FEDS Notes

September 27, 2017

Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence from the Survey of Consumer Finances

Lisa J. Dettling, Joanne W. Hsu, Lindsay Jacobs, Kevin B. Moore, and Jeffrey P. Thompson with assistance from Elizabeth Llanes

Newly released data from the Survey of Consumer Finances (SCF) show that wealth rose for families in all race and ethnicity groups between 2013 and 2016. The long-standing and substantial wealth disparities between families of different racial and ethnic groups, however, have changed little in the past few years. Wealth losses during the Great Recession, and the magnitude and timing of the recovery, also varied substantially across families grouped by race and ethnicity. This FEDS Note explores in more detail these patterns and average differences in financial and demographic profiles of families grouped by race/ethnicity.

Recent trends in wealth-holding

We first analyze trends in total net worth among families classified, according to their self-identification during the interview, as white non-Hispanic, black or African American non-Hispanic, Hispanic or Latino, and other or multiple race (we will henceforth refer to these groups as white, black, Hispanic, and other, respectively).1 Net worth is defined as the difference between families' gross assets and their liabilities.2 We will describe patterns at the median (the typical household within each group) and at the mean (the average within each group).

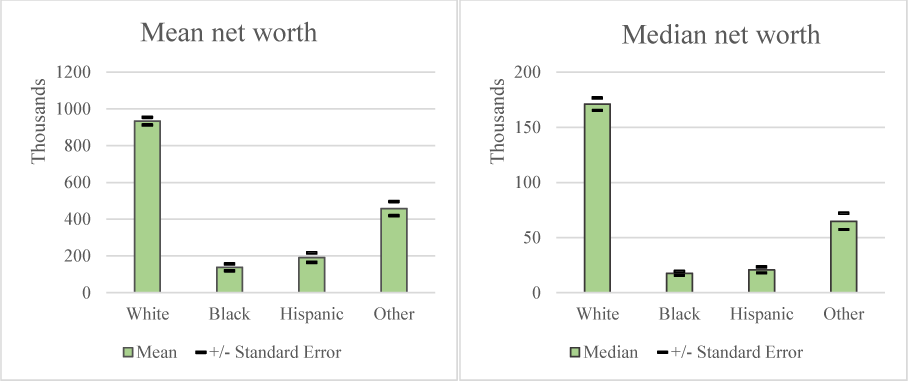

In 2016, white families had the highest level of both median and mean family wealth: $171,000 and $933,700, respectively (figure 1). Black and Hispanic families have considerably less wealth than white families. Black families' median and mean net worth is less than 15 percent that of white families, at $17,600 and $138,200, respectively. Hispanic families' median and mean net worth was $20,700 and $191,200, respectively. Other families--a diverse group that includes those identifying as Asian, American Indian, Alaska Native, Native Hawaiian, Pacific Islander, other race, and all respondents reporting more than one racial identification--have lower net worth than white families but higher net worth than black and Hispanic families. The same patterns of inequality in the distribution of wealth across all families are also evident within race/ethnicity groups: For each of the four race/ethnicity groups, the mean is substantially higher than the median, reflecting the concentration of wealth at the top of the wealth distribution.

Thousands of 2016 dollars

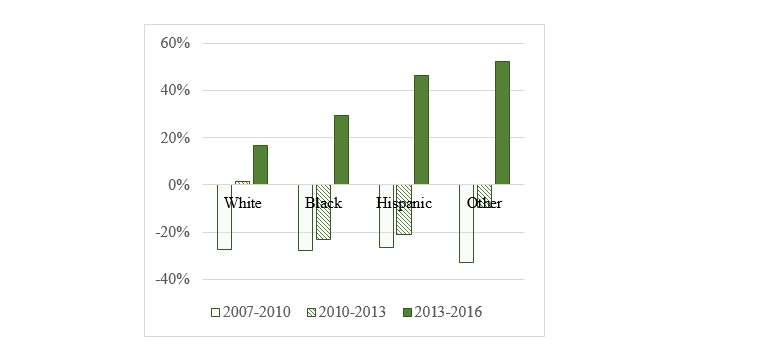

Between 2013 and 2016, median net worth rose for all groups (figure 2). Growth rates for the 2013-16 period were proportionally larger for Hispanic, other, and black families, rising between 30 and 50 percent, compared with white families, whose net worth rose 17 percent. Even with the large percentage gains for black and Hispanic families, the white-black gap in median net worth increased from $132,800 in 2013 to $153,500 in 2016, and the white-Hispanic gap increased from $132,200 in 2013 to $150,300 in 2016.

Percent change

Source: Federal Reserve Board, Survey of Consumer Finances.

Experiences in the Great Recession (2007 to 2010) and the immediate aftermath (2010 to 2013) also varied across groups. Median net worth fell about 30 percent for all groups during the Great Recession. However, for black and Hispanic families, net worth continued to fall an additional 20 percent in the 2010-13 period, while white families' net worth was essentially unchanged, and other families' net worth fell a more modest 10 percent.

