds could cover with their unencumbered cash. We also show that this higher capital requirement reduces the effective leverage funds have in UST repo from 56x to 25x, negatively impacting hedge funds' return on equity on their relative value trades financed by UST repo. As a result, pricing spreads in hedge fund trades would have to about double to remain at their current profitability levels.

Hedge funds' Treasury exposures are large and highly concentrated

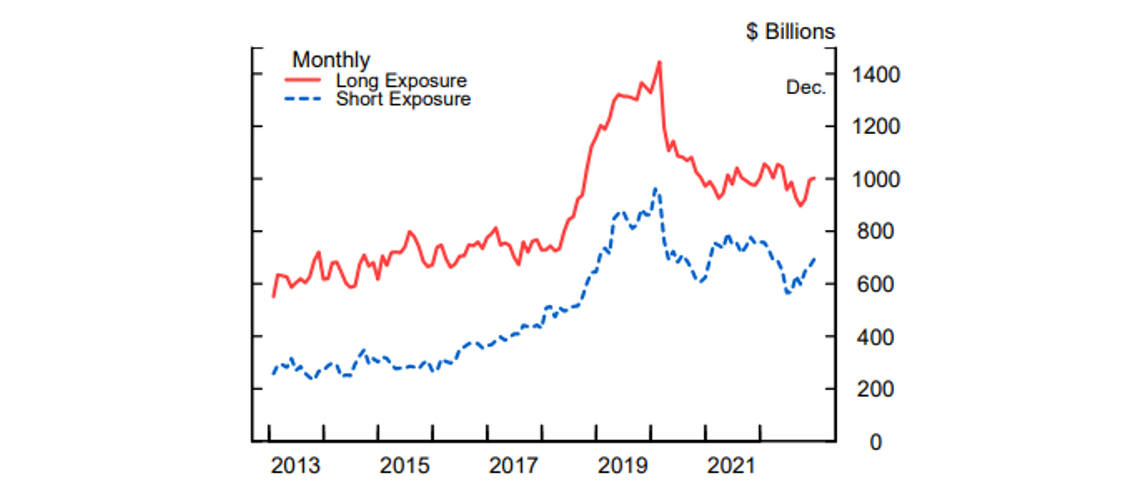

Prior to the pandemic, the sum of hedge funds' long and short UST exposures, including both UST securities holdings and derivatives, reached a peak level of $2.4 trillion, driven by a massive increase in Treasury cash-futures basis trading activity (Figure 1).3 In March 2020, as volatility in Treasury markets widened the cash-futures basis spread, funds that were engaged in this trade took significant losses. These losses caused some hedge funds to reach position volatility limits or stop-losses and liquidate their positions. In addition, margin requirements on Treasury futures increased to unprecedented levels, raising margin pressures on hedge funds' short futures positions. Hedge funds rapidly unwound their basis trades, amplifying the Treasury market disruptions at the time.4 Since then, hedge funds' UST exposures have remained elevated but notably below their pre-pandemic levels. According to the most recent Form PF data, long UST exposures of qualifying hedge funds (QHFs)– the largest hedge funds – were $1 trillion in December 2022, while their short UST exposures stood at $694 billion (Figure 1).

Source: SEC Form PF.

