November 19, 2021

Perspectives on Global Monetary Policy Coordination, Cooperation, and Correlation

Vice Chair Richard H. Clarida

At the "Macroeconomic Policy and Global Economic Recovery" 2021 Asia Economic Policy Conference, sponsored by the Federal Reserve Bank of San Francisco Center for Pacific Basin Studies, San Francisco, California (via webcast)

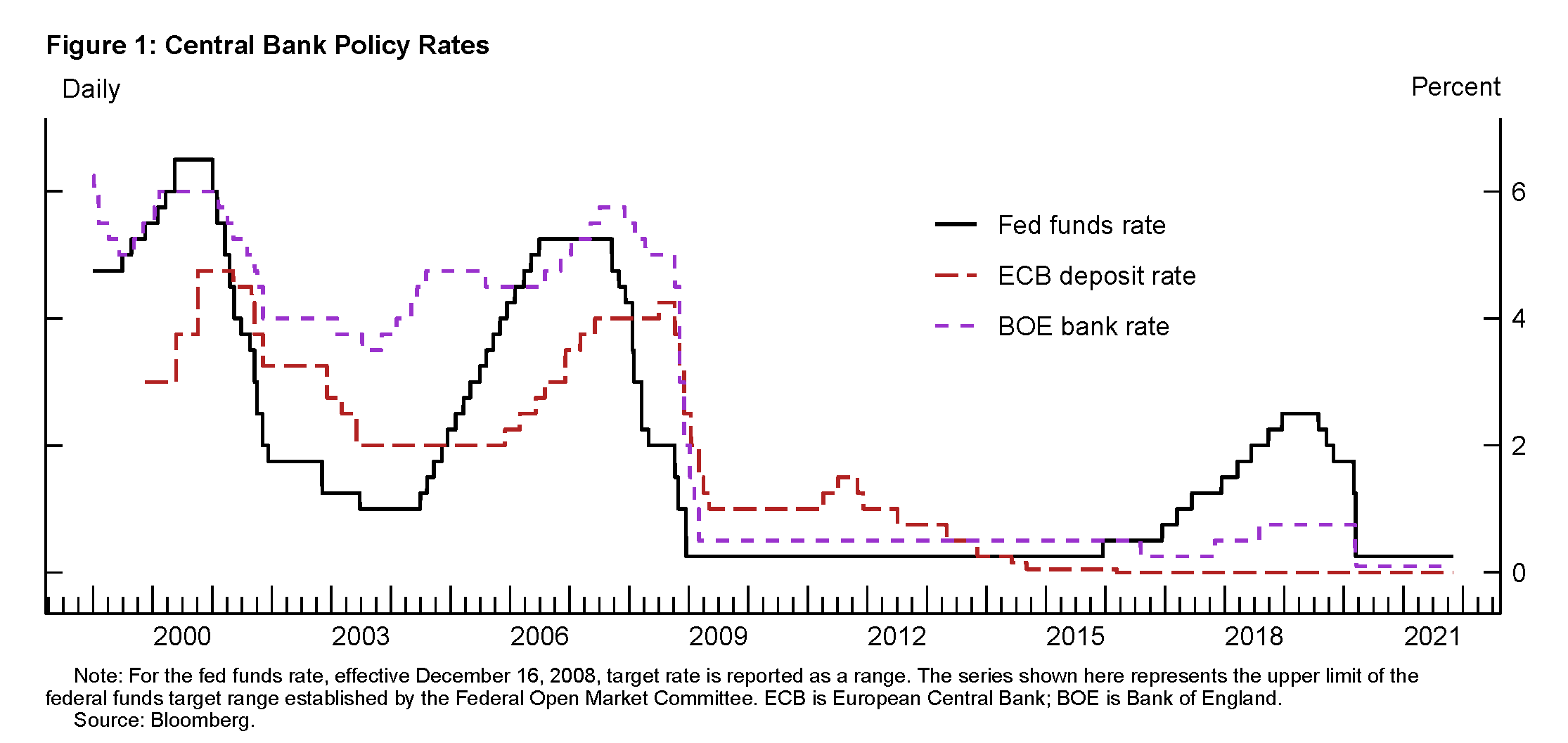

In my remarks today, I would like to offer some perspectives on global monetary policy correlation and what it can—and cannot—reveal about the prevalence and value of global monetary policy coordination or, in the limit, binding global monetary cooperation.1 In both the Global Financial Crisis (GFC) and the Global Pandemic Collapse (GPC), major central banks around the world responded by cutting policy rates to, and then keeping them at, their effective lower bounds (ELBs); by increasing their balance sheets through ambitious and expansive large-scale asset purchase and lending programs; and by offering forward guidance—both Delphic and Odyssean—on the stance of their future monetary policies.2

