April 17, 2017

Monetary Policy Expectations and Surprises

Vice Chairman Stanley Fischer

At the Columbia University School of International and Public Affairs, New York, New York

I will address the topic of central bank communications, with a particular emphasis on those times when financial markets and the central bank have different expectations about what a central bank decision will be. Such situations lead to surprises and often to market volatility.

Of course, not all surprises are equal. For one, communications that shift or solidify expectations that are diffuse or not strongly held are less likely to be disruptive than communications that run counter to strongly held market beliefs. Further, there are worse things than surprises. The central bank must provide its views regarding the likely evolution of monetary policy, even when this view is not shared by market participants. A concern for surprising the market should not be a constraint on following or communicating the appropriate path of monetary policy. That said, there are good reasons to avoid unintended surprises in the conduct of policy.1

Why should central banks avoid surprising financial markets? In recent decades, it has been increasingly acknowledged that monetary policy implementation relies importantly on the management of market expectations.2 In theory, clarity about the central bank's reaction function--that is, how the central bank adjusts the stance of monetary policy in response to changing economic conditions--allows the market to alter financial conditions smoothly. This typically helps meet the bank's policy targets, with the result that the markets are working in alignment with the policymaker's goals. Under this theory, repeated market surprises that raise questions about the central bank's reaction function could threaten to disrupt the relationship between the central bank and the markets, making the central bank's job more difficult in the future.3

How can the Fed avoid surprising markets? Clear communication of the Federal Open Market Committee's (FOMC's) views on the economic outlook and the likely evolution of policy is essential in managing the market's expectations. The Committee has a number of communication outlets, including the policy statement, the Chair's news conference, and the Summary of Economic Projections (SEP). The SEP in particular has been useful in providing information on policymakers' assessments of the potential growth rate of the economy and r*, the equilibrium real interest rate, both of which help guide the market's expectations of the eventual path of policy.

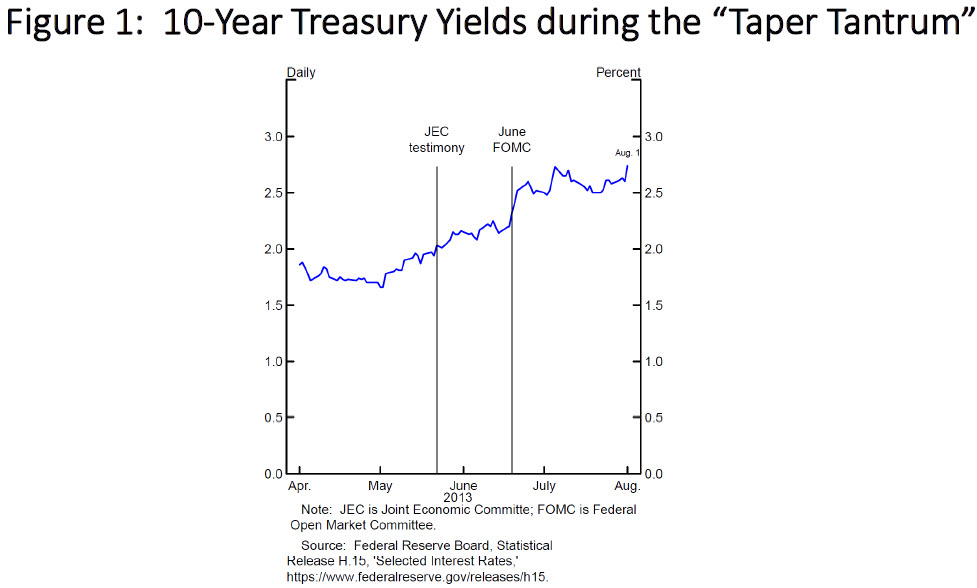

However, avoiding unintended market reactions has not always been easy. The example that immediately comes to mind is the taper tantrum of mid-2013. To recap, over the course of May and June in 2013, the yield on 10-year Treasury securities increased almost 1 percentage point amid increased market discussion of the eventual tapering of Fed asset purchases and some key communications on the topic (figure 1).4 In particular, the 10-year yield rose about 10 basis points after then Chairman Bernanke discussed tapering in public for the first time during the question-and-answer session of his Joint Economic Committee testimony on May 22, commenting that the FOMC could reduce the pace of purchases "in the next few meetings" if it saw continued improvement in the labor market that it was confident would be sustained.5 Yields rose even more sharply after the June FOMC meeting, when, during his postmeeting press conference, Chairman Bernanke noted that if the economy evolved as expected, the FOMC anticipated reducing the pace of purchases in the latter part of 2013 and halting purchases altogether by the middle of 2014.6

