July 28, 2008

Whither Federal Reserve Communications

Governor Frederic S. Mishkin

At the Peterson Institute for International Economics, Washington, D.C.

Over the years, the Federal Reserve has significantly increased the transparency of monetary policy making. For example, starting in 1979, the Federal Open Market Committee (FOMC) has included economic projections of the FOMC participants in each semiannual Monetary Report to Congress. Since 1994, the FOMC has publicly announced changes in its target for its policy instrument, the federal funds rate. Most recently, the FOMC extended the horizon for its projections in October 2007 and is now publishing these projections four times a year.1

Has the Federal Reserve gone far enough? Or would further advances in transparency be useful? I will argue here that the science of monetary policy suggests that the Federal Reserve can indeed go further in enhancing its communication strategy, and that doing so would produce important benefits in economic performance and democratic accountability. I will also outline a specific proposal of my own and address a few concerns that some might have with elements of this proposal.

Before proceeding, I would like to emphasize that my remarks today reflect only my own views and not necessarily those of anyone else on the Board of Governors or the FOMC. Indeed, this disclaimer has even more meaning now since, as many of you know, I will be leaving the Federal Reserve Board at the end of August and returning to Columbia University.2

What Are the Key Scientific Principles for Monetary Policy Communication?

To think about what kind of central bank communication is desirable, let's begin by considering some key scientific principles regarding the objectives of monetary policy and the benefits of central bank transparency.

Objectives of Monetary Policy

The modern science of monetary policy is based on the idea that the central bank's objective is to maximize the economic well-being of the households in the economy (Mishkin 2007d). Broadly speaking, this objective can be expressed in terms of two components: minimizing the deviations of inflation from its optimal rate and minimizing the deviations of real economic activity from its so-called natural rate, which is the efficient level determined by the productive potential of the economy. Moreover, this analytical formulation of the objectives of monetary policy captures the essential mission of the Federal Reserve System, as summarized by the Federal Reserve's dual mandate to promote price stability and maximum employment.3 By the way, I believe that the Federal Reserve's role as the lender of last resort is also crucial for fostering the stability of the financial system, but I will not elaborate further on that today.4

Policymakers, academic economists, and the general public broadly agree that maintaining a low and stable inflation rate significantly benefits the economy. For example, low and predictable inflation simplifies the savings and retirement planning of households, facilitates firms' production and investment decisions, and minimizes distortions that arise because the tax system is not completely indexed to inflation. Moreover, I interpret the available economic theory and empirical evidence as indicating that a long-run average inflation rate of about 2 percent, or perhaps a bit lower, is low enough to facilitate the everyday decisions of households and businesses while also alleviating the risk of debt deflation and other pitfalls of excessively low inflation.5

The rationale for promoting maximum sustainable employment is also fairly obvious: Recessions weaken household income and business production, and unemployment hurts workers and their families. As I have outlined elsewhere, these two objectives are typically complementary and mutually reinforcing: that is, done properly, stabilizing inflation contributes to stabilizing economic activity around its sustainable level, and vice versa.6

Nevertheless, it's important to note a fundamental difference between the objectives of price stability and maximum sustainable employment. On the one hand, the long-run average rate of inflation is solely determined by the actions of the Federal Reserve.7 On the other hand, the level of maximum sustainable employment is not something that can be chosen by the Federal Reserve, because no central bank can control the level of real economic activity or employment over the longer run.8 In fact, any attempt to use stimulative monetary policy to maintain employment above its long-run sustainable level would inevitably lead to an upward spiral of inflation with severe adverse consequences for household income and employment.

Recent research has also emphasized the challenges of making contemporaneous "real-time" assessments of the level of maximum sustainable employment, because this level cannot be directly observed and can be inferred only with considerable uncertainty. Thus, in making these assessments, monetary policy makers need to draw on a wide range of indicators from labor, product, and financial markets.9

Benefits of Central Bank Communication

A central element in successful monetary policy is the establishment of a nominal anchor. Why is this so important? The expectations for inflation of households and firms are a key factor in determining the actual behavior of inflation.10 In the absence of a firm nominal anchor, these expectations may wander as the private sector revises its assessment of the rate at which inflation is likely to settle, and those movements in expectations for future inflation can generate pressure on the current inflation rate.

By establishing a transparent and credible commitment to a specific numerical inflation objective, monetary policy can provide a firm anchor for long-run inflation expectations, thereby directly contributing to the objective of low and stable inflation.11 Additionally, the presence of a firm nominal anchor gives the central bank greater flexibility to respond decisively to adverse demand shocks. Such a commitment helps ensure that an aggressive policy easing is not misinterpreted as signaling a shift in the central bank's inflation objective and thereby minimizes the possibility that inflation expectations could move upward and lead to a rise in actual inflation. A strong nominal anchor can be especially valuable in periods of financial market stress, as we have been experiencing recently, when prompt and decisive policy action may be required to minimize the risk of a severe contraction in economic activity that could exacerbate uncertainty and financial market stress.12 Thus, the establishment of an explicit numerical inflation objective can play an important role in promoting financial stability as well as the stability of employment and inflation.

