FEDS Notes

March 01, 2018

Interest on Reserves and Arbitrage in Post-Crisis Money Markets

Thomas Keating and Marco Macchiavelli

The Federal Reserve (Fed) sets the rate paid on interest on reserves (IOR) as a primary tool for implementing monetary policy. By adjusting the rate paid on IOR, the Fed can raise or lower the value of reserves held by banks on deposit at the Fed. Although there are many types of money market participants, not all are eligible to receive IOR. Because of this limitation, some lenders are willing to lend overnight wholesale funds at rates below the IOR rate. This market segmentation creates an opportunity for IOR eligible banks to earn the positive spread between the IOR rate and the overnight funding rate by borrowing in overnight wholesale funding markets and holding the funds as reserve balances. As these trades do not involve credit or interest rate risk, we refer to these trades as "IOR arbitrage trades".

In this note, we use confidential, daily data on wholesale unsecured borrowing and reserve balances to empirically document several salient features of IOR arbitrage trades.1 We show that foreign banks, which make up most of the trading volumes in these markets, keep around 99% of each Eurodollar and 80% of each fed fund borrowed as reserve balances. Larger domestic banks borrow less often and in smaller amounts, but when they borrow they keep 100% of each Eurodollar and fed fund borrowed as reserves. Finally, small domestic banks seem not to borrow for arbitrage purposes. Overall, the volume of IOR arbitrage trades is concentrated at U.S. branches and agencies of foreign banks, which are subject to lower regulatory costs relative to domestic banks because they are exempt from the premiums the Federal Deposit Insurance Corporation (FDIC) charges to insure deposits and face less stringent implementations of Basel III leverage ratios. We also find that many institutions borrow in both the fed funds and Eurodollar markets on the same day, which provides evidence that the tight correlation between the fed funds and Eurodollar rates is, in part, due to these cross-market linkages.

Reserves, Monetary Policy Implementation, and Money Market Arbitrage

In response to the financial crisis beginning in the summer of 2007, the Federal Reserve used a variety of tools to support the liquidity of financial institutions and put downward pressure on longer-term interest rates.2 A byproduct of these measures to support the economy was a large increase in the aggregate amount of reserve balances in the banking system, which put downward pressure on the effective federal funds rate.3 In order to provide a floor for the federal funds rate in an environment of abundant excess reserves, the effective date of the authority to pay interest on reserves was accelerated from October 2011 to October 2008 allowing the Fed to use IOR as a monetary policy tool to keep the federal funds rate close to the target rate.4

