FEDS Notes

July 02, 2020

Modeling the Global Effects of the COVID-19 Sudden Stop in Capital Flows

Ozge Akinci, Gianluca Benigno, and Albert Queralto1

The COVID-19 outbreak has triggered unusually fast outflows of dollar funding from emerging market economies (EMEs).2 These outflows are known as sudden stop episodes, and are typically followed by economic contractions.3 In this note we provide an assessment of the macroeconomic effects of the COVID-induced sudden stop of capital flows to EMEs, using an open-economy DSGE model we recently developed (see Akinci and Queralto 2019). Unlike existing frameworks, like the Federal Reserve Board's SIGMA model (Erceg et al. 2008), our model features both domestic and international financial constraints, making it well-suited to capture the effects of an outflow of dollar funding. The model predicts output losses in EMEs due in part to the adverse effect of local currency depreciation on private-sector balance sheets with dollar debts. The financial stresses in EMEs, in turn, spill back to the U.S. economy, through both trade and financial channels. The model-predicted output losses are persistent (consistent with previous sudden stop episodes as shown in Benigno et al. 2020), with financial effects being a significant drag on the recovery. We stress that we are only tracing out the effects of one particular channel (the stop of capital flows and its associated effect on funding costs) and not the totality of COVID-related effects.

The Macroeconomic Effects on EMEs of the Sudden Stop Can Be Sizable

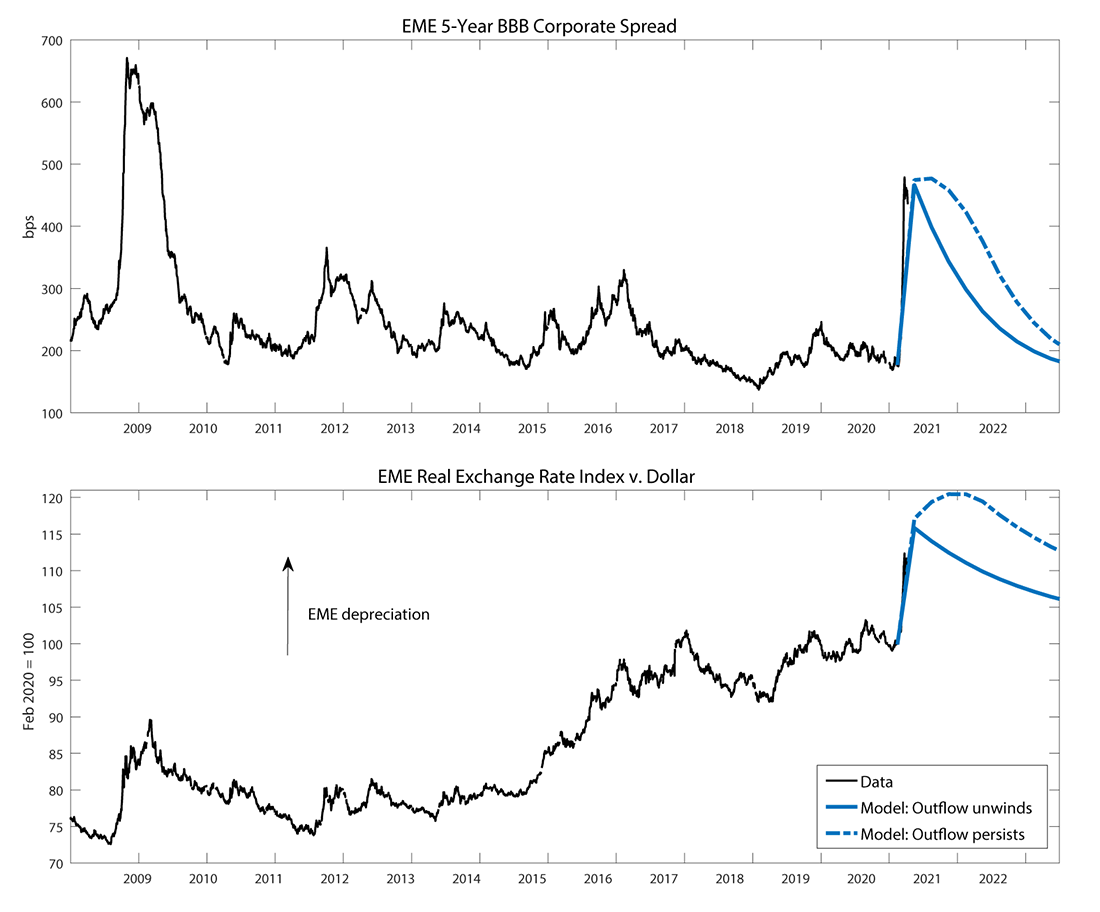

The chart below shows the evolution of EME credit spreads and exchange rates against the dollar since 2008. Credit spreads tightened and the exchange rate depreciated at an unprecedented speed in the wake of the COVID-19 outbreak in the United States: spreads rose 300 basis points and EME currencies fell 15 percent in just a few weeks since late February.

Notes: The spread shown in the top panel is measured as the difference in yields between five-year BBB corporate bonds and government bonds of the same maturity. It includes bonds issued by a broad set of both Asian (including China) and Latin American EMEs. The bottom panel shows the Federal Reserve Board's dollar index against EME currencies.

Sources: ICE Data Indices, LLC, used with permission; Board of Governors of the Federal Reserve System; authors' calculations.

We capture the sudden stop to capital flows in the model through a sharp tightening of the international credit constraint, which impairs EME borrowers' ability to roll over their short-term dollar debt. We size the shock so the model matches the rise in credit spreads seen since February. The exchange rate depreciation against the dollar predicted by the model roughly matches what has occurred so far.

We consider two scenarios for the evolution of the capital outflow pressure in the coming months, capturing different assumptions about the possible evolution of COVID-related risk aversion of global investors. In the first, the outflow pressure simply unwinds from its recent peak, at a rate chosen to replicate the historical persistence in the spread series. In the second, capital outflow pressures persist for a year before easing.

