June 23, 2017

Central Clearing and Liquidity

At the Federal Reserve Bank of Chicago Symposium on Central Clearing, Chicago, Illinois

Thank you for inviting me to speak today.1 The Federal Reserve Bank of Chicago and Darrell Duffie have provided a valuable public service in hosting this annual symposium on central clearing. I will start my remarks by taking stock of the progress made in strengthening central counterparties (or CCPs), and then offer some thoughts on central clearing and liquidity risks.

The huge losses suffered by the American International Group (AIG) on its over-the-counter derivatives positions contributed to the financial crisis and highlighted the risks in derivatives markets. In response, the Group of Twenty nations committed in 2009 to moving standardized derivatives to central clearing. Central clearing serves to address many of the weaknesses exposed during the crisis by fostering a reduction in risk exposures through multilateral netting and daily margin requirements as well as greater transparency through enhanced reporting requirements. Central clearing also enables a reduction in the potential cost of counterparty default by facilitating the orderly liquidation of a defaulting member's positions, and the sharing of risk among members of the CCP through some mutualization of the costs of such a default.

But central clearing will only make the financial system safer if CCPs themselves are run safely. Efforts to set heightened expectations for CCPs and other financial market infrastructures have been ongoing for years, with the regulatory community working collectively to clarify and significantly raise expectations. These efforts resulted in the Principles for Financial Market Infrastructures (or PFMI), which was published in 2012 by the Committee on Payments and Market Infrastructures (CPMI) and the International Organization of Securities Commissions (IOSCO). The PFMI lays out comprehensive expectations for CCPs and other financial market infrastructures.

Recent Accomplishments

Extensive work has been done to implement the PFMI.2 The joint CCP work plan agreed to in 2015 by the Financial Stability Board (or FSB), CPMI, IOSCO, and the Basel Committee on Banking Supervision (or BCBS) laid out an ambitious program to provide further guidance on the PFMI and better understand interdependencies between CCPs and their members.3

CPMI and IOSCO will soon publish more granular guidance on CCP resilience, focusing on governance, stress testing credit and liquidity risk, margin, and recovery planning. While this guidance will not establish new standards beyond those set out in the PFMI, I believe that it will encourage CCPs and their regulators to engage in thoughtful dialogue on how they could further enhance their practices.

The FSB has led the work on resolution planning for CCPs, publishing draft guidance this past February. The guidance covers a range of topics, including the powers that resolution authorities need in order to effectively resolve a CCP, the potential incentives related to using various loss-allocation tools in resolution, the application of the "no creditor worse off" safeguard, and the formation of crisis management groups--a key step in facilitating cross-border regulatory coordination in the event of a failure of a systemically important CCP.

Ensuring the safety of the system also requires an understanding of the interdependencies between CCPs and their clearing members. Work on this is ongoing. Preliminary analysis confirms that there are large interdependencies between banks and CCPs, including common exposures related to financial resources held to cover market and credit risk, as well as common lending and funding arrangements.

Having pushed for the move to greater central clearing, global authorities have a responsibility to ensure that CCPs do not themselves become a point of failure for the system. The progress I have just described is helping to meet this responsibility by making central clearing safer and more robust. Global authorities also have a responsibility to ensure that bank capital standards and other policies do not unnecessarily discourage central clearing. In my view, the calibration of the enhanced supplementary leverage ratio (SLR) for the U.S. global systemically important banks (G-SIBs) should be reconsidered from this perspective. A risk-insensitive leverage ratio can be a useful backstop to risk-based capital requirements. But such a ratio can have perverse incentives if it is the binding capital requirement because it treats relatively safe activities, such as central clearing, as equivalent to the most risky activities. There are several potential approaches to addressing this issue. For example, the BCBS is currently considering a proposal that would set a G-SIB's SLR surcharge at a level that is proportional to the G-SIB's risk-based capital surcharge. Taking this approach in the U.S. context could help to reduce the cost that the largest banks face in offering clearing services to their customers.

The Federal Reserve is also considering other steps. First, we are developing an interpretation of our rules in connection with the movement of some centrally cleared derivatives to a "settled-to-market" approach. Under this approach, daily variation margin is treated as a settlement payment rather than as posting collateral. Under our capital rules, this approach reduces the need for a bank to hold capital against these exposures under risk-based and supplementary leverage ratios. Second, we are also working to move from the "current exposure method" of assessing counterparty credit risk on derivative exposures to the standardized approach for counterparty credit risk (SA-CCR). The current exposure method generally treats potential future credit exposures on derivatives as a fixed percentage of the notional amount, which ignores whether a derivative is margined and undervalues netting benefits. SA-CCR is a more risk-sensitive measurement of exposure, which would appropriately recognize the counterparty risks on derivatives, including the lower risks on most centrally cleared derivatives.

