FEDS Notes

August 13, 2018

SOMA's Unrealized Loss: What does it mean?

Brian Bonis, Lauren Fiesthumel, and Jamie Noonan1

In May 2018, the Federal Reserve published its Federal Reserve Banks Combined Quarterly Financial Report for the first quarter of 2018.2 For the first time since 2013, the report showed the System Open Market Account (SOMA) portfolio having an unrealized loss position. In particular, SOMA displayed an unrealized loss position of $462 million. What does it mean for the Fed to have an unrealized loss position on its securities holdings? This Note discusses the various valuation measures of the Fed's securities holdings, what these values mean, and the expected evolution of the value of the SOMA portfolio. Importantly, as discussed below, the SOMA portfolio's unrealized position has no effect on the ability of the Federal Reserve, as a central bank, to meet its financial obligations and pursue its statutory goals of price stability and maximum employment; in addition, it has no implications for the evolution of the Federal Reserve's earnings remittances to the U.S. Treasury or, ultimately, for U.S. taxpayers when, as expected, securities are held to maturity.

1. Differences Between GAAP and Federal Reserve Accounting Principles

The Federal Reserve follows distinct accounting principles, which include a specific approach to report the value of the securities held in the SOMA portfolio (see the technical appendix for more information about the basis of the Reserve Bank accounting policies). On the Federal Reserve's weekly H.4.1 release, securities held outright in the SOMA are reported at face value, while unamortized premiums and discounts associated with those securities are reported on separate line items.3 In the Federal Reserve Banks Combined Quarterly Financial Report, SOMA securities are reported on an amortized cost basis, a valuation that is based on the face value of a security, adjusted in turn for any discounts or premiums associated with the purchase of the security.4 The premium or discount is amortized over the expected life of the security, and the security's value on an amortized cost basis is equal to the total purchase price paid less the amount of the premium or discount that has already been written down. At maturity, the Federal Reserve receives the face value, which at that point equals the security's amortized cost.

Publicly traded companies as well as many private companies in the United States follow GAAP (generally accepted accounting principles) for their financial reporting. Under GAAP, in certain circumstances securities are reported at "fair value."5 Fair value represents the market price that would be received in selling an asset in an orderly transaction between market participants at the measurement date, which is the date reported in the statements. As such, fair value for a fixed-income security is a function of future expected interest rates, which are used to discount the flow of future coupon and principal payments. Under fair value accounting, changes in the market value of a security are recognized as income or loss and affect the income and capital position of a company. For a private company, whose equity holders have a claim on the value of a company's assets, fair value accounting ensures that the financial statements are a reflection of the expected value of a company.

The Federal Reserve is a unique non-profit entity created by the Congress. Any income received in excess of the amount needed to pay expenses and dividends and to maintain surplus at the level of $6.825 billion is, by law, remitted to Treasury and does not affect the capital position or value of the Federal Reserve.6 Member banks hold shares of the Federal Reserve Banks, are paid a fixed dividend, and do not have a claim on the value of Federal Reserve assets, unlike in the case of a private company. Use of fair value accounting would create considerable volatility in Federal Reserve income as the value of its securities portfolio fluctuates over time. This is especially true because the values of Federal Reserve liabilities are not tied to interest rates to a similar degree. While the fair value of securities fluctuates with changes in interest rates, the valuation of a substantial portion of Federal Reserve liabilities does not. Consider, among various items, the case of reserve balances that depository institutions hold with the Federal Reserve. The value of this item, which accounts for a large share of the overall value of Federal Reserve liabilities and, at the same time, plays an important role in the conduct of monetary policy, does not depend on interest rates. Its level, instead, changes when, among other things, SOMA securities are purchased, sold, or eventually reach their maturity. Reporting the securities at amortized cost is more meaningful for the central bank because it provides a more transparent link between the amount of securities held for monetary policy purposes and the corresponding reserve balances.