{kind=link}

Information gathering is an important part of managing market expectations--for the simple reason that you do not know if you are going to surprise the market unless you have a good estimate of what the market is expecting. A remarkable feature of the taper tantrum is that it was a surprise that should not have been a surprise, at least from the perspective of the information the FOMC had at the time.

In assessing market expectations for policy, the FOMC reviews a variety of market indicators and also draws heavily on the Federal Reserve Bank of New York's Survey of Primary Dealers, whose respondents are the market makers in government securities and the New York Fed's trading counterparties. This survey, conducted about one week prior to each FOMC meeting, gauges primary dealers' expectations about the economy, monetary policy, and financial market developments.7

In the June 2013 primary dealer survey, the median expectation was for tapering to start in December 2013, with purchases ending in June 2014, a path not significantly different from that laid out by Chairman Bernanke in his postmeeting press conference. Thus, one could view Chairman Bernanke's remarks during his June 2013 press conference as consistent with "market expectations."

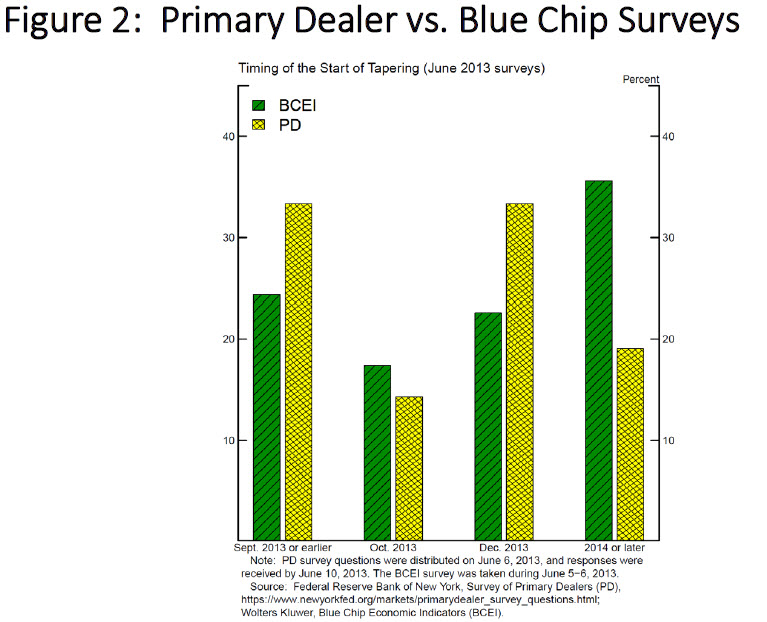

Why did markets react so sharply to the apparent confirmation of the median expectation? One simple possibility is that the median expectation of the primary dealers was not reflective of the median expectation of a wider range of market participants. Respondents to the primary dealer survey are more likely to be Fed watchers and therefore more likely in tune with Fed thinking than the average market participant. For example, as seen in figure 2, a comparison of the June 2013 primary dealer survey with the contemporaneous Blue Chip Economic Indicators survey, which draws from a wider sample of forecasters, reveals that Blue Chip respondents were more likely to expect a later start of tapering and thus more likely to have been surprised by Chairman Bernanke's communications.