Central Clearing and Liquidity

CCPs are different from most other financial intermediaries in the sense that the CCP stands between two parties to a cleared transaction whose payment obligations exactly offset each other. A CCP faces market or credit risk only in the event that one of its members defaults and its required initial margin or other pre-funded financial resources are insufficient to cover any adverse price swings that occur during the period between the time of default and the time that the CCP is able to liquidate the defaulting party's positions.

However, like most other financial intermediaries, CCPs do face liquidity risks. Their business model is based on timely payments and the ability to quickly convert either the underlying assets being cleared or non-cash collateral into cash. For this reason, CCPs should carefully consider liquidity when launching new products and only offer clearing of products that can be sold quickly, even in times of stress. Liquidity problems can occur in central clearing even if all counterparties have the financial resources to meet their obligations, if they are unable to convert those resources into cash quickly enough. The amount of liquidity risk that CCPs face can sometimes dwarf the amount of credit or market risk they face. This is particularly true for the clearing of cash securities such as Treasuries. In that case, the securities being cleared are extremely safe and likely to rise in value in times of stress. But in contrast to most cleared derivatives, the cash payments involved are very large because counterparties exchange cash for the delivery of the security on a gross basis.

I will look at these risks from two perspectives, first in terms of the payments that CCPs must make, and then in terms of the payments they expect to receive.

Payment Flows from CCPs

In the case of a member's default, a CCP must be equipped to make the cash payments owed to non-defaulting counterparties when due. This requirement can be met as long as there is sufficient margin, mutualized resources such as the guarantee fund, or the CCP's own resources held in cash and in the required currency. But if those funds are held in securities, then the CCP will need to convert them to cash, either by entering into a repurchase agreement, or using them as collateral to draw on a line of credit. And if the CCP holds either cash or securities denominated in a currency different from the one in which payment must be made, it will need to either engage in a spot FX transaction or in an FX swap.

Principle seven of the PFMI addresses these liquidity risks, calling for all CCPs to meet a "Cover 1 standard"--that is, to hold enough liquid resources in all relevant currencies to make payments on time in the event of the default of the clearing member that would generate the largest payment obligation under a wide range of potential stress scenarios. More complex CCPs and those with a systemic presence in multiple jurisdictions are encouraged to meet a "Cover 2 standard." The PFMI also provide guidance on the resources that qualify in meeting these requirements: cash held at a central bank or a creditworthy commercial bank, committed lines of credit, committed repurchase agreements, committed FX swap agreements, or highly marketable collateral that can be converted into cash under prearranged and highly reliable funding arrangements.

There are two sets of risks involved here. First, where should CCPs put their cash? As central clearing has expanded, CCPs have had to deal with increasingly large amounts of cash margin. CCPs can deposit some of these funds with commercial banks. But regulatory changes have made it more expensive for banks to take large deposits from other financial firms, and in some cases banks may be unwilling to accept more cash from a CCP. And many of the largest banks are also clearing members, which introduces a certain amount of wrong-way risk. A clearing-member default could be especially fraught if the defaulting bank also held large cash balances for the CCP. For this reason, CCPs may prudently place limits on the amount deposited at a given institution. In order to diversify their holdings, many also place cash in the repo market. If it is available, the ability to deposit cash at a central bank allows for another safe, flexible, and potentially attractive option--a subject I will return to later.

Second, how can CCPs be assured that they will be able to convert securities into cash or draw on other resources in times of stress? The PFMI uses the words "committed" and "pre-arranged" in describing qualifying liquid resources. Indeed, the PFMI does not view spot transactions on the open market as reliable sources of liquidity during times of stress. The Federal Reserve has strongly supported this approach. Liquidity plans should not take for granted that, at a time of stress involving a member default, lines of credit, repurchase agreements, or FX swaps could be arranged on the spot. Committed sources of liquidity are more likely to be available. They also allow market participants and regulators to make sure that plans are mutually consistent. If a CCP has arranged for a committed liquidity source, then the provider should account for it in its own plans and demonstrate that it can meet its commitment.

