July 13, 2017

Cross-Border Spillovers of Balance Sheet Normalization

Governor Lael Brainard

At the National Bureau of Economic Research’s Monetary Economics Summer Institute, Cambridge, Massachusetts

When the central banks in many advanced economies embarked on unconventional monetary policy, it raised concerns that there might be differences in the cross-border transmission of unconventional relative to conventional monetary policy.1 These concerns were sufficient to warrant a special Group of Seven (G-7) statement in 2013 establishing ground rules to address possible exchange rate effects of the changing composition of monetary policy.2

Today the world confronts similar questions in reverse. In the United States, in my assessment, normalization of the federal funds rate is now well under way, and the Federal Reserve is advancing plans to allow the balance sheet to run off at a gradual and predictable pace. And for the first time in many years, the global economy is experiencing synchronous growth, and authorities in the euro area and the United Kingdom are beginning to discuss the time when the need for monetary accommodation will diminish.

Unlike in previous tightening cycles, many central banks currently have two tools for removing accommodation. They can therefore pursue alternative normalization strategies--first seeking to guide policy rates higher before initiating balance sheet runoff, as in the United States, or instead starting to shrink the balance sheet before initiating a tightening of short-term rates, or undertaking both in tandem. Shrinking the balance sheet and raising the policy rate can both contribute to achieving the domestic goals of monetary policy, but it is an open question whether alternative normalization approaches might have materially different implications for the composition of demand and for cross-border spillovers, including through exchange rates and other financial channels.

Before discussing the cross-border effects of normalization, it is worth noting that the two tools for removing accommodation--raising policy rates and reducing central bank balance sheets--appear to affect domestic output and inflation in a qualitatively similar way. This means that central banks can substitute between raising the policy rate and shrinking the balance sheet to remove accommodation, just as both were used to support the recovery following the Great Recession.

Insofar as a range of approaches is likely to be consistent with achieving a central bank's domestic objectives, the choice of normalization strategy may be influenced by other considerations, including the ease of implementing and communicating policy changes, or the desire to minimize possible credit market distortions associated with the balance sheet. In the case of the Federal Reserve, the Federal Open Market Committee (FOMC) decided to delay balance sheet normalization until the federal funds rate had reached a high enough level to enable it to be cut materially if economic conditions deteriorate, thus guarding against the risk of returning to the effective lower bound (ELB) in an environment with a historically low neutral interest rate.3 The greater familiarity and past experience with the federal funds rate also weighed in favor of this instrument initially. Separately, for those central banks that, unlike the Federal Reserve, moved to negative interest rates, there may be special considerations associated with raising policy rates back into positive territory.

One question that naturally arises is whether the major central banks' normalization plans may have material implications for cross-border spillovers--an important issue that until very recently had received scant attention. This question is a natural extension of the literature examining the cross-border spillovers of the unconventional policy actions taken by the major central banks to provide accommodation.

Although this literature suggests there are good reasons to expect broadly similar cross-border spillovers from tightening through policy rates as through balance sheet runoff, the effects may not be exactly equivalent. The balance sheet might affect certain aspects of the economy and financial markets differently than the short-term rate due to the fact that the balance sheet more directly affects term premiums on longer-term securities, while the short-term rate more directly affects money market rates. As a result, similar to the domestic effects, while the international spillovers of conventional and unconventional monetary policy may operate broadly similarly, the relative magnitude of the different channels may be sufficiently different that, on net, the two policy strategies have distinct effects. For example, as will be discussed at greater length shortly, the two strategies may have very different implications for the exchange rate. Moreover, as was evident with the European Central Bank's (ECB) asset purchases in late 2014 and early 2015, and as we have seen again in reverse in recent weeks, in addition to the standard demand and exchange rate channels, expected or actual asset purchases may have spillovers to foreign financial conditions--by lowering term premiums and the associated longer-term foreign bond yields--that are greater than conventional monetary policy.