{kind=link}

In a related argument, former Federal Reserve Board Governor Jeremy Stein gave an insightful speech in May 2014 addressing how diversity in market expectations could have contributed to the taper tantrum.8 Jeremy pointed out that it is unhelpful to view the "market" as a single individual, a theme that has been explored by Hyun Song Shin of the Bank for International Settlements.9 Rather, the market is a collection of agents that can have widely divergent but perhaps strongly held beliefs at the individual level. Jeremy attributes the taper tantrum to the existence of highly leveraged quantitative easing optimists--in other words, individuals who expected the Federal Reserve to continue to accumulate assets much longer than the median expectation and who put little weight on the median market expectation. Once Chairman Bernanke affirmed the median expectation, these optimists had to quickly unwind their trades, with consequent sharp movements in asset prices.

Where does that leave us? The problem, to quote Jeremy at length, "is that in some circumstances there are very real limits to what even the most careful and deliberate communications strategy can do to temper market volatility. This is just the nature of the beast when dealing with speculative markets, and to suggest otherwise--to suggest that, say, 'good communication' alone can engineer a completely smooth exit from a period of extraordinary policy accommodation--is to create an unrealistic expectation."10

Jeremy was speaking about ending the accumulation of assets onto the Fed's balance sheet. As reported in the minutes for the March 2017 meeting, the FOMC is now discussing a different inflection point, the phasing out of reinvestment and the shrinking of the balance sheet.11 Question: How concerned should we be about a repeat of the taper tantrum as we move through this new inflection point?

We should start answering such a question by recognizing that there is always a chance of some market volatility. Nonetheless, we need to take into account that the New York Fed's Open Market Desk enhanced its information-gathering efforts after and, in part, as a response to the experience of the taper tantrum along two important dimensions. First, in 2014, the Desk augmented its Survey of Primary Dealers with a Survey of Market Participants, going some way to addressing concerns that primary dealers alone were not providing sufficient coverage of market beliefs.12 Second, more recently, questions have been added to the surveys to identify uncertainty about reinvestment policy for each individual survey respondent and not just the dispersion of beliefs about the expected change across respondents.

Starting with the market participant survey, as I noted earlier, one informational constraint that complicated the Fed's understanding of market dynamics around the taper tantrum was the possible divergence of beliefs between the primary dealers, who were surveyed, and the market at large. The differences between the expectations of the primary dealers and those of the panel for the Blue Chip Economic Indicators, shown in figure 2, provide some support for the view that the primary dealers' views may well have differed from those of a wider range of market participants, but it would have been preferable to have a poll of market participants rather than forecasters. Not long after the taper tantrum, in January 2014, the Desk began its separate Survey of Market Participants. The survey panel currently consists of 30 so-called buy-side firms, including hedge funds and asset managers.

Turning now to measures of individual uncertainty, in the April 2013 primary dealer survey, just prior to the taper tantrum, dealers were mostly questioned on their point estimates regarding the timing and conditions under which tapering would commence. Respondents were asked to provide their expectation for the monthly pace of asset purchases after each of several upcoming policy meetings. They were also asked to provide point estimates, or estimates of single particular values, for the quarter and year during which they expected asset purchases in Treasury and agency mortgage-backed securities to be completed. While these questions did provide some notion of the variation in beliefs across respondents, they did not provide much information on how strongly these beliefs were held by the individual respondents, nor on the extent to which their individual beliefs might have been reflected in the size of their market positions and, in particular, the amount of leverage underlying those positions.13

In contrast, the most recent primary dealer and market participant surveys, conducted prior to the March 2017 FOMC meeting, asked survey participants to indicate their view of their own uncertainty over several different aspects of policy. For example, in addition to their point estimates, participants were asked to indicate the percent chance they assigned to the federal funds rate being at various levels when the FOMC first announces a change to the reinvestment policy. They were also asked to assign probabilities to different dates for the first announced change in reinvestment policy.

Why is this information important? To go back to Jeremy Stein's argument about the taper tantrum, Jeremy pointed out that market participants' expectations for tapering varied widely, but he conjectured that some of the participants were very certain in their expectations and that it was primarily their reaction that fueled the taper tantrum. When the surveys reported only point estimates, we had a measure of dispersion across market participants, but we were in the dark on how firmly held these beliefs were. By asking participants to provide a distribution of outcomes, we also obtained a measure of how certain they are of a particular outcome.

