FEDS Notes

December 22, 2022

International Spillovers of Tighter Monetary Policy1

Dario Caldara, Francesco Ferrante, and Albert Queralto

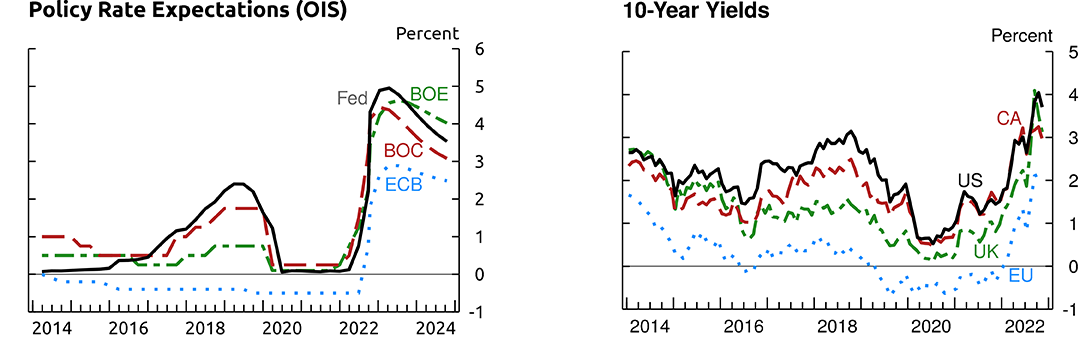

Central banks around the world are tightening monetary policy in response to a global surge in inflation not seen since the 1970s. This synchronization of global interest rate hikes and further increases expected by markets, illustrated in figure 1, have raised concerns about adverse international spillovers of tighter monetary policy. Some commentators have called on central banks to coordinate in their fight to tame inflation, arguing that a failure to account for spillovers could result in an unintendedly deep contraction in global economic activity.2 This note builds on a large body of academic and central bank research to review the key channels through which spillovers may materialize, with a focus on the special role of the dollar in international trade and finance.

Note: Policy rate expectations are calculated using OIS forecasts from November 15, 2022. Data for policy rate expectations are quarterly and end-of-period. Data for 10-year yields are monthly and end-of-period. Projections begin 2022:Q4. Solid black line, current. Dotted line, February.

Source: Bloomberg.

We show that central bank actions can produce spillovers to foreign economies and create tradeoffs for foreign policymakers. While central banks do take into account cross-border spillovers of their policies, in a world of unusually high uncertainty, there is a risk of underestimating these spillovers, which can lead to overtightening. Central banks are cognizant of this risk and need to manage it against the risk of undertightening that could deanchor long-term inflation expectations.

Channels of Monetary Policy Spillovers

Benchmark open-economy models assume that monetary policy in the home country—in this case, assumed to be the United States—affects economies abroad through three channels.3 The first channel is the exchange rate channel. A surprise rise in the U.S. interest rate relative to foreign rates usually leads to dollar appreciation. This currency movement lowers the prices of foreign goods and services relative to those of the United States, thereby restraining U.S. GDP and strengthening foreign GDP. The weaker currency and the resulting higher activity abroad push up foreign inflation. The second channel works through domestic demand. When U.S. policy tightens, U.S. aggregate demand slows, lowering U.S. imports of foreign products and damping foreign GDP and foreign inflation. The third channel, the financial channel, captures the effects of the rise in U.S. longer-term yields that typically accompanies a tightening of U.S. monetary policy. Higher U.S. longer-term yields lead international investors to rebalance their portfolios from foreign to U.S. assets, tightening foreign financial conditions and reducing GDP and inflation in the foreign country.4 The fact that the bulk of international transactions are denominated in dollars gives U.S. monetary policy a particularly salient role through the financial channel. A prominent way to measure the financial channel is by gauging how changes in U.S. term premiums prompted by a U.S. monetary policy action spill over to term premiums in foreign economies.5

The relative strength of the three channels determines the overall sign and size of the foreign effects of a tightening in domestic monetary policy. As summarized in Table 1, the appreciation of the dollar following an increase in domestic interest rates would tend, all else being equal, to increase foreign GDP and inflation, while the domestic demand and financial channels would depress them both. Quantifying spillovers through each channel is challenging, however. The magnitude of each effect depends on a multitude of structural features of the global economy, such as the degree of trade openness, financial vulnerabilities to currency depreciation against the dollar, and the use of the dollar as currency of invoicing in international trade. In addition, spillover effects depend on the monetary policy response of foreign central banks, a critical consideration in the current environment of synchronous global tightening. For example, the surprise relative change in interest rates, and thus the size of the effects on the dollar, depends on the change in monetary policy abroad as well. In light of these challenges, models calibrated to capture the most relevant structural features are useful tools in estimating the likely magnitudes of spillovers and their net effects.

