May 05, 2008

Mortgage Delinquencies and Foreclosures

Chairman Ben S. Bernanke

At the Columbia Business School's 32nd Annual Dinner, New York, New York

President Bollinger, Dean Hubbard, Co-Chairman Kravis, and distinguished guests, I am very pleased to be here and especially honored to receive the Columbia Business School's Distinguished Leadership in Government Award. This evening I would like to offer a few thoughts on mortgage markets and the recent increase in the pace of delinquencies and foreclosures. My particular focus will be on geographic variation in mortgage performance and how that variation can help us better understand and prevent foreclosures. I will also discuss some initiatives taken by the Federal Reserve to address the foreclosure crisis as well as other policies that might be used to strengthen mortgage and housing markets.

Geographic Variation in Loan Mortgage Performance

As my listeners know, conditions in mortgage markets remain quite difficult, and mortgage delinquencies have climbed steeply. The sharpest increases have been among subprime mortgages, particularly those with adjustable interest rates: About one quarter of subprime adjustable-rate mortgages are currently 90 days or more delinquent or in foreclosure.1 Delinquency rates also have increased in the prime and near-prime segments of the mortgage market, although not nearly so much as in the subprime sector. As a consequence of rising delinquencies, foreclosure proceedings were initiated on some 1.5 million U.S. homes during 2007, up 53 percent from 2006, and the rate of foreclosure starts looks likely to be yet higher in 2008. Not all foreclosure starts result in the borrower's loss of the home; sometimes the borrower is able to make up the missed payments or other arrangements are made with the lender. But, given the number of borrowers in distress and the weakness of the general housing market, the share of foreclosure initiations that ultimately result in the loss of the home seems likely to be higher in the current episode than customarily has been the case.

Many foreclosures are not preventable. Investors, for example, are unlikely to want to hold onto a property whose value has depreciated significantly, and some borrowers--perhaps because they were put into an inappropriate loan or because personal circumstances have changed--cannot realistically sustain homeownership. However, if a foreclosure is preventable, and the borrower wants to stay in the home, the economic case for trying to avoid foreclosure is strong. Because foreclosures impose high costs, including legal and administrative costs as well as the costs of leaving the property vacant for a possibly extended period, both the borrower and the lender often are better off avoiding foreclosure. Moreover, it is important to recognize that the costs of foreclosure may extend well beyond those borne directly by the borrower and the lender. Clusters of foreclosures can destabilize communities, reduce the property values of nearby homes, and lower municipal tax revenues. At both the local and national levels, foreclosures add to the stock of homes for sale, increasing downward pressure on home prices in general. In the current environment, more-rapid declines in house prices may have an adverse impact on the broader economy and, through their effects on the valuation of mortgage-related assets, on the stability of the financial system. Thus, finding ways to avoid preventable foreclosures is a legitimate and important concern of public policy.

To determine the appropriate public- and private-sector responses to the rise in mortgage delinquencies and foreclosures, we need to better understand the sources of this phenomenon. In good times and bad, a mortgage default can be triggered by a life event, such as the loss of a job, serious illness or injury, or divorce. However, another factor is now playing an increasing role in many markets: declines in home values, which reduce homeowners' equity and may consequently affect their ability or incentive to make the financial sacrifices necessary to stay in their homes.

On the principle that a picture is worth a thousand words, Federal Reserve staff, using detailed, county-by-county information on mortgage performance, have developed a series of "heat maps," which summarize the incidence of serious mortgage delinquencies across the nation as well as some of the key drivers of loan performance. As the examples will make clear, the figures (with the exception of one map depicting house price changes) use warmer colors--orange and red--to show counties for which the factor being considered has a higher value or change. Lower values or changes (again, with the exception of that one map) are indicated by shades of green. Yellow indicates areas where the factor under consideration has a moderate value or change.

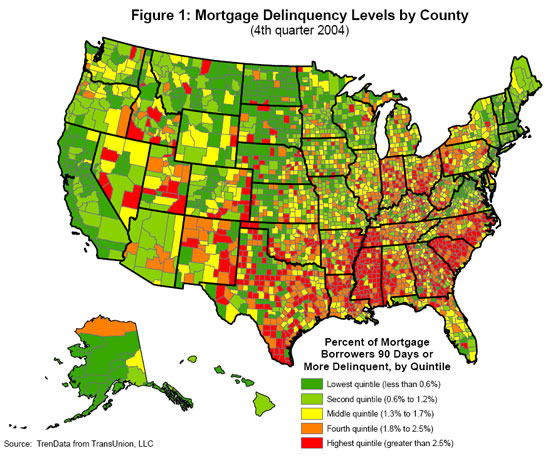

Nationally, as of the fourth quarter of 2007, the rate of serious delinquency, as measured by credit records, stood at 2 percent of all mortgage borrowers, up nearly 50 percent from the end of 2004.2 The fourth quarter of 2004 is a useful benchmark, because general economic conditions were fairly normal and the lax underwriting that emerged later was not yet evident.