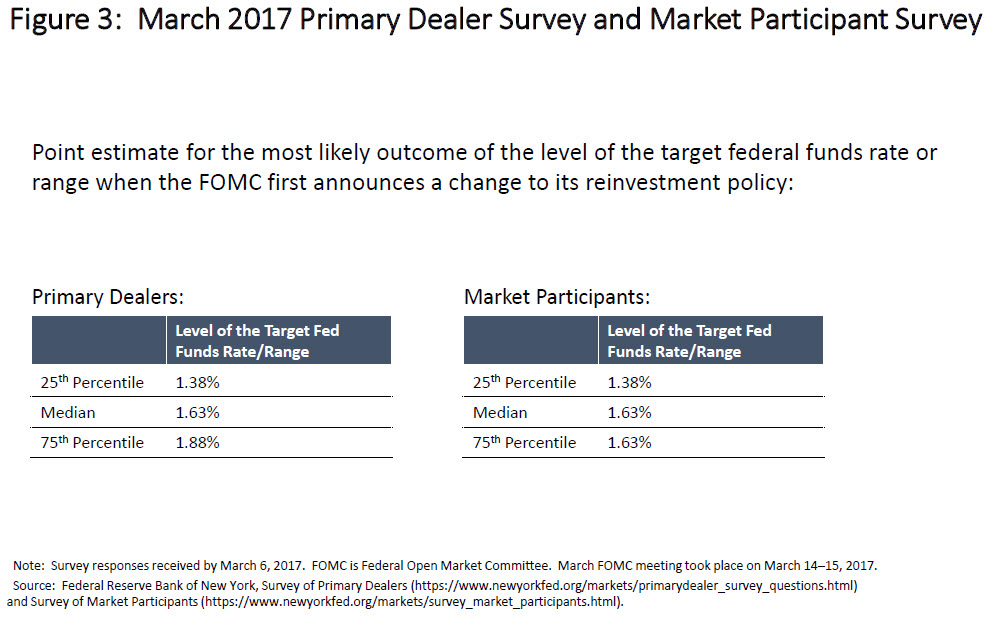

To highlight some results from the March 2017 surveys, as shown in figure 3, the primary dealers' median projection for the level of the target federal funds rate when the FOMC first announces a change in its reinvestment policy was reported to be 1.63 percent. The 25th percentile of the distribution across respondents was 1.38 percent, and the 75th percentile was 1.88 percent, suggesting a fairly tight range around the median expectation. The reported range was even tighter for the market participants around a median projection of 1.63 percent.