To explore possible differences, it is useful to compare two different approaches to policy normalization, each of which is designed to have identical effects on aggregate domestic activity and thus, at least in the long run, on inflation. At one extreme, a central bank could opt to tighten primarily through conventional policy hikes, while maintaining the balance sheet by reinvesting the proceeds of maturing assets. At the other extreme, a central bank could rely primarily on reducing the balance sheet, while keeping policy rates unchanged in the near term.

The question is whether there are circumstances in which the choice of normalization strategies, which are similarly effective in achieving domestic mandates, might matter for the global economy. Where the two approaches have entirely equivalent effects, the central bank could freely substitute between them without changing the composition of home demand, and net exports, the exchange rate, and foreign output would also be unaffected.

Conversely, under different assumptions about the transmission channels of monetary policy, alternative approaches to normalization can have quite different implications for foreign economies. Most prominently, the exchange rate may be more sensitive to the path of short term rates than to balance sheet adjustments, as some research suggests.4 Although several papers using an event study approach find on balance little disparity in the exchange rate sensitivity to short-term compared to long-term interest rates, this lack of empirical consensus may simply reflect the difficulty of disentangling changes in short-term and longer-term interest rates, which are highly correlated.5

Indeed, the greater sensitivity of exchange rates to expected short-term interest rates than to term premiums was a key rationale behind the Operation Twist strategy in the early 1960s.6 Under Operation Twist, the Federal Reserve and the Treasury made large-scale purchases of longer-term Treasury securities to drive down yields and stimulate the economy, which was suffering from an unemployment rate of nearly 7 percent. This policy was combined with a modest increase in short-term interest rates intended to alleviate the capital outflow pressures that threatened the sustainability of the Bretton Woods global monetary system. Ultimately, this policy mix did succeed in reducing long-term interest rates, and also contributed to a reduction in private capital outflows that relieved pressure on U.S. international reserves, at least for a time.

Let's turn to a simulation of a highly stylized model to explore how a greater sensitivity of the exchange rate to conventional policy relative to balance sheet actions can make a difference in terms of cross-border transmission. In particular, let's assume a 100-basis-point rise in long-term yields coming from the conventional channel of higher policy rates has double the effect on the exchange rate as a 100 basis point rise in yields coming from higher term premiums.7 If a large country, which is already at potential, experiences a favorable domestic demand shock, it would need to tighten monetary policy to return output to potential. If the central bank chooses to use the short-term interest rate as its active policy tool, and keeps its balance sheet on hold, the current and expected path of short-term interest rates rises, putting upward pressure on long-term bond yields and causing the real exchange rate to appreciate. The stronger currency coupled with some initial expansion of domestic demand in turn cause a deterioration in real net exports.

Turning to the effects abroad, the decline in domestic real net exports corresponds to an increase in foreign net exports, which will tend to boost foreign GDP, other things being equal. How this affects a particular foreign economy will depend on its circumstances and the corresponding policy response of the foreign central bank. In the case where the foreign economy is pinned at the effective lower bound, the increase in net exports will provide a welcome boost to aggregate demand. By contrast, if foreign output is already near potential, the foreign central bank will need to respond by tightening policy in order to keep its economy in balance.

Now, let's instead consider tightening through the balance sheet. If the same amount of policy tightening in the country experiencing a positive demand shock is achieved exclusively through a reduction in the balance sheet, while keeping the policy rate unchanged, the exchange rate would appreciate to a smaller degree, reflecting the lower assumed sensitivity of the exchange rate to the term premium than to policy rates. Net exports would decline by less--reflecting both the smaller exchange rate appreciation and the smaller rise in domestic demand--and similarly this would result in smaller cross-border spillovers to foreign GDP.