As these examples make clear, we certainly do observe that national monetary policies are often correlated, and such examples are not confined to recent experience. Indeed, the international monetary economics literature abounds with historical and empirical studies of correlated global monetary policy cycles, not to mention the evident secular downtrend in global monetary policy rates observed in recent decades. Moreover, global monetary policies often also do appear at least sometimes to be coordinated. There are certainly enough meetings of Group of Seven (G-7), Group of Twenty, and Bank for International Settlements (BIS) central bank governors—virtual and in person—that provide such opportunities. By contrast with evidence of central bank correlation and coordination, the historical record suggests that, since the collapse of the Bretton Woods system 50 years ago, rarely, if ever, do major sovereign central banks actually enter into, at least publicly—let alone respect—binding commitments to pursue formal cooperative policies.3 Here and throughout the lecture, I shall reserve the meaning of the adjective cooperative, as in "cooperative" central bank policies, to define policies that can, at least conceptually, be thought of as policies pursued by sovereign central banks that fully incorporate any spillovers from one central bank's policies to the other central bank's mandates. Cooperative policies defined this way will, in general, differ from noncooperative policies—in the sense of the Nash equilibrium concept—designed to achieve domestic mandates assigned by sovereign institutions while taking other central bank policies as given. In these remarks, I will draw on perspectives informed not only by economic analysis—including my own academic research on the theory and empirics of central banks' policymaking—but also by my observations and experiences serving as Vice Chair of the Federal Reserve Board during what has certainly been an eventful three years.

To begin with the theory, it has long been appreciated that in the sorts of economic models used by central banks around the world, the calibrated gains to international monetary policy cooperation are found to be rather modest relative to a status quo ante in which each country runs a sensible policy, taking as given the sensible policies of the other countries. Today I will make a somewhat different, and less often discussed, case questioning formal global monetary policy cooperation—that, in practice, adopting it could plausibly erode central bank credibility and public support for central bank instrument independence.

International monetary policy coordination, which I think of as including the sharing of information and analysis among central banks regarding the evolution of their individual economies as well as the considerations that govern the setting of their policy instruments—in other words, information about their policy reaction functions can, and in my observation certainly does, enhance the design and effectiveness of monetary policy execution for each country. I shall give some examples later.

But while international monetary policy coordination may enhance the efficiency of monetary policy execution, I am skeptical that in practice there are additional material, reliable, and robust gains that would flow from a formal regime of binding monetary policy cooperation, at least among major G-7 economies with flexible exchange rates, open capital accounts, and central bank mandates that include price stability. Or, more precisely, it seems that whatever gains might exist in theory, they likely do not exceed the full cost of committing to such an arrangement in practice. In such a regime, national monetary policies in each country would be constrained to be set in such a way so as to jointly maximize some metric for global price stability and perhaps also other objectives. The reason is that there can be global externalities to monetary policy that create such theoretical gains to cooperation. However, as Clarida, Galí, and Gertler (2002), among others, have shown in the context of central banks with domestic price-stability mandates, to achieve the theoretical gains to international monetary policy cooperation, policy in each country must be set with reference to an index of inflation in all countries party to the cooperative agreement.

This is a policy that no central bank would choose were it not bound to the agreement to achieve domestic price stability while taking other central banks' policies as given, which, of course, raises the question of how such an agreement might be enforced. In theory, if central banks were bound to set policy based solely on a policy rule that is a function of observed macroeconomic data, enforcement would be simple. But in practice, no sovereign central bank outsources its policy to an Excel spreadsheet, and, moreover, best-practice policy rules incorporate inputs—such as the neutral rate of interest or expected inflation—that are unobserved and time varying and thus difficult to monitor. Finally, central bank mandates vary across sovereign jurisdictions. For example, the Federal Reserve is mandated to pursue policies that achieve "maximum employment and price stability." The European Central Bank (ECB) is mandated by treaty to pursue price stability but also has a secondary mandate to contribute to achieving the objectives of the European Union, which include balanced economic growth and full employment. Similarly, the Bank of England's primary objective is to achieve the U.K. government's target of 2 percent inflation, but its secondary objective is to support the government's policy aims, including those for employment, growth, and—more recently—environmental sustainability. So even though all major central banks are mandated to achieve "price stability" in some form or fashion, their mandates typically include other obligations that vary across jurisdictions. Because these obligations can, and sometimes do, require central banks to make a tradeoff—for example, in the United States, between inflation and employment in the presence of supply shocks—defining the objective that a cooperative agreement would choose to maximize would be a formidable task.