{kind=link}

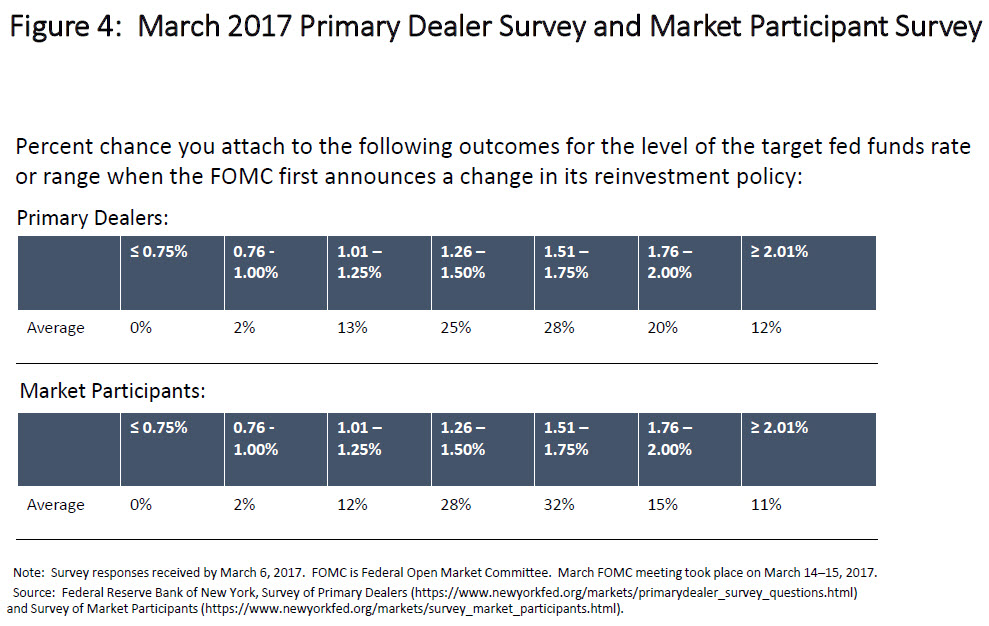

However, it would be a mistake to infer from the narrowness of these ranges a firmness in expectations. As shown in figure 4, when respondents of each survey were asked to indicate the percent chance assigned to different fed funds target levels when the change in policy is announced, the average of all of their reported distributions was wide and flat. The primary dealer survey places roughly equal weight on rates between 1.26 and 2.00 percent. In the underlying nonpublic data for the individual responses, the reported distributions were somewhat narrower but still reflected significant uncertainty, with no primary dealer placing more than 50 percent probability on any particular target range. Like the dealers, the market participants also report wide individual distributions of beliefs.

{kind=link}

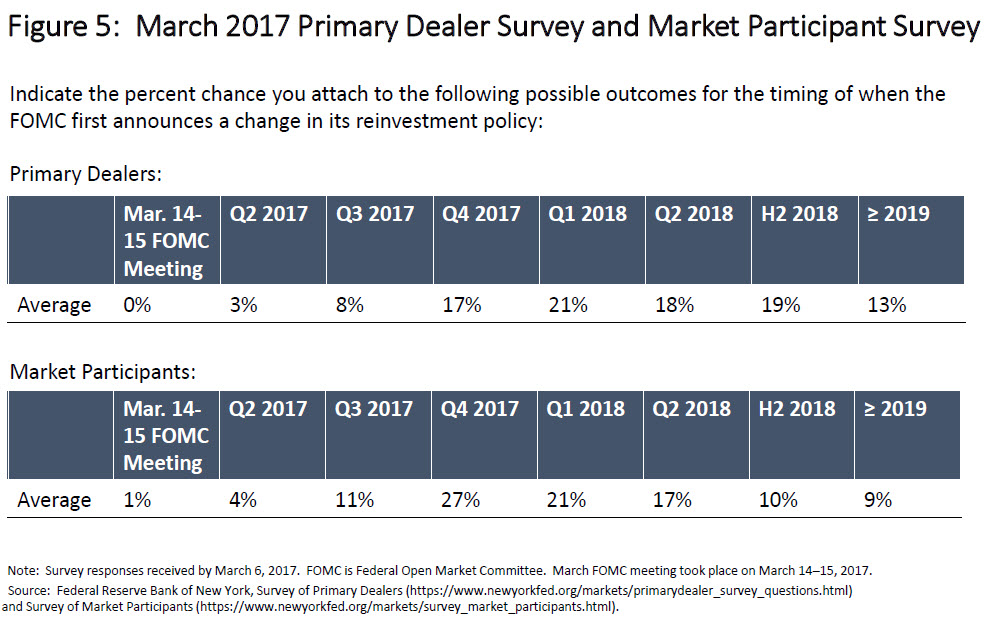

Likewise, when primary dealers were asked about the timing of the announced change in reinvestment policy, the average of their responses was a relatively flat distribution of possible dates, with almost equal probability on the announcement occurring in the fourth quarter of 2017, the first two quarters of 2018, or the second half of 2018 (figure 5). Again, the individual distributions were narrower but still showed a significant amount of uncertainty. Highlighting the usefulness of also surveying market participants, expectations in the market survey are distinctly shifted toward an early announcement date relative to the expectations of the primary dealers.

{kind=link}

The surveys reveal that while beliefs are dispersed across participants, importantly individual survey participants are also significantly uncertain--in other words, any given participant does not appear to have firmly decided on the likely path of policy. The general point is that while we often measure and report differences in views across individuals, the uncertainty that individuals feel internally is also relevant. Recent survey results that show that market participants assign a positive probability to a wide range of outcomes also suggest that the factors that exacerbated the taper tantrum--dispersed but firmly held beliefs--may be less pronounced in current circumstances than they were at the time of the taper tantrum.