Table 1: Channels of Monetary Policy Spillovers Abroad

| Transmission Channels | Effect on Foreign Output | Effect on Foreign Inflation |

|---|---|---|

| Exchange Rate (dollar appreciation) | + | + |

| Domestic Demand | - | - |

| Financial | - | - |

Accordingly, in what follows we illustrate and discuss spillovers using two variants of an open-economy model, similar to the SIGMA model used by Federal Reserve Board staff for policy simulations.6 The model includes a U.S. bloc and a "rest of the world" bloc and is calibrated to capture many of the structural features that are important to estimating the effect of synchronous monetary policy tightening. The first variant is our "benchmark" model, which incorporates the exchange rate, demand, and financial channels. This model assumes that neither bloc nor currency has a dominant role in the international financial system. The second variant is our "dollar dominance" model, which assumes that foreign exporters use the dollar as currency of invoicing rather than their own country's currency and also features a material role for dollar-denominated borrowing.7 Dollar invoicing means that when the dollar appreciates foreign goods do not become cheaper for U.S. consumers, thus limiting the competitiveness gains to foreign exporters through the exchange rate channel.8 The second feature of the dollar-dominance model, dollar-denominated borrowing abroad, leads currency depreciation to tighten foreign financial conditions through exacerbating currency mismatches on foreign balance sheets. These features alter the relative strength of the three channels and a comparison using the second model versus the first can tell us how the magnitudes are affected by the assumptions embedded in the dollar dominance model.9

Model Results

We begin our analysis by discussing the spillover effects of an unanticipated U.S. monetary tightening on the rest of the world. We then discuss the spillovers of foreign monetary tightening on the United States. Our goal is to illustrate the effects and the magnitudes of monetary policy actions themselves on domestic and foreign economies in isolation from other unexpected developments. Our third experiment considers a scenario where tightening happens synchronously in the two blocs in response to a surge in global inflation, in line with current developments, and we discuss the implications both when central banks recognize the spillovers from synchronous tightening (the more realistic case) and when they might ignore them.

