March 08, 2019

Monetary Policy: Normalization and the Road Ahead

At the 2019 SIEPR Economic Summit, Stanford Institute of Economic Policy Research, Stanford, California

Thank you for the opportunity to speak here today at the Stanford Institute for Economic Policy Research, a place dedicated to scholarship supporting policies to better peoples' lives. As today is International Women's Day, I would like to preface my remarks by commending the American Economic Association for highlighting the diversity challenges of the economics profession and charting a way forward. Diversity is also a priority at the Fed: I want the Fed to be known within the economics profession as a great place for women, minorities, and others of diverse backgrounds to be respected, listened to, and happy.

Just over 10 years ago, the Federal Open Market Committee (FOMC, or the Committee) lowered the federal funds rate close to zero, which we refer to as the effective lower bound, or ELB. Unable to lower rates further, the Committee turned to two novel tools to promote the recovery. The first was forward guidance, which is communication about the future path of interest rates. The second was large-scale purchases of longer-term securities, which became known as quantitative easing, or QE. There is a range of views, but most studies have found that these tools provided significant support for the recovery. From the outset, the Committee viewed them as extraordinary measures to be unwound, or "normalized," when conditions ultimately warranted.

Today I will explore some important features of normalization and then turn to what comes after. In some ways, we are returning to the pre-crisis normal. In other ways, things will be different. The world has moved on in the last decade, and attempting to re-create the past would be neither practical nor wise. As normalization moves into its later stages, my colleagues and I also believe that this is an important moment to take stock of issues raised by the remarkable experiences of the past decade. We are therefore conducting a review of the Fed's monetary policy strategy, tools, and communications practices. I will conclude with some thoughts on the review.

Balance Sheet Normalization

Between December 2008 and October 2014, the Federal Reserve purchased $3.7 trillion in longer-term Treasury and agency securities in order to support the economy both by easing dislocations in market functioning and by driving down longer-term interest rates. Consistent with the Committee's long-stated intention, in October 2017 we started the process of balance sheet normalization. We began gradually reducing the reinvestment of payments received as assets matured or were prepaid, allowing our holdings to shrink. The process of reducing the size of the portfolio is now well along.

To frame the discussion of the final stages of normalization of the size of the balance sheet, it is useful to consider what the phrase "normal balance sheet" meant in the decades before the crisis. During that period, the main monetary policy decision for the FOMC was choosing a target value for the federal funds rate. Subject to that choice, the Fed allowed the demand for its liabilities to determine the size of the balance sheet. This is a feature of "normal" that we are returning to: After normalization, the size of the Fed's balance sheet will once again be driven by the demand for our liabilities.

