October 04, 2018

Trends in Urban and Rural Community Banks

Vice Chairman for Supervision Randal K. Quarles

At "Community Banking in the 21st Century" Sixth Annual Community Banking Research and Policy Conference, sponsored by the Federal Reserve System, the Conference of State Bank Supervisors, and the Federal Deposit Insurance Corporation, St. Louis, Missouri

Good morning. I want to thank the conference organizers for inviting me to speak to you today.1 It is an honor and a pleasure to be part of this unique annual event that brings together bankers, bank supervisors, and researchers to discuss the latest community banking research, recent trends in community banking practices, and policy issues that are on the minds of conference attendees.

I want to start, first, by conveying my own perspective on the importance of community banks. Community banks have a long history of providing essential financial services to households, small businesses, and small farms in communities across the United States. Their ability to effectively provide these services speaks to the strength of the community banking business model--that is, establishing and maintaining local relationships, and offering customers a face-to-face interaction with a local banker.

And it is something I have observed firsthand, especially for community banks in rural communities. Growing up in rural Colorado and Utah, I saw the importance of community bankers having local knowledge and being personally invested in the same communities that they serve. That local knowledge, and the relationship-based lending that is the hallmark of community banking, can stem losses during downturns, as community banks may be able to work with borrowers to avoid losses. Indeed, research has shown that small business lending at small banks declined less severely than at large banks during the last recession.2 At the same time, I have seen the challenges that many community banks face. I want to be careful not to overstate those challenges--to paraphrase Mark Twain, the reports of your demise are greatly exaggerated--and I believe that the community bank model has many advantages and will continue to play an integral role in our financial system.

These sorts of dynamics are one reason that community banks are an important topic for research. As you probably know, this is the sixth annual community banking conference cosponsored by the Federal Reserve and the Conference of State Bank Supervisors (CSBS), and it is the first conference for which the Federal Deposit Insurance Corporation is joining as a cosponsor. The organizers of the inaugural conference decided that, rather than holding a traditional academic-style conference, they would invite bankers and bank supervisors to hear what the researchers had to say and to share their real-world experience with the researchers. The hope was that these interactions would prove beneficial to all three groups. The positive feedback that we have received from conference attendees over the past five years strongly supports the wisdom of the organizers' decision.

Over time, the conference has evolved, with some new features introduced each year. The Case Study Competition, which is sponsored by the CSBS, introduces undergraduates to community banking and some of the challenges that community bankers face. The Emerging Scholars Program was also added to the conference a few years ago. This program is intended to support Ph.D. students who are considering or working on a dissertation on a banking-related topic and encourage them to develop a research agenda that focuses on community banking issues. I would like to congratulate this year's winning case study team, Eastern Kentucky University, and emerging scholars, Jiayi Xu, Cao Fang, and Flora Ma.

Not All Community Banks Are the Same

Turning to the topic of today's speech, it occurs to me that we often speak of community banks as though they are all pretty much the same. But, in reality, there is considerable heterogeneity within the group of firms that are commonly considered to be community banks.3 One important dimension of diversity is size, which can range anywhere from less than $100 million in assets to around $10 billion in assets. As noted by Chairman Powell when he spoke at this conference two years ago, looking at community banks as a monolithic group masks some important differences between the smallest and largest community banking organizations.4 For example, essentially all of the decline in the number of community banking organizations over the past two decades has taken place among those with assets less than $100 million. And these smallest banking organizations have consistently had a lower average rate of return on assets than their larger peers.

Another significant aspect of diversity among community banks is the type of market served--urban versus rural. These two types of areas differ in many respects, including the age distribution of the population, the share of the population with a college degree, homeownership rates, poverty rates, and the share of the population with internet access.5 And while the national population has been growing over the past 20 to 30 years, many rural areas have experienced population declines, and the share of the population living in rural areas has been falling.6 Furthermore, since 2008, most job growth in the United States has occurred in urban areas.7

Given these differing circumstances, it is not surprising that community banks operating in rural and urban areas tend to face different challenges. For example, the number of competitors faced by a banking organization tends to be larger in urban banking markets than in rural markets, while hiring and retaining high-quality employees can be more difficult in rural areas. And some observers have expressed concern about the implications of bank consolidation over the past two or three decades for access to banking services in rural areas while also wondering about the future viability of rural community banks.

The number of community banks has been declining over the last 20 years, but community banks still account for more than 95 percent of banks operating in the United States. The decline has been roughly similar for urban and rural community banks, leaving the share of community banks that operate primarily in rural markets quite stable at just over 50 percent. While urban community banks are quite a bit larger than rural community banks on average, over the last 20 years, rural community banks have consistently earned higher rates of return on assets and rates of return on equity than their urban peers despite a more challenging economic environment.

While the data present a compelling high-level picture, they do not tell the whole story. For example, averages across a large number of markets do not tell us what is going on in any individual market. In addition, much of the data that I am presenting today is aggregated to the county level, which obscures community-level dynamics: Some communities within a county may have lost banks or bank branches, while others may have gained. In the rural Mountain West, where I grew up, a single county can be physically larger than some Eastern states. And the demographics of the communities--for example, high- or low-income--that have lost or gained are also not visible, but important. Federal Reserve staff are engaged in efforts to further our understanding of the effects of losses of banks or bank branches on the people who live and work in the affected communities.