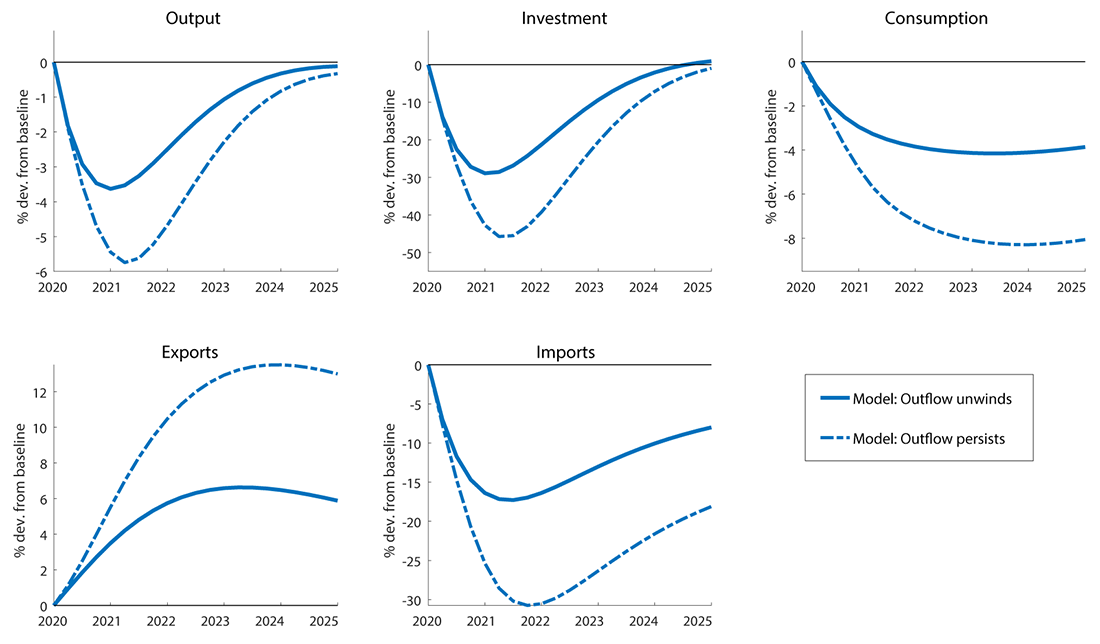

The effects on EMEs of the sudden stop shock are shown in the chart below. As borrowing constraints tighten and currencies depreciate, EME borrowers' balance sheet deteriorate as firms struggle with their dollar-denominated debt. This leads to a sharp rise in the cost of capital, depressing investment spending. Because exporting firms set prices in dollars, the boost to exports from currency depreciation is relatively weak: exports rise by little in 2020 and 2021 (see also research documenting evidence consistent with this feature of the model), while imports plunge.4 Despite an improvement in net exports, economic activity drops sharply as domestic purchases plummet. Overall, the model predicts significant adverse effects on EME activity owing to the sudden stop of capital flows. As one might expect, these adverse effects are estimated to be much larger if the capital outflow pressure remains elevated, with the drag on EME GDP reaching nearly 6 percent by mid-2021.

Source: Authors' calculations.

Loosening Monetary Policy Can Help

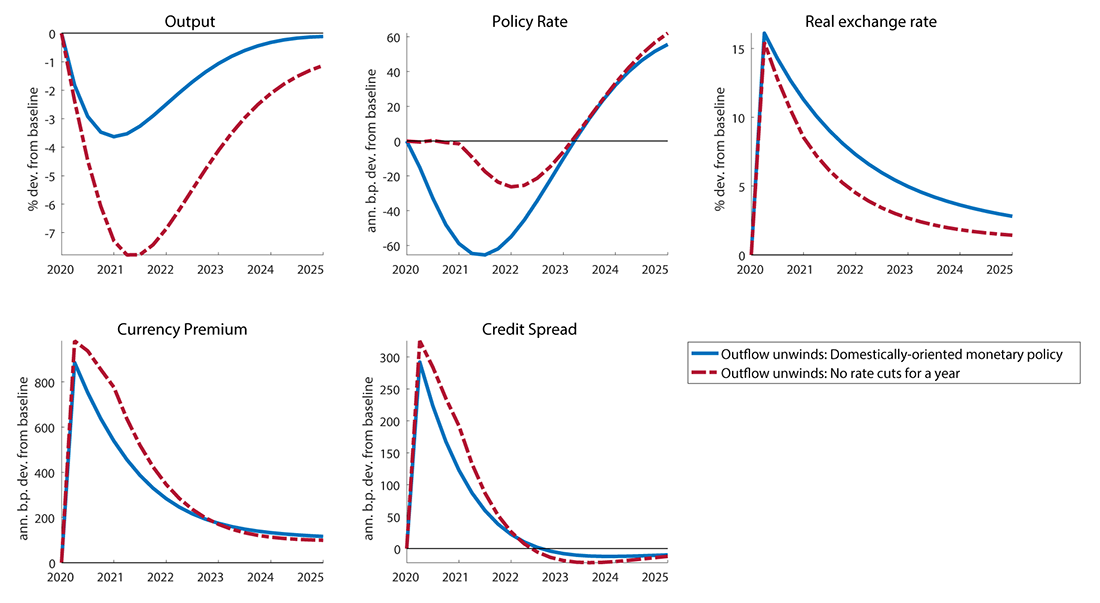

Our baseline simulation assumes a domestically oriented monetary policy rule, which implies that EME monetary authorities ease policy substantially in the wake of the sudden stop (see Aoki et al. 2020 for an analysis of the role of financial policies in EMEs in these circumstances). Our model shows that loosening monetary policy can help mitigate the adverse effects of the sudden stop in flows.

To illustrate, as shown in the chart below, we assume an alternative scenario in which EME central banks avoid cutting rates for a year after the onset of the shock, perhaps motivated by fears that such easings would exacerbate capital outflows and currency depreciation. GDP drops precipitously, more than twice as much compared to a loosening of policy, despite the presence of dollar-denominated debt. The reason is that for the typical borrower, currency depreciation raises the value of just a fraction of liabilities, while contractionary policy triggers a general decline in domestic asset prices, adversely affecting the typical firm.

In fact, tight policy can be particularly perverse in this environment. Our model predicts that capital outflows accelerate when local balance sheets weaken, as global lenders become even more leery of lending to these borrowers. This explains the wider local currency premium in the "no rate cuts" scenario, which works to offset the effect of the higher policy rate on the exchange rate. The net effect is a nearly unchanged path of the exchange rate under the tighter policy, at the cost of a much more severe output contraction. In short, cutting too little too late has devastating real consequences, at little gain in terms of exchange rate stability.5

Source: Authors' calculations.