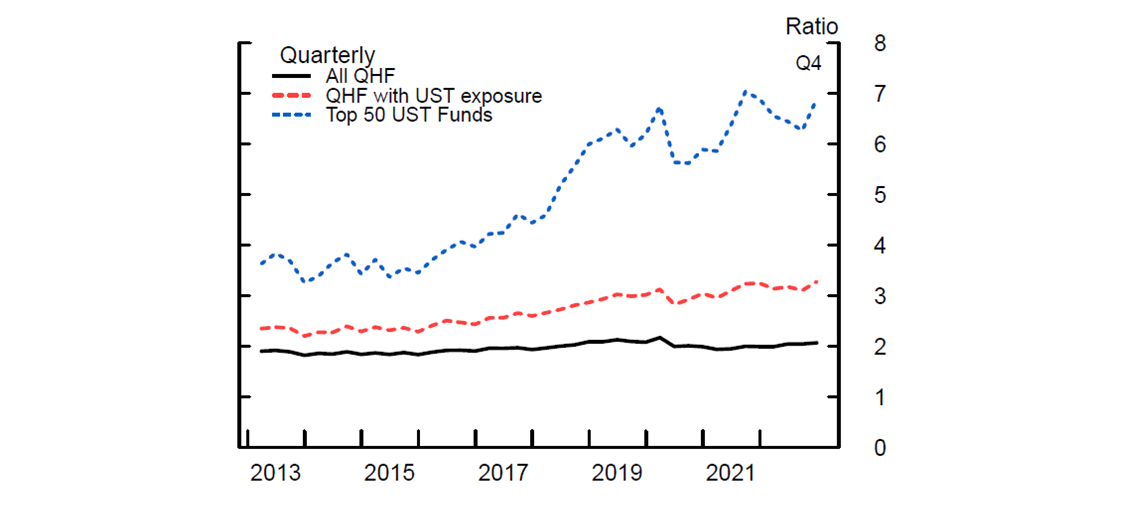

Hedge funds' UST exposures are concentrated in a small set of highly leveraged funds. The top 50 funds ranked by gross UST exposure – out of a universe of 2069 QHFs as of Q4 2022 – have consistently held about 80 percent of total QHFs' UST exposures since the inception of Form PF in 2012. Furthermore, leverage at these top UST-holding funds has been significantly higher than that of the average QHF. As depicted in Figure 2, while leverage has remained moderate at the sector level, leverage at the top 50 UST funds has increased markedly since 2018 and remained elevated in December 2022. These funds had average balance sheet leverage of 6.9-to-1 and gross notional leverage (not shown) of 33.4-to-1 at year end 2022, near their historical highs.5

Source: SEC Form PF.

Hedge funds are significant players in repo markets, where they transact with large dealers and face very low or zero haircuts

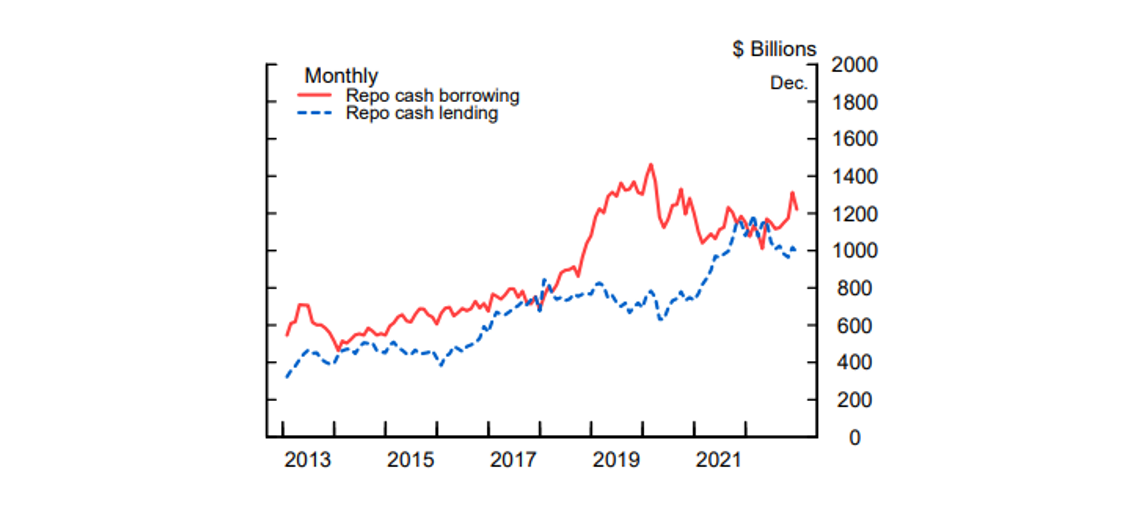

Hedge funds typically use repo transactions to finance long positions and source short positions in UST markets, non-U.S. sovereign bond markets, and other fixed income markets. Most of their repo market activities take place in the noncentrally cleared bilateral repo market, while a minority is in the centrally cleared repo market through FICC's sponsored repo program.