National Trends in Urban versus Rural Community Banks over the Past 20 Years

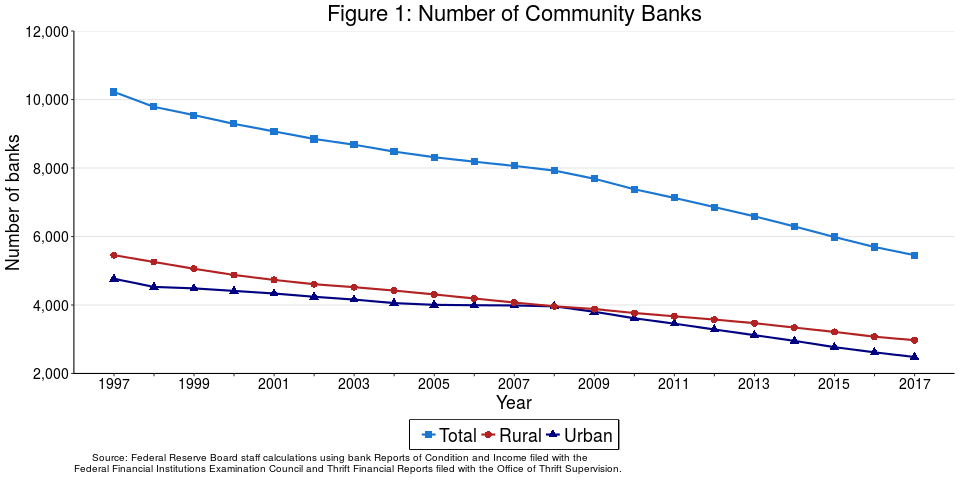

The number of banks in the United States fell by almost half over the past 20 years--from about 10,700 in 1997 to about 5,600 in 2017. About 97 percent of the decrease was accounted for by community banks. Looking at the trend in the number of urban and rural community banks (figure 1), we see that the number of banks in both of these categories has been falling over time. The rate of decline was steeper for rural banks than for urban banks before the financial crisis but has reversed in the post-crisis period. This reversal may be due to the fact that, as we will see momentarily, urban community banks suffered more severe losses in the immediate post-crisis period than did rural community banks. And the share of community banks that operate primarily in rural markets has increased slightly, from 53 percent to 54 percent.

{kind=link}

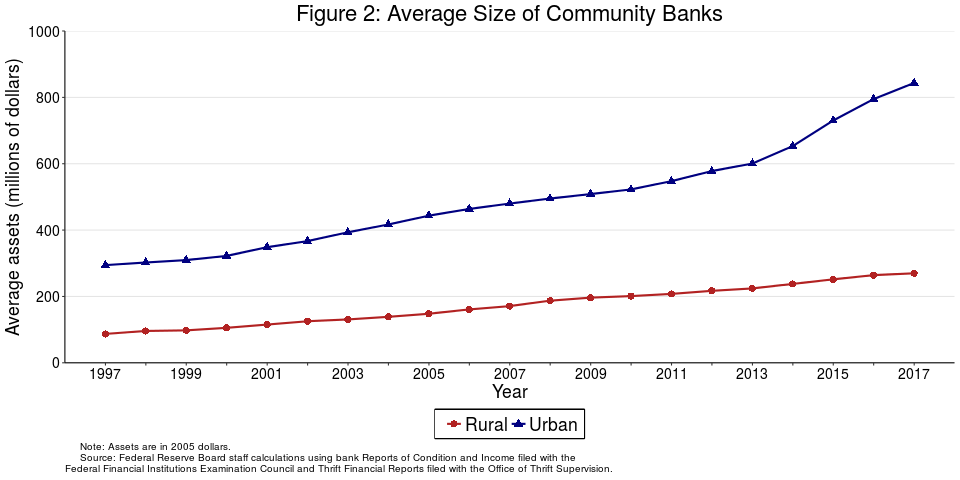

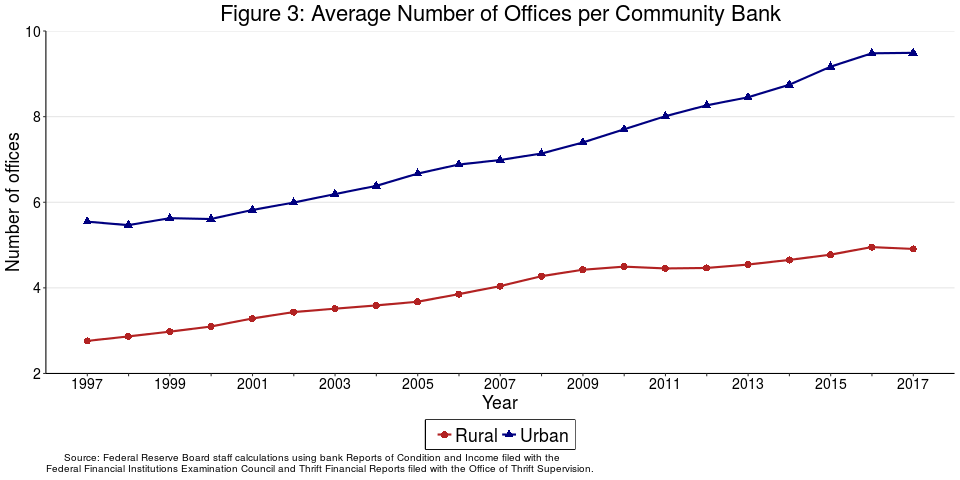

While there are more rural community banks than urban community banks, the latter consistently account for a larger volume of deposits, loans, and offices than the former. This difference is due, in part, to the average size of an urban community bank, in terms of total assets, being about two and a half to three and a half times that of the average rural community bank (figure 2). As community banks have increased in asset size, they have also grown their branch networks. The average number of branches for an urban bank is about 1.7 to 2 times that of a rural bank (figure 3).