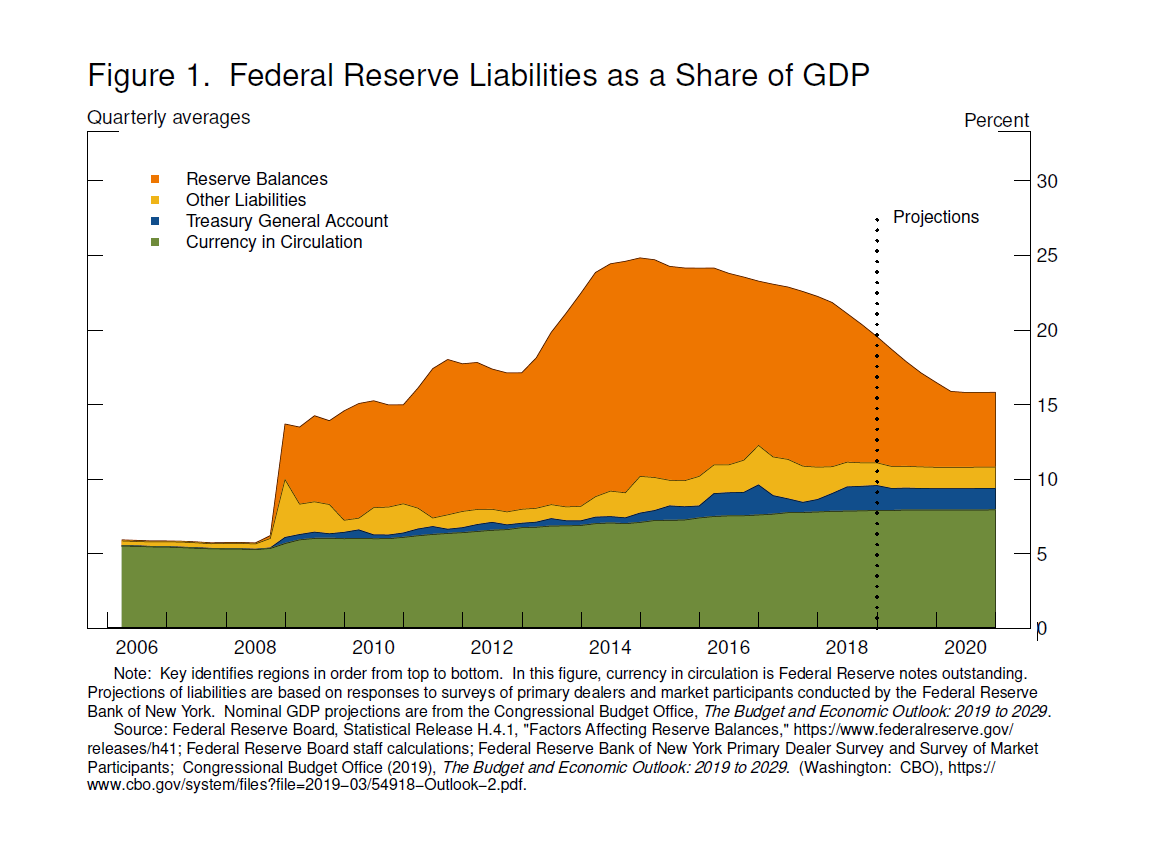

To see what this means, consider figure 1, which shows the size of the Fed's balance sheet through time, as measured by total liabilities. The values are stated as a percentage of the dollar value of GDP, or gross domestic product.1 Liabilities began to grow sharply at the end of 2008 and continued to increase until the end of 2014. Since that time, liabilities relative to GDP have fallen appreciably. To understand these changes, it is useful to focus on a snapshot of the balance sheet at three points in time: before the crisis, when the balance sheet was at its largest, and a rough projection for the end of this year (table 1).

{kind=link}

{kind=link}

In 2006, the dominant liability was currency held by the public, and the dominant asset was Treasury securities. The Fed's asset purchase programs increased the balance sheet from just below 6 percent to nearly 25 percent of GDP by the end of 2014.2 Balance sheets must balance, of course, and the Fed issued reserves as payment for the assets purchased. This action pushed reserves to nearly 15 percent of GDP.

The Committee has long said that the size of the balance sheet will be considered normalized when the balance sheet is once again at the smallest level consistent with conducting monetary policy efficiently and effectively. Just how large that will be is uncertain, because we do not yet have a clear sense of the normal level of demand for our liabilities. Current estimates suggest, however, that something in the ballpark of the 2019:Q4 projected values may be the new normal. The normalized balance sheet may be smaller or larger than that estimate and will grow gradually over time as demand for currency rises with the economy. In all plausible cases, the balance sheet will be considerably larger than before the crisis.

To understand the differences between the new and old normal, consider the final column in the table, which shows the change, measured in percentage points of GDP, between 2006:Q4 and the 2019:Q4 projection in the table. In this estimate, relative to before the crisis, the balance sheet will have grown as a share of GDP by about 10.6 percentage points. Bank reserves account for the biggest part of the growth, or about 5.6 percent of GDP. The crisis revealed that banks, especially the largest and most complex, faced much more liquidity risk than had previously been thought. Because of both new liquidity regulations and improved management, banks now hold much higher levels of high-quality liquid assets than before the crisis. Many banks choose to hold reserves as an important part of their strong liquidity positions.