Figure 1 shows the national patterns of serious mortgage delinquency in 2004, which, again, I am taking as representative of a relatively normal period, with orange and red indicating the highest rates of delinquency and greens indicating the lowest. In 2004, the areas of the country with the highest rates of serious delinquency included significant portions of the Southeast; parts of the Midwest, most notably Ohio and Indiana; portions of the Rocky Mountain region; and Texas, Oklahoma, and areas in the Mississippi valley. In contrast, many parts of the country experienced exceptionally good loan performance at that time, including most of the West Coast, New England, and much of southern Florida.

{kind=link}

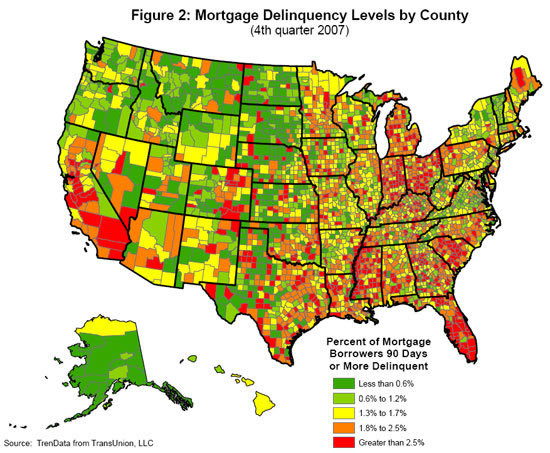

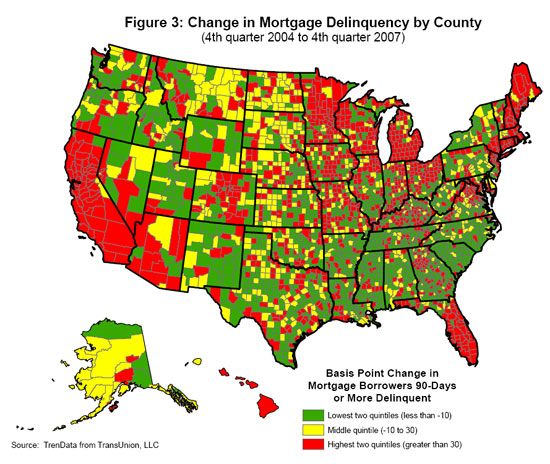

However, conditions in some areas changed greatly in a relatively short period of time. Figure 2 shows the pattern of delinquency rates as of the last quarter of 2007. Many of the areas that exhibited elevated delinquency rates in 2004 continued to show relatively high rates of delinquency in 2007. But some areas that had low rates in 2004 experienced high rates three years later. Figure 3 makes this point more sharply by showing the pattern of increases in delinquency rates between 2004 and 2007, with the largest increases shown in red. The strong regional pattern is evident in the figure. Although many parts of the country have seen significant increases in mortgage delinquencies and foreclosures, a number of areas--such as California, parts of Nevada, Arizona, Colorado, Florida, portions of the upper Midwest, and New England--have been particularly hard hit.

{kind=link}

{kind=link}

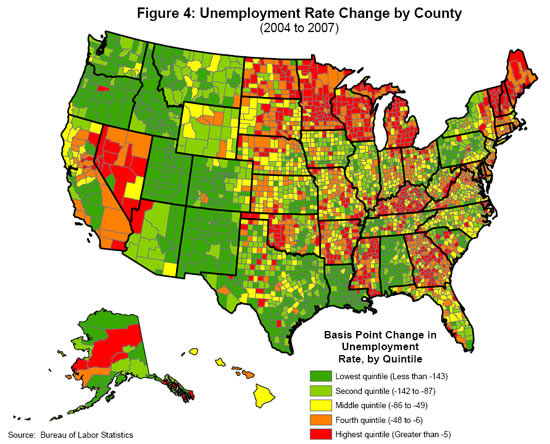

The regional pattern of the recent rise in mortgage delinquencies and foreclosures requires explanation. Again, we can use heat maps to examine the underlying relationships across geographic regions between changes in mortgage delinquency rates and factors identified as driving loan performance. For example, the change in the unemployment rate in a county can be used as a proxy for disruptions in family incomes and subsequent financial stress. Figure 4 shows changes in average annual unemployment rates across counties between 2004 and 2007, with counties indicated in red experiencing increases or only slight decreases in joblessness.3 The data suggest that increases in unemployment rates account for at least some of the recent increases in mortgage delinquencies. Parts of New England, states in the Great Lakes region--including Minnesota, Michigan, and Wisconsin--and a number of other states, such as Nevada, show both increased mortgage delinquencies and notable increases in unemployment rates.