{kind=link}

{kind=link}

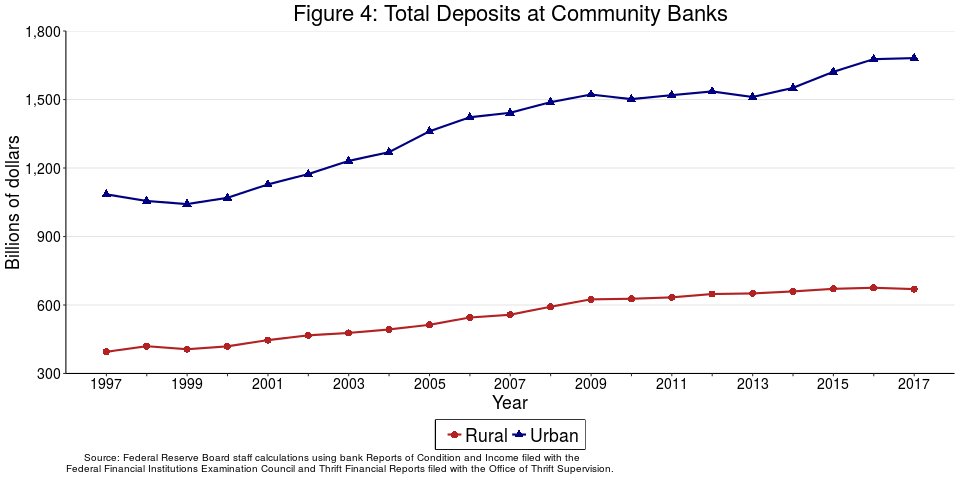

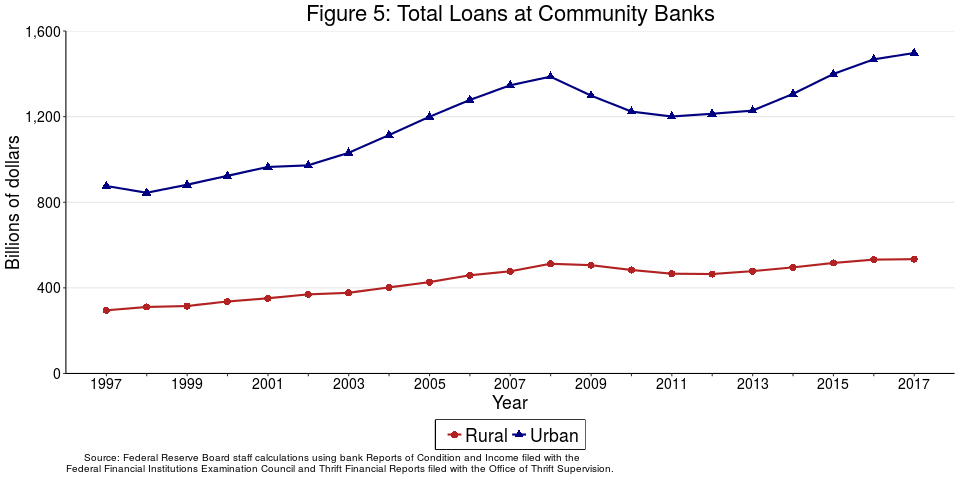

Looking next at the total amount of deposits held by all urban community banks and all rural community banks, we can see that both have been trending upward over time (figure 4). Growth in total loans outstanding was strong for both urban and rural community banks between 1997 and 2008 (figure 5). Declines in lending between 2008 and 2011 were more severe for urban community banks than rural ones. Coming out of the recent recessions, rural community banks have seen quite modest loan growth since 2011, while the pace of growth in urban community bank lending has been strong since 2013. This divergence in recent growth rates may be due to the fact that the recovery from the recent recession has been much more robust in urban areas than in rural areas of the country.