Thus, for a foreign economy that is at the effective lower bound, tightening in the home country through balance-sheet policy will be less welcome than through short-term rates. The foreign economy will experience less exchange rate depreciation, and so less of a boost to net exports. In addition, the stimulus to the foreign economy could be further diluted to the extent that the balance sheet policy boosted term premiums on its long-term bonds and hence tightened financial conditions, although this effect has not been built into the simulation model. By contrast, for a foreign economy that is close to potential, adjustment through the balance sheet in the home country will mean less of a need for the foreign central bank to respond by tightening policy than under home country adjustment through conventional policy.

So far, we have considered the case of central banks with freely floating exchange rates and well-anchored inflation expectations. What about central banks with managed exchange rates or weakly anchored inflation expectations? To keep the analysis simple, let's assume a foreign central bank aims to completely stabilize its exchange rate vis-à-vis a core country. Let's again consider circumstances in which the core country experiences a positive demand shock that calls for policy tightening. Although the pegging economy is likely to experience spillovers under either approach to normalization in the core country, the spillovers are likely to be greater when the core country tightens through the policy rate. The tightening in the core country will compel the country that is fixing its exchange rate to tighten policy in sync and the core country's currency will rise more against its trading partners with conventional tightening, leading to greater effective appreciation of the pegging country's currency as well. Although the pegging economy will benefit somewhat from the stronger demand of the core country, that benefit is likely to be outweighed by the adverse effects of a tightening of domestic monetary policy when domestic conditions would not otherwise call for it. Such considerations may have played a role in the market dynamics experienced by China as discussions about initiating rate hikes progressed in the United States in the second half of 2015 and early 2016.8

Next let's explore alternative approaches to policy normalization by countries facing a similar need to tighten. This question is timely; with synchronous expansions now underway, we may be approaching a turning point before too long. In particular, let's consider the case when two large countries, which are assumed identical for the sake of simplicity, experience the same positive shock to domestic demand. Under these assumptions, if both economies were to choose the same normalization strategy--putting primary reliance on either the balance sheet or short-term interest rates--the implications for the exchange rate and net exports are the same: In both cases, the exchange rate between the two countries does not change, and neither do net exports between the countries. Each central bank would adjust interest rates by the same amount--enough to offset the stimulus from the demand shock--and with interest differentials unchanged, there would be no pressure on the exchange rate between them to move.9 Of course, if there are other economies in the rest of the world that do not experience the same shock, the choice of normalization strategy does matter, similar to the analysis of spillovers from the single core country, presumably magnified by the larger combined global weight of the two economies.

Now let's turn to the case in which the two central banks choose to rely on different policy tools.10 In this case, one country responds to the positive shock by hiking its policy rate to reduce output to its initial level, while the second country responds by shrinking its balance sheet. The country that relies on the policy rate to make the adjustment experiences an appreciation in the exchange rate, a deterioration in net exports and some expansion of domestic demand, while the country that chooses to rely solely on the balance sheet for tightening experiences a depreciation of its exchange rate and an increase in net exports. Thus, while both countries achieve their domestic stabilization objectives, whether the requisite policy tightening occurs through increases in policy rates or reductions in the balance sheet matters for the composition of demand, the external balance, and the exchange rate.

I highlighted at the outset the commitment adopted by many leading nations to set monetary policy to achieve domestic objectives such that the exchange rate would not be a primary consideration in the setting of monetary policy. In the case that balance-sheet and conventional monetary policies have equivalent effects on both domestic spending and the exchange rate, this common principle is straightforward. But if the cross-border spillovers of reductions in the balance sheet and increases in the policy rate are not equivalent, the sequencing of policy rate and balance sheet normalization could have important implications for the exchange rate and external balance.

Finally, in circumstances where a major central bank is continuing to expand its balance sheet or maintaining a large balance sheet over a sustained period, this policy would likely exert downward pressure on term premiums around the globe, especially in those foreign economies whose bonds were perceived as close substitutes. Indeed, until very recently, it had been notable how little long yields moved up in the United States even as discussions of balance sheet normalization have moved to the forefront. This likely reflects at least in part the expectation that ongoing asset purchase programs in other advanced economies would continue holding down long-term yields globally. The tide seems to have turned in recent weeks, as long yields in the U.S. have increased notably on market perceptions that foreign officials are beginning to deliberate their own normalization strategies.