As shown in Figure 3, hedge funds' total repo borrowing roughly doubled over the two years preceding the pandemic, while their repo lending, which had been similar in magnitude, remained mostly flat. This was consistent with the increase in hedge funds' UST gross exposures due to the basis trade. Following the March 2020 market turmoil, hedge funds' repo borrowing has declined somewhat but overall remained elevated by historical standards. More recently, and consistent with the re-emergence of the Treasury cash-futures basis trade, repo borrowing trended up during the last months of 2022, standing at $1.2 trillion at the end of December.

Source: SEC Form PF.

Like UST gross exposures, repo borrowing is highly concentrated, with the top 50 UST funds accounting for 89 percent of total QHFs' repo borrowing (or $1.08 trillion) as of end of 2022. Furthermore, the elevated volumes of hedge fund repo borrowing have been largely driven by the activities of large relative value, macro, and multi-strategy funds; with about half of total hedge fund repo borrowing financed by U.S. financial institutions.6

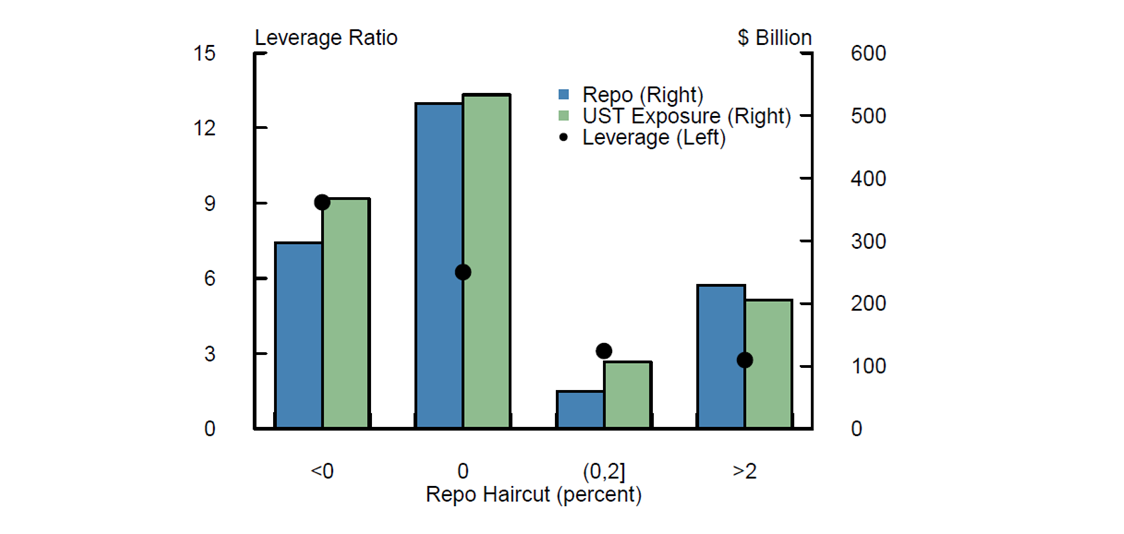

Form PF data shows that hedge funds have historically faced low haircuts on their repo financing transactions, consistent with their high levels of balance sheet leverage.7 As shown by the blue bars in Figure 4, 73.8 percent (or about $815 billion) of total repo borrowing volume by QHFs was transacted at zero or negative haircuts, meaning that the fund's borrowing was equal to or more than the value of the collateral. Furthermore, the dots in Figure 4 show that these zero or negative haircuts have typically been associated with elevated leverage, with average balance sheet leverage ratios of funds transacting at zero or negative haircuts significantly higher (6.2-to-1 and 9-to-1, respectively) than that of the average QHF (2.1-to-1) at year end 2022.