The rest of the increase in liabilities is accounted for by three other categories. First, public currency holdings will have grown by 2.4 percentage points as a share of GDP. Second, the U.S. Treasury maintains an account at the Fed, which has been running 1.4 percentage points higher as a share of GDP. And, third, other liabilities, which are mainly associated with the mechanics of the national and international financial system, will have grown by 1.1 percentage points.

As was the case before the crisis, the FOMC's chosen operating regime for controlling short-term interest rates also plays a role in determining the appropriate quantity of reserves. In January, the Committee stated its intention to continue in our current regime in which our main policy rate, the federal funds rate or possibly some successor, is held within its target range by the interest rates we set on reserves and on the overnight reverse repo facility.3 In this system, active management of the supply of reserves is not required. Thus, the supply of reserves must be "ample," in the sense of being sufficient to satisfy reserve demands even in the face of volatility in factors affecting the reserve market.4 Put another way, the quantity of reserves will equal the typical reserve demands of depositories plus a buffer to allow for reserve market fluctuations.

While the precise level of reserves that will prove ample is uncertain, standard projections, such as those in the table, suggest we could be near that level later this year. As we feel our way cautiously to this goal, we will move transparently and predictably in order to minimize needless market disruption and risks to our dual-mandate objectives. The Committee is now well along in our discussions of a plan to conclude balance sheet runoff later this year. Once balance sheet runoff ends, we may, if appropriate, hold the size of the balance sheet constant for a time to allow reserves to very gradually decline to the desired level as other liabilities, such as currency, increase. We expect to announce further details of this plan reasonably soon.

There is no real precedent for the balance sheet normalization process, and we have adapted our approach along the way. In these final phases, we will adjust the details of our normalization plans if economic and financial conditions warrant. After decisions regarding the size of the balance sheet have been made, we will turn to remaining issues, such as the ultimate maturity composition of the portfolio. The Committee has long stated that it intends to return to a portfolio consisting primarily of Treasury securities.

Forward Guidance and the Normalization of Policy Communication

The Committee has also been normalizing communication about our policy after a decade of forward guidance. Since December 2008, the FOMC's postmeeting statement had contained ever-evolving forms of guidance about keeping the federal funds rate at the ELB or about the gradual pace at which that rate would return to more normal levels. We removed the last elements of this crisis-era guidance in January.5 The federal funds rate is now within the broad range of estimates of the neutral rate--the interest rate that tends neither to stimulate nor to restrain the economy. Committee participants generally agree that this policy stance is appropriate to promote our dual mandate of maximum employment and price stability. Future adjustments will depend on what incoming data tell us about the baseline outlook and risks to that outlook.

Policy communication will not simply revert to the ways of the early 2000s, however, for transparency advances have continued apace since then. The most significant change from the standpoint of forward guidance is that, since January 2012, the FOMC's quarterly Summary of Economic Projections (SEP) has included federal funds rate projections reaching up to three years into the future--often referred to as the "dot plot." Returning to a world of little or no explicit forward guidance in the FOMC's postmeeting statement presents a challenge, for the dot plot has, on occasion, been a source of confusion. Until now, forward guidance in the statement has been a main tool for communicating committee intentions and minimizing that confusion.

For example, in early 2014, the Committee's intentions were at odds with a common misreading of the dots, and Chair Yellen explained, "[O]ne should not look to the dot plot, so to speak, as the primary way in which the Committee wants to or is speaking about policy to the public at large. The FOMC statement is the device that the Committee as a policymaking group uses to express its opinions . . . about the likely path of rates."6 If the Committee remains largely out of the business of explicit forward guidance, we will need to find other ways to address the collateral confusion that sometimes surrounds the dots.

As readers of the FOMC minutes will know, at our last meeting in January there was an impromptu discussion among some participants of general concerns about the dots. My own view is that, if properly understood, the dot plot can be a constructive element of comprehensive policy communication. Let me follow my two predecessors as Chair in attempting to advance that proper understanding.