I believe that, in practice, beyond the issue of enforcement and agreement on terms, there could well be another challenge with policy cooperation that is absent from most theoretical discussions. Simply stated and in the context of a price-stability mandate for each central bank, the problem—as I see it—is the threat to the credibility of the central bank, the challenges to central bank communication, and the resulting potential loss of support for its policy actions from the public when the policy choices that would be required by binding monetary policy cooperation react not only to home inflation deviations from target, but also to deviations of foreign inflation from target. In theoretical models, the commitment to the inflation target is just assumed to be perfect and credible, but in practice, credibility appears to be a function of central bank communication and of the policies actually implemented pushing inflation toward—and, in the absence of shocks, keeping inflation at—target. I suspect that, in practice, central banks would have a hard time maintaining credibility and independence as well as communicating a policy that raised home interest rates aggressively not because home inflation is too high but because foreign inflation is!

While, perhaps for these reasons, we do not have many confirmed sightings of genuine binding monetary policy cooperation, we do observe many examples of monetary policy correlation (see figure 1). Monetary policies will obviously be correlated if countries are subject to common shocks—such as in the GFC and the GPC—but can also be correlated as a consequence of integrated global capital markets. The Clarida, Galí, and Gertler (2002) model provides a simple illustration of how this correlation can come about. In the "home" country, the optimal inflation-targeting monetary policy can be written as a Taylor-type rule:

{kind=link}

$$ R_{t} = r_{t} + (1 + \frac{\lambda}{\alpha})\pi_{t}, $$

where $$r_t$$ is the "neutral" interest rate in the home country consistent with price stability and trend growth and $$\pi_t$$ is inflation in the home country. The ratio $$\lambda/\alpha$$ captures the extent to which the home central bank trades off its inflation and gross domestic product (GDP) objectives when they are in conflict. The parameter $$\alpha$$ indexes the priority the central bank places on stabilizing GDP growth relative to its trend path. When $$\alpha$$ is large, the central bank leans against high inflation less aggressively than it would were $$\alpha$$ small. With an integrated global capital market, the neutral policy rate at home is a function of trend GDP growth at home as well as expected foreign GDP growth:

$$ r_{t} = 2E_{t}\{\Delta \bar{y}_{t+1}\} + E_{t}\{\Delta y^{*}_{t+1}\}. $$

Now, to the extent the foreign central bank has a comparative advantage in tracking or forecasting foreign output growth—which, of course, it should, since such growth will depend on the foreign central bank's monetary policy—sharing this information with the home central bank can improve that institution's estimate of the home equilibrium real interest rate and thus the effectiveness of its policy rule in meeting its domestic objectives.

The foreign central bank sets its policy rate in an analogous fashion:

$$ R^{*}_{t} = r^{*}_{t} + (1 + \frac{\lambda}{\alpha^{*}})\pi^{*}_{t}. $$

The ratio $$\lambda/\alpha^{*}$$ captures the extent to which the foreign central bank trades off its inflation and GDP objectives when they are in conflict, and note that this tradeoff may be different than that of the home central bank. With an integrated global capital market, the neutral policy rate abroad is given by

