July 19, 2018

Introductory Remarks

Vice Chairman for Supervision Randal K. Quarles

At the Alternative Reference Rates Committee Roundtable, The Federal Reserve Bank of New York, New York, New York (via prerecorded video)

Good morning. I am sorry that I cannot be with you in person for this third roundtable hosted by the Alternative Reference Rates Committee (ARRC), but I wanted to tape these remarks to make clear the Federal Reserve's full commitment to mitigating the risk to financial stability should a key reference rate cease to be available. We support the ARRC and its work. And support for the ARRC is not limited to the Federal Reserve System: the Bureau of Consumer Financial Protection, Commodity Futures Trading Commission, Federal Deposit Insurance Corporation, Federal Housing Finance Agency, Office of the Comptroller of the Currency, Office of Financial Research, Securities and Exchange Commission, and U.S. Treasury Department are all ex officio members of the ARRC.

Since many have only recently begun to pay more attention to these issues, let me remind you of our reasons for convening the ARRC four years ago. The Federal Reserve began its role in co-chairing the Financial Stability Board's working group on interest rate benchmarks and joined in international efforts to strengthen LIBOR following reports that employees at several banks sought to manipulate these rates. We have served on the ICE Benchmark Administration's (IBA's) LIBOR Oversight Committee as an observer and actively worked with IBA in developing the reforms set out in IBA's Roadmap for LIBOR. Thanks in part to this, and thanks much more to the U.K. Financial Conduct Authority's (FCA's) efforts as the regulator of LIBOR, the safeguards against that type of manipulation happening again have been greatly and appropriately tightened.

But as part of this process, we also examined data that we had begun to collect on the markets that underlie LIBOR and found that those markets had become extraordinarily thin. On most days, the banks that submit to LIBOR have been forced to rely on their own judgement and models in submitting to LIBOR rather than actual transactions. Many of them have become justifiably uncomfortable with a system that pins hundreds of trillions of dollars' worth of financial contracts to that type of judgement call.

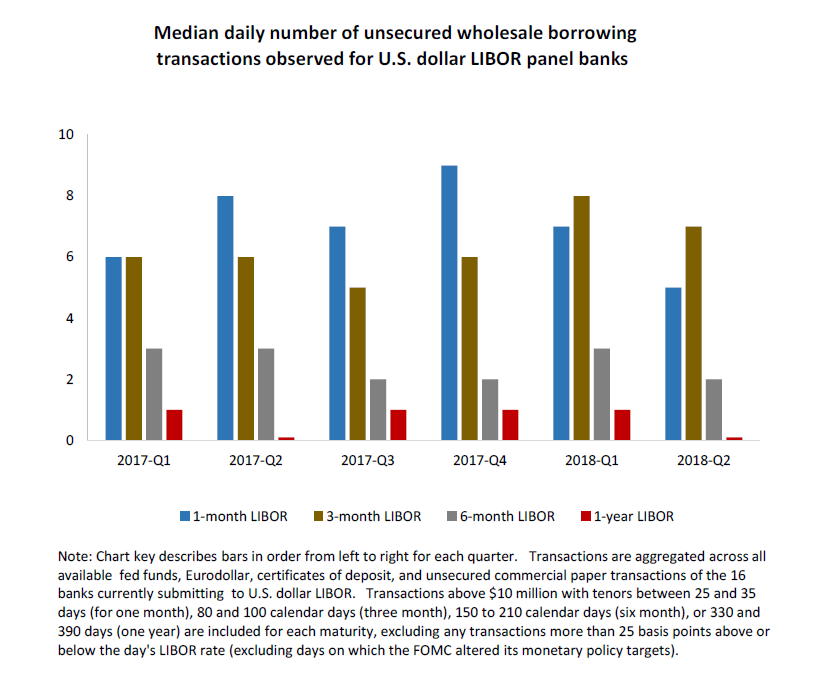

People may have some general sense of this, but because IBA does not release data on the transactions that actually underlie LIBOR, many may not be aware of how truly thin these markets have become. At the last roundtable, Jay Powell showed data on the volume of borrowing in wholesale unsecured U.S. dollar markets. That chart can be found in the ARRC's Second Report, which estimated that on a typical day the volume of three-month funding transactions was about $500 million. On many days there is much less. By way of comparison, we estimate that there are roughly $200 trillion of financial securities referencing U.S. dollar LIBOR.

To help provide some further transparency, I will show data that we have on the number of transactions involved. These data are based on the information available to the Federal Reserve, which is fairly comprehensive but still may differ in some respects from that available to IBA, so I should caution that this is merely an informed estimate of the number of transactions underlying U.S. dollar LIBOR and may not be exact. As you can see in the slide, there are a few more transactions at the shorter LIBOR maturities. On average, we observe six or seven transactions per day at market rates that could underpin one- and three-month LIBOR across all of the panel banks. The longer maturities have even fewer transactions. There are two to three transactions each day for six-month LIBOR. On average, there is only one transaction that we see underlying one-year LIBOR, and many days there are no transactions at all.

{kind=link}

The secured overnight financing rate (SOFR) has only been in existence three months, and SOFR futures have only been trading for two months, but on a daily basis there are already more transactions underlying them than there are underpinning LIBOR. And SOFR itself reflects over $700 billion in overnight repurchase agreement (repo) transactions every day. One of the many benefits of using a rate so firmly anchored in a market of this depth is that no one can question whether SOFR is representative. It clearly is.