Of course, this liquidity is not free, nor should it be. Regulatory changes have forced banks to closely examine their liquidity planning and to internalize the costs of liquidity provision. The costs of committed liquidity facilities will be passed on to clearing members. These costs are perhaps highest in clearing Treasury securities, where liquidity needs can be especially large. To meet its estimated needs, DTCC's Fixed Income Clearing Corporation (FICC) is planning to institute a committed repo arrangement with its clearing members. Despite initial concerns, the industry seems prepared to absorb these costs, but they will not be trivial for many members.4

Payment Flows to CCPs

While initial and variation margin help mitigate credit risk in central clearing, they can also create liquidity risk. Clearing members and their clients are required to make margin payments to CCPs on a daily basis, and in times of market volatility these payments may rise dramatically. This source of liquidity risk can occur even in the absence of a default. For example, after the UK referendum on Brexit, the resulting price swings triggered many CCPs to make substantial intraday and end-of-day margin calls. Fortunately, members had prepared and were able to make the needed payments, but the sums involved caught many off guard and the experience served as a useful warning.

According to data from the Commodity Futures Trading Commission (CFTC), the top five CCPs requested $27 billion in additional margin over the two days following the referendum, about five times the average amount.5 In most cases, clearing members have an hour to meet intraday margin calls. Clearing members have no choice but to hold enough liquid resources to meet the range of possible margin calls, as the consequences of missing a margin call are considerable.

Brexit was only the most recent example in which margin calls were unexpectedly large. Margin calls were also quite large after the stock market crash of October 1987. That episode helps to demonstrate how complicated payments flows can be and why liquidity risk also needs to be viewed from a macroprudential perspective, considering potential risks to flows across the system. After falling about 9 percent the week before, on October 19, 1987, the S&P 500 stock market index fell about 20 percent. Margin calls were about 10 times their normal size, and caused a very complicated set of payment flows across multiple exchanges, CCPs, and banks.6

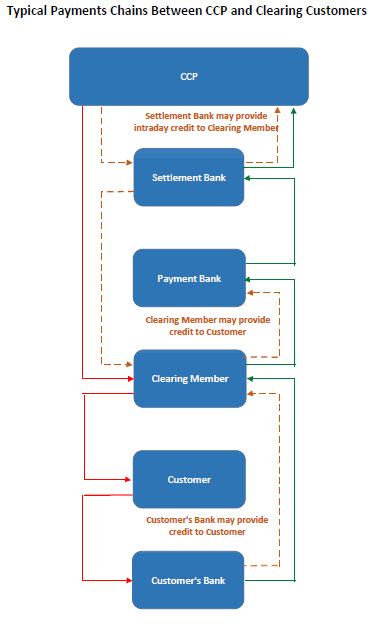

The next slide helps to represent the ensuing payment flows.7 Calls requesting payment are on the left in red. When making a margin call, a CCP requests payment from its clearing members. Clearing members in turn request margin payments from the customers for whom they are clearing, and those customers must then direct their bank to make the payment. If everything works as it should, payments (in green, on the right) will ensue. The customer's bank will deliver the requested payment to the clearing member's bank (or payment bank). The payment bank will then deliver the funds to a settlement bank used by the CCP, and the settlement bank will then credit the funds to the CCP. In theory, each of these payments would have to happen sequentially, but often parties offer intraday credit (represented by the dashed orange lines) to help smooth these flows. For example, the settlement bank may provide intraday credit to the clearing member, sending funds to the CCP before the member has delivered funds to the payment bank or before those funds have been transferred to the settlement bank. Clearing members or the customer's bank may also provide intraday credit to their customers, again making payments before funds have been received in order to help speed the payments chain.