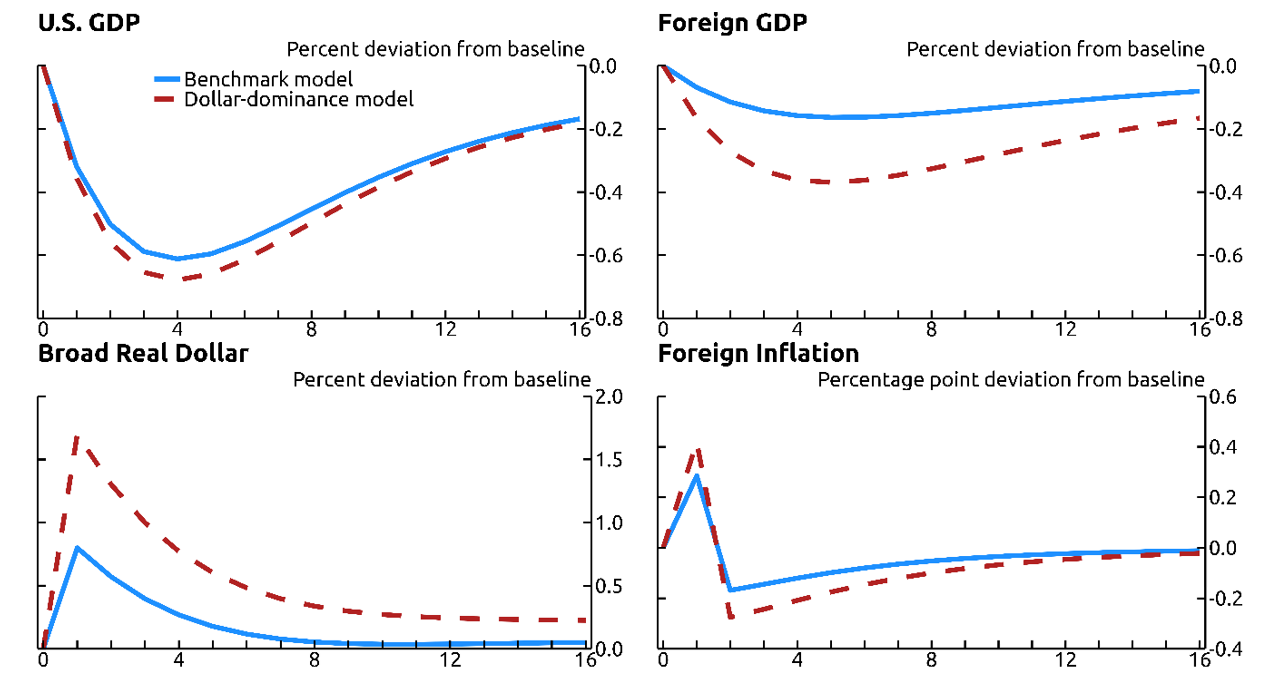

A U.S. monetary tightening generates a tradeoff for foreign central banks, with the net effect from the three channels in our model reducing foreign GDP and producing a short-lived rise in foreign inflation. These spillovers are considerably larger in the dollar-dominance model than in the benchmark model. As shown in figure 2, we consider the effects of a 100 basis point rise in the federal funds rate in the benchmark model and in the dollar-dominance model.10 In both models, the U.S. tightening lowers U.S. GDP by about 0.6 percent. By lowering U.S. demand for foreign products, it also weakens foreign activity. The two models differ in how the appreciation of the broad real dollar transmits to the foreign economy, however. In the benchmark model, the depreciation of foreign currencies makes foreign products more attractive, pushing foreign activity up. In the dollar-dominance model, foreign countries' net exports do not benefit as much from their cheaper currencies, as foreign exporters set prices in dollars. In addition, in the dollar-dominance model, the stronger dollar tightens financial constraints abroad by increasing the debt-servicing burden of dollar-denominated debt. Accordingly, the financial channel strengthens, slowing investment spending abroad, and sharp capital outflows from the foreign economies result in larger depreciation of their currencies. All told, foreign GDP falls by a relatively modest 0.15 percent in the benchmark model but by twice as much in the dollar-dominance model. The stronger dollar makes foreign imports of U.S. products more expensive, leading inflation abroad to increase in the near term. Inflation declines thereafter as the dollar depreciates and weaker U.S. demand exerts increasing downward pressure on foreign activity. U.S. GDP also declines somewhat more in the dollar-dominance model than in the benchmark model, reflecting "spillbacks" from the greater contraction in foreign activity.

Note: Horizontal axis shows quarters since the shock.

Source: Board staff calculations based on the benchmark model and the dollar-dominance model.

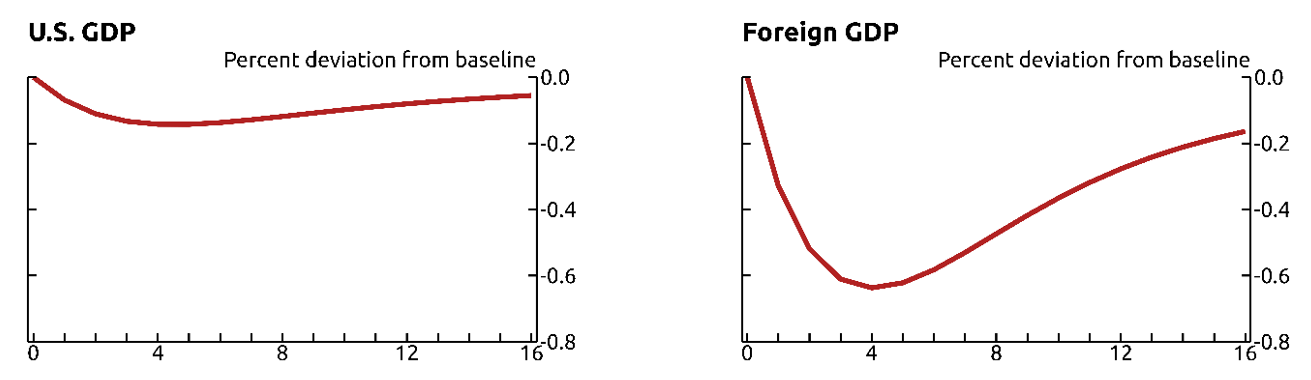

Our dollar-dominance model also suggests that, because of the special role of the dollar, spillovers of foreign tightenings on the United States are not as large as the reverse. To illustrate this point, our next experiment, shown in figure 3, considers spillovers to the United States of a 100 basis point monetary tightening in the foreign economies in the dollar-dominance model. The results in the benchmark model are very similar since dollar dominance does not influence much how foreign economies affect the U.S. economy. U.S. GDP falls 0.15 percent at the trough, about half of the decline in foreign GDP due to a tightening in the United States of the same size shown in figure 2.