I have used a simple stylized model to illustrate circumstances in which the choice of normalization strategies adopted by major central banks can potentially be quite consequential. If anything, the analysis presented here serves to highlight the importance of research assessing this question from both an empirical and theoretical perspective.

Let me conclude by returning to the policy choices facing central banks. The Federal Reserve chose to remove accommodation initially through increases in the federal funds rate. In light of recent policy moves, I consider normalization of the federal funds rate to be well under way. If the data continue to confirm a strong labor market and firming economic activity, I believe it would be appropriate relatively soon to commence the gradual and predictable process of allowing the balance sheet to run off.

Once that process begins, I will want to assess the inflation process closely before making a determination on further adjustments to the federal funds rate in light of the recent softness in core PCE (personal consumption expenditures) inflation. In my view, the neutral level of the federal funds rate is likely to remain close to zero in real terms over the medium term. If that is the case, we would not have much more additional work to do on moving to a neutral stance. I will want to monitor inflation developments carefully, and to move cautiously on further increases in the federal funds rate, so as to help guide inflation back up around our symmetric target.

Meanwhile, in recent days, we have begun to hear acknowledgement from other major central banks that they too are seeing conditions that suggest policy normalization could be on the table before too long, against the backdrop of a brighter global outlook. As I just discussed, the pace and timing of how central banks around the world proceed with normalization, and the importance of balance sheet policy relative to changes in short term rates in these normalization plans, could have important implications for exchange rates and financial conditions globally.

Appendix: Description of Stylized Model and Simulation Results

A. Model Description

The model is a stylized open economy model that includes two symmetric countries linked through trade flows. The model is specified in real terms under the implicit assumption that inflation is constant (so that real and nominal variables move by the same amount). Moreover, the model abstracts from any financial linkages between the two economies, including the possibility that monetary policy actions in one country could directly affect yields in the other (e.g., through portfolio balance channels), though such effects are clearly important empirically.

The two countries include a "Home" (H) county and a "Foreign" (F) country of equal size. Variables in the foreign country are denoted with an asterisk. In each country, the national accounting identity specifies that output, $$ y$$, is equal to the sum of absorption $$ d$$ and net exports $$ nx$$, that is:

$$$$ y=d+nx, \\ y^*=d^*-nx,$$$$

where the second equation incorporates the global resource constraint that $$ nx+{nx}^*=0$$. Here output ($$ y$$) and absorption ($$ d$$) are expressed in percent deviation from their respective steady states, while net exports are expressed as share of output, and are equal to zero in the steady state (that is, prior to any shocks).

Home and foreign absorption depend on long-term interest rates according to the following expressions:

$$$$ d=-\sigma(rc+ru)+u, \\ d^*=-\sigma\left({rc}^*+{ru}^*\right)+u^*,$$$$

Here $$ rc$$ is the component of long-term interest rates that is driven by conventional monetary policy, $$ ru$$ is the component of long-term interest rates that is driven by unconventional monetary policy, and $$ u$$ is an exogenous aggregate demand shock (with autocorrelation given by $$ \rho$$). These interest rate components are assumed to have identical effects on aggregate demand, with the parameter $$ \sigma$$ determining the sensitivity of aggregate demand to either component (n.b., interest rates are expressed in percentage points deviation from the steady state).

Net exports are assumed to fall if the real exchange rate ($$ e$$) rises/appreciates, and also if domestic demand is higher relative to foreign demand (since this boost imports). Thus:

$$$$ nx=-\eta{e}-\alpha\left(d-d^*\right)$$$$

where $$ \eta$$ is the elasticity of net exports with respect to the exchange rate, and $$ \alpha$$ is the elasticity of net exports to the differential between home and foreign absorption. The real exchange rate is expressed in percent deviation from the steady state.