Note: Data are as of December 2022. Key identifies in order from left to right.

Source: SEC Form PF.

In line with our analysis of Form PF data, a recent OFR study based on a pilot collection of data on noncentrally cleared bilateral repo trades, shows that a large share of hedge funds' Treasury repo borrowing in this market is transacted at a zero haircut. Zero haircuts are in part driven by transactions settled on a net basis, whereby the hedge fund will engage in a repo and a reverse repo with the same counterparty, and the same end-date, usually short-term, but over different Treasury collateral.8 This nearly symmetric trade that allows hedge funds to temporarily exchange one Treasury against another can be particularly attractive for relative-value hedge funds betting that one Treasury will appreciate relative to another. Zero haircuts are also likely driven by cross-product margining (CPM). In this practice, the dealer estimates and collects margin for their risk exposure over all trades and exposures in the hedge fund's portfolio, rather than at the trade level, taking into account offsetting positions. Furthermore, this practice is highly dependent on the commercial relationship between the dealer and the hedge fund, and dealers might waive haircuts on the UST repo leg of a trade to clients with whom they have a CPM agreement. Yet, lack of data on netting and CPM limits our ability to assess how much these margining practices contribute to the low or zero repo haircuts hedge funds obtain on their repo borrowing. Finally, zero haircuts could also occur because dealers perceive the risks of lending collateralized by Treasury securities to be low and want to maintain profitable relationships with hedge fund clients.

Low or zero haircuts allow hedge funds to become more highly leveraged and to arbitrage very small price differentials, as in the case of Treasury cash-futures basis trades and other relative-value trades. However, these low or zero haircuts hedge funds obtain on their repo trades may exacerbate the effects of an episode of market stress, as a widening of arbitrage spreads, decreased availability of funding, or increased haircuts could trigger distressed unwinding of highly leveraged positions, potentially contributing to increased Treasury market volatility and amplifying dislocations in the Treasury, futures, and repo markets. In addition, while our analysis focuses on hedge fund leverage, low or zero haircuts may increase vulnerabilities associated with counterparty credit risk, as insufficient haircuts would leave counterparties without sufficient collateral to absorb losses in the event of default, potentially amplifying the initial shock from one market participant's default.

The impact of increased haircuts on hedge funds' Treasury repo

As of December 2022, we estimate that hedge funds had $553 billion in repo borrowing collateralized by Treasury securities.9 We use reported fund-level repo haircuts to estimate the collateralization of this Treasury repo, which must be supported by hedge fund capital. For example, if a hedge fund wants to purchase a Treasury security for $102 but can only borrow $100 by posting the Treasury security as collateral in a repo transaction, then it must provide for the remaining $2 out of its capital to make the purchase. As shown in Table 1, this capital amount was $9.88 billion as of December 2022, which implies that hedge funds in the aggregate were effectively leveraged 56-to-1 ($553 billion / $9.88 billion) on their Treasury repo trades, though individual funds facing zero haircuts did not require any capital to support their repo borrowing and were effectively infinitely leveraged on these trades. We next provide an approximate analysis on the quantitative effects of a hypothetical 200-basis point minimum haircut on hedge funds' repo borrowing collateralized by Treasury securities.10 The analysis is at the hedge fund level, focusing on the additional capital that hedge funds would need to support their existing repo borrowing levels. Note, however, that most funds already satisfy the collateral requirement and, in our analysis, do not need additional capital to support existing borrowing. Our analysis only affects funds with repo haircuts that are below 200 basis points. The results of our exercise are summarized in Table 1.