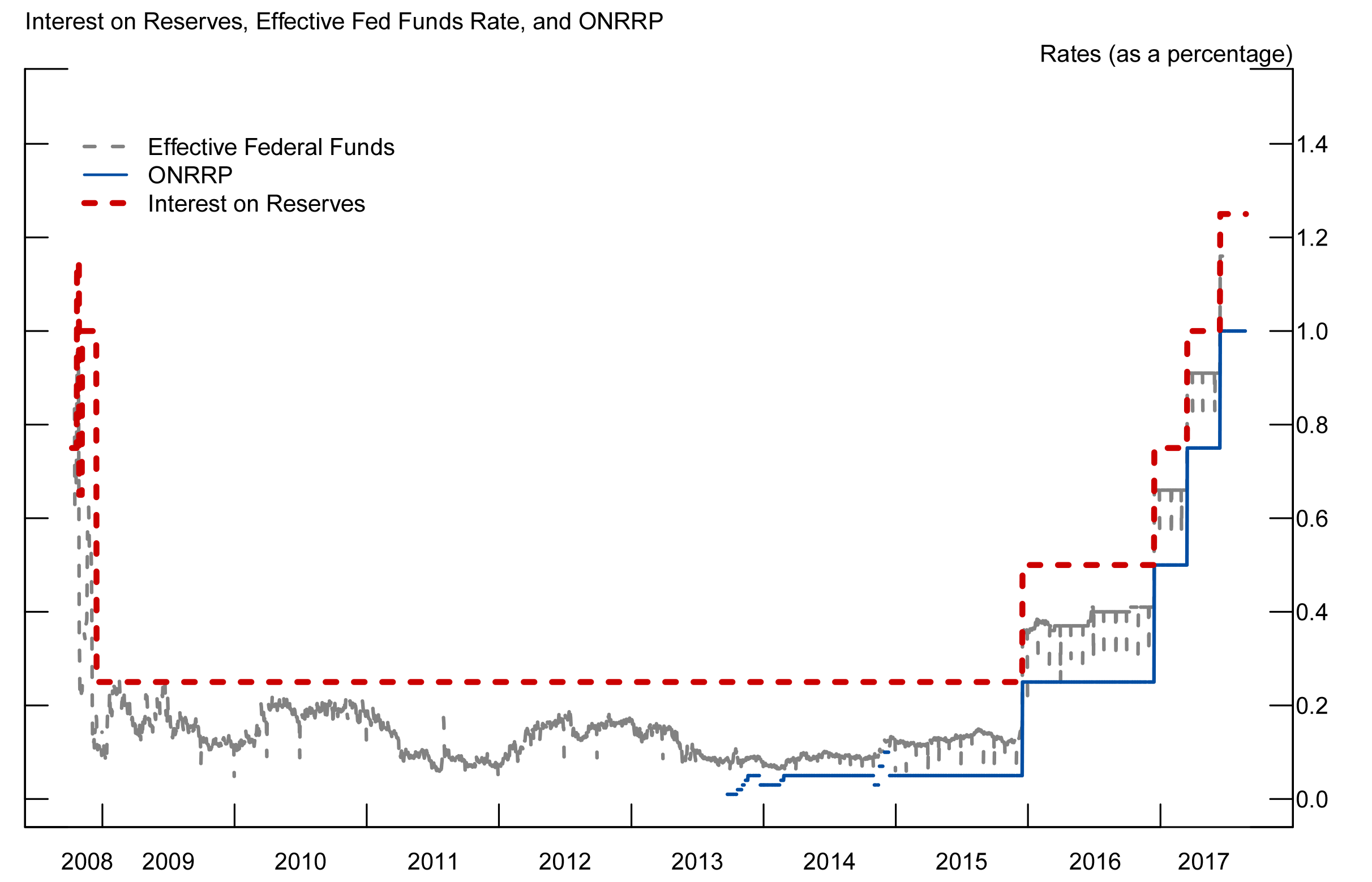

If banks eligible to receive IOR were the only participants in money markets, it is likely that IOR would have proved sufficient to establish a floor under money market rates as no bank would have been willing to make an overnight unsecured loan below the IOR rate. However, some money market participants are ineligible to receive IOR, such as money market funds (MMFs) and government-sponsored enterprises (GSEs). Thus, these investors are willing to make loans below the IOR rate, eroding the lower bound on money market rates that interest on reserves was expected to create. This can be seen in figure 1, which displays the evolution of the effective federal funds rate, the IOR rate, and the overnight reverse repurchase (ON RRP) facility offering rate.5

Source: FRBNY.

Nonetheless, absent other funding costs, competition among banks borrowing to fund IOR arbitrage should bid up money market rates very close to the IOR rate. However, the existence of balance sheet costs, such as the leverage ratio and FDIC premiums, increase the marginal cost of borrowing reserves, creating a wedge between the effective federal funds rate and the IOR rate.6

As these regulatory costs differ across jurisdictions, not all banks make the same profit when conducting IOR arbitrage trades. Specifically, foreign banking organizations (FBOs) are exempt from the FDIC insurance premiums domestic banks face to insure deposits.7 A further relevant regulatory differentiation is the implementation of leverage ratio calculations. Most foreign jurisdictions calculate leverage ratios using either month-end or quarter-end snapshots of banks' balance sheets, in contrast to the U.S. implementation which relies on daily averages. As a result of those calculation methods, most FBOs are constrained by their leverage ratio only at month-ends, meaning that they can ignore the leverage ratio implications of borrowing wholesale funds during the month by deleveraging at month-ends.8