The exchange rate is determined according to an interest rate parity condition which implies that the exchange rate appreciates when domestic interest rates are higher than foreign interest rates, with elasticities ( $$ \phi_c$$ and $$ \phi_u$$ ) that can differ depending on whether interest rate movements are driven by conventional or unconventional policy:

$$$$ e=\phi_{c}\left(rc-{rc}^*\right)+\phi_{u}\left(ru-{ru}^*\right).$$$$

The model is closed by specifying the behavior of the monetary authority. We assume that the monetary authority can adjust either the interest rate associated with conventional policy ($$ rc$$), or the interest rate linked to balance sheet actions ($$ ru$$), or both, to affect output (its goal variable). The conventional feedback rule is thus:

$$$$ rc=\gamma_{c}y, \\ {rc}^*=\gamma_{c}^{*}y^*,$$$$

whereas the unconventional feedback rule is:

$$$$ ru=\gamma_{u}y \\ {ru}^*=\gamma_{u}^{*}y^*.$$$$

The system above contains 10 equations in 10 endogenous variables ($$ y$$, $$ y^*$$, $$ d$$, $$ d^*$$, $$ nx$$, $$ e$$, $$ rc$$, $$ {rc}^*$$, $$ ru$$, $$ {ru}^*$$), as well two shocks, $$ u$$ and $$ u^*$$, that can move GDP, its components, exchange rates, and interest rates.

B. Simulation Results

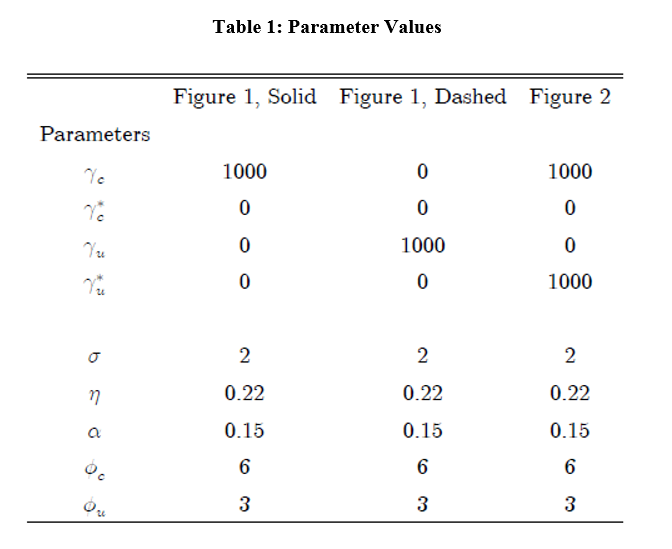

Figures 1 and 2 show the results of simulating the model under alternative assumptions about the shocks and monetary policy reaction. In each case, the economy starts in steady state with all variables at zero and experiences a demand shock in period 1 that dies out with an autocorrelation $$ \rho$$ of $$ 0.95$$. All parameter values are reported in Table 1.