Spillbacks to the United States Operate through Trade and Financial Channels

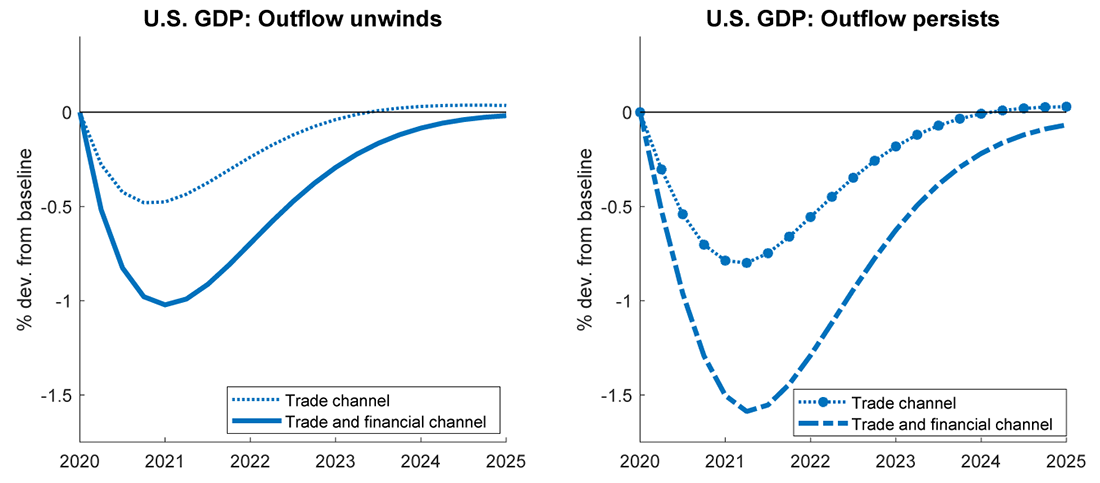

Our model estimates the sudden stop in EMEs impacts the U.S. economy through both trade and financial channels, as shown in the chart below. 6

Figure 4. Financial stresses in EMEs spill back to the U.S. economy through trade and financial channels

Source: Authors' calculations.

The trade channel operates through a fall in U.S. exports due to lower foreign demand, both because EME domestic purchases plummet and because U.S. goods become more expensive as the dollar appreciates. Overall, U.S. GDP declines by about 0.75 percent below the baseline solely due to the trade channel in the scenario in which EME capital outflow pressures persist.

The financial channel operates through U.S. banks' balance sheets exposure to EME risks. As discussed earlier, the sudden stop causes a sharp fall in returns on EME assets. Lower returns on these assets, in turn, erode the value of some U.S. bank assets, causing the financial accelerator to kick in: the initial drop to bank asset values is amplified to cause a fall in economy-wide asset prices generating higher U.S. credit spreads and lower investment spending. This channel also brings GDP down 0.75 percent relative to the baseline. As a result, in the scenario in which EME outflow pressure persists, U.S. GDP falls by 1.5 percent below baseline by early 2021, as both U.S. exports and investment spending decline. It is also important to note that the hit to U.S. GDP is quite persistent, as financial conditions remained fragile for some time.

One can argue that the model's estimate for the magnitude of spillbacks likely constitutes a lower bound. First, we abstract from indirect exposures of U.S. banks' balance sheets to EME risks through other advanced economies, especially the U.K., Germany, and France. Second, the model does not consider supply-side effects linked with global supply chains, of which many EMEs are an important part. One would expect such effects to contribute to a larger and more persistent drag on the U.S. economic outlook.7

Currency Swaps Can Mitigate the Financial Shock

In the model, the initiating shock is a sharp increase in the cost of accessing dollar funding markets (see Kalemli-Ozcan 2019 and Giovanni et al. 2017 for recent work emphasizing similar channels). The model captures the impact of this shock on both the financial and non-financial sectors in EMEs needing to roll over their dollar debt.8 EME borrowers have to substitute dollar-funding needs with domestically-sourced funding, but the cost of the latter skyrockets due to deteriorating balance sheet conditions. The economy thus suffers a downturn caused by firms losing access to dollar funding. The local currency depreciation caused by the economic slowdown damages local balance sheets, generating a downward spiral in which weakening balance sheets and a depreciating currency reinforce each other and contribute to financial stress. In this environment, timely provision of dollar liquidity to illiquid borrowers can help dampen the downward spiral. The model suggests the net benefits of liquidity provision policies are increasing in the stress in credit markets induced by the shock.9