More broadly, it should be noted that central bank transparency contributes importantly to democratic accountability and economic prosperity.13 In particular, in a democratic society, the central bank has a responsibility to provide the public and its elected representatives with a full and compelling rationale for monetary policy decisions. Clarification of the central bank's objectives and policy strategies also reduces economic and financial uncertainty and thereby facilitates efficient decisionmaking by households, businesses, and financial market participants.

How Has Federal Reserve Communication Been Enhanced?

The Federal Reserve has been a pioneer in a number of aspects of central bank communication, many of which I have mentioned at the beginning of these remarks. Now I would like to discuss some of the main aspects of the enhancements to the FOMC's communication strategy that were announced in November. First, the forecast horizon for the FOMC's economic projections now covers three calendar years instead of only two years. For example, the projections released after the past meeting extend to 2010. Second, the Committee now publishes these projections four times a year rather than twice a year. Third, the projections now include a forecast of overall consumer price inflation, as measured by the price index for personal consumption expenditures (PCE), a broad price index that corresponds closely to the price stability objective in the Federal Reserve's dual mandate. These forecasts of overall inflation complement the ongoing forecasts the Committee provides of the so-called core version of the PCE price index, which excludes the prices of food and energy.14 Fourth, the release of the projections now includes a narrative describing FOMC participants' views of the principal forces shaping the outlook and the sources of risks to that outlook.

As I indicated last November, I believe that these enhancements provide important information that will contribute to the public's understanding of our objectives and the rationale for our policy actions and hence will facilitate the decisionmaking of households and businesses.15

As reported last week in conjunction with the minutes of the latest FOMC meeting, the projections for overall PCE inflation at a three-year horizon (which is currently 2010) fell in a range of 1.6 percent to 2.1 percent, and the central tendency of these projections was 1.8 percent to 2 percent.16 Each FOMC participant's projection is made under the assumption of "appropriate" monetary policy--that is, the path of policy calibrated to achieve outcomes for economic activity and inflation that are, in the eyes of each participant, most consistent with the objectives of price stability and maximum employment. For that reason, the longer-run inflation projections provide information about each FOMC participant's assessment of the long-run inflation rate that best promotes those dual objectives--what I have referred to as the "mandate-consistent inflation rate."17 The increased information that these projections convey regarding FOMC participants' views of the mandate-consistent inflation rate, combined with the FOMC's continuing commitment to keeping inflation low and stable, should help anchor inflation expectations and actual inflation more firmly.

The longer-run projections of output growth and unemployment are heavily influenced by FOMC participants' assessments of the sustainable rates of output growth and employment. As a result, these projections can provide the public with useful information regarding the FOMC's estimates of the sustainable rate of output growth (often referred to as potential output growth) and of the sustainable unemployment rate (often referred to as the natural rate of unemployment).

Providing projections for the short run as well as for the longer run encourages FOMC participants to think in terms of desirable paths for inflation and output, a discipline that economic research suggests will produce better policy outcomes. These projections also are useful in enabling the FOMC to explain its policy decisions and strategies more fully in the context of its medium-term objectives for economic activity and inflation as well as the risks to those objectives. As a result, the public and the Congress can better assess whether our forecasts of the economy are reasonable and whether we are pursuing a policy that is consistent with achieving the dual mandate of price stability and maximum sustainable employment. The result should be increased accountability that is consistent with basic democratic principles.

Is There Room for Further Improvement?

Although the enhancements to the FOMC's communication strategy last November have been a major step forward, I believe that there is some room for further improvement.

Conceptual Considerations

As a conceptual matter, the three-year horizon of the projections may not be long enough to provide sufficient clarity about the views of FOMC participants regarding the mandate-consistent inflation rate, the sustainable growth rate of output, or the natural rate of unemployment. Moreover, these projections do not establish a transparent and credible commitment to a specific numerical inflation objective and hence do not provide a sufficiently firm nominal anchor.

In my view, the length of the forecast horizon is particularly relevant at the current juncture in considering the projections for output growth and unemployment. Because of the recent adverse shocks to the economy--including turmoil in financial markets and the sharp increase in the prices of oil--output growth in recent quarters has fallen below potential, and the unemployment rate is, as best as I can judge, above the natural rate. Similarly, sharp increases in the prices of many commodities have driven inflation above rates consistent with price stability. Even under appropriate monetary policy, Committee forecasts of inflation, output growth, and unemployment might not settle at their respective long-run rates within the three-year horizon, obscuring Committee participants' views about these key parameters.

This problem may currently be somewhat less acute for the current set of inflation projections, because inflation is projected to moderate to about 2 percent or below by the end of the projection period. Nevertheless, to the extent that some slack in economic activity is projected to persist through 2010, that slack might well induce a modest further decline in inflation, implying that policymakers' projections for inflation in 2010 might be a bit higher than their assessments of the mandate-consistent inflation rate.