2. Interest Rates and Unrealized Gains and Losses

Although the Federal Reserve reports its SOMA securities holdings at amortized cost, it also reports, for informational purposes, the fair value of the SOMA portfolio and the resulting unrealized gain or loss position, which is calculated as the difference between the fair value of the portfolio and its amortized cost.7 As noted above, the fair value of securities in SOMA fluctuates with changes in interest rates. Currently, the SOMA portfolio includes primarily Treasury securities and agency mortgage-backed securities (MBS).8 Because market prices of Treasury securities and MBS move inversely with respect to interest rates, when interest rates rise, all else equal, the value of SOMA securities holdings decreases. The resulting decline in the fair value of SOMA securities holdings means that the unrealized gain or loss position will also deteriorate, leading to a smaller unrealized gain or a larger unrealized loss. The converse is true when interest rates fall.

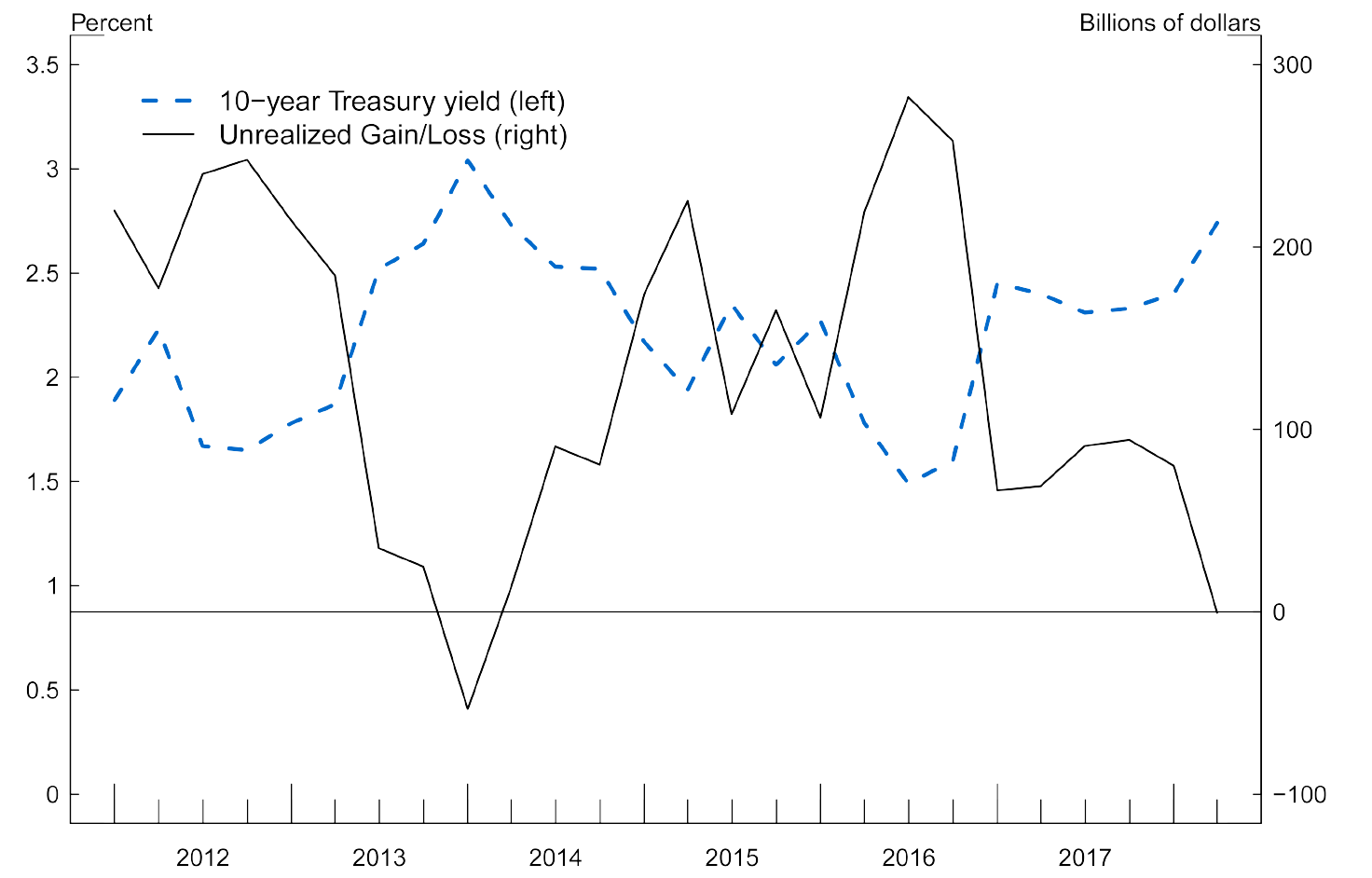

The figure below shows the inverse relationship between the 10-year Treasury yield and the SOMA's unrealized gain/loss position. Generally speaking, during the years following the financial crisis the SOMA portfolio displayed large unrealized gains that were driven by both the historically large portfolio size and the fact that longer-term interest rates had declined after many of the SOMA securities were purchased. Subsequently, as a result of an increase in longer-term interest rates, the SOMA exhibited an unrealized loss position in 2013 and, as indicated at the beginning of this note, most recently in the first quarter of 2018.