{kind=link}

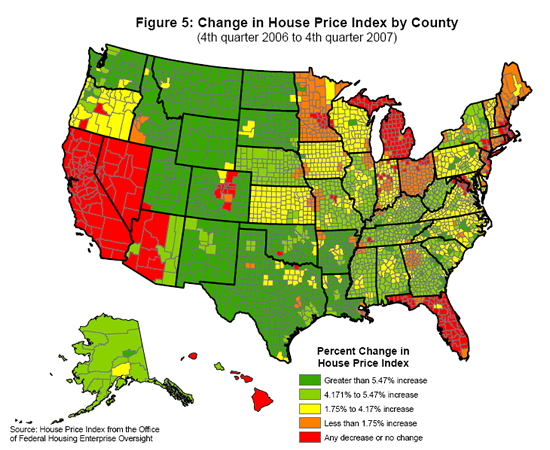

However, the behavior of unemployment does not seem sufficient to explain the increased delinquency rates in other areas, including California, Florida, and portions of Colorado, where mortgage delinquencies increased during a period in which unemployment generally decreased. Another important determinant of loan performance, identified by research at the Federal Reserve and elsewhere, is changes in house prices.4 Figure 5 shows the regional pattern of changes in house prices between 2006 and 2007, with unchanged prices and price declines indicated in red.5 The figure shows that Florida, California, Nevada, Michigan, and parts of Arizona and Colorado experienced decreases in house prices between the fourth quarter of 2006 and the fourth quarter of 2007 (a pattern which has continued and intensified in 2008).6 As I noted, sharp declines in house prices, and thus in homeowners' equity, reduce both the ability and incentive of homeowners, particularly those under financial stress for other reasons, to retain their homes.

{kind=link}

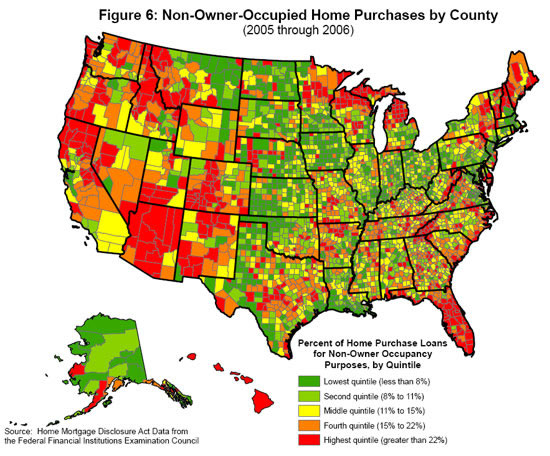

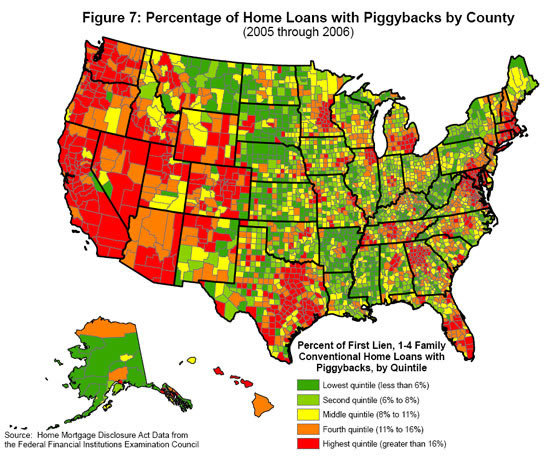

Other factors affect foreclosure rates, and once again the heat maps can give us a visual impression. Figure 6 shows the share of home purchases by non-owner occupiers--investors or purchasers of vacation homes, for example--during 2005 and 2006.7 Again, there is some correlation with the increase in delinquencies and foreclosures, as purchases by non-owner occupiers were relatively high in the West, Southwest, and in Florida. Figure 7 shows the incidence of junior liens (or piggyback loans), often an indicator of little borrower equity at the time of purchase. The greater use of these mortgages in the West and East Coasts presumably reflects higher house prices in those regions; again, the geographical pattern suggests that the use of piggyback loans may also have contributed to the recent rise in delinquencies and foreclosures.8