Table 1: The impact on hedge funds of a floor on Treasury repo haircuts

| As of December 2022 | 200 bps min. haircut, no change in borrowing | 200 bps min. haircut, no change in capital | |

|---|---|---|---|

| Treasury repo borrowing | $553 billion | $553 billion | $247 billion |

| Capital supporting Treasury repo | $9.88 billion | $22.29 billion | $9.88 billion |

| Leverage on Treasury repo | 56-to-1 | 25-to-1 | 25-to-1 |

Note: The first column reflects data and estimates as of December 2022. The second and third columns consider the effects of a hypothetical 200-basis point floor on Treasury repo haircuts faced by hedge funds. The second column assumes borrowing remains at Dec. 2022 levels, while the third column assumes borrowing levels adjust to post-requirement leverage levels.

If haircuts on repo collateralized by Treasury securities were subject to a minimum of 200 basis points, hedge funds in the aggregate would likely need to support their existing repo borrowing levels with more capital. To estimate the additional capital required, we subject each fund's estimated Treasury repo borrowing to a 200-basis point haircut and compare this to their estimated Treasury collateral posted, which is found by applying their reported fund-level haircut to their estimated Treasury repo borrowing. Aggregating across all funds as of December 2022, we find that funds would need $12.41 billion in additional capital to satisfy a 200-basis point minimum haircut on Treasury repo. Thus, hedge funds would require a total of $22.29 billion in capital to support their existing levels of $553 billion in Treasury repo borrowing under a minimum 200 basis point repo haircut requirement. Under the hypothetical haircut requirement, hedge funds' effective leverage ratio on Treasury repo decreases from 56-to-1 to about 25-to-1 ($553 billion / $22.29 billion). Our 25-to-1 leverage estimate is lower than the maximum leverage associated with a 200-basis point haircut requirement of about 50-to-1, because most hedge funds in our sample currently have repo haircuts more than 200 basis points and their leverage remains unchanged in our calculations.

We next consider whether hedge funds would be able to meet this hypothetical requirement for additional capital with their available unencumbered liquid resources. We use fund-level data on reported unencumbered cash and cash equivalents, which includes Treasury securities held outright or for liquidity purposes. We find that most funds have sufficient unencumbered cash to continue to support their Treasury repo borrowing. If we assume that the minority of funds without enough unencumbered cash to fund the increased haircut reduced their repo borrowing, then we estimate that the effect on overall Treasury repo borrowing levels would be minimal. Aside from liquid resources, which hedge funds might want to maintain for future liquidity needs, hedge funds could also unwind positions or sell securities already held in their portfolios.11 We use a fund's net asset value as a proxy for its ability to convert assets to acceptable collateral, and we find that all funds would theoretically have enough capital to continue supporting their Treasury repo borrowing.

Although our estimates suggest that hedge funds would generally be able to continue supporting their Treasury repo borrowing after the increase in haircuts, another important question is whether their trades would still be economically viable at the higher level of capital required. The requirement to post $12.41 billion in additional capital more than doubles the estimated amount that funds currently use of their own capital for these trades and reduces the effective leverage funds have in Treasury repo from 56x to 25x. This decrease in leverage reduces their return on equity on the relative value trades that they use repo to execute. Rather than maintaining these positions, funds might react by unwinding them because they have become insufficiently profitable. For example, if funds maintained their existing estimated levels of capital on Treasury repo at the post-mandate leverage ratio of 25-to-1, then this would imply that they could only support $247 billion in Treasury repo, implying a reduction of $306 billion in hedge funds' Treasury repo borrowing. If such a reduction in hedge funds' repo borrowing leads to a corresponding reduction in their Treasury holdings, then funds would have reduced their long Treasury exposures by about 30 percent (see Figure 1). These aggregates mask significant heterogeneity, as most funds are already in compliance with the hypothetical requirement and would be unaffected by it. However, a minority of funds that conduct most of the repo borrowing and are responsible for most of the Treasury positions currently face low or zero haircuts and would see their effective leverage ratios dramatically reduced.