$$ r^{*}_{t} = 2E_{t}\{\Delta \bar{y}^{*}_{t+1}\} + E_{t}\{\Delta y_{t+1}\}. $$

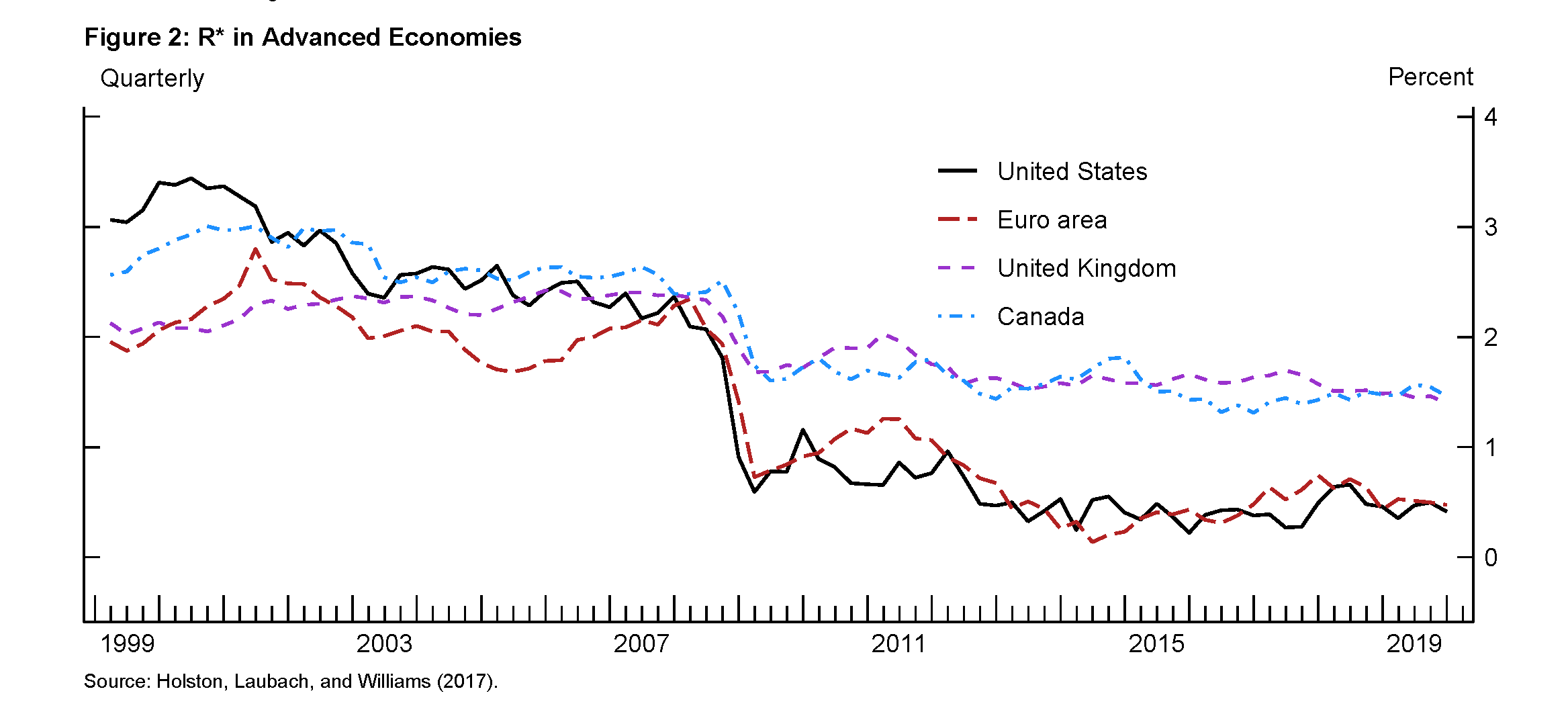

This simple example illustrates one channel through which globally integrated capital markets can introduce policy correlation even in the absence of policy coordination or cooperation. For example, even if home and foreign inflation rates and trend growth rates are uncorrelated across countries, sensible monetary policies can be correlated across countries if neutral policy rates are correlated, as they appear to be in the data (see figure 2, which is based on Holston, Laubach, and Williams, 2017).

{kind=link}

A recent working paper, Ferreira and Shousha (2021), models the determinants of the neutral policy rate in the United States and includes in the empirical specification an index of global productivity growth and demographic trends. Their empirical estimates attribute 85 basis points of the decline in U.S. neutral real interest rates since 2000 to global spillovers from the slowdown in global trend growth and demographic trends. So policy correlation can be an outcome of noncooperative monetary policy operating in an integrated global capital market and not evidence, in and of itself, of policy coordination, let alone cooperation. Before continuing, I consider briefly how monetary policy would differ under binding cooperation in the simple example sketched out earlier. Under international monetary policy cooperation, the policy rate is set according to

$$ R_{t} = r_{t} + (1 + \frac{\lambda}{\alpha})\pi_{t} + \frac{1}{3}(1+\frac{\lambda}{\alpha})\pi^{*}_{t}. $$

So, intuitively, while policy in the home country does place more weight on home inflation when setting the interest rate, it also reacts to foreign inflation as well, as I discussed earlier.

Consider the case with home inflation high and foreign inflation low. As can be seen from the preceding equation, the optimal policy under cooperation calls for the home interest rate to be lower—more accommodative—than it would be in the absence of cooperation. In practice, the home central bank's credibility as an inflation targeter to satisfy its domestic price-stability mandate might well suffer if it failed to respond aggressively to high domestic inflation because of, say, serious deflation abroad.