{kind=link}

{kind=link}

{kind=link}

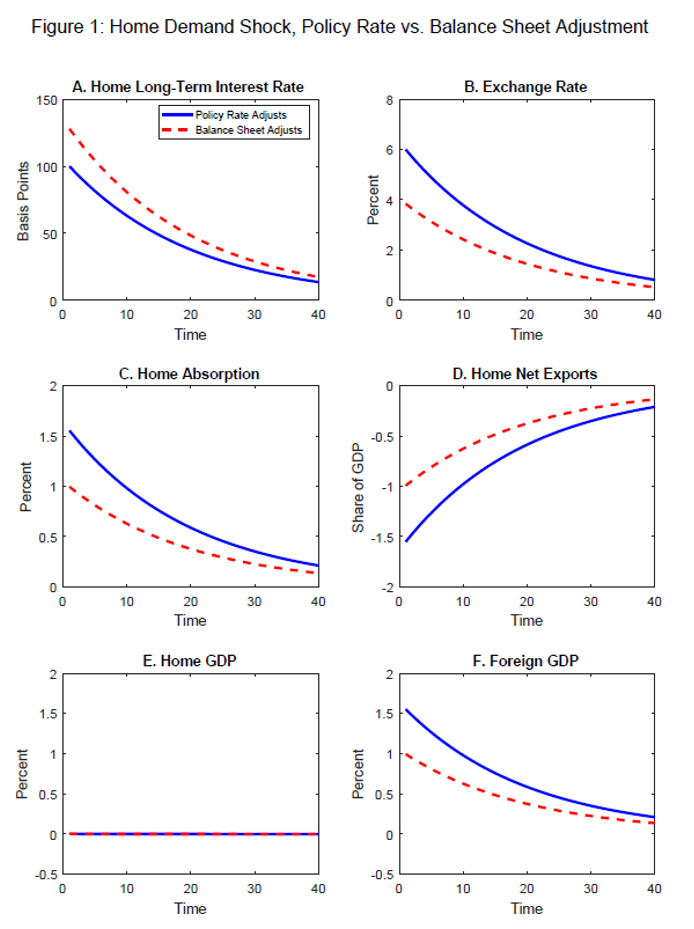

Figure 1. Home Demand Shock

Figure 1 illustrates the case of a favorable demand shock in the home country. The solid lines illustrate the case when Home uses the short-term interest rate as its active policy tool, and keeps its balance sheet on hold, consistent with a desire to delay balance sheet normalization.

The policy reaction is calibrated to be sufficiently aggressive that home GDP always remains at baseline (see column 2 of Table 1). The higher policy rate path (that is, higher $$ rc$$) causes the long-term interest rate (panel A) to rise, which in turn induces the real exchange rate to appreciate (panel B). The stronger currency and an expansion in domestic absorption (panel C) causes a deterioration in net exports (panel D). At the end of the period shown, domestic demand has nearly returned to baseline, while net exports are just a bit below baseline--consistent with Home country's GDP remaining at baseline (panel E). Because foreign monetary policy rates is assumed to remain on hold, foreign GDP (panel F) rises by the improvement in its net exports (that is, by the mirror image of panel D, given that foreign domestic absorption is unchanged).

The dashed lines illustrate the case of a favorable demand shock in the Home country when the central bank opts to tighten exclusively through reducing its balance sheet (again, by enough to keep output at potential--see column 3 of Table 1). Long-term interest rates (panel A) rise in response, but the exchange rate appreciates less in this case (panel B), reflecting the lower assumed sensitivity of the exchange rate to unconventional monetary policy actions ( $$ \phi_{u}\lt\phi_{c}$$ ). Net exports decline (panel D) by less--reflecting both the smaller exchange rate appreciation and a smaller rise in absorption (panel C)--which translates into less of a boost to foreign GDP (panel F) than when the home country adjusts through conventional policy.