Note: Horizontal axis shows quarters since the shock.

Source: Board staff calculations based on the dollar-dominance model.

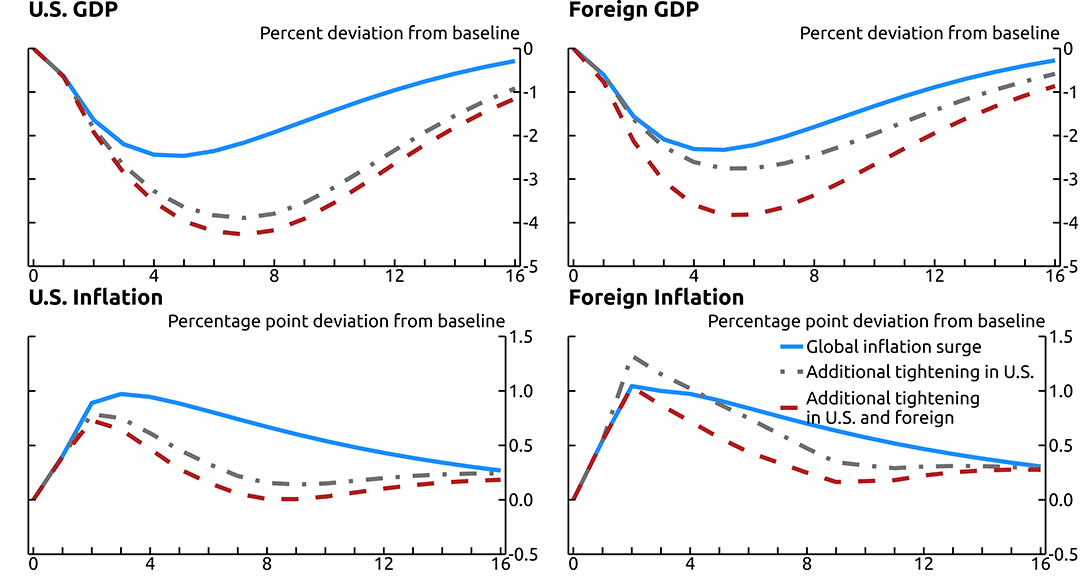

While central banks strive to take into account the full implications of cross-border spillovers of synchronous monetary tightening, in a world of high uncertainty, they may underestimate these effects. To illustrate this point, our final experiment, depicted in figure 4, considers a hypothetical scenario in which in response to a rise in global inflationary pressures, central banks do not take into account how their domestic policies might influence foreign policies. In this experiment, we use the dollar-dominance model to simulate the effects of a surge in global inflation driven by adverse supply shocks, shown by the blue lines. We then consider a scenario in which U.S. monetary policy responds more aggressively to higher inflation but assumes that the foreign central bank will continue following its original policy rule. In this scenario—shown by the gray lines—more-aggressive U.S. monetary policy leads to lower foreign GDP and higher foreign inflation in the short run. In the final scenario, shown by the red lines, contrary to U.S. monetary policymakers' expectation, foreign monetary policy, in fact, responds aggressively enough to fully offset the near-term increase in inflation induced by the more-aggressive U.S. policy response—perhaps due to concerns about de-anchoring of inflation expectations or to uncertainty surrounding the persistence of the additional inflation surge. As a result, foreign GDP declines substantially more than in the baseline scenario, lowering inflation in the medium term. The more-aggressive foreign tightening then spills back to the United States, leading to lower GDP and inflation paths relative to what U.S. monetary policy intended to accomplish with its more-aggressive stance. To reproduce the intended path of U.S. and foreign variables, monetary policies in each jurisdiction would need to be less tight than in the case where the synchronous nature of the tightening is not taken into account.

Note: Horizontal axis shows quarters since the shock.

Source: Board staff calculations based on the "dollar dominance" model.