Household financial profile

The detailed household balance sheet information collected in the SCF allows us to move beyond total wealth to explore differences in income and the types of assets and debt held by families within each race/ethnicity group.

Wealth tends to increase with income because of higher levels of saving among higher-income families, and because of the feedback effect on higher incomes from the returns generated by accumulated assets.3 In 2016, both median and mean incomes are higher for white families than for all other groups of families ($61,200 and $123,400, respectively) (table 1). Median and mean incomes are considerably lower for black and Hispanic families, whose median incomes are $35,400 and $38,500, respectively. Median and mean incomes for other families fall in between those of white families and black and Hispanic families.

Table 1. Household financial profile by race/ethnicity, 2016 survey

| White | Black | Hispanic | Other | |

|---|---|---|---|---|

| Income: | ||||

| Median | 61.2 | 35.4 | 38.5 | 50.6 |

| Mean | 123.4 | 54.0 | 57.3 | 86.9 |

| Net Worth: | ||||

| Median | 171 | 17.6 | 20.7 | 64.8 |

| Mean | 933.7 | 138.2 | 191.2 | 457.8 |

| Percent of families with zero or negative net worth | 9 | 19 | 13 | 14 |

| Assets (percent of families with): | ||||

| Primary residence | 73 | 45 | 46 | 54 |

| Vehicle | 90 | 73 | 80 | 80 |

| Retirement accounts | 60 | 34 | 30 | 48 |

| Business equity | 15 | 7 | 6 | 13 |

| Direct and indirect equity | 61 | 31 | 28 | 47 |

| Debts (percent of families with): | ||||

| Debt secured by primary residence | 46 | 32 | 31 | 38 |

| Vehicle loans | 34 | 33 | 32 | 34 |

| Credit card balances | 42 | 48 | 50 | 44 |

| Education loans | 20 | 31 | 19 | 26 |

| Wealth from housing (for homeowners): | ||||

| Percent of assets in housing | 32 | 37 | 39 | 35 |

| Mean net housing wealth | 215.8 | 94.4 | 129.8 | 220.7 |

| Credit Experiences (percent of families with): | ||||

| Payment-to-income ratio greater than 40% | 6 | 9 | 8 | 9 |

| Late on payments 60 days or more | 5 | 10 | 4 | 9 |

| Denied credit or feared denial | 15 | 35 | 32 | 25 |

Although most families do have some wealth, the number with zero or negative net worth (having debts that exceed assets) is nontrivial and varies by race/ethnicity. Nearly one in five black households has zero or negative net worth. The share of white households without any wealth is considerably smaller, at 9 percent. Hispanic and other households fall somewhere in between white and black families on this measure.

For many families, the primary residence is an important component of the balance sheet. Well over half of white households are homeowners (73 percent), compared with just under half of black and Hispanic households (around 45 percent) and 54 percent of other households. Among homeowners, white households also hold considerably higher levels of equity in their homes. Mean net housing wealth (the value of the home, less any debts on the home) among homeowners is $215,800 among white families but only $94,400 among black families and $129,800 among Hispanic families. White homeowners hold more home equity, but housing accounts for only 32 percent of their total assets, compared with 37 to 39 percent for black and Hispanic homeowners.

The most common type of asset owned by all types of families is vehicles. Ninety percent of white families own a vehicle, compared with 80 percent of Hispanic and other families, and 73 percent of black families. Retirement accounts, including IRAs and 401(k) plans, are also commonly held; 60 percent of white families have these accounts, compared with 34 percent of black families and 30 percent of Hispanic families. A family-owned business is another important component of some families' balance sheets. The highest business ownership rates are among white and other families (around 13 to 15 percent), with black and Hispanic families about half as likely to own a business. Ownership of equities--which may be held directly or indirectly through a retirement account--also varies substantially across groups, with more than 60 percent of white families owning equities, compared with around 30 percent of black and Hispanic families.

Compared with assets, debt is more evenly distributed across families grouped by race/ethnicity. A larger share of white families have debt secured by the primary residence than other groups of families, which partly reflects higher homeownership rates among white families. Vehicle loans are fairly evenly distributed across groups, with around 30 to 35 percent of families having such loans. Credit card debt is also fairly evenly distributed across groups, with between 42 and 50 percent of families having credit card debt. The incidence of education loans varies somewhat across groups. Black families are the most likely to have education debt (31 percent), and Hispanic families are the least likely to have education debt (19 percent).

Families' interactions with credit markets also vary somewhat across groups. Black and other families are the most likely to have high debt payment burdens: 9 percent of these families have debt-payment-to-income ratios above 40 percent. Hispanic families follow closely at 8 percent. Black families are the most likely to be late on payments. Black and Hispanic families have the highest incidence of credit constraints, with about one-third reporting they were either denied credit or did not apply for credit because they feared denial.