The market reaction to the release of the minutes of the March 2017 FOMC meeting supports this interpretation of the interaction of uncertainty and Fed policy communications. The minutes reported that, "provided that the economy continued to perform about as expected, most participants anticipated that gradual increases in the federal funds rate would continue and judged that a change to the Committee's reinvestment policy would likely be appropriate later this year."14 As was shown in figure 5, in the March 2017 surveys, respondents placed the most weight, 71 percent for the primary dealers and 57 percent for the market participants, on an announced change in reinvestment policy not occurring until 2018 at the earliest. Presumably, the April survey will reveal a shift in these distributions.

It is noteworthy, however, that even though the statement in the minutes of the March FOMC meeting regarding Committee members' expectations for announcing changes in the reinvestment policy was not aligned with market expectations, there was only a muted market reaction.15 Perhaps in part, that is because the market participant survey actually revealed a considerable amount of weight, though not the majority, on an announcement occurring this year. Or it is also possible that the diffuse expectations on timing prior to the release of the minutes were a factor in tamping down market volatility as market participants adjust their expectations.16

My tentative conclusion from market responses to the limited amount of discussion of the process of reducing the size of our balance sheet that has taken place so far is that we appear less likely to face major market disturbances now than we did in the case of the taper tantrum. But, of course, as we continue to discuss and eventually implement policies to reduce our balance sheet, we will have to continue to monitor market developments and expectations carefully.

I would like to conclude by briefly discussing two issues. First, a question: Can the Fed be too predictable? And, second, I will add a short comment on the SEP, the quarterly Summary of Economic Projections of the participants in the FOMC.

With regard to whether the Fed can be too predictable, it is hard to argue that predictability in our reaction to economic data could be anything but positive. To reference the beginning of my talk, clarity about the Fed's reaction function allows markets to anticipate Fed actions and smoothly adjust along with the path of policy.

But there is a circumstance where it might be reasonable to argue that the Fed could be too predictable--in particular, if the path of policy is not appropriately responsive to the incoming economic data and the implications for the economic outlook. Standard monetary policy rules suggest that the policy rate should respond to the level of economic variables such as the output gap and the inflation rate. As unexpected shocks hit the economy, the target level of the federal funds rate should adjust in response to those shocks as the FOMC adjusts the stance of policy to achieve its objectives. Indeed, it is these unexpected economic shocks that give rise to the range of uncertainty around the median federal funds rate projection of FOMC participants, represented through fan charts, which was recently incorporated into the SEP. The Federal Reserve could be too predictable if this type of fundamental uncertainty about the economy does not show through to uncertainty about the monetary policy path, which could imply that the Federal Reserve was not being sufficiently responsive to incoming data bearing on the economic outlook.

Let me conclude with a few words on the SEP results as portrayed in the dot plots. The SEP is a highly useful vehicle for providing information to market participants and others for whom Fed actions are important. But we need to remind ourselves that the SEP data for an individual show that person's judgment of the appropriate path of future fed funds rates and the corresponding paths of other variables for which the SEP includes forecasts.

Thus, one may say that the SEP shows the basis from which each participant in the FOMC discussion is likely to start. But the task of moving from that information to an interest rate decision is not simple and requires a great deal of analysis and back-and-forth among FOMC participants at each meeting.

References

Bernanke, Ben S. (2004). "The Logic of Monetary Policy," speech delivered at the National Economists Club, Washington, December 2.

-------- (2013a). "Communication and Monetary Policy," speech delivered at the National Economists Club Annual Dinner, Herbert Stein Memorial Lecture, Washington, November 19.

-------- (2013b). "Statement of Hon. Ben Bernanke, Chairman of the Board of Governors of the Federal Reserve System, Washington, DC (PDF)," in The Economic Outlook, hearing before the Joint Economic Committee, Congress of the United States, May 22, Senate Hearing 113-62, 113 Cong. Washington: Government Printing Office.

