December 05, 2018

Banks as Vital Infrastructure for Rural Communities of the West

Vice Chairman for Supervision Randal K. Quarles

At the Stanford Institute for Economic Policy Research, Stanford University, Stanford, California

It's a pleasure to be here at Stanford, an honor to be invited to speak by SIEPR and the Bill Lane Center--two institutions for which I have long had fondness and respect--and a great luxury to have the chance to talk for an hour with a group of people who share my love for a part of the world we call the West. Most of my day job enmeshes me, of necessity, in either broad systemic questions of global financial stability or the impossibly arcane minutiae of our convoluted and labyrinthine financial regulatory system. Both of those are perfectly worthy occupations but inescapably require a relentlessly global outlook. Yet my first intellectual passion as a very young man was for the history and life of a specific part of the world--the Western United States, as place and idea. Your own presence here in the audience suggests that many of you have been moved at some point in your life, as I have been, by the words of Wallace Stegner:

If there is such a thing as being conditioned by climate and geography, and I think there is, it is the West that has conditioned me. It has the forms and lights and colors that I respond to in nature and in art. If there is a western speech, I speak it; if there is a western character or personality, I am some variant of it; if there is a western culture in the small-c, anthropological sense, I have not escaped it.1

So, that is why I say it is a pleasure and an honor but most especially a luxury for me to speak to an audience that shares my concern for and love of the West on the topic of how the preoccupations of my day job--banking and finance--affect this particular part of the world. We all know that throughout the history of the West, banking and finance have played an important role as vital infrastructure for the economy. That remains true today, although it is often overlooked in the traditional litany of issues critical to the West. A strong banking industry is necessary for households and businesses to engage in the spending, saving, and investment that constitute economic activity, and one of the purposes of financial regulation is to ensure that banks continue to be able to serve this purpose. So it is my plan today to talk about the economy of the West and link the recent and future performance of the western economy to the central and supportive role banks play as vital infrastructure in their communities.

Defining the West

Let's start by defining our terms. What do we mean by the West? Before this audience, I approach this question with respect and a little caution, because I know that in a broad sense, it is what the Center for the American West has been addressing since its founding. That aside, it makes sense to use a definition, as the center often does, that includes parts of states in the middle of the country whose economies, heavily dependent on natural resources, ranching, and farming, more closely resemble Montana and New Mexico than they do states on the Eastern seaboard.