{kind=link}

{kind=link}

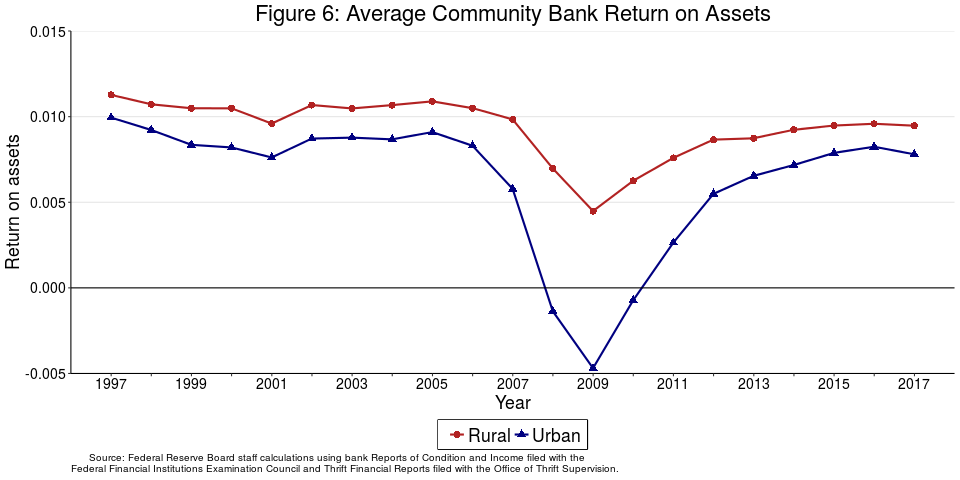

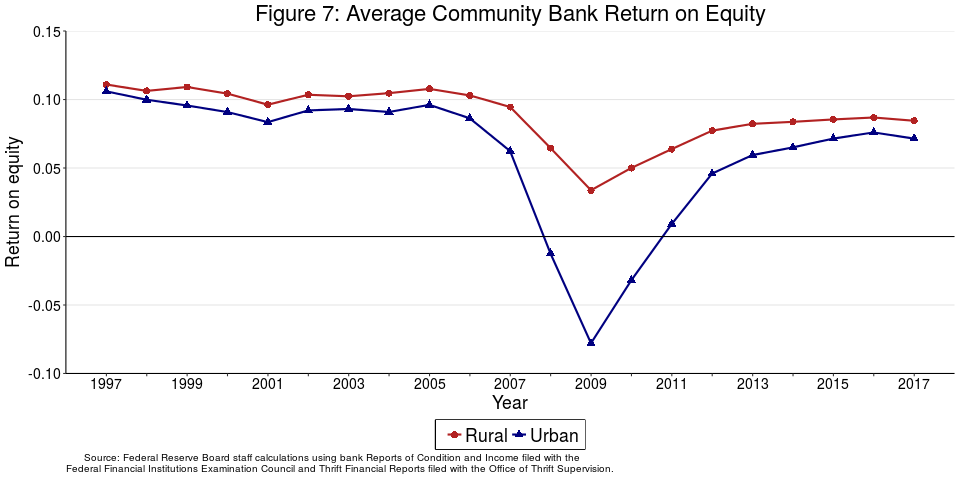

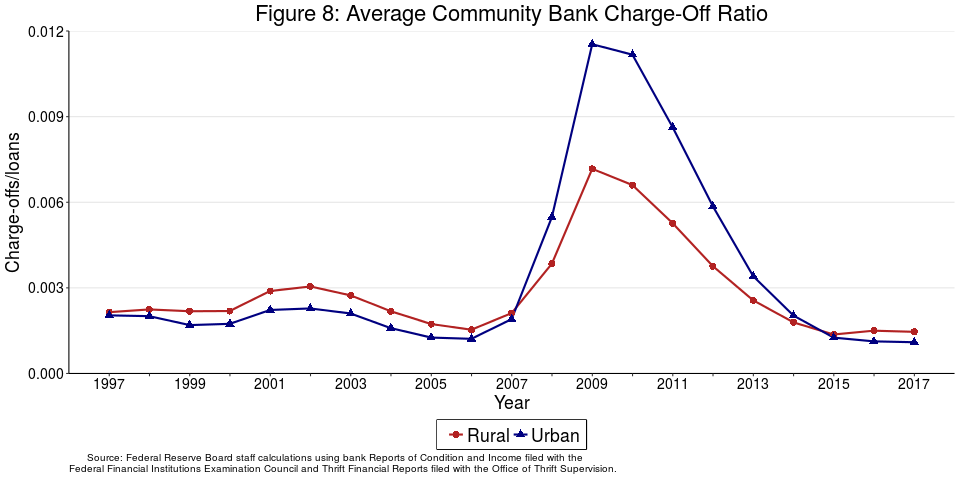

When it comes to performance measures, rural community banks consistently outperform urban community banks with regard to return on assets (figure 6) and return on equity (figure 7). This difference was particularly pronounced during the financial crisis, when profitability fell much more sharply at urban community banks than at rural community banks. Looking at charge‑off rates (figure 8), we see that they have been quite similar for the two types of community banks over most of the past 20 years, except for the period from 2008 to 2013, when rural community banks had lower charge-off rates than urban community banks.

{kind=link}

{kind=link}

{kind=link}

This data suggest that, despite facing a more challenging economic environment, rural community banks appear to be holding their own relative to urban community banks.