{kind=link}

{kind=link}

What are the implications of these relationships, particularly the linkage of mortgage payment problems and falling house prices? Loan servicers are used to dealing with mortgage delinquencies related to life events such as unemployment or illness, with the most common approaches being a temporary repayment plan or the folding of missed payments into the principal balance. A widespread decline in home prices, by contrast, is a relatively novel phenomenon, and lenders and servicers will have to develop new and flexible strategies to deal with this issue. In some cases, when the source of the problem is a decline of the value of the home well below the mortgage's principal balance, the best solution may be a write-down of principal or other permanent modification of the loan by the servicer, perhaps combined with a refinancing by the Federal Housing Administration or another lender. To be effective, such programs must be tightly targeted to borrowers at the highest risk of foreclosure, as measured, for example, by debt-to-income ratio or by the extent to which the mortgage is "underwater." Finding the right balance--particularly the need to avoid programs that give borrowers who can make their payments an incentive to default--is difficult. But realistic public- and private-sector policies must take into account the fact that traditional foreclosure avoidance strategies may not always work well in the current environment.

The Federal Reserve's Homeownership and Mortgage Initiatives

I would like to say a few words about the Federal Reserve's efforts to strengthen homeownership and reduce preventable foreclosures. The Federal Reserve's decisions regarding monetary policy and our efforts to increase financial stability affect housing and mortgage markets, of course. But, as an organization with a national presence in the form of regional Federal Reserve Banks and their Branches, we are also working to address these issues more directly. We are collaborating with other regulators, community groups, policy organizations, lenders, and public officials to identify ways to prevent unnecessary foreclosures and their negative effects on local economies.

Our efforts have taken a variety of forms. First, we have employed economic research and analysis, a particular strength of the Federal Reserve, to increase the sum of knowledge about mortgage and housing issues. For example, we are providing community leaders with detailed analyses identifying neighborhoods at high risk of foreclosures, analogous to the heat maps I showed you this evening.9 These analyses have helped community organizations better focus their scarce resources, such as deciding where to target counseling services or other intervention efforts. A Federal Reserve System work group has prepared overviews of the current state of knowledge about housing and mortgage markets, and further research is currently under way to fill in the most important analytical gaps.

Second, we are collaborating with interested parties across the country, taking advantage of our national presence and our existing relationships with local lenders, community groups, government officials, and other stakeholders, to take practical steps to address the causes and consequences of foreclosures. For example, I mentioned earlier the destabilizing effects foreclosures have on neighborhoods, resulting from factors such as decreased home values and deterioration of vacant properties from neglect. To help address this problem, the Federal Reserve is joining in a partnership with the nonprofit NeighborWorks America to develop materials, tools, and training programs to help communities and others acquire and manage vacant properties. The goal is to support the provision of affordable rental housing and new homeownership opportunities in low- and moderate-income neighborhoods. Federal Reserve Banks and Branches have also hosted numerous meetings and workshops to bring together local officials, lenders, community groups, and others to try to find ways to reduce the incidence of foreclosures and mitigate their economic and social effects.

Third, we are engaged with mortgage servicers to understand impediments they may face when modifying loans or offering other alternatives to foreclosure. Servicers still report difficulty connecting with troubled borrowers, and we have supported efforts to encourage borrowers to contact their lenders or housing counselors. Working with the Hope Now alliance and independently, we have encouraged the industry to increase their efforts to work with troubled borrowers, to develop guidelines and templates for reasonable standardized approaches to various loss-mitigation techniques, and to adopt uniform reporting standards, such as those sponsored by Hope Now. Clear disclosures of loan modifications will not only make it easier for regulators, the mortgage industry, and homeowners to assess the effectiveness of foreclosure-prevention efforts, but they will also foster greater transparency, and hence greater confidence, in the securitization market.

Prospectively, we are committed to promoting an environment that supports the homeownership goals of creditworthy borrowers. To this end, the Federal Reserve Board has proposed new regulations to better protect consumers from a range of unfair or deceptive mortgage lending and advertising practices. To help ensure that the rules are broadly enforced, we are engaging in a program with other federal and state agencies to conduct consumer compliance reviews of nondepository lenders and mortgage brokers. These reviews are targeting underwriting standards, risk-management strategies, and compliance with consumer protection laws and regulations.