Empirical Evidence

My discussion of room for improvement relative to the Federal Reserve's current communication strategy has been theoretical. There is, fortunately, evidence from a number of countries that have adopted an explicit numerical goal for inflation, including Canada, New Zealand, Sweden, and the United Kingdom.18 And there is also evidence from the experience of the European Central Bank (ECB), which has not adopted an explicit numerical goal but has provided a fairly precise verbal description of its commitment to keeping inflation "below, but close to, 2 percent in the medium term."19

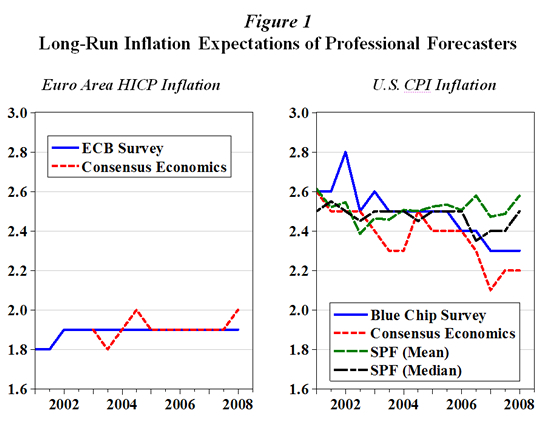

Over the past several years, empirical work that has drawn on this international experience has found some significant benefits in anchoring inflation expectations by establishing an explicit inflation objective. For example, let's take a look at three figures from a recent paper by Beechey, Johannsen, and Levin.20 Figure 1 depicts the long-run inflation expectations from surveys of professional forecasters in the euro area and in the United States. Inflation expectations in both economies are relatively well anchored. The lines on the left for the euro area are extremely flat, with only tiny and occasional deviations from the ECB's inflation goal of keeping inflation just below 2 percent over the medium run. In the United States, inflation expectations as measured by the mean or median forecast in the Survey of Professional Forecasters are also quite fixed at around 2-1/2 percent for consumer price index (CPI) inflation, but those in other surveys move around somewhat more.

{kind=link}

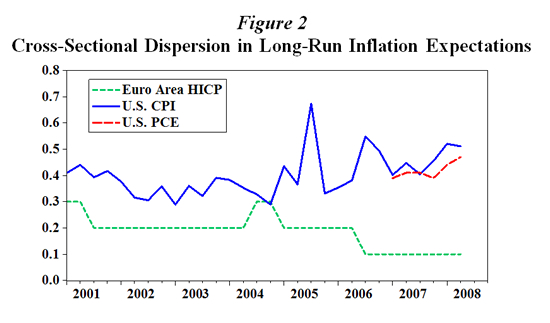

However, there is substantially greater disagreement in long-run inflation forecasts for the United States than for the euro area. As shown in figure 2, the standard deviation of U.S. inflation forecasts at each survey date is higher than the standard deviation of corresponding euro area inflation forecasts. Moreover, the degree of dispersion in the views of individual forecasters has gradually declined towards negligible levels for the euro area but not for the United States. One obvious interpretation of these patterns is that professional forecasters in the United States are less certain about the Federal Reserve's longer-term inflation goal.

{kind=link}

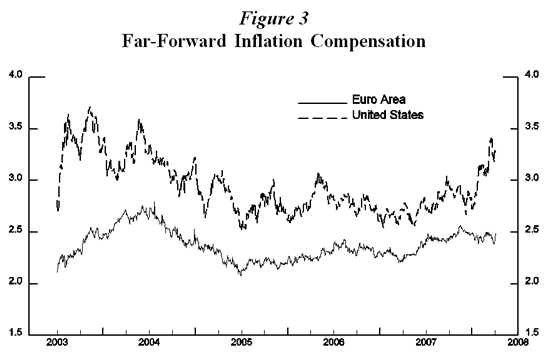

That uncertainty may also explain differences in the behavior of inflation compensation as implied by the gap between nominal and real yields on long-term bonds. Figure 3 depicts far-forward inflation compensation (that is, the one-year-forward rate nine years ahead) for the United States and the euro area. Inflation compensation, sometimes referred to as "breakeven inflation," reflects not only inflation expectations but also a premium that compensates for uncertainty about inflation outcomes at the specified horizon. Evidently, far-forward inflation compensation for the euro area displays much smaller fluctuations than for the United States, consistent with greater stability of inflation expectations and a lower degree of uncertainty about longer-run inflation outcomes. Moreover, regression analysis confirms that U.S. far-ahead forward inflation compensation exhibits statistically significant responses to surprises in macroeconomic data releases--consistent with the view that market participants are continuously revising their views about the longer-run outlook for U.S. inflation. In contrast, euro-area inflation compensation does not respond significantly to economic news.21

{kind=link}

One concern might be that these benefits in anchoring inflation expectations could come at the expense of the performance of output growth. However, the empirical evidence suggests that central banks with explicit inflation goals do not have worse output performances than central banks, such as the Federal Reserve, that have not specified an explicit numerical goal for inflation.22