Market-Level Trends for All Banks and Community Banks

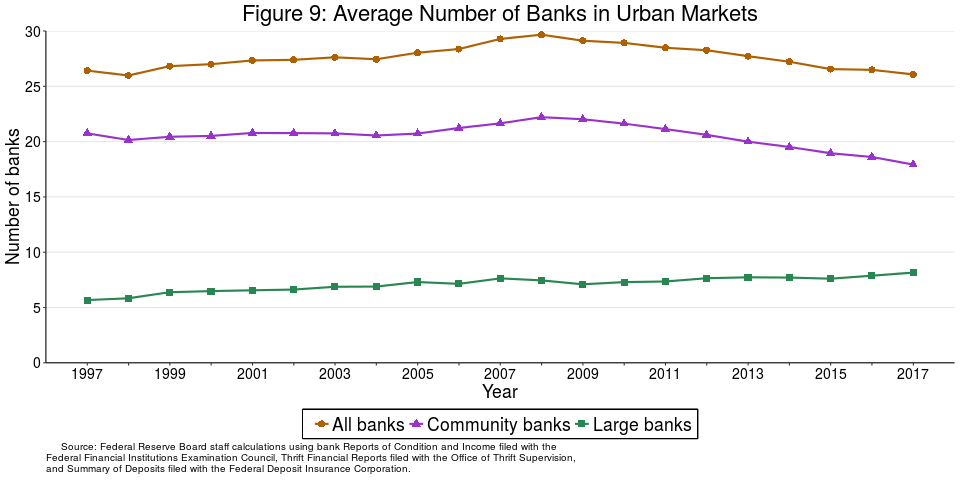

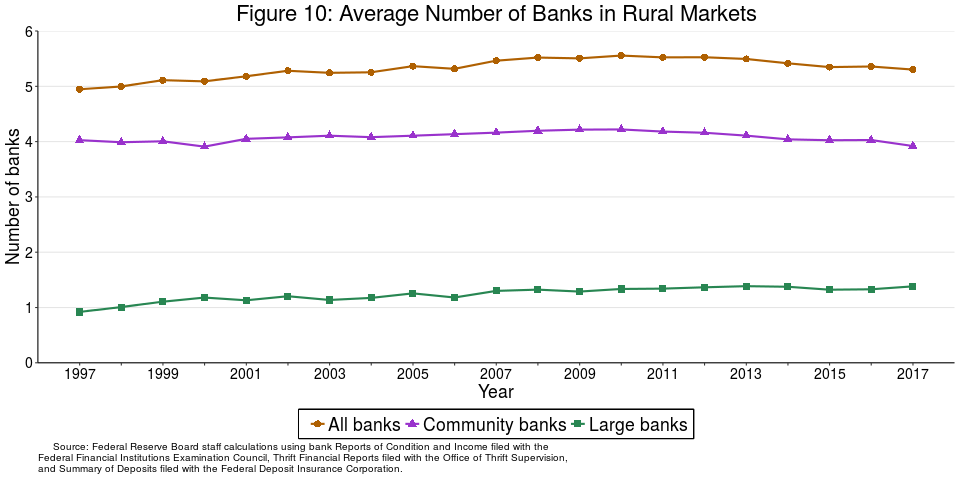

Now I would like to shift my focus from the banks themselves to the communities they serve by exploring whether access to banking services--provided by community or larger banks--has been declining in urban or rural areas of the country. As of 2017, the average urban market was home to 18 community banks and just over 8 large banks, which represents a change from 21 community banks and 6 large banks in 1997 (figure 9). The average number of community banks per rural market has been remarkably stable over the past 20 years at right around 4, while the average number of large banks per rural market has increased from just under 1 to 1.4 (figure 10). These statistics indicate that, perhaps surprisingly, the average number of banks in rural markets has actually increased in the past 20 years.