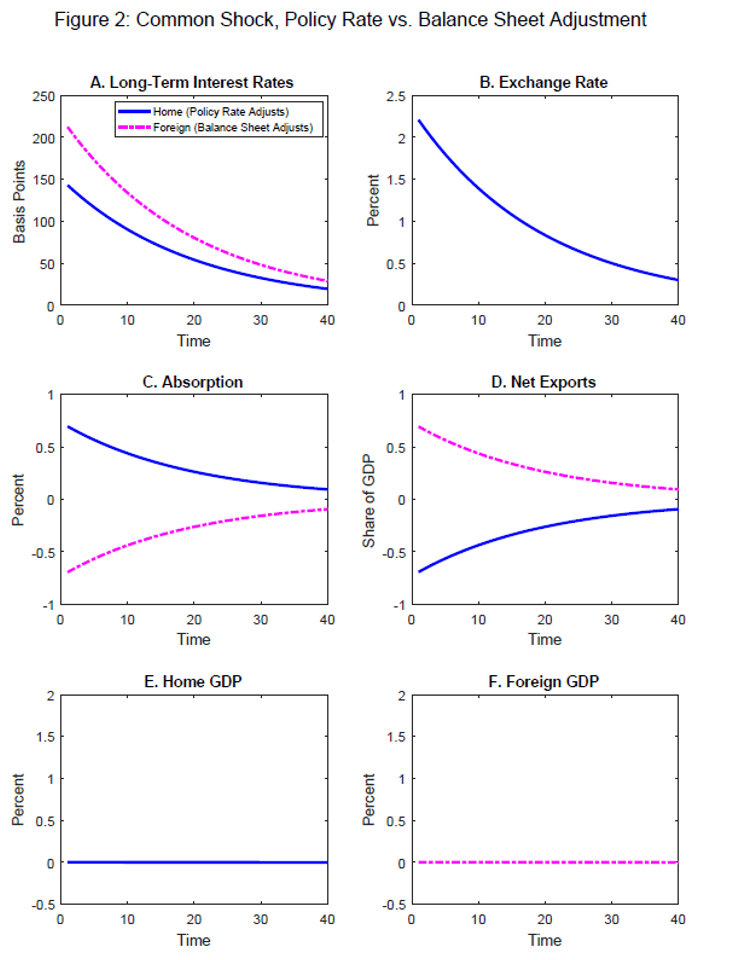

Figure 2. Common Demand Shock, Asymmetric Policy Tightening across Countries

Figure 2 shows a simulation in which the demand shock is assumed to be common across countries ( $$ u=u^*$$ ). The home country is assumed to pursue a policy of actively adjusting its policy rate, while the foreign Country is assumed to rely exclusively on normalizing through the balance sheet. In each case, the central banks of the two countries tighten policy aggressively enough to keep output at potential (see the parameter settings in column 4 of Table 1).

As policy rates rise in the home country (panel A) and the exchange rate is more sensitive to policy rates than to the balance sheet, the home country's exchange rate (panel B) appreciates, while its net exports (panel D) decline. Although GDP remains at baseline in each country (panels E and F) given our assumption that monetary policy keeps output at potential (which is unchanged), the alternative policy normalization choices clearly have important effects--even under a common shock--on both exchange rates and the composition of demand in each country. In particular, because exchange rates in the foreign country are less sensitive to balance sheet than to interest rate policy, the foreign central bank must enact a relatively larger interest rate tightening in order to keep its GDP at potential.

References

Alon, Titan, and Eric Swanson (2011). "Operation Twist and the Effect of Large-Scale Asset Purchases," FRBSF Economic Letter 2011-13. San Francisco: Federal Reserve Bank of San Francisco, April 25.

Bowman, David, Juan M. Londono, and Horacio Sapriza (2015), "U.S. Unconventional Monetary Policy and Transmission to Emerging Market Economies," Journal of International Money and Finance, vol. 55 (July), pp. 27-59.

Brainard, Lael (2015a). "Unconventional Monetary Policy and Cross-Border Spillovers," speech delivered at "Unconventional Monetary and Exchange Rate Policies," the 16th International Monetary Fund Jacques Polak Research Conference, sponsored by the International Monetary Fund, Washington, November 6.

Brainard, Lael (2015b), "Normalizing Monetary Policy When the Neutral Interest Rate is Low," speech delivered at the Stanford Institute for Economic Policy Research, Stanford, Calif., December 1.

Ferrari, Massimo, Jonathan Kearns, and Andreas Schrimpf (2016). "Monetary Shocks at High-Frequency and Their Changing FX Transmission around the Globe," August.

Glick, Reuven, and Sylvain Leduc, (2015). "Unconventional Monetary Policy and the Dollar: Conventional Signs, Unconventional Magnitudes (PDF)," Federal Reserve Bank of San Francisco Working Paper Series 2015-18, November.