Monetary Policy Spillovers Flow in Both Directions

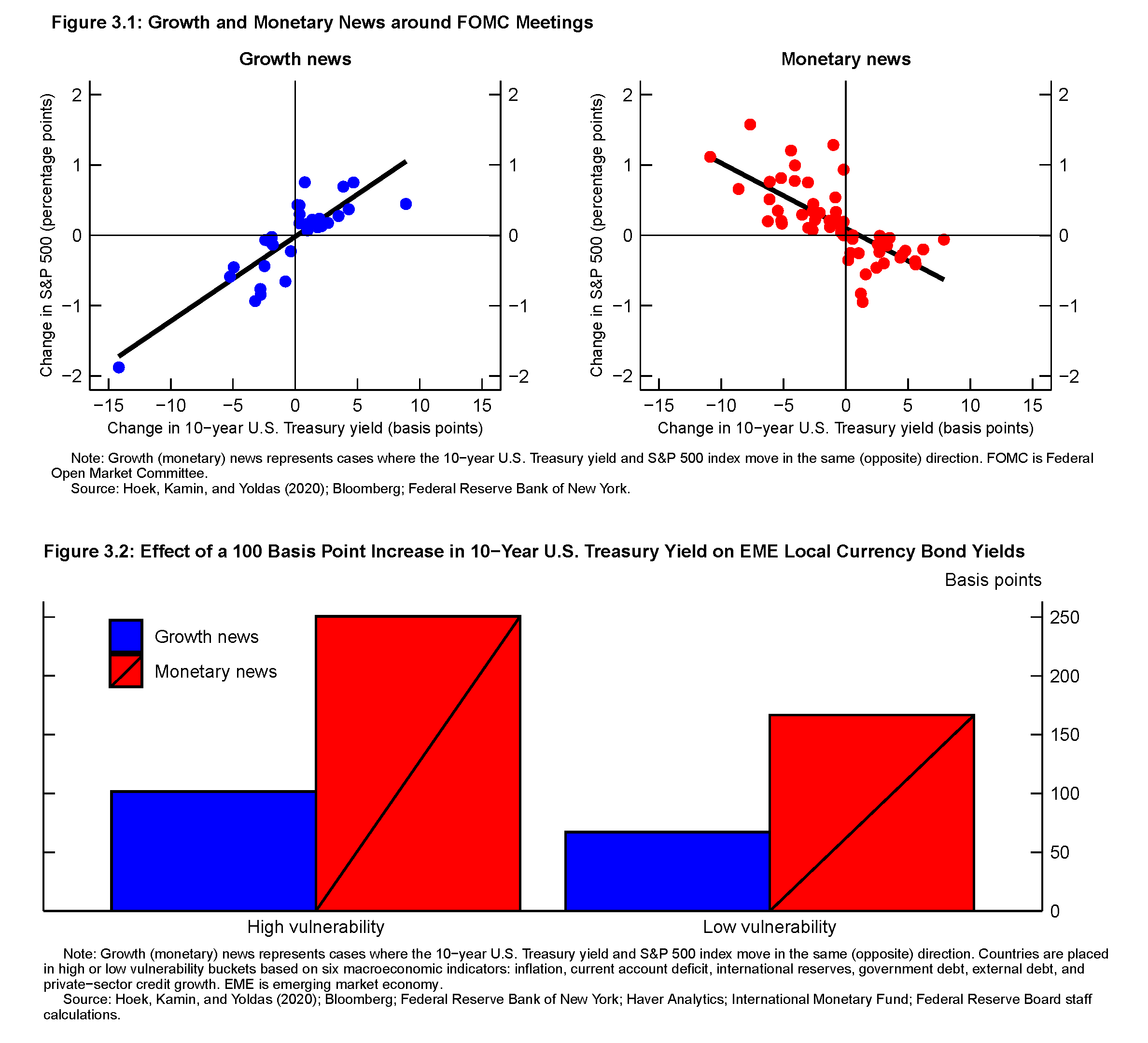

There is a vast literature that documents the existence of international spillovers from U.S. monetary policy, especially to emerging markets (EMs). Recent research—Hoek, Kamin, and Yoldas (2020)—suggests that the extent and consequences of such spillovers depend importantly on the source of a shift in U.S. monetary policy. Their key finding, illustrated in figure 3, is that Federal Reserve policy rate surprises attributed to stronger U.S. growth generally have only moderate spillovers to EM financial conditions, whereas U.S. policy rate changes attributed to U.S. inflationary pressures trigger more substantial spillovers to EM financial conditions. The authors also find compelling evidence that the magnitude of the cross-border spillovers attributed to U.S. monetary policy shifts depends on a country's macroeconomic vulnerability—as measured by inflation, current account deficit, international reserves, government debt, external debt, and private-sector credit growth, with more vulnerable EM countries experiencing larger spillovers from U.S. monetary policy.