Each participant's dots reflect that participant's view of the policy that would be appropriate in the scenario that he or she sees as most likely. As someone who has filled out an SEP projection 27 times over the last seven years, I can say that there are times when I feel that something like the "most likely" scenario I write down is, indeed, reasonably likely to happen. At other times, when uncertainty around the outlook is unusually high, I dutifully write down what I see as the appropriate funds rate path in the most likely scenario, but I do so aware that this projection may be easily misinterpreted, for what is "most likely" may not be particularly likely. Very different scenarios may be similarly likely. Further, at times downside risks may deserve significant weight in policy deliberations. In short, as Chairman Bernanke explained, the SEP projections are merely "inputs" to policy that do not convey "the risks, the uncertainties, all the things that inform our collective judgment."7

Effectively conveying our views about risks and their role in policy projections can be challenging at times, and we are always looking for ways to improve our communications. I have asked the communications subcommittee of the FOMC to explore ways in which we can more effectively communicate about the role of the rate projections. For now, let me leave you with a cautionary tale about focusing too much on dots. Here is a picture composed of different colored dots (figure 2). The meaning of it is not clear, although if you stare at it long enough you might see a pattern. But let's take a step back (figure 3). As you can see, if you are too focused on a few dots, you may miss the larger picture.

{kind=link}

{kind=link}

Delivering on the FOMC's intention to ultimately normalize policy continues to be a major priority at the Fed. Normalization is far along, and, considering the unprecedented nature of the exercise, it is proceeding smoothly. I am confident that we can effectively manage the remaining stages.

Beyond Normalization

We live in a time of intense scrutiny and declining trust in public institutions around the world. At the Fed, we are committed to working hard to build and sustain the public's trust. The Fed has special responsibilities in this regard. Our monetary policy independence allows us to serve the public without regard to short-term political considerations, which, as history has shown, is critical for sound monetary policymaking. But that precious grant of independence brings with it a special obligation to be open and transparent, welcoming scrutiny by the public and their elected representatives in Congress. Only in this way can the Fed maintain its legitimacy in our democratic system.

Among other initiatives, my colleagues and I on the FOMC are undertaking a year-long review of the Federal Reserve's monetary policy strategy, tools, and communication practices. The review will involve a series of "Fed Listens" events around the country. These will include town-hall-style meetings and a conference where academic and nonacademic experts will share their views. These events will inform staff work and FOMC discussions as we plan for the future. While this is the first time the Fed has opened itself up in this way, many central banks around the world have conducted similar reviews, and our approach builds on their experiences.

We believe that our existing framework for conducting monetary policy has generally served the public well, and the review may or may not produce major changes. Consistent with the experience of other central banks with these reviews, the process is more likely to produce evolution rather than revolution. We seek no changes in law and we are not considering fundamental changes in the structure of the Fed, or in the 2 percent inflation objective. While there is a high bar for adopting fundamental change, it simply seems like good institutional practice to engage broadly with the public as part of a comprehensive approach to enhanced transparency and accountability.