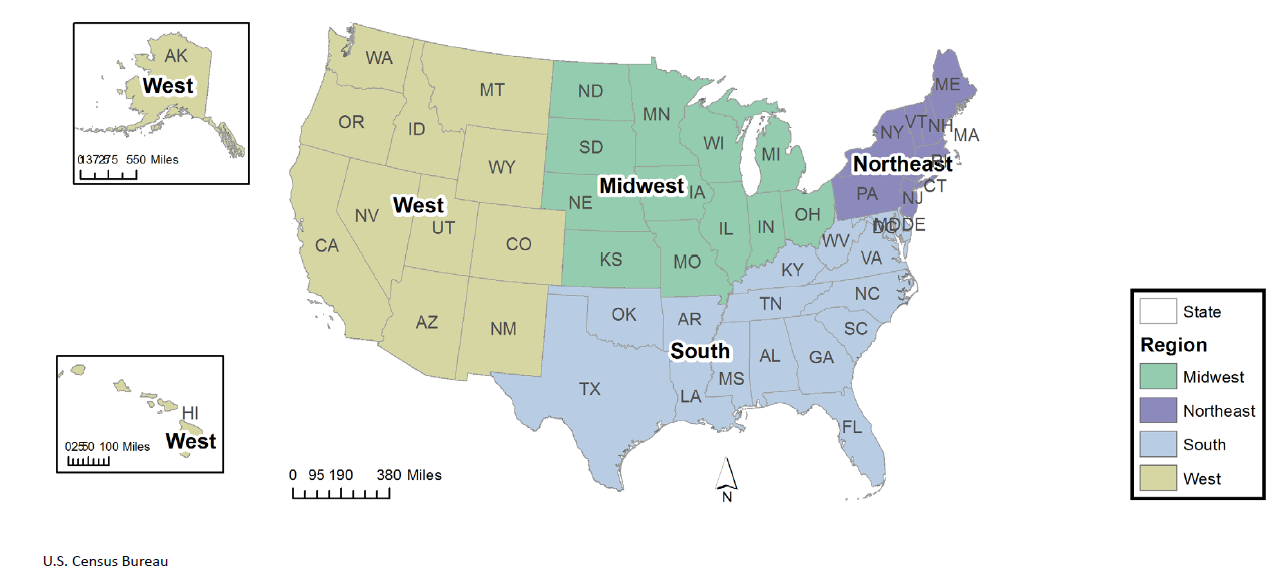

Nevertheless, for the purposes of these remarks, I am going to use a less expansive definition comprising the 13 westernmost states. I do so partly because this is a common definition of the West, and because it is the one used by the U.S. Census Bureau in dividing the country into four regions and this has helped me gather data for this speech more readily. (Figure 1)

{kind=link}

The first thing to mention that distinguishes the West from the rest of the country is apparent on this map--land area. The West is large and would appear even larger of course, if it weren't necessary to shrink the vastness of Alaska to fit on one page. Even using my more modest definition, the West still represents half of the land area of the United States. This is important in this context because of one theme I will be exploring today, which is the economy of the rural West and the banking services available there.

As this map should make plain, when we talk about rural America, to a significant extent we are talking about the rural West. Another way to put it is that while the West is half of the United States geographically, it is only a quarter of its population.2 Eight of the 13 states in our definition of the West are among the dozen in the nation with the lowest population density.3 Even after subtracting the large share of unpopulated government-owned land in the West, the overwhelming majority of the West is rural.

Yet it is also true that, as most of you know, the West is the most urban region of the country. Five of the 15 largest metro areas in the United States are located in the West, and 90 percent of the entire region's population lives in cities, compared to 81 percent of the country as a whole. 4,5 Nevada and Utah are among the least densely populated states, but 90 percent or more of their residents live in cities. Like the rest of the country, the West is urbanizing. I will return to the differences between urban and rural areas, but first, let's look at the economy of the West.

The Economy of the West: From Boom to Boom

The West accounts for 25 percent of U.S. gross domestic product, almost exactly the share of the U.S. population in the West. This isn't entirely a coincidence, because population relates to labor supply, which is one determinant of economic output. I mention this because it is also true that the change in population over time has a bearing on the economic health of communities and regions, and is part of the story for economic growth in the western United States.

In recent years, that story has been a very positive one. The U.S. economy is strong, and the western economy is especially strong. While we don't have state or regional numbers for this year, from 2015 through 2017, GDP, after adjusting for inflation, grew two to nearly three times as fast in the West as in the rest of the United States. Since the Great Recession ended in 2010, real GDP has grown twice as fast in the West as in the Northeast, about 50 percent faster than in the Midwest, and a third faster than in the South.6

But there is another distinction to the western economy, one that many in this audience know well, that brings these high-flying results down to earth. While the good times are typically very good in the West, the bad times are usually pretty bad, and that was certainly true during the Great Recession. From 2008 through 2010, the western economy contracted four times as much as the average for all of the United States. The same is true for per capita personal income, which contracted more sharply in the West than elsewhere, as job losses in the western region during the recession were worse than elsewhere.

Taking a longer perspective, however, even with the booms and the busts that have characterized the West for upwards of 200 years, the West is still the fastest growing region of the United States. Since 2000, real GDP has grown twice as fast in the West as in the Northeast and Midwest, and about 30 percent faster than in the South. Since 1988, the numbers are roughly the same. Per capita personal income grew faster in the West during good years, outweighing the sharper losses during the recession and since 2000 has grown about 20 percent faster in the West than in the rest of the country.

This picture of the West leading the nation in economic growth is also reflected in population, a key factor in that growth. From 2010 to 2017, the population of the West increased 7.4 percent, compared to 5.3 percent for the nation.7 One might guess that this strong growth is primarily in cities, and in fact reflects the drain of population from smaller towns that is reported to be happening all over the United States. But in fact, population gains in the West are quite well balanced between cities and towns, and smaller towns are doing better in the West than elsewhere in holding and even increasing their populations.