{kind=link}

{kind=link}

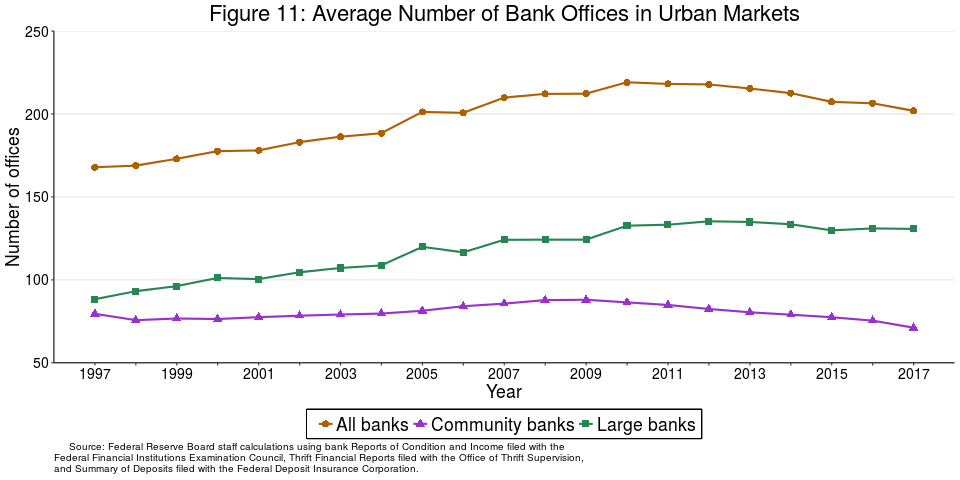

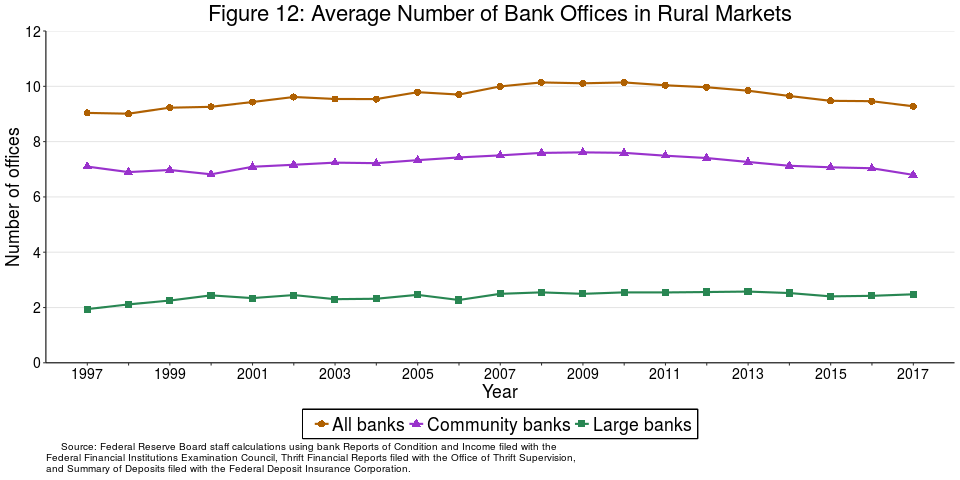

If we look at the number of bank branches rather than the number of competitors, we see a significant increase in the number of branches in the average urban market, with the entire increase coming from branches of large banks (figure 11). Over the same period, there was essentially no change in the number of branches in rural markets, with a slight shift upward in the share of branches accounted for by large banks (figure 12). Of course, there is substantial variation in the experiences of individual markets, as some local rural and urban markets gained and others lost bank branches.

{kind=link}

{kind=link}

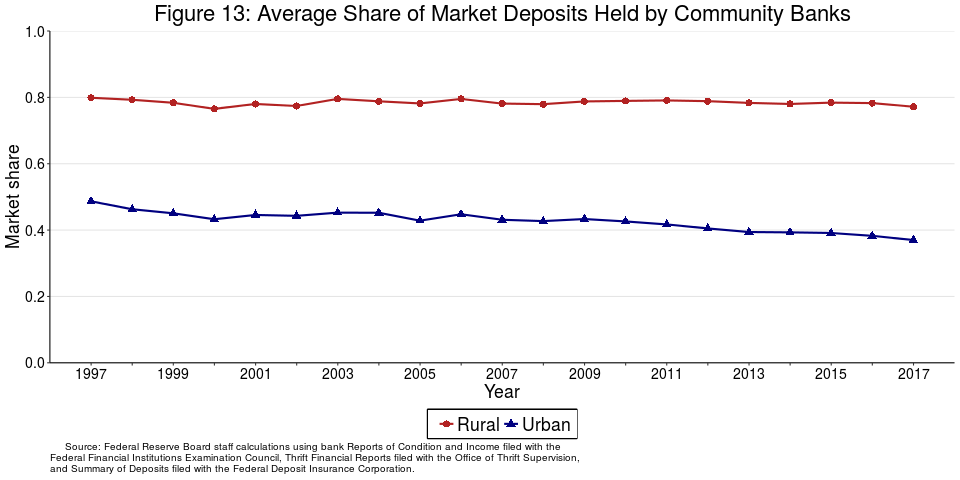

As the share of branches in the average banking market operated by community banks has declined, so, too, has the share of deposits held at community banks. This shift in deposit shares away from community banks, similar to the shift in branch shares, has been substantial in urban markets but only marginal in rural markets (figure 13). Community banks held almost half of all deposits at urban bank branches in 1997, but just over one-third in 2017. In rural markets, community banks collectively had a deposit market share of 80 percent in 1997, declining moderately to 77 percent in 2017.

{kind=link}

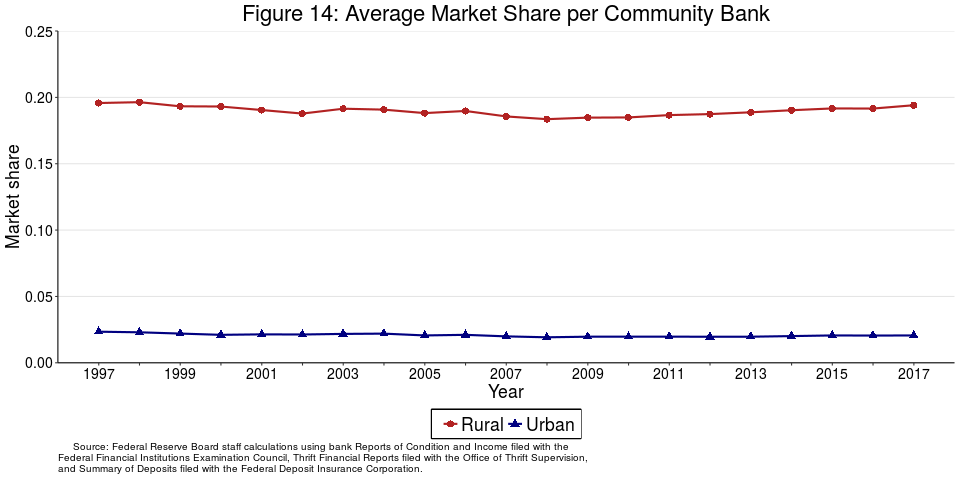

Despite the decline in the overall share of deposits held by community banks in urban and rural markets over the past 20 years, the average individual community bank operating in each type of market has seen almost no change in its deposit market share (figure 14). In other words, the decline in the share of market deposits held in aggregate by community banks is due to fewer community banks. The fact that the average individual community bank has maintained or increased its deposit market share since 2008 suggests that community banks have been able to compete quite successfully with larger banks in both urban and rural markets during and since the recent recession.