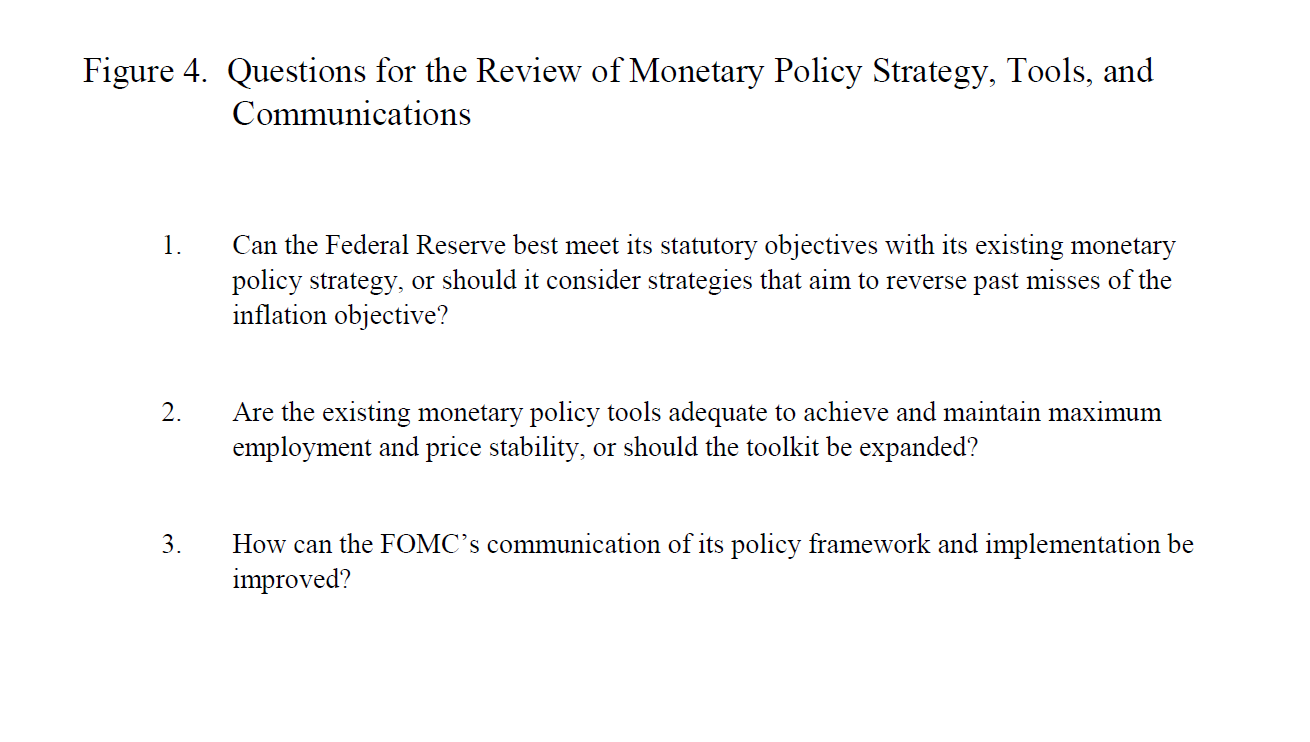

Without ruling out other topics, we have highlighted three questions that seem particularly important at present (figure 4):

{kind=link}

1. Can the Federal Reserve best meet its statutory objectives with its existing monetary policy strategy, or should it consider strategies that aim to reverse past misses of the inflation objective?

2. Are the existing monetary policy tools adequate to achieve and maintain maximum employment and price stability, or should the toolkit be expanded?