Conclusions

Summing up, U.S. monetary policy actions, in our models, can produce spillovers abroad and create tradeoffs for foreign economies, especially in an environment where the dollar has a dominant role in international trade and finance. Spillovers from foreign economies can be sizable for the United States as well, especially in the current environment in which many central banks are tightening at an unprecedentedly rapid pace in their commitment to fight inflation aggressively. Our analysis highlights that, should central banks misperceive spillovers when tightening synchronously, they risk giving too much weight to inflation and too little weight to economic activity.

Central banks around the world do take into account these spillovers and internalize them, including using open-economy models for their risk analysis that incorporate how their monetary policies affect other countries and how monetary policies abroad affect domestic variables relevant to their mandates. In a world facing unusually high uncertainty and being buffeted by large shocks, however, it is especially challenging to estimate spillovers and there are concerns that policymakers may underestimate them. In such a case, there is a risk of overtightening that central banks need to be, and we believe are, cognizant of. But policymakers have a tough balancing act to manage as they must also calibrate policy tightening to prevent the deanchoring of long-term inflation expectations.

References

Ahmed, Shaghil, Ozge Akinci, Albert Queralto (2021). "U.S. Monetary Policy Spillovers to Emerging Markets: Both Shocks and Vulnerabilities Matter," International Finance Discussion Papers 1321. Washington: Board of Governors of the Federal Reserve System. https://doi.org/10.17016/IFDP.2021.1321

Ammer, John, Michiel De Pooter, Christopher Erceg, and Steven Kamin (2016). "International Spillovers of Monetary Policy," IFDP Notes. Washington: Board of Governors of the Federal Reserve System, February 8, 2016. https://doi.org/10.17016/2573-2129.15

Christiano, Lawrence, Martin Eichenbaum, and Charles Evans (2005). "Nominal Rigidities and the Dynamic Effects of a Shock to Monetary Policy," Journal of Political Economy, vol. 113 (1), pp. 1-45.

Curcuru, Stephanie E., Michiel De Pooter, and George Eckerd (2018). "Measuring Monetary Policy Spillovers between U.S. and German Bond Yields," International Finance Discussion Papers 1226. https://doi.org/10.17016/IFDP.2018.1226

Erceg, Christopher J., Luca Guerrieri, and Christopher Gust. "SIGMA: a new open economy model for policy analysis." (2005), International Journal of Central Banking.

Gagnon, Joseph E., and Madi Sarsenbayev (2021), "Dollar Not So Dominant: Dollar Invoicing Has Only a Small Effect on Trade Prices," PIIE Working Paper 21-16 (Washington: Peterson Institute for International Economics, December), https://www.piie.com/sites/default/files/documents/wp21-16.pdf.

Gertler and Karadi (2011), "A Model of Unconventional Monetary Policy," Journal of Monetary Economics

Gilchrist, Simon, David López-Salido, and Egon Zakrajšek. 2015. "Monetary Policy and Real Borrowing Costs at the Zero Lower Bound." American Economic Journal: Macroeconomics, 7 (1): 77-109.

Gopinath, Gita, Emine Boz, Camila Casas, Federico J. Díez, Pierre-Olivier Gourinchas, and Mikkel Plagborg-Møller. 2020. "Dominant Currency Paradigm." American Economic Review, 110 (3): 677-719.

Iacoviello, M and G Navarro (2019), "Foreign effects of higher US interest rates", Journal of International Money and Finance 95: 232-250.

Lane, P. "The yield curve and monetary policy." Public lecture for the Centre for Finance and the Department of Economics at University College London (2019).

Rey, H (2013) "Dilemma not Trilemma: The global financial cycle and monetary policy independence", paper presented at the Jackson Hole Symposium, August 2013. Available at http://www.kansascityfed.org/publications/research/escp/escp-2013.cfm

Smets, Frank, and Rafael Wouters (2007). "Shocks and Frictions in US Business Cycles: A Bayesian DSGE Approach," American Economic Review, 97(3): 586-606.

Appendix: Description of Models

Benchmark Model

The model is a dynamic stochastic general equilibrium (DSGE) framework that includes two country blocks: a "U.S." block and a "rest of the world" block. It incorporates an array of nominal and real rigidities calibrated using historical data to produce empirically plausible dynamics, as in Christiano, Eichenbaum, and Evans (2005) and Smets and Wouters (2007). These include habit formation in consumption and adjustment costs on investment, which imply a gradual adjustment of domestic demand to real interest rates; nominal price and wage rigidities captured by Calvo-style staggered contracts by price and wage setters, implying that the behavior of price and wage inflation satisfies a "Phillips curve'' relation; and dynamic price and wage indexation, whereby lagged price and wage inflation enter the respective Phillips curves. The model also includes a "financial accelerator" effect on investment spending, following the approach of Gertler and Karadi (2011).