In this regard, facilities such as the swap lines and the FIMA repo facilities set up by the Federal Reserve have helped support the smooth functioning of dollar funding markets around the world and thus reduced the likelihood that EMEs will face acute dollar funding outflows. This should moderate some of the negative macroeconomic effects of the capital outflows on their own economies by curtailing the rise in credit spreads. Success in doing so would also limit the adverse spillbacks to output and employment in the United States. However, the swap lines and FIMA repo facility are designed to address short-term liquidity problems faced by solvent borrowers. Other policy actions currently being taken, such as the new IMF programs to address longer-term balance-of-payments issues and the debt repayment standstills agreed by the G-20, will also prove helpful in addressing the deeper and more prolonged distress that some EMEs may experience as a consequence of the pandemic and its global economic effects.

References

Akinci, Ozge and Albert Queralto (2019). Exchange Rate Dynamics and Monetary Spillovers with Imperfect Financial Markets. Board of Governors of the Federal Reserve System, International Finance Discussion Papers, Number 1254.

Akinci, Ozge and Ryan Chahrou (2018). Good News, Leverage, and Sudden Stops. Federal Reserve Bank of New York, Liberty Street Economics.

Alfaro, Laura, Alejandro Cuñat, Harald Fadinger, and Yanping Liu, (2018). The Real Exchange Rate, Innovation and Productivity: Heterogeneity, Asymmetries and Hysteresis. National Bureau of Economic Research.

Amiti, Mary, Oleg Itskhoki, and Jozef Konings (2014). Importers, Exporters, and Exchange Rate Disconnect. American Economic Review, July 2014, 104 (7), 1942-78.

Aoki, Kosuke, Gianluca Benigno, and Nobuhiro Kiyotaki (2019). Monetary and Financial Polices in Emerging Markets. Working paper (LSE, Princeton University, and University of Tokyo).

Benigno, Gianluca, Andrew Foerster, Christopher Otrok, and Alessandro Rebucci (2020). On the legacy of financial crises: Lessons from Mexico's sudden stop history. VOX CEPR Policy Portal.

Bruno, Valentina, Se-Jik Kim, and Hyun Shin (2018). Exchange Rates and the Working Capital Channel of Trade Fluctuations. AEA Papers and Proceedings, May 2018, 108, 531-36.

Calvo, Guillermo A., Alejandro Izquierdo, and Ernesto Talvi (2006). Sudden Stops and Phoenix Miracles in Emerging Markets. American Economic Review, May 2006, 96 (2), 405-410.

di Giovanni, Julian. The Impact of the Coronavirus on U.S. GDP Growth via the Global Supply Chain: A Quantitative Analysis. March 2020.

di Giovanni, Julian, Sebnem Kalemli-Ozcan, Mehmet Fatih Ulu, and Yusuf Soner Baskaya (2017). International Spillovers and Local Credit Cycles. Working Paper 23149, National Bureau of Economic Research, February 2017.

Erceg, Christopher J, Luca Guerrieri, and Christopher Gust (2006). SIGMA: A New Open Economy Model for Policy Analysis. International Journal of Central Banking, 2006.

Gertler, Mark and Nobuhiro Kiyotaki (2010). Financial Intermediation and Credit Policy in Business Cycle Analysis. Handbook of Monetary Economics, Volume 3, 2010, 547-599.

Goldberg, Linda and Sarah Ngo Hamerling (2020). How Covid-19 Pressures on International Capital Flows Stack Up. May 2020.

Goldberg, Linda S. and Cedric Tille (2008). Vehicle currency use in international trade. Journal of International Economics, December 2008, 76 (2), 177{192.

Gopinath, Gita, Emine Boz, Camila Casas, Federico J. Díez, Pierre-Olivier Gourinchas, and Mikkel Plagborg-Møller (2020). Dominant Currency Paradigm. American Economic Review, March 2020, 110 (3), 677-719.