Source: Federal Reserve, H.15 Select Interest Rates, https://www.federalreserve.gov/releases/h15/; Federal Reserve, Federal Reserve Banks Combined Quarterly Financial Report and Federal Reserve Banks Combined Financial Statements.

In general, calculating the fair value of a portfolio of securities and the resulting unrealized gain or loss position can require some degree of estimation of the expected payment stream of the underlying securities. As Treasury securities are very liquid assets, market pricing is readily available for every CUSIP. However, to calculate the fair value of agency MBS holdings in the SOMA portfolio, model-based valuation is required due to the embedded prepayment options in the underlying mortgages. Different prepayment model structures and assumptions can lead to different model-based estimates. This means that the fair values calculated by different sources can differ.

3. Monetary Policy and SOMA Gains and Losses

When securities are sold or prepayments from MBS are received, the gains or losses resulting from these transactions become realized and affect the Reserve Banks' net income and remittances to the Treasury. Any realized gains and losses are recorded in the non-interest income portion of the Combined Statements of Operations on the Federal Reserve's Financial Reports. In recent years, the only SOMA securities sales conducted by the Desk were for small-value testing purposes and any gains or losses that were realized did not have a meaningful impact on net income. There are cases, however, in which a significant number of SOMA securities were sold before maturity, and the sales affected the Federal Reserve's net income and remittances to the Treasury. One such circumstance was the Maturity Extension Program (MEP), under which the Federal Reserve sold or redeemed nearly $700 billion of shorter-term Treasury securities between the end of September 2011 and the end of 2012. As interest rates at that time were lower than when the securities were originally purchased, the Federal Reserve, as a result of this program, recorded net gains of $2.3 billion in 2011 and $13.3 billion in 2012.

Looking forward, the FOMC has indicated that securities sales are not anticipated to be part of the balance sheet normalization program. In particular, in the 2014 Policy Normalization Principles and Plans, the Committee announced that it intends to "reduce the Federal Reserve's securities holdings in a gradual and predictable manner primarily by ceasing to reinvest repayments of principal on securities held in the SOMA." This strategy, therefore, implies that the Federal Reserve's Treasury securities will be held until maturity, at which point the Federal Reserve will receive the par values for the securities, thus not realizing any gains or losses. Differently from holdings of Treasury securities, the Federal Reserve's holdings of MBS are subject to prepayment risk. Prepayments of MBS principal can result in small realized gains or losses and have, therefore, analogous implications to those of small-value sales of the securities in the SOMA portfolio. In a declining interest rate environment, principal prepayments are likely to increase, but it would be highly unlikely that the realized losses stemming from prepayments could significantly affect the overall net income result for the Federal Reserve. In an increasing interest rate environment, prepayments would be depressed, leading to muted realized losses on MBS, even as the fair value of MBS would decline. However, these Principles and Plans also note that for agency MBS, "limited sales might be warranted in the longer run to reduce or eliminate residual holdings." If sales were to occur in this situation, then associated realized gains or losses with any sales would affect net income.

Even under the very unlikely hypothetical scenario in which the Fed sold a large amount of securities prior to maturity and incurred a sizable realized loss as a result, the Federal Reserve would still be able to meet its responsibilities and financial obligations. In particular, from a monetary policy standpoint, the losses alone would not affect the amount of depository institutions' reserves held with Federal Reserve Banks and would have no effect on the conduct of monetary policy. Moreover, in the unlikely scenario in which realized losses were sufficiently large enough to result in an overall net income loss for the Reserve Banks, the Federal Reserve would still meet its financial obligations to cover operating expenses. In that case, remittances to the Treasury would be suspended and a deferred asset would be recorded on the Federal Reserve's balance sheet, representing a claim on future net earnings that the Reserve Banks would need to realize before remittances to the Treasury would resume.9 Given that a large portion of the Federal Reserve's liabilities are comprised of Federal Reserve notes, which have no interest expense and are mostly collateralized by interest-earning Treasury and agency mortgage-backed securities, it is unlikely that the Federal Reserve Banks would be in an overall net loss position for very long.