3. How can the FOMC's communication of its policy framework and implementation be improved?

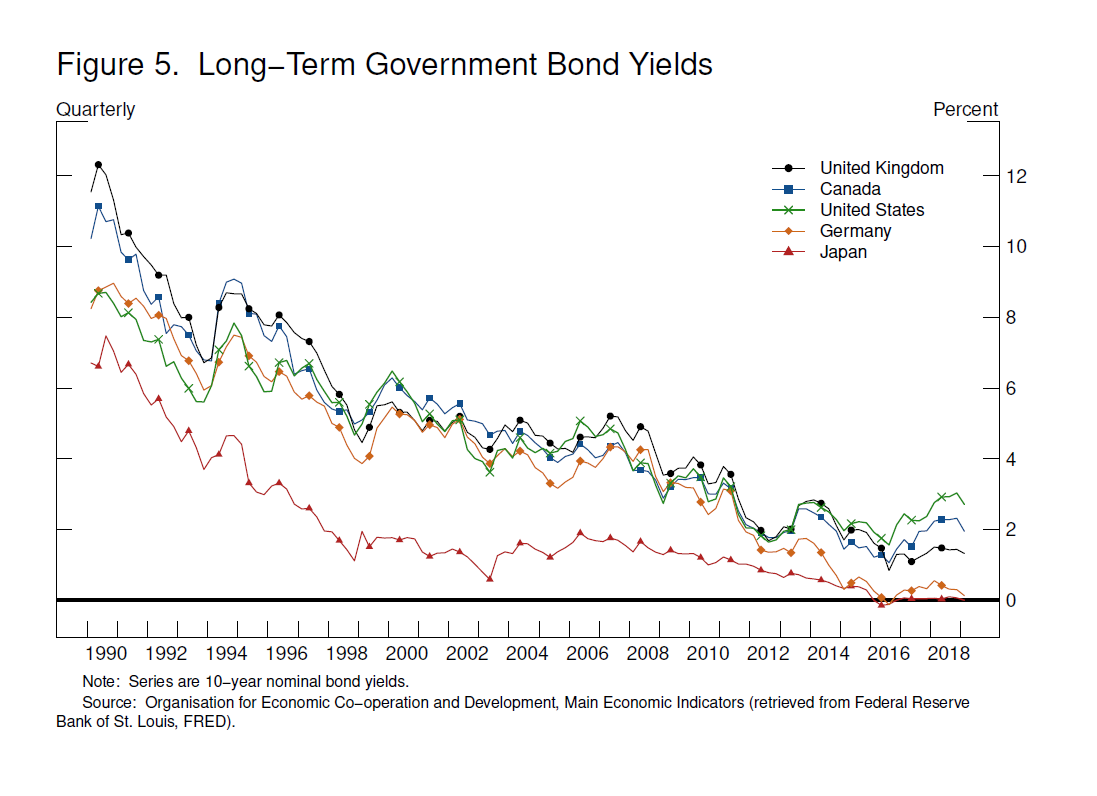

I would like to spend a few minutes discussing the first topic. Because interest rates around the world have steadily declined for several decades, rates in normal times now tend to be much closer to zero than in the past (figure 5).8 Thus, when a recession comes, the Fed is likely to have less capacity to cut interest rates to stimulate the economy than in the past, suggesting that trips to the ELB may be more frequent. The post-crisis period has seen many economies around the world stuck for an extended period at the ELB, with slow growth and inflation well below target. Persistently weak inflation could lead inflation expectations to drift downward, which would imply still lower interest rates, leaving even less room for central banks to cut interest rates to support the economy during a downturn. It is therefore very important for central banks to find more effective ways to battle the low-inflation syndrome that seems to accompany proximity to the ELB.

{kind=link}

In the late 1990s, motivated by the Japanese experience with deflation and sluggish economic performance, economists began developing the argument that a central bank might substantially reduce the economic costs of ELB spells by adopting a makeup strategy.9 The simplest version goes like this: If a spell with interest rates near the ELB leads to a persistent shortfall of inflation relative to the central bank's goal, once the ELB spell ends, the central bank would deliberately make up for the lost inflation by stimulating the economy and temporarily pushing inflation modestly above the target. In standard macroeconomic models, if households and businesses are confident that this future inflationary stimulus will be coming, that prospect will promote anticipatory consumption and investment. This can substantially reduce the economic costs of ELB spells.10 Researchers have suggested many variations on makeup strategies.11 For example, the central bank could target average inflation over time, implying that misses on either side of the target would be offset.

By the time of the crisis, there was a well-established body of model-based research suggesting that some kind of makeup policy could be beneficial.12 In light of this research, one might ask why the Fed and other major central banks chose not to pursue such a policy.13 The answer lies in the uncertain distance between models and reality. For makeup strategies to achieve their stabilizing benefits, households and businesses must be quite confident that the "makeup stimulus" is really coming. This confidence is what prompts them to raise spending and investment in the midst of a downturn. In models, confidence in the policy is merely an assumption. In practice, when policymakers considered these policies in the wake of the crisis, they had major questions about whether a central bank's promise of good times to come would have moved the hearts, minds, and pocketbooks of the public. Part of the problem is that when the time comes to deliver the inflationary stimulus, that policy is likely to be unpopular--what is known as the time consistency problem in economics.14

Experience in the United States and around the world suggests that more frequent ELB episodes could prove quite costly in the future. My FOMC colleagues and I believe that we have a responsibility to the American people to consider policies that might promote significantly better economic outcomes. Makeup strategies are probably the most prominent idea and deserve serious attention. They are largely untried, however, and we have reason to question how they would perform in practice. Before they could be successfully implemented, there would have to be widespread societal understanding and acceptance--as I suggested, a high bar for any fundamental change. In this review, we seek to start a discussion about makeup strategies and other policies that might broadly benefit the American people.