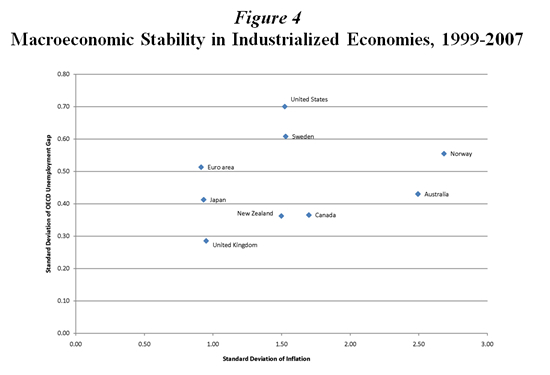

In addition, the international experience suggests that an explicit inflation goal does not imply that these central banks place more emphasis on stabilizing inflation to the detriment of stabilizing output. Figure 4 plots the standard deviation of headline inflation (measured as the quarter-on-quarter change at an annual rate) against the standard deviation of the unemployment gap as estimated by the Organisation for Economic Co-operation and Development. Note that the United States appears near the top of the graph, as the country with the highest volatility of unemployment gaps.23 Moreover, a number of researchers have shown that the response of policy interest rates to economic activity and inflation in the United States and euro area is quite similar, suggesting that the Federal Reserve and the ECB place similar weights on inflation and activity.24

{kind=link}

This overview of the evidence should not be viewed as suggesting that the steps that the FOMC has taken to improve its communications over the past couple of decades or the more recent enhancements last fall have provided no benefits. Rather, this analysis supports the view that some room for further improvement still remains.

What Should Be Done? A Proposal

In light of these considerations, I would like to suggest several specific modifications to the Federal Reserve's current communication strategy.

- First, the horizon for the projections on output growth, unemployment, and inflation should be lengthened. This change might involve simply an announcement of FOMC participants' assessment of where inflation, output growth, and unemployment would converge under appropriate monetary policy in the long run. Alternatively, the horizon for the projections could be extended out further, say to five or more years.

- Second, FOMC participants should work toward reaching a consensus on the specific numerical value of the mandate-consistent inflation rate, and this consensus value should be reflected in their longer-run projections for inflation.25

- Third, the FOMC should emphasize its intention that this consensus value of the mandate-consistent inflation rate would only be modified for sound economic reasons, such as substantial improvements in the measurement of inflation or marked changes in the structure of the economy.

Would This Proposal Work?

It is reasonable to ask a few questions about whether these proposed changes would be feasible or desirable adjustments to the Federal Reserve's communication strategy.

Would This Proposal Be Consistent with the Dual Mandate?

Some commentators have worried that establishing a specific numerical inflation objective might lead to an overemphasis on controlling inflation and not enough concern about stabilizing real economic activity. My proposal is, however, consistent with the dual mandate, because it has the advantage of being less likely to be misinterpreted as a commitment to control inflation within a tight range over short horizons, since it only involves a consensus on the mandate-consistent inflation rate and an agreement not to change it without scientific justification. By so doing, this proposal should enhance the ability of monetary policy to stabilize fluctuations in economic activity, and therefore support the dual objectives provided to the Federal Reserve by congressional legislation.

One lesson from the experiences of foreign central banks with explicit inflation objectives is that such a goal is indeed consistent with a dual mandate for stable prices and maximum employment. Some of the central banks that have explicit inflation objectives have mandates that specifically include other objectives such as output stabilization and financial stability. For example, the regulations governing the Norwegian central bank specifically state that monetary policy should contribute to stable developments in output and employment. Similarly, the Reserve Bank of Australia aims at encouraging strong and sustainable economic growth while ensuring that consumer inflation is consistent with the explicit numerical objective over the medium run.

Even at central banks where the inflation objective appears to be the primary goal, policymakers do acknowledge that the stability of economic activity is also an important objective. For instance, Charles Goodhart, a former member of the Bank of England's Monetary Policy Committee (MPC), has emphasized that the MPC aims at stabilizing both inflation and real economic activity and that its monetary policy strategy is quite similar to that of other central banks such as the Federal Reserve.26 Moreover, as I noted earlier, the empirical evidence is consistent with this view: Central banks with explicit inflation objectives do not have worse outcomes for output growth and do not appear to be favoring inflation stabilization at the expense of output stabilization.

Should the Inflation Objective Be Stated as a Specific Numerical Value Rather Than a Range?

Establishing a specific numerical value for the inflation objective is a crucial aspect of my proposal. As discussed in my recent speech with the whimsical title of "Comfort Zones, Shmumfort Zones," publishing a range of values for the inflation objective has a number of undesirable features.27 For example, when the price stability objective is formulated in terms of an acceptable range of inflation outcomes, the policy implications may be difficult to interpret and may make it harder for a committee of policymakers to decide on an appropriate course of monetary policy.