IIF (2019). International Institute of Finance Capital Flows Tracker: The Covid-19 Cliff. April 2019.

IMF (2020). Policy Responses to Covid-19. April 2020.

Appendix: Model

This appendix includes details on the key features of the model. EME banks and nonfinancial corporations fund local assets by issuing short-term debt to domestic residents in local currency, and internationally in dollars. Dollar and local-currency funding are imperfect substitutes: dollar funding is attractive because it pays a lower yield than domestic-currency debt, but comes with tighter borrowing constraints because local assets have less value as collateral for international loans than they do for domestic loans.

An implication of this imperfect substitutability is that EMEs' interest differentials against the U.S. are not fully arbitraged away. Instead, EME borrowers' balance sheet health can directly impact the dollar exchange rate of EME currencies, via a deviation from interest parity: a positive "currency premium" exists on the local safe rate over the dollar rate, which depends inversely on the balance sheet health of local borrowers—a consequence of the tighter constraints associated with issuing dollar debt. Thus, the model partly endogenizes capital outflow pressures (proxied by deviations from interest parity) by tying the latter to EME borrowers' financial health. This prediction is consistent with evidence in Giovanni et al. (2017), who show that the premium on domestic relative to foreign borrowing costs in EMEs tends to fluctuate countercyclically and rise when global financial conditions tighten.

We model the COVID-19 dollar outflow as a tightening in EME borrowers' constraint associated with issuing dollar debt: due to a turn in sentiment, global lenders become leery about lending to EME banks and firms, requiring more collateral per unit lent. EME firms respond by substituting into domestic-currency alternatives, but the latter are a poor substitute because they require a much higher yield. As the currency premium widens, EME currencies depreciate, further weakening balance sheets end exacerbating the outflow.

1. Ozge Akinci is a senior economist and Gianluca Benigno is an assistant vice president in the Federal Reserve Bank of New York's Research and Statistics Group. Albert Queralto is a principal economist at the Federal Reserve Board. The authors are very grateful to Shaghil Ahmed, Linda Goldberg, Steven Kamin, and Tom Klitgaard for comments and suggestions. This FEDS note was published jointly as a Liberty Street Economics blog post. The views expressed here are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Board of Governors of the Federal Reserve System or of anyone else associated with the Federal Reserve System. Return to text

2. For example, IIF (2020) documents that capital outflows from EMEs since late January of this year are many times larger than at the peak of previous crisis episodes. Return to text

3. See Calvo et al. (2006) or Akinci and Chahrour (2018), among others. Return to text

4. Goldberg and Tille (2008) and Gopinath et al. (2020) provide empirical evidence showing that a large fraction of international trade is invoiced in a U.S. dollars. This model feature is also consistent with firm-level evidence suggesting a muted impact of large exchange rate movements on exports – see Amiti et al. (2014) and Alfaro et al. (2008). Return to text

5. According to the IMF's Policy Tracker, several EMEs have eased monetary policy some in response to the COVID-19 sudden stop. However, as documented in Goldberg and Hamerling (2020), EMEs have generally cut rates by less than advanced economies in the wake of the COVID-19 shock. Return to text

6. In the model, the share in GDP of U.S. exports to the EME bloc (which consists of a broad set of emerging economies, including China), and vice versa, is calibrated using recent data from the IMF's Direction of Trade statistics. Regarding the financial sector, in the model EME assets constitute 5 percent of total U.S. banks' assets, consistent with data from the BIS consolidated banking statistics as of year-end 2019. Return to text

7. Giovanni (2020) presents an empirical evaluation of the Covid-19 shock on U.S. growth via global supply chains. Return to text

8. Our model abstracts from some of the specific details related to the dollar funding issue. For example, the BIS in several research papers emphasizes the importance of dollar funding coming from credit-intensive global value chains, and the hedging needs of non-bank actors in the FX swap market to hedge U.S. credit risk. Return to text

9. See, for example, the analysis of liquidity facilities in the work by Gertler and Kiyotaki (2010) that our model builds upon. Return to text

Akinci, Ozge, Gianluca Benigno, and Albert Queralto (2020). "Modeling the Global Effects of the COVID-19 Sudden Stop in Capital Flows," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, July 02, 2020, https://doi.org/10.17016/2380-7172.2586.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.