Conclusion

Tonight I have focused on policy normalization and our efforts to engage the public in what may come after. Before concluding, I will say a few words on current conditions and the outlook.

Right now, most measures of the health and strength of the labor market look as favorable as they have in many decades. Inflation will probably run a bit below our objective for a time due to declines in energy prices, but those effects are likely to prove transitory. Core inflation, which is often a reliable indicator of where inflation is headed over time, is quite close to 2 percent. Despite this favorable picture, we have seen some cross-currents in recent months. With nothing in the outlook demanding an immediate policy response and particularly given muted inflation pressures, the Committee has adopted a patient, wait-and-see approach to considering any alteration in the stance of policy.

Considering monetary policy more broadly, we are inviting thorough public scrutiny and are hoping to foster conversation regarding how the Fed can best exercise the precious monetary policy independence we have been granted. Our goal is to enhance the public's trust in the Federal Reserve--our most valuable asset.

References

Bank of Japan (2016). "New Framework for Strengthening Monetary Easing: 'Quantitative and Qualitative Monetary Easing with Yield Curve Control' (PDF)," announcement, September 21.

Bernanke, Ben S. (2017). "Monetary Policy in a New Era," paper presented at "Rethinking Macroeconomic Policy," a conference held at the Peterson Institute of International Economics, Washington, October 12-13.

Bernanke, Ben S., Michael T. Kiley, and John M. Roberts (2019). "Monetary Policy Strategies for a Low-Rate Environment (PDF)," Finance and Economics Discussion Series 2019-009. Washington: Board of Governors of the Federal Reserve System, February.

Brand, Claus, Marcin Bielecki, and Adrian Penalver, eds. (2018). "The Natural Rate of Interest: Estimates, Drivers, and Challenges to Monetary Policy (PDF)," ECB Occasional Paper Series No. 217. Frankfurt, Germany: European Central Bank, December.

Eggertsson, Gauti B., and Michael Woodford (2003). "The Zero Bound on Interest Rates and Optimal Monetary Policy (PDF)," Brookings Papers on Economic Activity, no. 1, pp. 139-211.

English, William B., J. David López-Salido, and Robert J. Tetlow (2015). "The Federal Reserve's Framework for Monetary Policy: Recent Changes and New Questions," IMF Economic Review, vol. 63 (April), pp. 22-70.

Friedman, Milton (1969). The Optimum Quantity of Money. New York: MacMillan.

Hebden, James, and J. David López-Salido (2018). "From Taylor's Rule to Bernanke's Temporary Price Level Targeting (PDF)," Finance and Economics Discussion Series 2018-051. Washington: Board of Governors of the Federal Reserve System, July.

Holston, Kathryn, Thomas Laubach, and John C. Williams (2017). "Measuring the Natural Rate of Interest: International Trends and Determinants," Journal of International Economics, vol. 108 (May, Supplement 1), pp. S59-S75.

Kiley, Michael T., and John M. Roberts (2017), "Monetary Policy in a Low Interest Rate World (PDF)," Brookings Papers on Economic Activity, Spring, pp. 317-72.

King, Mervyn, and David Low (2014). "Measuring the 'World' Real Interest Rate (PDF)," NBER Working Paper Series 19887. Cambridge, Mass.: National Bureau of Economic Research, February.

Mertens, Thomas M., and John C. Williams (2019). Monetary Policy Frameworks and the Effective Lower Bound on Interest Rates (PDF), Staff Report 877. New York: Federal Reserve Bank of New York, January.