Describing inflation objectives in terms of a comfort zone could also lead to perverse expectations dynamics that leads to larger fluctuations in economic activity.28 Moreover, the uncertainty associated with long-run inflation under a zone could affect the perceived long-term real interest rates faced by households and firms through differential effects on the expectations of different agents, a pitfall that seems particularly plausible given the dispersion in professional forecasters' long-run expectations for U.S. inflation, as shown in figure 2.29

Indeed, one important lesson from the international experience is that point objectives have proven more effective than ranges in anchoring inflation expectations.30 And even in cases where the inflation objective is formulated in terms of a band, emphasizing the midpoint of that band helps allay concerns that the central bank will only take aggressive policy actions at the edges of the band. In light of these considerations, many foreign central banks have taken steps to move away from an inflation objective that is expressed as a range and have moved toward an objective that is expressed as a single numerical value, as does my proposal here.

For example, the Bank of England initially announced an inflation objective in terms of a range from 1 percent to 4 percent for the Retail Price Index excluding mortgage interest payments (RPIX), but this range was perceived as a band of indifference that implied the Bank would be equally satisfied with inflation outcomes anywhere within the range. Perhaps partly as a result, inflation expectations and realized inflation tended to remain close to the top of the range. Thus, the objective subsequently was modified to a point target of 2-1/2 percent for RPIX inflation, where inflation above or below that value was viewed as being equally undesirable. Inflation expectations converged quickly to this new rate in surveys of both households and professional forecasters, and the move was favorably received both by the public and by financial markets.31

In another instructive example, the ECB had initially emphasized a broad objective of keeping inflation below 2 percent over the medium term, but in May 2003, the ECB clarified that policy would be aimed at maintaining inflation below, but close to, 2 percent. That clarification was welcomed by market participants and likely contributed to the firm anchoring of long-run inflation expectations.

Would This Proposal Be Misinterpreted as Establishing a Goal for Maximum Employment?

As I have emphasized, a central bank can determine the long-run average inflation rate but cannot choose the maximum sustainable level of employment, which is determined by the underlying structure of the real economy. Thus, one might worry whether providing longer-horizon projections for output growth and employment as well as inflation might be mistakenly interpreted as establishing specific--and ultimately infeasible--goals for real economic activity. I do not believe this potential pitfall poses a substantial risk. Because monetary policy determines the inflation rate in the long run, agreement on the mandate-consistent inflation rate among FOMC members can only lower uncertainty about future inflation. In contrast, differences in the long-run projections for output growth and unemployment across FOMC participants are inevitable, as these factors are outside of the Committee's control and inherently uncertain given our understanding of economic fluctuations. The ongoing dispersion in long-run projections for output growth and unemployment that is a feature of my proposal would help underscore that these projections are assessments of potential output growth and the natural rate of unemployment and should not be viewed as numerical objectives chosen by the FOMC.

Could the Numerical Inflation Objective Be Modified if Appropriate?

One might be concerned about whether the numerical inflation objective could be subsequently adjusted for sound economic reasons. However, I would again draw on the experience from other central banks and point out that changing the technical specification of the inflation goal has been very well received elsewhere.

For example, in late 2003, the inflation target of the Bank of England was switched from a 2-1/2 percent target for RPIX inflation to a 2 percent target for the CPI.32 Despite some concerns both from the public and the Bank about the change, it appears to have been implemented with few problems. Indeed, figure 5 shows the distribution of professional forecasters' medium- to long-range inflation projections in the United Kingdom in the fourth quarter of 2001, the first quarter of 2004, and the second quarter of this year. These expectations were initially clustered relatively tightly around the inflation objective of a 2-1/2 percent rate but moved to the new value of 2 percent within a few months of the announced change and have remained firmly anchored since then, especially compared with the dispersion in views regarding the longer-term outlook for U.S. inflation (Gürkaynak, Levin, and Swanson, 2008). Similarly, as I mentioned earlier, the ECB also clarified its inflation objective, and this change was implemented smoothly.

{kind=link}

Would This Proposal Provide a Sufficient Degree of Commitment to the Nominal Anchor?

By stating its intention not to modify the mandate-consistent inflation rate without a clear technical rationale, I believe that the FOMC would provide a firm nominal anchor that would not differ much in practice from some alternative commitment to a specific numerical inflation objective. In explaining this view, I want to draw on some conversations with my son, who is currently enrolled in law school, and to take advantage of the opportunity to demonstrate my erudition by using a bit of Latin. (As you may know, I've already demonstrated my command of Yiddish in another recent speech.33 )

In this instance, the relevant legal term is stare decisis, which means "to stand by things decided."34 This concept plays a crucial role in the functioning of our legal system: When the Supreme Court makes a decision in any given case, the reasoning behind that decision serves as a precedent that guides all subsequent legal considerations, except for particular circumstances in which the Supreme Court finds compelling reasons for modifying or overturning a prior decision. The approach that I have recommended here would operate in a roughly similar way. Because the consensus on the mandate-consistent inflation rate would be very transparent, the FOMC would not be inclined to modify that consensus value except for sound economic reasons; hence, this proposal would be sufficient to provide a firm anchor for long-run inflation expectations.