A reduction in the amount of leverage available to hedge funds operating in Treasury markets can have positive or negative effects on Treasury market functioning. Higher haircuts on Treasury repo increase the amount of loss-absorbing capacity in leveraged Treasury positions, reducing the maximal leverage available on the position and the exposure at default of the counterparty. This can increase the resilience of the Treasury market to shocks in stress periods. On the other hand, to the extent that hedge funds influence relative pricing relationships as marginal investors in Treasury markets, a reduction in their effective leverage on relative value trades may make them less willing to act on small price discrepancies. This may affect the size and volatility of spreads among related instruments in Treasury cash and derivatives markets, as well as market liquidity conditions in those markets. For example, our finding that capital deployed to support trades financed with Treasury repo would have to about double implies that pricing spreads in hedge fund trades would also have to about double to remain at their current profitability levels.

Our quantitative analysis is subject to several assumptions, estimation methods, data limitations, and other caveats. We discuss three of these issues.12 Our exercise can be interpreted as examining the effects if no netting were allowed, as we have largely ignored the potential effects of netting or cross product margining due to data limitations.13 For example, because of payment and settlement netting features found in widely used repo master agreements, it is possible that a mandated floor on haircuts for repo borrowing collateralized by Treasury securities would still result in insignificant amounts of equity capital supporting transactions if a symmetric haircut is applied to reverse repo transactions and the transactions are netted. Another key assumption we make is that the reported fund-level repo haircuts apply to all a fund's repo regardless of collateral type. Because haircuts on Treasury repo are likely to be significantly lower than haircuts on other types of collateral such as MBS, this assumption may bias upward our estimates for capital allocated to support repo borrowing in funds that have low proportions of estimated Treasury repo. Finally, our quantitative analysis is static and does not consider how market participants may adapt to higher Treasury repo haircuts.

Our analysis is a first step towards estimating how a floor on repo haircuts might affect hedge funds' activities in Treasury markets. More comprehensive data on the hedge fund-counterparty relationship would help us better understand the exposures associated with Treasury secured financing transactions by enabling additional analysis that considers potential netting, cross product margining, and relationship effects.

1. We thank Benjamin Iorio for excellent research assistance. We also thank Danny Barth, Jay Kahn, Dan Li, Adam Minson, Lubomir Petrasek, and Sam Schulhofer-Wohl for helpful comments and suggestions. The views expressed are solely those of the authors and do not necessarily reflect the views of the Board of Governors of the Federal Reserve System. Return to text

2. On Form PF, QHFs are hedge funds with at least $500 million in net assets under management that are managed by advisers with at least $1.5 billion in regulatory assets under management invested in hedge funds. QHFs file Form PF on a quarterly basis, rather than annual, and are required to disclose more detailed information on their assets and liabilities than the smaller funds. QHFs account for about 85 percent of total gross hedge fund assets. Return to text

3. The (long) Treasury cash-futures basis trade consists of a short position in a Treasury futures contract and a long position in a Treasury security deliverable into the futures contract. These trades often involve significant financial leverage from financing the cash Treasury position in repo markets and embedded leverage through low margins on the Treasury futures contract. Return to text

4. Of note, dealers continued to finance hedge fund Treasury activities even as market volatility and repo rates spiked in March 2020, suggesting that the decline in hedge funds' Treasury holdings, in the aggregate, was likely not driven by their inability to finance these UST positions. See Banegas, Ayelen, Phillip J. Monin, and Lubomir Petrasek (2021). "Sizing hedge funds' Treasury market activities and holdings," FEDS Notes, https://doi.org/10.17016/2380-7172.2979, for a detailed discussion on hedge funds' UST market activities during the March 2020 turmoil. Return to text

5. Balance sheet leverage is defined as gross asset value divided by net asset value and measures leverage due to financial borrowings, including repo. Gross notional leverage attempts to additionally account for embedded leverage due to derivatives and is defined as gross notional exposure divided by net asset value. Return to text