Nessén, Marianne, and David Vestin (2005). "Average Inflation Targeting," Journal of Money, Credit and Banking, vol. 37 (October), pp. 837-63.

Rachel, Lukasz, and Thomas D. Smith (2017). "Are Low Real Interest Rates Here to Stay?" International Journal of Central Banking, vol. 13 (September), pp. 1-42.

Reifschneider, David, and John C. Williams (2000), "Three Lessons for Monetary Policy in a Low Inflation Era," Journal of Money, Credit and Banking, vol. 32 (November), pp. 936-66.

Wolman, Alexander L. (2005). "Real Implications of the Zero Bound on Nominal Interest Rates," Journal of Money, Credit and Banking, vol. 37 (March), pp. 273‑96.

1. The balance sheet had been steady at around 5 percent of GDP since about 1980, as currency slowly grew as a share of GDP, but the increase was offset by a decline in reserves. Return to text

2. This size is similar to that of the balance sheet relative to GDP in the wake of the Great Depression. Return to text

3. As noted in the minutes of the November 2018 FOMC meeting (see https://www.federalreserve.gov/monetarypolicy/fomcminutes20181108.htm), participants discussed costs and benefits of various alternatives to the federal funds rate, such as the overnight bank funding rate, and recommended further study of the issue. Return to text

4. Both supply and demand factors can show large fluctuations. Return to text

5. Of course, "patience" as used in the January FOMC statement (see https://www.federalreserve.gov/newsevents/pressreleases/monetary20190130a.htm) might be seen as forward guidance. This type of guidance was used at times before the crisis and may play a role in the future. It is not, however, the explicit guidance about the medium-term level or direction of rates that distinguished the crisis-era guidance. Return to text

6. See page 9 of Chair Yellen's March 2014 press conference transcript, available at https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20140319.pdf. Return to text

7. See page 6 of Chairman Bernanke's April 2012 press conference transcript, available at https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20120425.pdf. Note that the SEP does provide some general information about the balance of risks, but this information is far less complete than the detail provided on the modal outlook. Return to text

8. For evidence on the secular decline in interest rates in the United States and abroad, see King and Low (2014); Holston, Laubach, and Williams (2017); Rachel and Smith (2017); and Brand, Bielecki, and Penalver (2018). Return to text

9. See Reifschneider and Williams (2000) and references therein. Return to text

10. Eggertsson and Woodford (2003), for example, show that optimal policy at the ELB entails a commitment to reflate the price level during subsequent economic expansions. See also Wolman (2005) for a discussion of the effectiveness of price-level targeting at the ELB. For a discussion of the relationship between price-level targeting and average-inflation targeting, see Nessén and Vestin (2005). Return to text

11. The strategy in Reifschneider and Williams (2000), for instance, involves a central bank following a Taylor rule modified to make up for shortfalls in policy accommodation during ELB episodes. Kiley and Roberts (2017) study a strategy in which policymakers aim for inflation higher than 2 percent during normal times to compensate for below-target inflation during ELB episodes. See also Bernanke (2017) for a strategy in which low inflation is made up if it occurs when the federal funds rate is at or near the ELB. Return to text

12. See, for example, English, López-Salido, and Tetlow (2015); Hebden and López-Salido (2018); Bernanke, Kiley, and Roberts (2019); and Mertens and Williams (2019). Return to text

13. The Bank of Japan (2016) came closest, announcing in September 2016 an "inflation-overshooting commitment" (p. 1). The commitment did not, however, come with any explicit goal for a degree or duration of overshoot. Return to text

14. Transcripts of FOMC discussions (see, for example, 2011 transcripts, available at https://www.federalreserve.gov/monetarypolicy/fomchistorical2011.htm) reveal that some policymakers were dubious about whether it would be appropriate or even feasible for a current FOMC to bind a future FOMC to a policy that it might find objectionable, which contributed to more general doubts over whether the policy would be credible. Return to text