Conclusion

While the recent enhancements of the Federal Reserve's communication strategy have been beneficial, I believe that the science of monetary policy indicates that the FOMC needs to go even further. Thus, I have suggested that the FOMC should lengthen the horizons of its projections, reach a consensus on a specific numerical value for the mandate-consistent inflation rate, and indicate that this consensus value would be modified only for good scientific reasons. I have argued that moving in this direction would improve economic outcomes by anchoring inflation expectations more firmly while allowing sufficient flexibility to ensure that monetary policy would continue to be fully consistent with our dual mandate of price stability and maximum employment.

Of course, once I return to academia at the end of next month, I will no longer be participating in any official consideration of these issues. However, I hope that the views that I have expressed today will be useful in contributing to the continuing evolution of the Federal Reserve's communication strategy.

References

Ball, Laurence, and Niahm Sheridan (2003). "Does Inflation Targeting Matter?" in Ben S. Bernanke and Michael Woodford, eds., The Inflation-Targeting Debate. Chicago: University of Chicago Press, pp. 249-76.

Bank of England (2008). "Key Monetary Policy Dates Since 1990."

Beechey, Meredith J., Benjamin K. Johannsen, and Andrew Levin (2008). "Are Long-Run Inflation Expectations Anchored More Firmly in the Euro Area than in the United States?" Manuscript, Board of Governors of the Federal Reserve System. A previous version of this paper was issued as CEPR Discussion Paper 6536. London: Centre for Economic Policy Research, October.

Bernanke, Ben S. (2007). "Federal Reserve Communications," speech delivered at the Cato Institute 25th Annual Monetary Conference, Washington, November 14, www.federalreserve.gov/newsevents/speech/bernanke20071114a.htm.

Bernanke, Ben S., Thomas Laubach, Frederic S. Mishkin, and Adam S. Posen (1999). Inflation Targeting: Lessons from the International Experience. Princeton: Princeton University Press.

Brown, Gordon (2003). "Remit for the Monetary Policy Committee of the Bank of England and the New Inflation Target (188 KB PDF)," letter from the Chancellor of the Exchequer to the Governor of the Bank of England, and accompanying annex (35 KB PDF).

Central Bank of Chile (2007). "Monetary Policy in an Inflation Targeting Framework," January.

Christiano, Lawrence, Roberto Motto, and Massimo Rostagno (2007). "Shocks, Structures or Monetary Policies? The Euro Area and US after 2001," NBER Working Paper 13521. Cambridge, Mass.: National Bureau of Economic Research.

European Central Bank (2003). Background Studies for the ECB's Evaluation of its Monetary Policy Strategy. Frankfurt: European Central Bank, May.

Federal Open Market Committee (2008). "Minutes of the Federal Open Market Committee, April 29-30, 2008," released May 21.

Fraser, Bernie (1993). "Some Aspects of Monetary Policy (58 KB PDF)," speech delivered to Australian Business Economists, Sydney, March 31.

Friedman, Milton (1963). Inflation: Causes and Consequences. New York: Asia Publishing House.

Giavazzi, Francesco, and Frederic S. Mishkin (2006). "An Evaluation of Swedish Monetary Policy Between 1995 and 2005 (1.41 MB PDF)," a report prepared for the Riksdag Committee on Finance. Stockholm: Sveriges Riksdag.

Goodhart, Charles A.E. (2005). "The Monetary Policy Committee's Reaction Function: An Exercise in Estimation,"Topics in Macroeconomics, vol. 5 (no. 1), article 18.

Gürkaynak, Refet S., Brian Sack, and Eric T. Swanson (2005). "The Sensitivity of Long-Term Interest Rates to Economic News: Evidence and Implications for Macroeconomic Models," American Economic Review, vol. 95 (March), pp. 425-36.

Gürkaynak, Refet S., Andrew Levin, and Eric T. Swanson (2008). "Does Inflation Targeting Anchor Long-Run Inflation Expectations? Evidence from Long-Term Bond Yields in the U.S., U.K., and Sweden." Manuscript, Board of Governors of the Federal Reserve System. A previous version was issued as CEPR Discussion Paper 5808. London: Centre for Economic Policy Research, August.

Gürkaynak, Refet S., Andrew Levin, Andrew N. Marder, and Eric T. Swanson (2006). "Inflation Targeting and the Anchoring of Inflation Expectations in the Western Hemisphere," in Frederic S. Mishkin and Klaus Schmidt-Hebbel, eds., Inflation Targeting. Santiago: Bank of Chile.

King, Mervyn (2004). Speech (108 KB PDF) delivered at the annual Birmingham Forward/CBI Business Luncheon, Aston Villa Football Club, Birmingham, United Kingdom, January 20.

Levin, Andrew T., Fabio M. Natalucci, and Jeremy M. Piger (2004). "The Macroeconomic Effects of Inflation Targeting (406 KB PDF)," Federal Reserve Bank of St. Louis, Review, vol. 86 (July/August), pp. 51-80.