Demographic profiles by race/ethnicity

In addition to the differences in the levels and types of wealth previously described, the data also indicate substantial variation by race/ethnicity in many of the factors that are associated with the accumulation of wealth.4 Among the potential reasons that wealth is relatively high among white households, for example, is that they tend to be older, more highly educated, more likely to have received an inheritance, and less likely to be a single parent than their black and Hispanic counterparts (table 2).

Wealth generally increases with age and plateaus or modestly decreases from near-retirement age onward, reflecting life-cycle earnings and saving behavior. Just over half of white households are headed by someone 55 or older, compared with 38 percent of black households and approximately one-fourth for Hispanic households.

Wealth is also correlated with family structure because of higher levels of saving among families with more earners or lower living expenses. Black households stand out for being the least likely to have a married or partnered head--just 37 percent--compared with more than 54 percent for each of the other three groups. White households are the least likely to be headed by a single parent (8 percent), compared with 16 percent among Hispanics and 27 percent among black families. Black families are less likely to be dual-earner households than the other groups of families.

Table 2. Demographic and economic profile by race/ethnicity, 2016 survey

| White | Black | Hispanic | Other | |

|---|---|---|---|---|

| Age distribution | ||||

| Under age 35 | 18 | 21 | 25 | 28 |

| 35 to 54 | 31 | 40 | 49 | 42 |

| 55 to 74 | 37 | 30 | 22 | 24 |

| 75 and older | 14 | 8 | 4 | 5 |

| Family structure | ||||

| Married or with partner | 61 | 37 | 62 | 54 |

| Single without kids | 31 | 36 | 23 | 34 |

| Single with kids | 8 | 27 | 16 | 12 |

| With kids | 36 | 47 | 61 | 45 |

| With two earners | 29 | 18 | 27 | 25 |

| Education | ||||

| Less than high school | 8 | 17 | 36 | 12 |

| High school only | 26 | 29 | 25 | 21 |

| Some college, no degree | 15 | 20 | 12 | 18 |

| Associates degree | 12 | 11 | 10 | 13 |

| Bachelor's degree or higher (BA+) | 39 | 23 | 17 | 36 |

| Both head and spouse/partner have BA+ | 18 | 5 | 6 | 16 |

| At least one of the head's parents had BA+ | 31 | 19 | 14 | 36 |

| Family financial assistance | ||||

| Received inheritance | 26 | 8 | 5 | 15 |

| Can get $3,000 from family or friends in emergency | 71 | 43 | 49 | 64 |

White and other heads of households are much more likely to have obtained a college degree or some advanced level of higher education (39 percent and 36 percent, respectively). In contrast, only 23 percent of black heads of households and 17 percent of Hispanic heads of households have a college degree or higher level of education. Furthermore, the proportion of families that consist of two spouses who both have at least a college degree also varies by group: 18 percent of white families, 5 percent of black families, 6 percent of Hispanic families, and 16 percent of other families.

These differences across groups in educational attainment appear to persist across generations as well. For 31 percent of white families, one or both parents of the head had at least a bachelor's degree, compared with 19 percent of black families and 14 percent of Hispanic families.

Intergenerational relationships can also influence how families accumulate wealth--for example, receiving assets from relatives in the form of inheritances and other major gifts. In addition, households are better able to maintain their wealth when they can count on help from family and friends to weather unexpected financial emergencies. White families stand out as the most likely to have received an inheritance or other major gift--26 percent of white families have received an inheritance, compared with less than 10 percent of black families and Hispanic families. Most white households (71 percent) report being able to get $3,000 from family or friends in a financial emergency, compared with less than half of Hispanic and black households (49 percent and 43 percent, respectively).

The four race/ethnicity groups vary in many demographic and economic factors that are correlated with household wealth, but even accounting for variation in all of the demographic factors, the gaps between families grouped by race/ethnicity remain (although they are considerably smaller). Results from regression analyses show that accounting for the demographic factors in table 2 shrinks the gap to about one-third of the overall gap for white families and black families, and about one-fifth of the overall gap for white families and Hispanic families.5 Still, the adjusted gaps in net worth remain sizable.

Recent wealth changes for race/ethnicity groups by educational attainment

Educational attainment is a significant predictor of income and wealth: 2016 SCF data indicate that overall, families with a bachelor's degree have mean and median wealth values that are more than five times the values for less educated families. This pattern is also evident within each of the race/ethnicity groups, though the magnitude of the difference by education varies across the four race/ethnicity groups (table 3). For example, the median college-educated black family's net worth is about six times that of the median black family with less education, and the ratio is about 4.5 for Hispanic families.