{kind=link}

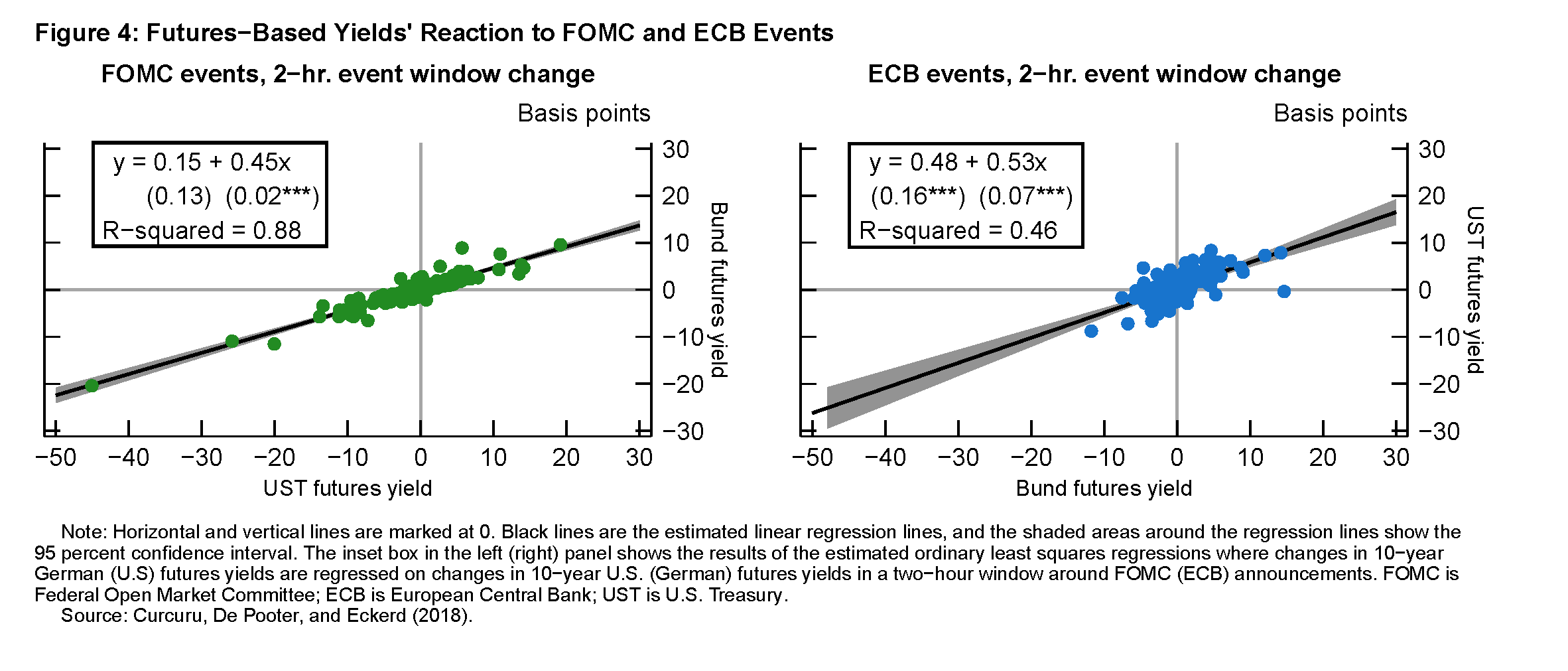

A recent paper—Curcuru, De Pooter, and Eckerd (2018)—examines and compares the consequences of ECB policy actions for U.S. financial conditions and the consequences of Federal Reserve policy actions for euro-area financial conditions. Their main findings are summarized in the two panels in figure 4. The left panel presents evidence of statistically significant spillovers from Federal Open Market Committee (FOMC) policy announcements to euro-area bond markets. But, as shown in the right panel, the authors find that the spillovers from ECB policy announcements to U.S. yields are roughly as large as those from FOMC announcements to bund yields.

{kind=link}

While I will certainly acknowledge that both fundamental and financial shocks originating in the United States, including shifts in the direction of U.S. monetary policy, can and do propagate globally (see, for example, Miranda-Agrippino and Rey, forthcoming), the evidence suggests that causality can and does run in both directions. It is not difficult to recall external events that have triggered spillovers from foreign sovereign markets to the U.S. economy that have had observable implications for U.S. monetary policy.

The Mexican peso crisis of 1994–95 and the Asian financial crisis of 1997–98 resulted in substantial declines in economic activity in emerging markets but had only a modest effect on the U.S. economy. One reason for this outcome was "safe haven" flows into the dollar assets that pushed down U.S. bond yields. But the Russian default of August 1998, followed by the collapse of Long-Term Capital Management, had more substantial effects on global markets and posed greater risk to the U.S. economy, and these events triggered a policy response by the Federal Reserve that cut the federal funds rate 75 basis points between September and November of that year. When in the next year the global financial system stabilized, the Federal Reserve reversed those actions and returned the federal funds rate to the level prevailing before those events.