Mishkin, Frederic S. (2007a). "Inflation Dynamics," speech delivered at the Annual Macro Conference, Federal Reserve Bank of San Francisco, San Francisco, March 23.

_________ (2007b). "Monetary Policy and the Dual Mandate," speech delivered at Bridgewater College, Bridgewater, Va., April 10.

_________ (2007c). "Estimating Potential Output," speech delivered at the Conference on Price Measurement for Monetary Policy, Federal Reserve Bank of Dallas, Dallas, May 24.

_________ (2007d). "Will Monetary Policy Become More of a Science?" Finance and Economics Discussion Series 2007-44. Washington: Board of Governors of the Federal Reserve System, September.

_________ (2007e). "Headline versus Core Inflation in the Conduct of Monetary Policy," speech delivered at the Business Cycles, International Transmission, and Macroeconomic Policies Conference, HEC Montreal, Montreal, Canada, October 20.

_________ (2007f). "Financial Instability and the Federal Reserve as a Liquidity Provider," speech delivered at the Museum of American Finance Commemoration of the Panic of 1907, New York, October 26.

_________ (2007g). "Financial Instability and Monetary Policy," speech delivered at the Risk USA 2007 Conference, New York, November 5.

_________ (2007h). "The Federal Reserve's Enhanced Communication Strategy and the Science of Monetary Policy," speech delivered to the Undergraduate Economics Association at the Massachusetts Institute of Technology, Cambridge, Mass., November 29.

_________ (2008a). "Monetary Policy Flexibility, Risk Management, and Financial Disruptions," speech delivered at the Federal Reserve Bank of New York, New York, January 11.

_________ (2008b). "Does Stabilizing Inflation Contribute to Stabilizing Economic Activity?" speech delivered at East Carolina University's Beta Gamma Sigma Distinguished Lecture Series, Greenville, N.C., February 25.

_________ (2008c). "Comfort Zones, Shmumfort Zones," speech delivered at the Sandridge Lecture of the Virginia Association of Economists and the H. Parker Willis Lecture of Washington and Lee University, Lexington, Va., March 27.

_________ (2008d). "Central Bank Commitment and Communication," speech delivered at the Princeton Center for Economic Policy Studies, New York, April 3.

_________ (2008e). "How Should We Respond to Asset Price Bubbles?" speech delivered at the Wharton Financial Institutions Center and Oliver Wyman Institute's Annual Financial Risk Roundtable, Philadelphia, May 15.

Mishkin, Frederic S., and Adam S. Posen (1997). "Inflation Targeting: Lessons from Four Countries," Federal Reserve Bank of New York, Economic Policy Review, vol. 3 (August), pp. 9-110.

Mishkin, Frederic S., and Klaus Schmidt-Hebbel (2001). "One Decade of Inflation Targeting in the World: What Do We Know and What Do We Need to Know?" in Norman Loayza and Raimundo Soto, eds., Inflation Targeting: Design, Performance, Challenges. Santiago: Central Bank of Chile, pp. 117-219.

_________ (2007). "Does Inflation Targeting Make a Difference?" in Frederic S. Mishkin and Klaus Schmidt-Hebbel, eds., Monetary Policy Under Inflation Targeting. Santiago: Central Bank of Chile, pp. 291-372.

Mishkin, Frederic S., and Niklas J. Westelius (2008). "Inflation Band Targeting and Optimal Inflation Contracts," Journal of Money, Credit and Banking, vol. 40 (June), pp. 557-82.

Orphanides, Athanasios, and Volker Wieland (2000). "Inflation Zone Targeting," European Economic Review, vol. 44 (June), pp. 1351-87.

Reserve Bank of Australia and the Treasurer of Australia (1996). "Statement on the Conduct of Monetary Policy," August 14.

Reserve Bank of Australia (2008). "About Monetary Policy."

Smets, Frank, and Raf Wouters (2005). "Comparing Shocks and Frictions in US and Euro Area Business Cycles: A Bayesian DSGE Approach," Journal of Applied Econometrics, vol. 20 (no. 2, Recent Developments in Business Cycle Analysis), pp. 161-83.

Footnotes

1. A more detailed review of past enhancements in Federal Reserve communications can be found in Bernanke (2007) and Mishkin (2007h). Return to text

2. I appreciate assistance from Brian Doyle, Michael Kiley, and Andrew Levin in the preparation of these remarks. Return to text

3. Mishkin (2007b). Return to text

4. Mishkin (2007f, 2007g, 2008a, 2008e) discusses the lender-of-last-resort function and reviews the Federal Reserve's recent measures for providing additional liquidity to financial markets. Return to text

5. Mishkin (2008c). Return to text

6. Mishkin (2008b). Return to text

7. This is the point of Milton Friedman's famous adage, "Inflation is always and everywhere a monetary phenomenon" (Friedman, 1963, p. 17). Return to text