Hofmann, Boris, Ilhyock Shim, and Hyun Song Shin (2016). "Risk-Taking Channel of Currency Appreciation (PDF)," BIS Working Paper No. 538. Basel, Switzerland: Bank for International Settlements, January (revised May 2017).

Modigliani, Franco, and Richard Sutch (1966). "Innovations in Interest Rate Policy," American Economic Review, vol. 56 (March), pp. 178-97.

Rey, Hélène (2014). "International Channels of Transmission of Monetary Policy and the Mundellian Trilemma (PDF)," paper presented at the 15th Jacques Polak Annual Research Conference, sponsored by the International Monetary Fund, Washington, November 13-14.

Ross, Myron H. (1966), "'Operation Twist': A Mistaken Policy?" Journal of Political Economy, vol. 74 (April), pp. 195-99.

Stavrakeva, Vania, and Jenny Tang (2016). "Exchange Rates and the Yield Curve," Research Department Working Papers 16-21. Boston: Federal Reserve Bank of Boston, April.

Stein, Jerome L. (1965). "International Short-Term Capital Movements," American Economic Review, vol. 55 (March), pp. 40-66.

Swanson, Eric T. (2017). "Measuring the Effects of Federal Reserve Forward Guidance and Asset Purchases on Financial Markets," NBER Working Paper 23311. Washington: National Bureau of Economic Research, April (revised June).

1. I am grateful to John Ammer, Bastian von Beschwitz, Christopher Erceg, Matteo Iacoviello, and John Roberts for their assistance in preparing this text. The remarks represent my own views, which do not necessarily represent those of the Federal Reserve Board or the Federal Open Market Committee. Return to text

2. The new commitment stated: "We reaffirm that our fiscal and monetary policies have been and will remain oriented towards meeting our respective domestic objectives using domestic instruments, and that we will not target exchange rates." See Group of Seven (2013), "Statement by G7 Finance Ministers and Central Bank Governors," February 12, paragraph 1. The corresponding Group of Twenty statement included the new commitment: "We will not target our exchange rates for competitive purposes." See Group of Twenty (2013), "Communiqué of Meeting of G20 Finance Ministers and Central Bank Governors," February 16, paragraph 5. Return to text

3. See, for example, Board of Governors of the Federal Reserve System (2015), "Federal Reserve Issues FOMC Statement," press release, December 16; and Brainard (2015b). Return to text

4. See, for instance, Stavrakeva and Tang (2016). Return to text

5. See Glick and Leduc (2015), Ferrari, Kearns, and Schrimpf (2016), and Swanson (2017); Swanson attempts to identify separately the effects of forward guidance and asset purchases. Return to text

6. See Ross (1966), Modigliani and Sutch (1966), Stein (1965), and Alon and Swanson (2011). Return to text

7. This simulation is shown in figure 1 in the appendix. The stylized model is composed of two identical countries that are linked through trade flows. The model is calibrated so that either type of policy action keeps the home country's GDP at baseline. Return to text

8. See Brainard (2015a). A number of recent studies have considered financial spillovers to EMEs, including Rey (2014) and Bowman, Londono, and Sapriza (2015). The analysis of Hofmann, Shim, and Shin (2016) suggests that EMEs may be hurt more if their banks or nonfinancial corporations have relatively large dollar liabilities, as the larger dollar appreciation associated with the policy rate tool would precipitate greater EME balance sheet deterioration in this case. Return to text

9. In this simple example, in which the two countries are hit by identical shocks, the offset in spillovers between the two economies will be complete. If one country faces a larger aggregate demand shock than the other, then the situation becomes more like the one-country case we examined before, the policy adjustments lead to spillovers of different magnitudes, and the offset will be partial. Return to text

10. This simulation is shown in figure 2 in the appendix. Return to text