{kind=link}

Head Offices

As I have mentioned, the average numbers of banks and bank branches have increased or remained constant in rural markets in recent years despite a wave of mergers that has greatly reduced the number of U.S. banking organizations. Industry consolidation has led to fewer banks but maintained most of the branches of the acquired banks. In addition, most mergers and acquisitions have involved expansion into new markets by the acquiring bank rather than acquisitions of local competitors, which has allowed local communities to continue to enjoy a variety of potential providers of banking services despite the industry consolidation.8

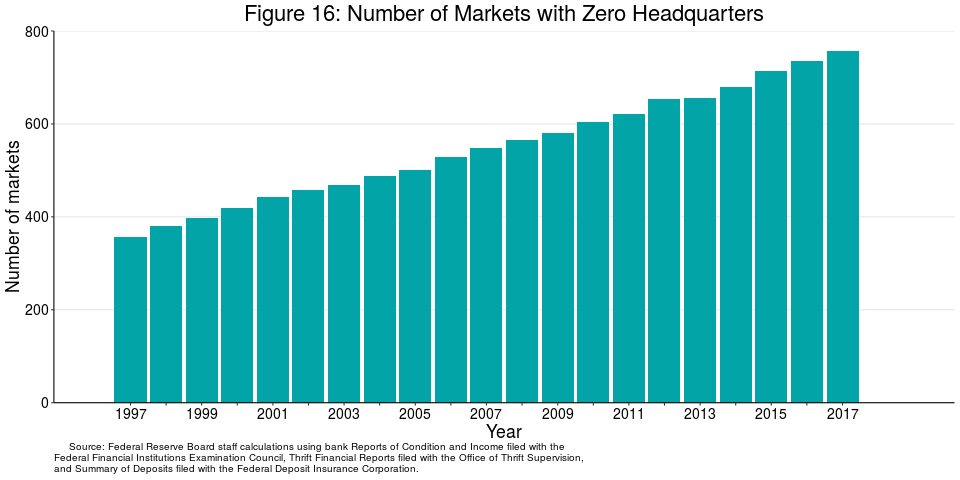

One unavoidable aspect of consolidation is a loss in the number of bank headquarters offices. The number of bank headquarters located in urban markets has fallen by half over the past 20 years, while the number in rural markets has fallen by 45 percent.9 Consolidation has led to a doubling in the number of banking markets--almost all of which are rural--in which no banks are headquartered (figure 16). We hear anecdotally that banks are more attuned to the needs of the communities in which they are headquartered, so the significance of this loss could have an effect on the local markets.

{kind=link}

Qualitative Evidence at a More Micro Level

As I previewed at the beginning of my remarks, data and averages often do not tell the whole story. At the end of the day, we care about bank branch locations because we care about the people and communities that they are serving or, in some cases, not serving adequately. So even if the data tell us that most rural markets are well served, we need to focus our attention on those markets that may not be as well served and how that is affecting the people who bank, or cannot bank, there. That is why the Federal Reserve System's Community Development function has undertaken a national series of listening sessions to assess the real effects of bank closures on rural communities. Reserve Bank staff members are conducting the sessions around the country to gather information from consumers and small business owners in rural communities that have been directly affected by bank closures.

To identify where to conduct these sessions, we used data to identify rural towns that have experienced bank branch closures; in some cases, these towns lost the only bank in town and now have no remaining banks. Then we convened local residents and small business owners to ask them about what the loss of a bank meant to them and their community.

For some residents, the closure has not been much of a problem. Most, if not all, of the listening session participants in Clark, South Dakota, noted that they do most of their routine banking online. Some in Clark even noted that they did not think ATMs (automated teller machines) were necessary, as most of the retail businesses in town offer cash back with debit card purchases. Nonetheless, residents of Clark spoke positively about the importance of the personal touch a local bank can provide. Residents liked familiar faces at the teller window and loan officers who understand the local economy when making small business loan decisions.

However, online banking is not necessarily an opportunity for everyone. Indeed, even for community banks themselves, technology may be perceived as a threat or an opportunity, depending for example on whether the necessary infrastructure is available. In Nicholas County, Kentucky, which is located in Appalachia, many residents do not have access to high-speed internet; this lack of access has led most residents to travel outside of the county to conduct their banking needs. This situation is certainly not optimal for anyone, but it presents a particular challenge to the elderly, those without a car, and busy small business owners who do not have time to travel 25 miles each way to make change and deposit checks. In Centre County, Pennsylvania, we heard that the transportation challenge is particularly acute for the Amish--10 miles is a long way to travel by horse and buggy.

The loss of a bank branch also has a ripple effect on a community as a whole. In the village of Brushton, New York, which lost its only bank branch in 2014, small business owners commented that when residents must leave the village to access banking services, they are more likely to shop, eat, and pay for services in other towns, which creates additional hardship for the small businesses of Brushton. Additionally, as the ability of community members to access cash has decreased, credit card use has increased. Small business owners in Brushton say that this growth in credit card usage has significantly increased the cost of doing business.

Lastly, one theme that we heard loud and clear across the country was that the loss of a local bank meant the loss of an important civic institution. Banks do not just cash checks and make loans--they also place ads in small town newspapers, donate to local nonprofits, and sponsor local Little League teams. As towns lose banks and bankers, they also lose important local leaders.

We will continue to conduct these listening sessions across the country throughout the fall. In fact, one of these listening sessions will take place next week just two hours down the road in Reynolds County, Missouri. We look forward to sharing the collective results of our efforts in a report that should be published in early 2019.