Reserve Balances and Unsecured Borrowing Data

Our analysis examines confidential Federal Reserve daily data on individual bank reserve balance holdings and transaction-level wholesale borrowing activity.9 The daily dataset runs from November 2015 to March 2017 and consists of amount, rate, maturity, and type of overnight unsecured borrowing (CDs, Eurodollars and fed funds) by individual banks, along with each banks' daily reserve position at the Fed. In the final dataset there are 81 FDIC-exempt banks and 105 FDIC-insured banks. All the FDIC-exempt banks are U.S. subsidiaries of foreign banks, while the vast majority of the FDIC-insured banks are domestic.10

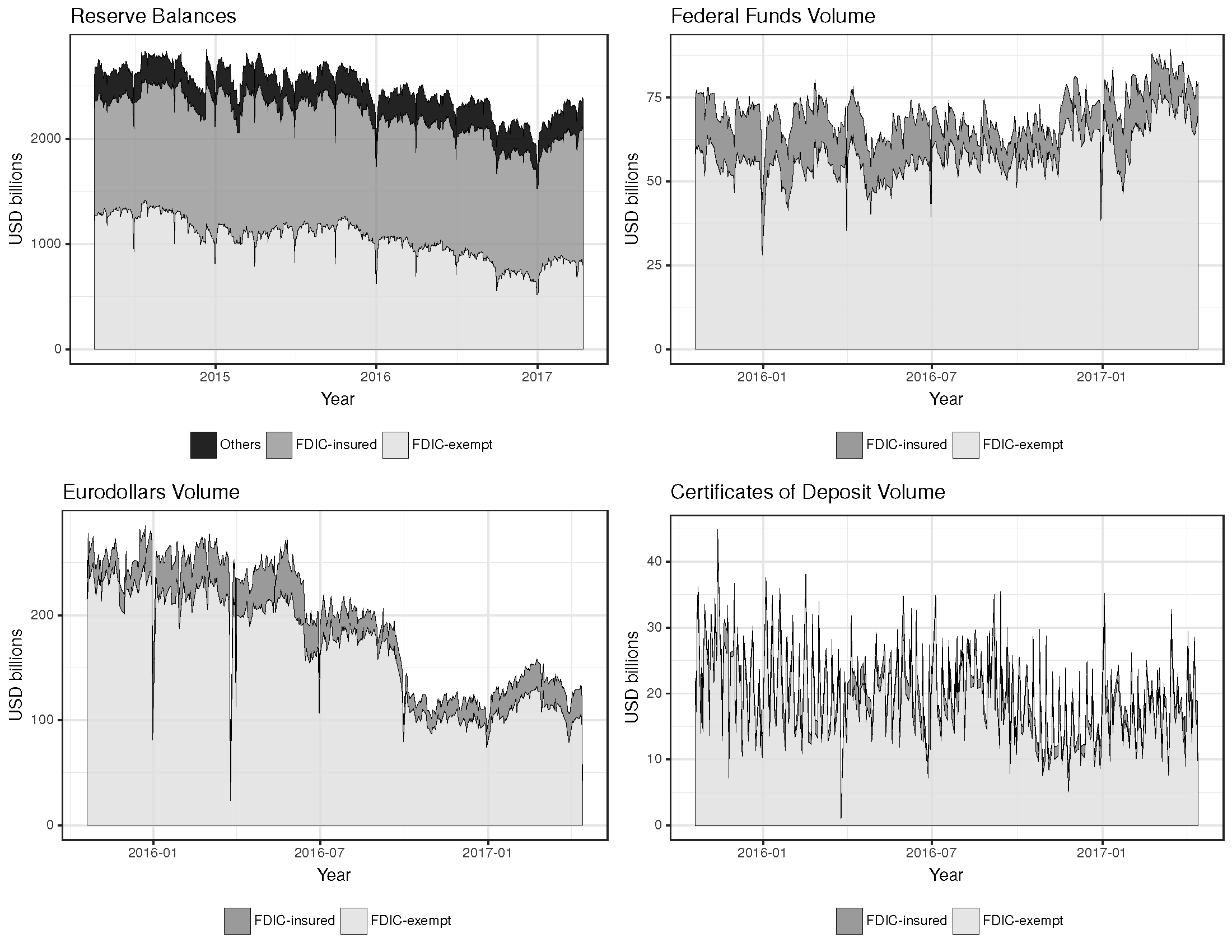

Although the distribution of reserves in our sample is about evenly split between FDIC-insured (domestic) and FDIC-exempt (foreign) banks, foreign banks account for almost all of the unsecured borrowing volume in the federal funds, Eurodollar, and CD markets, as seen in figure 2.11 This suggests that a non-negligible portion of foreign banks' reserves are financed by unsecured overnight borrowing, while domestic banks mostly finance reserves with other liabilities, such as deposits.

Note: Chart key identifies regions in order from top to bottom.

Sources: Federal Reserve accounting system for reserve balances, FR2420 for borrowing volumes.

IOR Arbitrage

Using this dataset, we are able to investigate IOR arbitrage trades across money market instruments and groups of banks (FDIC-exempt vs FDIC-insured, small vs large), as well as analyze trading linkages and pricing patterns across the federal funds and Eurodollar markets.

IOR Arbitrage Trades

To estimate the proportion of daily unsecured borrowing used to fund a reserve position as part of an IOR arbitrage trade, we estimate the following panel regression:

$$$$ \Delta . {Reserves }_{it} = \beta_1 Net{CD}_{it} + \beta_2 Net{ED}_{it} + \beta_3 Net{FF}_{it} + \gamma_t+ \epsilon_{it} $$$$

$$\Delta . {Reserves}$$ is the daily change in reserve balances (in $ billion), Net CD is the daily net issuance of certificates of deposits, Net ED is the daily net issuance of Eurodollar, and Net FF is the daily net issuance of fed funds. Net issuance (in $ billion) of these instruments is the difference between the amount issued and the amount maturing each day, thus measuring any increase or decrease in outstanding funding each day. As a result, the $$(\beta_1,\beta_2,\beta_3)$$ coefficients capture how much of the additional amount raised is on average held in reserves to earn IOR. Finally, $$\gamma_t$$ is a set of daily fixed effects.