-------- (2013c). "Transcript of Chairman Bernanke's Press Conference (PDF)," June 19.

Board of Governors of the Federal Reserve System (2017). "Minutes of the Federal Open Market Committee, March 14-15, 2017," press release, April 5.

Shin, Hyun Song (2017). "How Much Should We Read into Shifts in Long-Dated Yields?" speech delivered at the U.S. Monetary Policy Forum, New York, March 3.

Spicer, Jonathan (2017). "Fed Could Promptly Begin Shedding Bonds This Year: Dudley," U.S. News, March 31, http://money.usnews.com/investing/news/articles/2017-03-31/fed-could-begin-trimming-bond-portfolio-this-year-dudley.

Stein, Jeremy C. (2014). "Challenges for Monetary Policy Communication," speech delivered at the Money Marketeers of New York University, New York, May 6.

Woodford, Michael (2005). "Central Bank Communication and Policy Effectiveness (PDF)," in The Greenspan Era: Lessons for the Future, proceedings of a symposium sponsored by the Federal Reserve Bank of Kansas City, held in Jackson Hole, Wyo., Aug. 25-27. Kansas City, Mo.: Federal Reserve Bank of Kansas City, pp. 399-474.

1. I am grateful to Joseph Gruber and Don Kim of the Federal Reserve Board for their assistance. The views expressed are mine and not necessarily those of the Federal Reserve Board or the Federal Open Market Committee. Return to text

2. Bernanke (2004, 2013a) and Woodford (2005) underscore how central bank efforts to shape market expectations can enhance policy effectiveness. The critical role of market expectations in determining asset prices and reactions to policy changes has long been recognized; it is the explicit recognition of this link in formal models and the analysis of policy that is the recent major achievement. Return to text

3. Historically, there have been times when central banks have preferred to surprise markets--most notably, when changing the value of exchange rate pegs during the era of fixed exchanges. Indicating that a change in the peg was coming would invite an immediate run on the currency, at a significant cost to the central bank's foreign reserves--even in economies with extensive capital controls. Return to text

4. Also notably, Eurodollar futures rates and OIS (overnight index swap) forward rates for intermediate horizons rose sharply, likely in part because some investors who were surprised by the tapering news also revised their expectations about the path of the policy rate. Return to text

5. See Bernanke (2013b), p. 11. Return to text

6. See Bernanke (2013c). Return to text

7. The responses to the survey are received by the Federal Reserve Bank of New York's Markets Group typically by the penultimate Monday before the FOMC meeting. At the time of the taper tantrum, there were 21 primary dealer participants. Currently, there are 23 primary dealers. Past survey results can be found on the Federal Reserve Bank of New York's website at https://www.newyorkfed.org/markets/primarydealer_survey_questions.html. Return to text

8. See Stein (2014). Return to text

9. For a recent example, see Shin (2017). Shin suggests using caution when extrapolating "market" expectations from movements in asset prices, pointing to examples where technical factors likely complicate the interaction of market participants' actions relative to their expectations. Return to text

10. See Stein (2014), paragraph 12. Return to text

11. See Board of Governors (2017). Return to text

12. Past market participant surveys can be found on the Federal Reserve Bank of New York's website at https://www.newyorkfed.org/markets/survey_market_participants.html. Return to text

13. Participants in the April 2013 survey were asked for their probability distribution across the total holdings of the System Open Market Account portfolio at year-end 2013 and year-end 2014, providing some, though incomplete, indication of the extent of uncertainty among market participants. Return to text

14. See Board of Governors (2017), p. 3. Return to text

15. The immediate reaction in yields was a slight rise, but the action quickly reversed, and yields ended the afternoon down 3 to 4 basis points. Return to text

16. Of note, Federal Reserve Bank of New York President William Dudley's comments on March 31, mentioning "sometime later this year or sometime in 2018" (as quoted in Spicer (2017), paragraph 2)) for the timing of a reinvestment policy change, may also have been a factor behind the muted market reaction to the March FOMC minutes. Return to text