In more recent times, global shocks have also been consequential for U.S. economic prospects and monetary policy. Examples include the 2011–13 euro-zone crisis and the China devaluation and capital flight episode of 2015–16, when worries about a hard landing and renminbi depreciation, respectively, roiled world markets. Both of these shocks originated in economies with large footprints in the global economy and financial system, and, as a result, they induced substantial disruptions in global financial markets. During both episodes, U.S. stock markets fell and the dollar appreciated, especially during 2015 and 2016. As ever, these adverse global shocks triggered safe-haven flows that pushed U.S. Treasury yields down. But despite the drop in Treasury yields, overall financial conditions in the United States tightened, weighing on aggregate demand.

U.S. monetary policy responded to these global "headwinds," helping stave off actual contractions of U.S. activity. During the 2011–13 euro-zone crisis, the Federal Reserve was already pursuing very accommodative policies in the wake of the GFC, but the introduction of the maturity extension program in September 2011 and the announcement in September 2012 of the third installment of quantitative easing were in part aimed at offsetting the effect of these global headwinds on U.S. aggregate demand. Regarding the aforementioned China devaluation episode of 2015–16, Federal Reserve statements and transcripts from that time indicate that concerns about these developments and their effect on the U.S. economy were a factor that contributed to the delay in implementing previously signaled policy rate increases.4 Again, as in the 1997–98 episode discussed earlier, once the "storm had passed," the previously signaled policy normalization process commenced in 2017.

The Federal Reserve and ECB Framework Reviews

The monetary policy framework reviews conducted by the Federal Reserve and the ECB provide another example of monetary policy correlation. In February 2019, the Federal Reserve System launched a review of its monetary policy strategy, tools, and communication practices. A key motivation for the Fed's review as well as the ECB's review was the substantial decline in estimates of the neutral real interest rate, r*, that, over the longer run, is consistent with price stability. This decline has critical implications for monetary policy because it leaves central banks with less conventional policy space to offset adverse shocks to aggregate demand.5

As discussed in Clarida (2020), the Fed's review, from the outset, built on three pillars: a series of Fed Listens events, a flagship research conference, and a series of rigorous briefings for the Committee commencing in July 2019 and running through January 2020.6 While our plans to conclude the review earlier in 2020 were, like so many things, delayed by the arrival of the pandemic, in August 2020, the Federal Reserve did announce, with unanimous support, an evolution of its monetary policy strategy to flexible average inflation targeting.7

Similar to the Federal Reserve, the ECB launched a review of its monetary policy strategy in January 2020.8 Since the time of its previous strategy review in 2003, like the Fed, the ECB observed profound structural changes in the global and euro-area economies that have driven down neutral interest rates and increased the incidence and duration of episodes in which nominal policy interest rates are close to the ELB. So the ECB's review sought to adapt its monetary policy to the current economic environment and to ensure that its policy could remain effective at the ELB. In its review, the ECB heard from a wide variety of European organizations and citizens, including through a series of ECB Listens events.9 The ECB's Governing Council engaged in a series of deliberations, also informed by extensive staff background analysis on a range of topics. In July 2021, with unanimous support from its Governing Council, the ECB announced its new strategy.10 Key elements of that strategy are a symmetric 2 percent inflation target, a view that the ELB requires especially forceful or persistent monetary policy measures to keep inflation expectations from drifting lower, and the affirmation that the full range of measures it has used in recent years will remain in its toolkit.

The similarities in the two framework evolutions are due to the fact that powerful common global forces are driving down neutral policy rates and limiting the effectiveness of monetary policy in downturns to offset declines in aggregate demand. This asymmetry of policy effectiveness caused by the ELB imparts a secular downward bias to inflation that, if not offset, could de-anchor inflation expectations below the central bank's price-stability objectives. In addition, the similarities in the processes according to which these two framework reviews were conducted reflected also a convergence in thinking about best practices for such reviews that was facilitated by a working group on central bank frameworks set up by the BIS.

Conclusion

In this speech, I have offered some perspectives on global monetary policy correlation and what it can—and cannot—reveal about the prevalence and value of global monetary policy coordination or, in the limit, binding global monetary cooperation. I have argued that, while there are several recent and historical examples where we certainly do observe that national monetary policies are often correlated, adopting formal global monetary policy cooperation could plausibly erode central bank credibility and public support for central bank independence. But I also observe that international monetary policy coordination, defined as including the sharing of information and analysis among central banks regarding the evolution of their individual economies and information about their policy reaction functions, can enhance the design and effectiveness of monetary policy execution for each country.