If all funds borrowed in unsecured markets were held as reserve balances, each additional dollar of borrowing by a bank would result in a one dollar increase in its reserve position. $$\beta_m$$, where m indexes a specific funding market (ED, FF or CD), thus represents the percentage of each dollar of borrowing that is held as reserves at the Fed. When $$\beta_m$$=1, which we call "complete pass-through," 100 percent of each additional dollar of borrowing is held in a bank's reserve account.

Table 1 displays the main regression results. As excess reserves are such a large fraction of total reserves for the vast majority of banks in the sample, the results are virtually identical for total and excess reserves.

Table 1. Estimated IOR Arbitrage Pass-through Across Markets

| Table 1. Estimated IOR Arbitrage Pass-through Across Markets | (1) Δ Total Reserves | (2) Δ Excess Reserves |

|---|---|---|

| Net Eurodollars | 0.99*** | 0.99*** |

| Net Federal Funds | 0.74*** | 0.74*** |

| Net Certificate of Deposits | 0.72*** | 0.72*** |

Note: *** indicates significance at 1 percent level based on clustered standard errors.

The results demonstrate that, on average, 99 cents of each dollar borrowed in the Eurodollar market is held as reserves overnight, earning IOR. This near complete pass-through of Eurodollar funding to overnight reserve holdings suggests that banks use Eurodollar borrowing to fund IOR arbitrage. Net borrowing in fed funds and CDs are also strongly associated with increases in reserve balances, but with lower pass-through rates.12

IOR Arbitrage and FDIC Insurance Status

Table 2 extends the above regression to differentiate between FDIC-exempt and FDIC-insured banks, which largely represents the distinction between FBOs (FDIC-exempt) and domestic (FDIC-insured) banks. FDIC-exempt banks display the largest pass-throughs from net borrowing into reserve balances across the different funding markets, which is to be expected given the lower cost to these institutions of funding higher reserve balances.