Table 3. Mean and median net worth by race and educational attainment of head, 2013-16 surveys

| Median net worth | Mean net worth | |||

|---|---|---|---|---|

| 2013 | 2016 | 2013 | 2016 | |

| No bachelor's degree | ||||

| White | 87.1 | 98.1 | 323.1 | 367.8 |

| Black | 10.3 | 11.6 | 78.9 | 99.3 |

| Hispanic | 13.1 | 17.5 | 76.3 | 105.7 |

| Other | 17.4 | 34.3 | 128.8 | 183.7 |

| Bachelor's degree or higher | ||||

| White | 375.5 | 397.1 | 1,440.1 | 1,821.3 |

| Black | 36.8 | 68.2 | 184.4 | 271.2 |

| Hispanic | 58.0 | 77.9 | 401.8 | 609.6 |

| Other | 216.1 | 210.2 | 813.0 | 941.0 |

In addition to substantial heterogeneity within race/ethnicity groups by education, there are also large disparities across race/ethnicity groups for families with similar levels of education. Among households headed by someone with a college degree, net worth is substantially higher for white families than for the other three groups of families. The median net worth of college graduates in 2016 was $397,100 for white families, but well below $100,000 for black families and Hispanic families. Of course, even within these race/ethnicity and education groups, many of the demographic and economic differences highlighted in tables 1 and 2 help to explain some of these patterns.

Growth rates between 2013 and 2016 also varied substantially across race/ethnicity and educational attainment groups. Among college graduates, mean and median wealth grew proportionally more for black and Hispanic households than for other families: mean wealth of college degree holders rose approximately 50 percent for black and Hispanic households and only 26 percent for white families. Among less educated families, proportional growth rates at the mean and median were highest for Hispanic families and other families.

This FEDS Note has described broad patterns in wealth-holding across families grouped by race and ethnicity, and some of the economic and demographic determinants of those patterns, using newly released data from the SCF. While all groups experienced losses during the Great Recession, the 2016 SCF data reveal broad-based growth in household net worth across groups since 2013. However, disparities in wealth-holding, asset-holding, and debt-holding remain: White families have considerably more wealth than black, Hispanic, and other families, even among those with similar levels of education. While this FEDS Note documents substantial heterogeneity across race/ethnicity groups, there is substantial variation in family circumstances and financial experiences within each group as well.

1. For more on the race/ethnicity classifications used in this FEDS Note, see the appendix to Jesse Bricker, Lisa J. Dettling, Alice Henriques, Joanne W. Hsu, Lindsay Jacobs, Kevin B. Moore, Sarah Pack, John Sabelhaus, Jeffrey Thompson, and Richard A. Windle (2017), "Changes in U.S. Family Finances from 2013 to 2016: Evidence from the Survey of Consumer Finances," Federal Reserve Bulletin vol. 103 (henceforth, the Bulletin article). The other or multiple race group consists of a very racially/ethnically diverse set of families, including those identifying as Asian, American Indian, Alaska Native, Native Hawaiian, Pacific Islander, other race, and all respondents reporting more than one racial identification. Because of small sample sizes, we do not have statistical power to further disaggregate this group of families. In 2016, families reporting more than one racial identification were the largest subgroup of the other or multiple race group (about 50 percent of families), followed by Asian families (about 30 percent of families), though the composition of this group varies over time. Because of the varied composition of the other group and changes in its composition over time, readers should exercise caution when making inferences. Return to text

2. See the appendix to the Bulletin article for more details on components of net worth in the SCF. Return to text

3. See the Bulletin article for more on savings patterns by income. Return to text

4. For patterns in wealth-holding by family characteristics, see the Bulletin article; Janet L. Yellen (2014), "Perspectives on Inequality and Opportunity from the Survey of Consumer Finances," speech at the Conference on Economic Opportunity and Inequality, Federal Reserve Bank of Boston, Boston, Mass., October 17, https://www.federalreserve.gov/newsevents/speech/yellen20141017a.htm; and Martin Browning and Annamaria Lusardi (1996), "Household Saving: Micro Theories and Micro Facts," Journal of Economic Literature, vol. 34 (December), pp. 1797–855. Return to text

5. These findings are similar for both mean and median net worth. For more details on the methods used here, and for more extensive analysis using additional factors, see Jeffrey P. Thompson and Gustavo A. Suarez (2015), "Exploring the Racial Wealth Gap Using the Survey of Consumer Finances," Finance and Economics Discussion Series 2015-076 (Washington: Board of Governors of the Federal Reserve System, August), http://dx.doi.org/10.17016/FEDS.2015.076. Return to text

Dettling, Lisa J., Joanne W. Hsu, Lindsay Jacobs, Kevin B. Moore, and Jeffrey P. Thompson (2017). "Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence from the Survey of Consumer Finances," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, September 27, 2017, https://doi.org/10.17016/2380-7172.2083.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.