6. Form PF defines U.S. financial institutions as any of the following: a financial institution chartered in the U.S.; (ii) a financial institution that is separately incorporated or otherwise organized in the U.S. but has a parent that is a financial institution chartered outside the U.S.; or (iii) a branch or agency that resides outside the U.S. but has a parent that is a financial institution chartered in the United States. Other types of creditors include non-U.S. financial institutions, and U.S. and non-U.S. creditors that are not financial institutions. Return to text

7. Reportedly, zero haircuts have been a long-standing practice in high quality G10 sovereign collateral. Return to text

8. See Hempel, Samuel, Jay Kahn, Robert Mann, and Mark Paddrik (2023) "Why Is So Much Repo Not Centrally Cleared?" OFR Brief Series, for a discussion on repo haircuts in the noncentrally cleared bilateral repo market. Return to text

9. Because the Form PF data do not contain hedge fund repo borrowing by collateral type, we develop methods to estimate a hedge fund's repo borrowing that is collateralized by Treasury securities. To estimate a fund's Treasury repo borrowing, we use the reported exposures of the fund to asset classes that are often used as collateral in bilateral repo and methods developed in Banegas, Petrasek, and Monin (2021) to estimate how much exposure is held physically versus through derivatives. SIFMA's US Repo Statistics and Hempel, Kahn, Mann, and Paddrik (2023) suggest that common collateral types in the non-centrally cleared bilateral repo market include Treasury securities, agency and GSE securities, private MBS/ABS, and corporate bonds. These data focus on U.S. repo markets, though hedge funds conduct repo borrowing with non-U.S. sovereign bonds (such as those in the eurozone and in Japan) used as collateral, as suggested by survey data on repo haircuts faced by the buy side from FRBNY. To estimate fund-level repo borrowing collateralized by Treasury securities, we allocate reported repo collateral across several asset classes, including U.S. Treasuries, G10 sovereigns (ex-U.S.), agency securities, GSE bonds, and MBS, proportionally based on the fund's reported long exposures to these asset classes (using estimates for exposure held physically where available). Unallocated amounts are placed into an "Other" collateral class (which could include corporate bonds, equities, ABS, CLOs, and cash and cash equivalents). To estimate the amount of borrowing associated with these collateral types, we use the funds' reported overcollateralization rate and average haircuts from the FRBNY repo buyside survey. Return to text

10. A 200-basis point haircut is reportedly the standard for Treasury repo in triparty markets. We use this level as a benchmark to focus our discussion, not to imply that this is the appropriate level for a minimum mandate. Return to text

11. Hedge funds could also raise new investments or potentially post other fully paid securities such as corporate bonds as collateral, though repo agreements may define acceptable marginable securities more narrowly. Return to text

12. There are other salient assumptions and caveats. Our exercise contemplates a shock in which haircuts on Treasury repo are suddenly subject to a floor; in reality, funds and their counterparties would have more lead time to adjust. Moreover, the requirement we consider applies at the transaction level and only to Treasury repo in which the hedge fund is the cash borrower ("Repo Seller"), and not to reverse repo transactions or at the portfolio level. In addition, due to the availability of data on repo borrowing and Treasury exposures, our analysis considers only large hedge funds filing Form PF (i.e., QHFs). Moreover, we are unable to analyze hedge funds' secured financing transactions that are not conducted under a repo agreement, such as those that are instead governed by securities lending agreement, due to data limitations. Finally, we note that anecdotal and survey evidence suggest that hedge funds also obtain low or zero haircuts on their repo borrowing with some types of non-U.S. sovereign bond collateral. Return to text

13. Hempel, Kahn, Mann and Paddrik (2023) offer an example calculation of how an increase in haircuts on netted packages may enlarge the potential range for the difference in yields between the two Treasury securities used as collateral. Return to text

Banegas, Ayelen, and Phillip Monin (2023). "Hedge Fund Treasury Exposures, Repo, and Margining," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, September, 08, 2023, https://doi.org/10.17016/2380-7172.3377.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.