With LIBOR reliant on expert judgment rather than direct transactions, many banks increasingly uncomfortable providing that judgment, and the official sector unable to compel them to do so indefinitely, it was obvious to us that this structure--which bases so many trillions of financial instruments on such a small number of underlying transactions--was potentially unstable. It was clear that the market needed to develop alternatives in case the worst happened, and this was the reason that we convened the ARRC four years ago.

We asked the ARRC to identify a robust alternative to U.S. dollar LIBOR and to develop a plan to promote its use. Sandie O'Connor will speak shortly about the ARRC's work, but I want to emphasize that this has been a model of cooperative effort between the private sector and the public sector. When the ARRC started, the interest rate benchmarks that they would eventually narrow their choice down to did not even exist. Those rates have not been easy to create, and as the ARRC expressed interest in a Treasury repo rate benchmark that would span the widest possible scope of the market, the Federal Reserve Bank of New York put great effort in working with the Federal Reserve Board and Office of Financial Research to create SOFR. The result, the rate the ARRC has chosen, reflects the largest and deepest rates market in the world and is a huge accomplishment for all of us.

That accomplishment is only the start of what will be many. As I noted, just three months after SOFR has begun production, we have already seen the introduction of futures markets on the Chicago Mercantile Exchange. LCH has now begun to offer clearing of SOFR overnight index and basis swaps, and CME Group will begin to do so within a few months. These are steps that the private sector must lead, and they have, but it is important that the public sector encourage the development of SOFR markets where it can. The ARRC has issued a first letter to U.S. regulators asking us to consider exemptions for legacy swaps seeking to incorporate the International Swaps and Derivatives Association's protocol or exemptions for amending to move from LIBOR to SOFR, and these are issues that we should look at seriously; we should avoid placing unintended hurdles in the way of those who may seek to transition from LIBOR.

Here is something you don't hear often in the context of any large, complex undertaking involving input from a large number of stakeholders: The effort to implement SOFR is ahead of schedule. The ARRC has recognized that we have to make transitioning to SOFR as easy as it can be. That is the reason that it has added the creation of a forward-looking term rate as the final step in its Paced Transition Plan. As the ARRC has noted and the Financial Stability Board has now reiterated, this kind of forward-looking term rate will be useful in facilitating a transition away from LIBOR in some cash markets, such as corporate loans, but it is not primarily intended for use in derivatives markets. In fact, we have to encourage use of SOFR in derivatives markets to the fullest extent possible if a robust forward-looking term rate is to be created.

For that reason, we also have to find ways to encourage uses of SOFR in those cash markets where it is appropriate. The European Investment Bank's recent announcement that it would issue a floating rate note paying a compound average of Sterling Overnight Index Average (SONIA) shows that this can be done.1 In the spirit of encouraging this type of use of SOFR, I think it is appropriate for the Federal Reserve to consider publishing a compound average of SOFR that market participants could then use. It has been suggested that we could call it SAFR, for secured average financing rate, and this is something that we are encouraging our staff to explore. Publishing a compound average rate that encourages broader use of SOFR would help make our financial system more resilient. Sandie will talk more about the creation of the forward-looking term version of SOFR in her remarks. SAFR would not be a competitor to this forward-looking rate, it would be in alliance with it. If there were a large volume of products referencing the compound average rate, there would likely be related demand for futures contracts to hedge those positions, helping to make the forward rate more robust.

It is important that we find ways to make it as easy as possible to use SOFR because the risks to LIBOR are, at this stage, quite considerable. Even as the ARRC and similar currency groups in other jurisdictions were being formed, the FCA was exerting considerable effort to convince banks to continue submitting to LIBOR. We have to be aware that two banks left the U.S. dollar panels despite this encouragement, and that the agreement that the FCA reached with the remaining banks to continue submitting voluntarily through the end of 2021 now has just three-and-a-half years left. And as Andrew Bailey noted last week, there is also the prospect that LIBOR could be judged to be nonrepresentative under the European Union's Benchmark Regulations, which would severely curtail the liquidity of products referencing LIBOR.

Apart from the questions as to whether LIBOR will continue or whether IBA or the FCA may judge that it is not representative, market participants should consider whether a rate with so few transactions underlying it is really their best option. Do we really need or want to use other tenors of LIBOR in municipal or financial floating-rate notes? For some, the answer to this may still be yes, but it is then imperative that they work to incorporate safer fallback language into their contracts as quickly as they can. This is something that the ARRC has been working on intensively this year and much of today's roundtable will discuss. But for others, the safest thing you can do would be to move away from using LIBOR. Regardless of your answer to this question, we all have a stake in the ARRC's work, both in promoting SOFR and in promoting better contract language. I want to thank you all for coming to this roundtable, and want to thank Sandie and the ARRC for all the work that has made it possible.

1. See the European Investment Bank's announcement at www.eib.org/investor_relations/press/2018/fi-2018-12-EIB%20issues%20markets%20first%20SONIA%20GBP%20benchmark%20with%20GBP%201bn%205y%20issuance.htm. Return to text