The Federal Reserve also is continuing its long-standing practice of providing educational and information resources to help consumers make informed personal financial decisions, including choosing the right mortgage. Through their community affairs offices, Federal Reserve Banks are working to establish foreclosure-mitigation resource centers on their websites to be used by small municipalities, housing counselors, and community groups. For consumers who have questions about banking procedures and rules or who believe they may have been treated unfairly by their lender, the Federal Reserve Consumer Help Center directs queries to the various regulatory agencies so that a consumer has only one call to make to ask questions or file complaints.10

Additional Mortgage Initiatives

Additional government policies can help address problems in the mortgage markets. The Congress can take an important step by moving quickly to reconcile and enact legislation permitting the Federal Housing Administration (FHA) to increase its scale and improve its management of risks. Such legislation could help the FHA reach a wider range of borrowers and develop appropriate underwriting and pricing methodologies to deal with any increase in credit risk. Giving the FHA greater latitude to set underwriting standards and risk-based premiums for mortgage refinancing, as well as more flexibility in product development, would allow it to help still more troubled borrowers.

Separately, the government-sponsored enterprises (GSEs)--Fannie Mae and Freddie Mac‑‑could do more. Recently, the Congress expanded Fannie Mae's and Freddie Mac's role in the mortgage market by temporarily increasing the limits on the sizes of the mortgages they can accept for securitization. In addition, because the GSEs have resolved some of their accounting and operational problems, their federal regulator, the Office of Federal Housing Enterprise Oversight, has lifted some of the constraints that it had imposed on them. Thus, now is an especially appropriate time for the GSEs to move quickly to raise significant new capital, which they will need to take advantage of these new securitization and investment opportunities, to provide assistance to the housing markets in times of stress, and to do so in a safe and sound manner.

As the GSEs expand their role in housing markets, the Congress should move forward on GSE reform legislation, which includes strengthening the regulatory oversight of these companies. As the Federal Reserve has testified on many occasions, it is very important for the health and stability of our housing finance system that the Congress provide the GSE regulator with broad authority to set capital standards, establish a clear and credible receivership process, and define and monitor a transparent public purpose--one that transcends just shareholder interests--for the accumulation of assets held in their portfolios.

Conclusion

The realtor's mantra is "location, location, location," and, as I have discussed this evening, local variation in housing and mortgage markets is considerable. This variation is useful for understanding the sources of the increase in mortgage delinquencies and foreclosures, and it should be taken into account as servicers and policymakers consider how best to avoid preventable foreclosures.

Most Americans are paying their mortgages on time and are not at risk of foreclosure. But high rates of delinquency and foreclosure can have substantial spillover effects on the housing market, the financial markets, and the broader economy. Therefore, doing what we can to avoid preventable foreclosures is not just in the interest of lenders and borrowers. It's in everybody's interest.

References

Avery, Robert B., Kenneth P. Brevoort, and Glenn B. Canner (2007). "The 2006 HMDA Data (1.26 MB PDF)," Federal Reserve Bulletin, vol. 93 (December), pp. A73-A109.

Gerardi, Kristopher, Adam Hale Shapiro, and Paul S. Willen (2007). "Subprime Outcomes, Risky Mortgages, Homeownership Experiences, and Foreclosures," Working Paper No. 07-15. Boston: Federal Reserve Bank of Boston, December 3.

Footnotes

1. Based on servicer data from First American LoanPerformance. Return to text

2. This information from TrenData is drawn from the credit records of a geographically stratified random sample of more than 20 million individuals (roughly a 1 in 10 sample of all credit records) for each calendar quarter beginning in 1992. TrenData is a registered trademark of TransUnion LLC. "Serious delinquency" includes accounts that are 90 days or more past due or in foreclosure. Return to text

3. Unemployment rate data are from the Bureau of Labor Statistics. Return to text

4. For example, see Gerardi, Shapiro, and Willen (2007). Return to text

5. Displayed is the annual percentage change in the Office of Federal Housing Enterprise Oversight price index for each county from the end of 2006 to the end of 2007. Return to text

6. Several different series measure home price changes. The index compiled by the Office of Federal Housing Enterprise Oversight uses the values of homes whose mortgages were purchased by Fannie Mae or Freddie Mac. Return to text

7. Information on non-owner occupiers comes from Home Mortgage Disclosure Act (HMDA) data. HMDA is implemented by Regulation C (12 CFR 203) of the Federal Reserve Board. For more information about HMDA, see Avery, Brevoort, and Canner (2007). Return to text

8. For details about the technique used to identify piggyback loans and for more information about their use, see Avery, Brevoort, and Canner (2007). Return to text

9. See www.newyorkfed.org/mortgagemaps/ to view more maps related to mortgage lending. Return to text

10. Consumers can call 1-888-851-1920 or visit http://www.federalreserveconsumerhelp.gov/. Return to text