On the open economy side, the model assumes that both consumers and firms face costs of adjusting the ratio of imports to domestically-produced goods in their consumption and investment baskets. This formulation implies that import demand varies directly with domestic absorption and inversely with the relative price of imported goods, but with the elasticity to relative price changes dampened in the near term due to the adjustment costs. The benchmark model assumes that exporters in both countries practice "producer currency pricing," whereby export prices are set (and are rigid) in the producer's currency. This feature implies that the pass-through of exchange rate changes into import prices is high for all exporters (in the U.S. and abroad).

Dollar Dominance Model

The dollar dominance model has a similar basic structure as the benchmark model, but departs in two important ways: first, following the "dominant currency" paradigm, it assumes that all exporters set prices in dollars—that is, U.S. exporters are set in dollars as in the benchmark model, but foreign export prices are set in dollars also. This feature reduces the pass-through of exchange rate changes into the foreign block's export prices. Second, a significant fraction of foreign firms' liabilities are denominated in dollars, while their assets are denominated in the local currency. This currency mismatch between assets and liabilities makes foreign firms' balance sheets vulnerable to exchange rate depreciation, in a way that magnifies the financial accelerator.

Unlike the benchmark model, in which uncovered interest parity (UIP) holds, the dollar-dominance model features endogenous deviations from UIP—which arise due to limits in the ability of foreign borrowers to arbitrage between debt denominated in different currencies—with premiums on foreign currencies wider when foreign borrowers' balance sheets weaken. Combined with the presence of dollar debt on balance sheets, this feature magnifies the exchange rate response to a given shift in U.S. monetary policy.

1. Federal Reserve Board, Division of International Finance. All errors and omissions are responsibility of the authors. The views expressed in this note are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Board of Governors of the Federal Reserve System or of anyone else associated with the Federal Reserve System. We would like to thank David Yu for valuable research assistance. Return to text

2. See Obstfeld (2022). Return to text

3. See Ammer, De Pooter, Erceg, and Kamin (2016) for an extended discussion and quantification of these channels. Return to text

4. The financial channel has been documented in recent academic literature, including Rey (2013) and Iacoviello and Navarro (2018). Return to text

5. Estimates of financial spillovers based on this approach can be found in Curcuru, De Pooter, and Eckerd (2018). Return to text

6. For details on the SIGMA model see, for example Erceg, Guerrieri and Gust (2005). Return to text

7. The model is based on Ahmed, Akinci and Queralto (2021). Foreign countries, particularly emerging market economies, now borrow in their own currency to a much greater extent than in the 1990s, when vulnerabilities due to currency mismatch (known as "original sin") were much more prevalent than they are now. Carstens and Shin (2019) argue that despite this development, financial vulnerabilities to dollar appreciation remain, as currency mismatch has shifted to global lenders—a phenomenon they dub "original sin redux". Return to text

8. For evidence in favor of the dominant status of the dollar in export pricing, see Gopinath, Boz, Casas, Diez, Gourinchas, and Plagborg- Møller (2020). However, some studies caution that the assumption that foreign exporters set prices in dollars might overestimate the effects of the dollar on global trade prices, see, for example Gagnon and Sarsenbayev (2021). Return to text

9. See Appendix for more-detailed descriptions of the models. Return to text

10. In the benchmark model, we assume that domestic monetary tightening triggers an increase in the domestic 10‑year term premium of 10 basis points. This value is a conservative estimate based on the evidence in Gilchrist, López-Salido and Zakrajšek (2015) for the U.S. or in Lane (2019) for the euro area. In addition, we assume that, in response to domestic tightening, foreign term premiums rise by 5 basis points. The magnitude of this spillover on foreign term premiums is in line with the empirical evidence in in Curcuru, De Pooter, and Eckerd (2018). In the "dollar dominance" simulation, we assume foreign term premiums rise by 10 basis points instead of 5 basis points due to tighter foreign financial constraints. Return to text

Caldara, Dario, Francesco Ferrante, and Albert Queralto (2022). "International Spillovers of Tighter Monetary Policy," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, December 22, 2022, https://doi.org/10.17016/2380-7172.3238.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.