Table 2. Estimated IOR Arbitrage Pass-through Across Markets by FDIC Status

| Table 2. Estimated IOR Arbitrage Pass-through Across Markets by FDIC Status | (1) Δ Total Reserves | (2) Δ Excess Reserves | |

|---|---|---|---|

| Net Federal Funds | FDIC-insured | 0.60*** | 0.60*** |

| FDIC-exempt | 0.78*** | 0.78*** | |

| Net Eurodollars | FDIC-insured | 0.93*** | 0.93*** |

| FDIC-exempt | 1.00*** | 1.00*** | |

| Net Certificate of Deposits | FDIC-insured | 0.42 | 0.39 |

| FDIC-exempt | 0.74*** | 0.74*** | |

Note: *** indicates significance at 1 percent level based on clustered standard errors.

IOR Arbitrage, FDIC Insurance Status, and Bank Size

Table 3 further differentiates pass-through rates by including bank size along with money market and FDIC status in the regression. Within each FDIC status, the top 15 banks by reserve balances each day are classified as "larger," while the remainder are referred to as "smaller." Both smaller and larger FDIC-exempt banks, which are the FBOs in our panel, exhibit very similar pass-through for borrowings in each market. In contrast, the pass-through rates differ substantially between smaller and larger FDIC-insured banks, which are overwhelmingly domestic institutions. Larger FDIC-insured banks displayed complete pass-through of overnight borrowing in the fed funds and Eurodollar market. Whereas the pass-through of Eurodollar and fed funds borrowing by smaller FDIC-insured banks was not statistically different from zero. Which implies that those banks likely borrow to settle obligations to other institutions rather than to fund IOR arbitrage.

Table 3. Estimated IOR Arbitrage Pass-through Across Markets by FDIC Status and Bank Size

| Table 3. Estimated IOR Arbitrage Pass-through Across Markets by FDIC Status and Bank Size | (1) Δ Excess Reserves for smaller banks | (2) Δ Excess Reserves for larger banks | |

|---|---|---|---|

| Net Federal Funds | FDIC-insured | 0.10 | 1.00*** |

| FDIC-exempt | 0.79*** | 0.80*** | |

| Net Eurodollars | FDIC-insured | 0.02 | 1.00*** |

| FDIC-exempt | 0.96*** | 1.02*** | |

| Net Certificate of Deposits | FDIC-insured | 0.54*** | 0.34 |

| FDIC-exempt | 0.73*** | 0.77*** | |

Note: *** indicates significance at 1 percent level based on clustered standard errors.

IOR Arbitrage, Money Market Pricing, and Cross-Market Linkages

As seen in figure 2 and discussed above, FDIC-exempt foreign banks account for almost all of the unsecured borrowing volume in the federal funds and Eurodollar markets. Unsurprisingly then, when we estimated the borrowing costs of the bank categories we investigated, we found that FDIC-exempt foreign banks borrowed, on average, at the effective rates in these markets, the same rates paid by smaller, FDIC-insured domestic banks.13 Interestingly though, our findings indicate that when larger FDIC-insured domestic banks borrow in these markets they pay rates 13 to 17 basis points lower than smaller domestic banks and foreign banks. This finding is possibly driven by higher regulatory costs of such borrowing for larger domestic banks, likely including FDIC insurance premiums and leverage constraints. Specifically, it is possible that larger domestic banks only borrow in these money markets to fund IOR arbitrage when they have sufficient balance sheet space and can borrow at rates low enough to make the trade profitable.

We also observe that all but the smaller domestic banks that borrow in the fed funds market on a certain day are also likely to borrow in the Eurodollar market that same day, providing supporting evidence that the presence of a considerable set of banks active in both markets each day contributes to the tight interest rate connection observed between fed funds and Eurodollar markets. In contrast, there is little cross-market linkage on the lending side as most lenders in the fed funds market are Federal Home Loan Banks, while most lenders in the Eurodollar market are MMFs and non-financial corporations.