{kind=link}

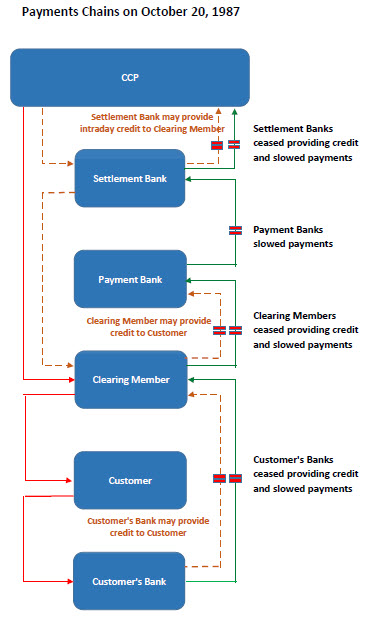

Over the course of October 19, 1987, the system worked largely as I have just described. But on October 20, every single link in these payments and credit chains was interrupted. This is represented graphically in the next slide. By that morning, many settlement banks and clearing members had yet to receive offsetting payments for credit that had been extended the previous day. Goldman Sachs and Kidder, Peabody had together extended $1.5 billion in credit that had not yet been paid.8 As a result, some firms pulled back on providing further credit, which then forced each link of the payments chain to operate sequentially. Payments slowed, with the unintended consequence that uncovered positions grew larger and stayed open for even longer. Without credit, some customers were unable to meet their margin calls and were forced to liquidate their positions. This gridlock sparked fears that a clearing member or even a CCP would be forced to default. The Federal Reserve reacted to this threat by encouraging banks to continue to extend credit and by injecting funds into the system to help ensure that credit was available. The 1987 stock market crash did not leave much lasting impact on the economy, but if these liquidity problems had been allowed to cause the default of a major clearing member or even a CCP then it could have had a much more serious impact. While this might seem like simply an interesting bit of history, the payments chains involved in central clearing are still very similar today. To guard against the same sorts of liquidity risk today, we need to make sure that every link in these chains will work as it is intended to under stress.

{kind=link}

While neither Brexit nor the October 1987 crash involved a clearing member default, these incidents do point to the potential complications of such a default. I have already discussed the steps that a CCP might need to take in the event of a default to meet its liquidity needs. Some of those needs, such as committed lines of credit or repo agreements, could involve tapping financial resources at the same banks that are clearing members. Thus, clearing members may need to juggle several different liquidity exposures simultaneously in the event of a default. They may face draws on committed sources of liquidity, and if there are market stresses around the default, which seems a near certainty, they may at the same time face a sudden increase in intraday margin calls and their own internal demands for more liquid resources.9 These are risks that we should seek to understand better.

Policy Implications

The Federal Reserve is the primary supervisory authority for two designated financial market utilities (or DFMUs), and plays a secondary role relative to the six other DFMUs. As a central bank, we are particularly concerned with liquidity issues.10 I will address four policy issues that need careful consideration as the public sector and market participants continue to address liquidity risks in central clearing.

Stress Testing

The 1987 stock market crash showed that we need to look at liquidity risks from a systemwide perspective. That event involved multiple CCPs and also involved multiple links in the payments chains between banks and CCPs. Conducting supervisory stress tests on CCPs that take liquidity risks into account would help authorities better assess the resilience of the financial system. A stress test focused on cross-CCP liquidity risks could help to identify assumptions that are not mutually consistent; for example, if each CCP's plans involve liquidating Treasuries, is it realistic to believe that every CCP could do so simultaneously?

Authorities in both the United States and Europe have made progress in conducting supervisory stress tests of CCPs. In the United States, the CFTC conducted a useful set of tests of five major CCPs last year.11 The tests analyzed each individual institution's ability to withstand the credit risks emanating from the default of one or more clearing members. This was innovative and necessary work. It would be useful to build on it by adding tests that focus on liquidity risks across CCPs and their largest common clearing members. Such an exercise could focus on the robustness of the system as a whole rather than individual CCPs. The European Securities and Markets Authority is already expanding its supervisory stress testing exercise to incorporate liquidity risk. A similar exercise here in the United States should be seriously considered.

Ensuring Efficiency

The industry collectively needs to ensure that the liquidity flows involved in central clearing are handled efficiently and in a way that minimizes potential disruption. As I noted, there was some concern about the size of margin calls following Brexit, and certain CCPs have taken measures to address this. For example, LCH has subsequently made changes to its intraday margining procedures in an effort to reduce liquidity pressures on its clearing members, allowing them to offset losses on their client accounts with gains on the house account.12

Other CCPs are also actively engaged in efforts to increase their efficiency.FICC is looking at potential solutions using distributed ledger technology to clear both legs of overnight repo trades, which could allow for greater netting opportunities and thereby reduce potential liquidity needs.13 Several CCPs are also looking at ways to expand central clearing to directly include more buy-side firms, which could also offer greater netting opportunities. Doing so could also offer new sources of liquidity if the new entrants are able to take part in the CCP's committed liquidity arrangements. Diversification of sources of liquidity would offer tangible benefits--CCPs would avoid relying on the same limited set of clearing members for all of their liquidity needs. As one example, the Options Clearing Corporation established an innovative pre-funded, committed repurchase facility with a leading pension fund.

As regulators, we should encourage innovations that increase clearing efficiency and reduce liquidity risks where they meet the PFMI and our supervisory expectations.

Central Bank Accounts

As I discussed earlier, CCPs have a complicated set of decisions on how and where to hold their cash balances. Title VIII of the Dodd-Frank Act authorized the Federal Reserve to establish accounts for DFMUs, and we now have accounts with each of the eight institutions that the Financial Stability Oversight Council has so designated. These accounts permit DFMUs to hold funds at the Federal Reserve, but not to borrow from it.14 Allowing DFMUs to deposit balances at the Federal Reserve helps them avoid some of the risk involved in holding balances with their clearing members. Doing so also provides CCPs with a flexible way to hold balances on days when margin payments unexpectedly spike and it is difficult to find banks that are willing to accept an unexpected influx in deposits. In such a case, it may also be too late in the day to rely on the repo market. The availability of Fed accounts could help avoid potential market disruptions in those types of circumstances.