Conclusion

To sum up, the numbers of urban and rural community banks have been declining over the past 20 years, but community banks continue to play an important role in both types of markets. Urban and rural community banks face different challenges, but, on average, both seem to be faring well in the post-crisis period. And the average rural banking market has not seen any decline in the number of banks or bank branches over recent years. For the local areas where the availability of banking services has declined, we are in the process of assessing the effects of this decline on the people who live and work in those communities. I look forward to continuing to engage in this area and monitor the developments in this most vital part of the banking ecosystem.

1. The views I express here are my own and not necessarily those of the Board of Governors of the Federal Reserve System. Return to text

2. While small banks reduced small business lending by roughly 13 percent between 2009 and 2011, large banks reduced lending by nearly 30 percent. See Rebel A. Cole (2012), How Did the Financial Crisis Affect Small Business Lending in the United States? report developed under contract with the U.S. Small Business Administration, Office of Advocacy (Washington: SBA, November). Return to text

3. For the purpose of my remarks today, "community bank" means a bank or thrift with less than $10 billion in assets (in constant 2005 dollars). I exclude from this definition any bank or thrift that has less than $10 billion in assets but is part of a larger organization with more than $10 billion in total banking assets. "Urban community bank" is one that derives more than half of its deposits from offices located in one or more metropolitan statistical areas, and "rural community bank" derives at least half of its deposits from nonmetro areas. Using the more nuanced Federal Deposit Insurance Corporation (FDIC) definition of a community bank, which takes into account both size and activities, would have very little effect on the trends that I will be discussing. The FDIC definition can be found in Federal Deposit Insurance Corporation (2012), "Defining the Community Bank (PDF)," in FDIC Community Banking Study (Washington: FDIC, December). Return to text

4. See Jerome H. Powell (2016), "Trends in Community Bank Performance over the Past 20 Years," speech delivered at "Community Banking in the 21st Century," Fourth Annual Community Banking Research and Policy Conference, sponsored by the Federal Reserve System and the Conference of State Bank Supervisors, St. Louis, Mo., September 29. Return to text

5. See U.S. Census Bureau (2016), "New Census Data Show Differences between Urban and Rural Populations," press release, December 8. Return to text

6. See Kim Parker, Juliana Menasce Horowitz, Anna Brown, Richard Fry, D'Vera Cohn, and Ruth Igielnik (2018), "Demographic and Economic Trends in Urban, Suburban and Rural Communities," in What Unites and Divides Urban, Suburban and Rural Communities (Washington: Pew Research Center, May); or John M. Anderlik and Richard D. Cofer, Jr. (2014), "Long-Term Trends in Rural Depopulation and Their Implications for Community Banks (PDF)," FDIC Quarterly, vol. 8 (2), pp. 44-59. Return to text

7. See Mark Muro and Jacob Whiton (2018), "Geographic Gaps Are Widening While U.S. Economic Growth Increases," Brookings Institution, The Avenue (blog), January 23; and Brian Thiede, Lillie Greiman, Stephan Weiler, Steven C. Beda, and Tessa Conroy (2017), "The Divide between Rural and Urban America, in 6 Charts," U.S. News & World Report, March 20. Return to text

8. One way that economists measure the structure of a market is by measures of market concentration. Not surprisingly, rural markets are, on average, much more concentrated than urban markets. However, average concentration levels have been declining in rural markets while increasing slightly in urban markets over the past two decades. Return to text

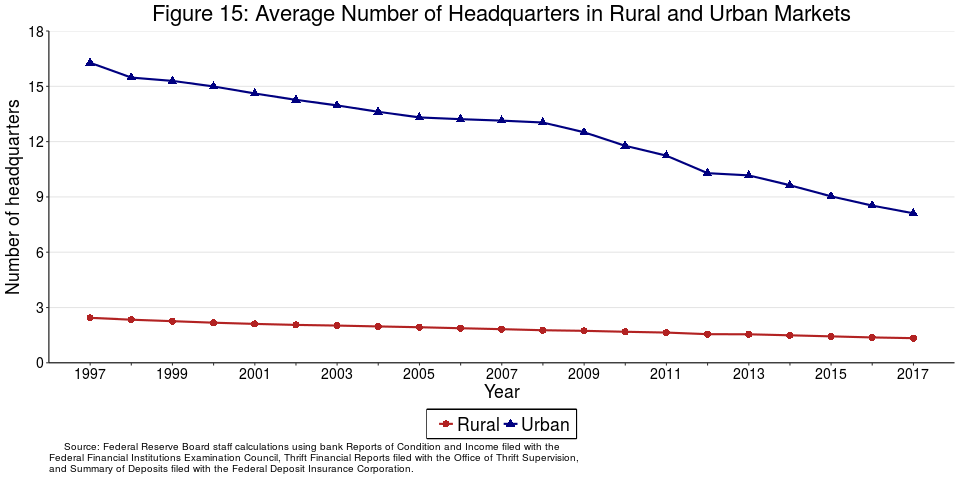

9. The average urban market has more headquarters offices than the average rural market (figure 15). There are just over 8 banks headquartered in the average urban market (down from just over 14 in 1997), compared with an average of 1.3 banks headquartered in the average rural market (down from 2.4 in 1997). Return to text

{kind=link}