Concluding Remarks

In the post-crisis reserve-abundant world, most cash lenders in money markets are not eligible to earn interest on reserves and are therefore willing to lend money at rates below the IOR rate. This creates an arbitrage opportunity for banks that are able to earn interest on their reserve balances. Using confidential daily data we find that foreign banks, which make up most of the trading volumes in these markets, engage in IOR arbitrage trades and invest around 99% of each Eurodollar and 80% of each fed fund borrowed as reserve balances. We further find that FDIC-exempt banks and banks in jurisdictions that calculate the leverage ratio at month- or quarter-end engage in the vast majority of IOR arbitrage trades, both in terms of volume and number of transactions. We also find that among FDIC-insured banks, which are almost exclusively domestic banks, the largest banks sometimes engage in IOR arbitrage, while smaller banks generally do not borrow unsecured funds for IOR arbitrage purposes. Finally, the degree of cross-market participation by bank borrowers seems to support the almost-perfect correlation between the effective interest rates in both the fed funds and Eurodollars markets.

1. This note summarizes the key findings of an earlier FEDS Working Paper by the same authors. Please see Keating and Macchiavelli (2017) for more detail. Return to text

2. These tools included the provision of liquidity through the Discount Window and credit programs such as the Term Auction Facility (TAF), Primary Dealer Credit Facility (PDCF), Term Securities Lending Facility (TSLF), and the Term Asset-Backed Securities Loan Facility (TALF), among others. In addition to these steps, the Federal Reserve engaged in a series of large-scale asset purchases (LSAPs) by purchasing longer-term Treasury securities and agency mortgage-backed securities (MBS). Return to text

3. See Keister and McAndrews (2009). Return to text

4. The Financial Services Regulatory Relief Act of 2006 authorized the Federal Reserve Banks to pay interest on reserve held by or on behalf of depository institutions at Reserve Banks, subject to regulations of the Board of Governors, effective October 1, 2011. The effective date of this authority was advanced to October 1, 2008, by the Emergency Economic Stabilization Act of 2008. Return to text

5. In an effort to create a firmer floor on money market rates, in September 2013 the Federal Reserve began testing the Overnight Reverse Repurchase (ON RRP) facility, an OMO which provides overnight reverse repos to an expanded range of eligible counterparties relative to IOR. These counterparties can invest cash overnight at the Federal Reserve, and receive OMO-eligible assets as collateral. By providing access to MMFs and GSEs, the ON RRP facility has been largely successful in establishing a floor for overnight tri-party repo rates. Return to text

6. See Frost et al. (2015). Return to text

7. The Dodd-Frank Act of 2010 widened the FDIC assessment base from total domestic deposits to total assets less tangible equity, thereby shifting reserves into the assessment base. Following implementation in April 2011, this change increased the marginal cost to domestic banks of holding reserves relative to FBOs, creating an asymmetry in the cost of funding reserves. Return to text

8. This "window dressing" dynamic is also present in the repo market, see Anbil and Senyuz (2017). Return to text

9. Individual bank reserve balance holdings are from the Federal Reserve's Reserves Central – Reserve Account Administration application, which contains daily data on reserve balance holdings by institution; daily transaction-level wholesale borrowing in fed funds, Eurodollars, and certificates of deposits (CDs) by domestically chartered commercial banks, and U.S. branches and agencies of foreign banks are from the FR 2420 report. Return to text

10. In our sample there are seven foreign banks with grandfathered FDIC insurance and who pay FDIC insurance premiums. Return to text

11. Fed funds and Eurodollars volumes in Figure 2 include both overnight and term loans, while the publicly available FR 2420 data published by FRBNY include only overnight fed funds and Eurodollars. Return to text

12. The incomplete pass-through in fed funds is mainly attributable to smaller domestic banks, which may borrow in the overnight market because they find themselves short of reserves for operational purposes. Return to text

13. Since many banks on any given day borrow from multiple lenders in each market, for each bank we calculate a daily volume-weighted overnight rate. In the panel, about 98% of both fed funds and Eurodollar borrowing volumes are overnight. Return to text

Keating, Thomas, and Marco Macchiavelli (2018). "Interest on Reserves and Arbitrage in Post-Crisis Money Markets," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, March 1, 2018, https://doi.org/10.17016/2380-7172.2136.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.