Cross-Border Cooperation

The lessons from Brexit also point to the need for cross-border cooperation. Brexit triggered payments flows to CCPs across many jurisdictions. As far as liquidity risks are concerned, it is immaterial whether a CCP is based in the United States or abroad so long as it clears U.S. dollar denominated assets and must make and receive U.S. dollar payments. There are different possible approaches to such cross-border issues. Efforts to address these liquidity risks should carefully take into consideration the effect that they would have on the broader financial system. For example, splintering central clearing by currency area would fragment liquidity and reduce netting opportunities, which in the case of events like Brexit could actually trigger even greater liquidity risk. In my opinion, we should be searching for cooperative solutions to these issues.

Conclusion

In the years following the financial crisis, one of the primary lessons for market participants and their regulators was the criticality of liquidity risk management. Financial firms such as Lehman Brothers and AIG struggled to obtain sufficient liquidity to meet their obligations. Liquidity is also a crucial concern in central clearing, and while regulatory reforms have done much to strengthen both CCPs and their clearing members, we should continue to make progress in creating a more robust and efficient system.

1. The views I express here are my own and not necessarily those of others at the Federal Reserve. Return to text

2. In 2013, CPMI-IOSCO launched a multi-level, multi-year monitoring program to evaluate how the principles and responsibilities in the PFMI are being implemented around the world. Several different assessments have been completed to date and the findings have provided important insight on both the progress and methods by which authorities and CCPs have sought to implement the PFMI. In 2014, CPMI-IOSCO published supplemental guidance and a menu of recovery tools to help financial market infrastructures, including CCPs, meet the expectations in the PFMI that all financial market infrastructures have a comprehensive and effective recovery plan. Return to text

3. While the work done in the context of the joint work plan represents significant regulatory efforts related to CCPs, progress is also being made on a parallel path. In particular, it is important to highlight the adoption and implementation of the SEC's Covered Clearing Agency Standards, which further strengthens the risk management standards that clearing agencies registered with the SEC must meet. In addition, the SEC and the industry have been working jointly to shorten the settlement cycle to two days for many securities products, culminating in the SEC's adoption of amendments to Rule 15c6-1(a) earlier this year. Return to text

4. "Treasury repos may hit 20bp under DTCC liquidity plan," Risk.net, November 25, 2015. Return to text

5. "Derivatives traders forced to provide $27bn collateral post-Brexit," Financial Times, November 16, 2016. Return to text

6. Cash equities were traded in New York on the New York Stock Exchange, equity futures were traded and cleared in Chicago by the Chicago Mercantile Exchange, while stock options were traded on the Chicago Board Options Exchange and cleared by the Options Clearing Corporation. Return to text

7. This figure is an adaptation from one presented in Andrew Brimmer (1989), "Central Banking and Systemic Risks in Capital Markets," Journal of Economic Perspectives, Spring, 3–16. Return to text

8. "The Day the Nation's Cash Pipeline Almost Ran Dry," The New York Times, October 2, 1988. Return to text

9. Regulatory changes since the financial crisis have encouraged banks to hold much greater amounts of high-quality liquid assets, which would help them in meeting such liquidity demands. Return to text

10. Section 804 of the Dodd-Frank Act requires the Financial Stability Oversight Council to designate those financial market utilities that the council determines are, or are likely to become, systemically important. Eight utilities have been designated: The Clearing House Payments Company, L.L.C.; CLS Bank International; Chicago Mercantile Exchange, Inc.; The Depository Trust Company; Fixed Income Clearing Corporation; ICE Clear Credit L.L.C.; National Securities Clearing Corporation; and The Options Clearing Corporation. Return to text

11. "Supervisory Stress Test of Clearinghouses (PDF)," Commodity Futures Trading Commission, November 2016. Return to text

12. LCH has also moved forward by one hour the timing of the last intraday margin call and made procedural changes that will speed up the processing of the call, which should also help with payment flows. Return to text

13. "DTCC & Digital Asset Move to Next Phase after Successful Proof-Of-Concept for Repo Transactions Using Distributed Ledger Technology," DTCC, February 2017. Return to text

14. According to title VIII of the Dodd-Frank Act, a designated financial market utility may only borrow from the discount window only in unusual and exigent circumstances and only upon a majority vote of the Board of Governors following consultation with the Secretary of the Treasury. Return to text