Thank you very much for your time and attention. I look forward to my conversation with Sylvain.

References

Campbell, Jeffrey R., Charles L. Evans, Jonas D.M. Fisher, and Alejandro Justiniano (2012). "Macroeconomic Effects of Federal Reserve Forward Guidance (PDF)," Brookings Papers on Economic Activity, Spring, pp. 1–54.*

Clarida, Richard H. (2020). "The Federal Reserve's New Monetary Policy Framework: A Robust Evolution," speech delivered at the Peterson Institute for International Economics, Washington (via webcast), August 31.

——— (2021). "The Federal Reserve's New Framework and Outcome-Based Forward Guidance," speech delivered at "SOMC: The Federal Reserve's New Policy Framework," a forum sponsored by the Manhattan Institute's Shadow Open Market Committee, New York (via webcast), April 14.

Clarida, Richard, Jordi Galí, and Mark Gertler (2002). "A Simple Framework for International Monetary Policy Analysis," Journal of Monetary Economics, vol. 49 (July), pp. 879–904.

Curcuru, Stephanie E., Michiel De Pooter, and George Eckerd (2018). "Measuring Monetary Policy Spillovers between U.S. and German Bond Yields," International Finance Discussion Papers 1226. Washington: Board of Governors of the Federal Reserve System, April.

European Central Bank (2020). "ECB Launches Review of Its Monetary Policy Strategy," press release, January 23.

——— (2021a). "Strategy Review," webpage, https://www.ecb.europa.eu/home/search/review/html/index.en.html.

——— (2021b). "ECB's Governing Council Approves Its New Monetary Policy Strategy," press release, July 8.

Ferreira, Thiago, and Samer Shousha (2021). "Supply of Sovereign Safe Assets and Global Interest Rates," International Finance Discussion Papers 1315. Washington: Board of Governors of the Federal Reserve System, April.

Hoek, Jasper, Steve Kamin, and Emre Yoldas (2020). "When Is Bad News Good News? U.S. Monetary Policy, Macroeconomic News, and Financial Conditions in Emerging Markets (PDF)," International Finance Discussion Papers 1269. Washington: Board of Governors of the Federal Reserve System, January.

Holston, Kathryn, Thomas Laubach, and John C. Williams (2017). "Measuring the Natural Rate of Interest: International Trends and Determinants," Journal of International Economics, vol. 108 (May, S1), pp. S59–75.

Miranda-Agrippino, Silvia, and Hélène Rey (forthcoming). "The Global Financial Cycle," in Gita Gopinath, Elhanan Helpman, and Kenneth Rogoff, eds., Handbook of International Economics, vol. 5. Oxford, United Kingdom: North‑Holland.

Powell, Jerome H. (2020). "New Economic Challenges and the Fed's Monetary Policy Review," speech delivered at "Navigating the Decade Ahead: Implications for Monetary Policy," a symposium sponsored by the Federal Reserve Bank of Kansas City, held in Jackson Hole, Wyo., August 27.

1. The views expressed are my own and not necessarily those of other Federal Reserve Board members or Federal Open Market Committee participants. I would like to thank Burcu Duygan-Bump, Chiara Scotti, and Paul Wood for assistance in preparing these remarks. Return to text

2. The terms "Delphic" and "Odyssean" are used to describe different types of forward guidance. Delphic forward guidance forecasts macroeconomic performance and likely monetary policy actions under that forecast, whereas Odyssean forward guidance publicly commits the FOMC to a future action. For more details, see Campbell and others (2012). Return to text

3. While adopting the euro—and, more broadly, joining a currency union—is the ultimate binding commitment to cooperative monetary policy, the focus of my remarks today is on countries that are not members of a currency union. Return to text

4. The minutes and transcripts of these FOMC meetings are accessible on the Board's website at https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm. Return to text

5. For a detailed discussion of the elements that motivated the launch of the review, see Clarida (2020, 2021) and Powell (2020). Return to text

6. Summaries of these discussions can be found in the minutes of these FOMC meetings, which are accessible on the Board's website at https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm. Return to text

7. The Statement on Longer-Run Goals and Monetary Policy Strategy is available on the Board's website at https://www.federalreserve.gov/monetarypolicy/review-of-monetary-policy-strategy-tools-and-communications-statement-on-longer-run-goals-monetary-policy-strategy.htm. Return to text

8. See European Central Bank (2020). Return to text

9. See European Central Bank (2021a). Return to text

10. See European Central Bank (2021b). Return to text

* This reference was updated on November 22, 2021. Return to text