Importantly, we conclude by stressing that there is no reason to believe that policy actions would be affected by their impact on the Federal Reserve's net income. In fact, the fair value of the Federal Reserve's portfolio as well as its earnings, gains, or losses do not affect the ability to carry out its responsibilities as the nation's central bank, which is to conduct monetary policy to achieve its statutory goals of maximum employment and stable prices.

Technical Appendix

GAAP accounting principles are established by accounting standard-setting bodies, such as the Financial Accounting Standards Board. However, accounting principles for entities with the unique powers and responsibilities of the nation's central bank have not been formulated by these bodies. In light of this, the Board of Governors has developed specialized accounting principles and practices that it considers appropriate for the central bank. These accounting principles and practices are documented in the Financial Accounting Manual for Federal Reserve Banks (FAM) which is issued by the Board of Governors (The Financial Accounting Manual for Federal Reserve Banks is available at https://www.federalreserve.gov/aboutthefed/financial-accounting-manual-for-federal-reserve-banks.htm). All 12 regional Reserve Banks are required to adopt and apply accounting policies and practices that are consistent with the FAM. The individual Reserve Bank financial statements are combined to create the Combined Federal Reserve Bank financial statements. The 12 Reserve Banks operate independently but under the supervision of the Board of Governors of the Federal Reserve System.

1. We thank Gurubala Kotta for excellent assistance. Return to text

2. Federal Reserve Banks Combined Quarterly Financial Reports (Unaudited) are available at https://www.federalreserve.gov/aboutthefed/combined-quarterly-financial-reports-unaudited.htm. Federal Reserve System Audited Annual Financial Statements are available at https://www.federalreserve.gov/aboutthefed/audited-annual-financial-statements.htm. Return to text

3. When the Federal Reserve purchases a security, the market price paid generally differs from the security's face value. If the security is purchased for more (less) than its face value, the difference between the purchase price and the face value--the premium (the discount) on that security--is recorded as a separate asset (contra-asset) on the H.4.1 release. Return to text

4. The amortized cost valuation is, in turn, adjusted for credit impairment, if any. In the Supplemental Financial Information of the Quarterly Financial Report, there are tables that disclose the par values of the securities. Return to text

5. Under the Financial Accounting Standards Board's Accounting Standards Codification (FASB ASC), securities holdings are classified into three categories: held-to-maturity securities, trading securities, and available-for-sale securities. Trading securities and available-for-sale securities are reported at fair value. Return to text

6. The Board of Governors requires the Reserve Banks to transfer excess earnings to the Treasury as interest on Federal Reserve notes after providing for the costs of operations, payment of dividends, and surplus funds that exceed the aggregate limitation of $6.825 billion. The $6.825 billion surplus limitation is required by the Federal Reserve Act, as amended by the Economic Growth, Regulatory Relief, and Consumer Protection Act, which was enacted on May 24, 2018. Return to text

7. These are presented in Table 2 of the Supplemental Financial Information section in Combined Quarterly Financial Report and in Section 5.d. of the Notes to Combined Financial Statements section in the annual Reserve Bank Combined Financial Statements. Return to text

8. SOMA also contains agency debt securities as well as foreign currency denominated securities held for the purpose of managing the Federal Reserve's foreign exchange reserves, although these components make up a much smaller fraction of the portfolio. Return to text

9. From time to time, some individual Reserve Banks have reported a deferred asset. For more information, see section 11.96 Accrued Remittances to Treasury / Deferred Asset in the January 2018 Financial Accounting Manual for Federal Reserve Banks: https://www.federalreserve.gov/aboutthefed/files/BSTfinaccountingmanual.pdf Return to text

Bonis, Brian, Lauren Fiesthumel and Jamie Noonan (2018). "SOMA's Unrealized Loss: What does it mean? ," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, August 13, 2018, https://doi.org/10.17016/2380-7172.2234.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.