8. Mishkin (2007b). Return to text

9. Mishkin (2007c). Return to text

10. Mishkin (2007a). Return to text

11. Mishkin (2008d). Return to text

12. Mishkin (2008a). Return to text

13. Bernanke (2007). Return to text

14. Mishkin (2007e) discusses several key distinctions between overall inflation and core inflation in informing the conduct of monetary policy. Return to text

15. Mishkin (2007h). Return to text

16. The range of projections from the April FOMC meeting was 1.5 percent to 2 percent for overall PCE, while the central tendency was 1.8 percent to 2 percent (FOMC, 2008). Return to text

17. This is particularly true when the underlying level of inflation is reasonably close to the mandate-consistent rate, as I believe to be the case at the present time. Return to text

18. Further details on the experiences of these countries--as well as other economies that have adopted explicit numerical inflation objectives--may be found in Mishkin and Posen (1997), Bernanke and others (1999), and Mishkin and Schmidt-Hebbel (2001, 2007). Return to text

19. See ECB (2003, p. 6). Indeed, the experience of other central banks confirms that establishing a specific numerical value for the inflation objective can be viewed as a technical issue that does not necessarily require any new legislation, but, of course, this depends on the political system in each country. In Sweden, for example, the government announced in 1991 that low inflation was an overriding political goal, but the Riksbank's January 1993 announcement of an explicit inflation objective did not coincide with any legislative action (Giavazzi and Mishkin, 2006). The Riksbank stated an inflation goal accompanied by a two-year start-up period, so that the goal was to become operational in January 1995. Soon after the initial announcement by the Riksbank, various changes to its legislative mandate were proposed. Many of these were adopted in 1999, when a new constitution and new Riksbank Act came into effect. Similarly, the Reserve Bank of Australia announced a numerical inflation objective in 1993, and this objective was formalized about three years later when the government and governor issued a joint "Statement on the Conduct of Monetary Policy" (see Fraser, 1993; Reserve Bank of Australia and the Treasurer of Australia, 1996; and Reserve Bank of Australia, 2008). And in Chile, the law establishes broad objectives for the Central Bank of Chile, but the Bank itself has elaborated that its mandate for price stability is to be interpreted at aiming for a 3 percent inflation rate at a two-year horizon (see Central Bank of Chile, 2007). Return to text

20. Beechey, Johannsen, and Levin (2008). Return to text

21. Gürkaynak, Sack, and Swanson (2005) demonstrated the sensitivity of U.S. far-ahead forward nominal interest rates to economic news. Gürkaynak, Levin, and Swanson (2008) examined far-ahead forward inflation compensation and found significant effects of news for the United States but not for Sweden or the United Kingdom; Gürkaynak, Levin, Marder, and Swanson (2007) obtained consistent results for Canada and Chile, and Beechey, Johannsen, and Levin (2008) found no significant effects of news on far-ahead forward inflation compensation for the euro area. Return to text

22. See Ball and Sheridan (2003) and Levin, Natalucci, and Piger (2003). Return to text

23. Of course, this evidence is only suggestive, because differences in economic structure may account for some of these differences; for example, most of the countries with explicit inflation objectives are small and relatively open economies that might be expected to have higher volatility of both unemployment and inflation. It should also be noted that the U.S. economy is closer to the center of the pack instead of an outlier when the volatility of the real economy is measured in terms of output gaps rather than unemployment gaps. Return to text

24. See Smets and Wouters (2005) and Christiano, Motto, and Rostagno (2007). Return to text

25. FOMC participants would work toward reaching this consensus about mandate-consistent inflation using the overall inflation rate, as measured by PCE inflation, to be consistent with the Federal Reserve's dual mandate. Overall and core (excluding changes in the prices of food and energy) inflation rates are likely to be at similar rates at a horizon of five or more years. Return to text

26. Goodhart (2005). Return to text

27. Mishkin (2008c). Return to text

28. Mishkin (2008c). Return to text

29. At a given point in time, the yield on a bond with a specific maturity is determined by the views of the "marginal investor" who is indifferent between buying and selling that bond. Thus, if financial market participants have heterogenous views about the central bank's inflation objective, the identity of the marginal investor might vary systematically over time in ways that influence the evolution of long-term bond yields. Another pitfall is that if a central bank places a high degree of emphasis on the boundaries of a range, then these threshold effects imply nonlinearities in the conduct of monetary policy that are likely to produce less desirable economic outcomes; see Orphanides and Wieland (2000). Return to text

30. See Mishkin and Westelius (2008) and Mishkin (2008c). Return to text

31. In June 1995, the range of 1 percent to 4 percent was dropped and the goal became an inflation rate of 2-1/2 percent or less for RPIX inflation. The goal became a point target of 2-1/2 percent on the RPIX with deviations in either direction treated symmetrically in December 1997, about seven months after the creation of the Monetary Policy Committee and the granting of Bank of England independence (Bank of England, 2008). Return to text

32. See Brown (2003) and King (2004) for the rationale behind the change. Return to text

33. Mishkin (2008c). Return to text

34. The full legal term is stare decisis et non quieta movere, and the literal translation from the Latin is as follows: "Stand by things decided and do not move that which is still." Return to text