In the cities of the West, those communities of 50,000 or more, the population grew 7.8 percent from 2010 to 2017, eclipsed by the 10 percent growth in southern cities but well above the 2 percent to 3 percent increase in the cities of the Northeast and Midwest.8 At the same time, the West led the other regions of the United States in growth for towns and cities from 10,000 to 50,000 in size, and likewise for towns between 5,000 and 10,000.

Now let's look at small towns, those with 5,000 or fewer residents. It is this cohort of towns and their people that to my mind is really the essence of rural America. There is a widespread impression that small towns all over America are shrinking and that population is shifting to larger towns and cities, and that is the story we can see in much of the regional data. From 2010 to 2017, the average small town shrank by 2 percent in the Northeast, by 1.4 percent in the Midwest, and only grew 1.3 percent in the South, while larger towns and cities grew substantially faster there and elsewhere.

What about the West, where urbanization is happening more quickly than anywhere else? In fact, the average western small town grew 7.8 percent in those seven years, which is roughly the same healthy pace of growth registered in western towns and cities from the smallest to the largest.

With a nod to Mark Twain, the message here is that reports of the death of small towns, at least in the West, have been greatly exaggerated. I don't mean to minimize the challenges small towns face, because they are considerable, or suggest that western small towns are immune to them, because they certainly are not. But the more positive message I come away with here is that a rising tide of prosperity in the West seems to be lifting communities large and small, and that the many instances of small towns in decline that we all hear about are counterbalanced by other small towns growing healthily. Another lesson is that population growth and the attendant economic growth in the West is not zero sum, and that small towns can still grow healthily while the metropolises of the West continue to attract people, partly from outside the region. I will return to the issue of how the economies of the urban and rural West differ, but the backdrop is that population data are promising for both.

Banking in the West

Now that I have outlined how the economy of the West relates to that of the rest of the United States, let me do the same for banking in the West. There is a lot to this topic, but my focus is banking as it is experienced at the retail level by households and small- and medium-sized businesses. Again, I use the Census Bureau's list of 13 states to define the West, and for a simpler comparison, and in honor of Frank Church, I will refer to the other 37 states as "eastern" even though they cover several regions. Some of you are old enough to remember Frank Church, the U.S. Senator from Idaho--a Stanford grad and hero of mine when I was a teenager. When he ran for president in 1976 and had some success in the primaries, he was challenged by the press that said his victories were limited to the West, and he replied "What do you mean I can't win an eastern state? I won Nebraska!"

One dimension to how households and most businesses experience banking is the number of banks competing for their services, and one difference between the West and the East is that the West has fewer banks, even if we count them on a per capita basis.9 In addition, banks in the West tend to be larger. One reason for the disparity in the average number and size of banks is that historically, a larger share of western states allowed statewide branching or had relatively limited branching restrictions, leading to the development of fewer and larger banks.10

In metropolitan areas of the West, the average number of banks was 23 in 2017, compared to 27 in eastern metro areas. In rural counties of the West, customers had access to an average of 4.6 banks in 2017, compared to 5.4 banks in the East. In both urban and rural areas, in both the East and the West, the average number of banks increased in the years leading up to the financial crisis but has been declining since then. While there is certainly more to say about banking services in cities, I want to focus on rural areas for the moment. Over the last 20 years, rural westerners have consistently had access to something like 20 percent fewer banks than rural easterners, which amounts to about one less bank per rural county. That may not sound like much, but that one less bank, on average, can make a big difference to the households and small businesses inhabiting those rural counties.

In any community, access to credit is essential for economic growth. In any community, but especially in rural communities, small businesses are key drivers of growth. Small businesses heavily rely on banks for funding, and community banks, those with less than $10 billion in assets, account for a disproportionate share of bank lending to small businesses.

But across the country, the number of community banks has fallen by half over the past 20 years, mostly due to consolidation. This fall has been slightly larger in the West than the East, but the reason I highlight this trend is that I believe it has significant consequences for rural communities in the West. The reason returns me to that map I showed earlier. The West is vast, and many rural communities in the West must deal with the challenges of isolation from larger towns and cities that few communities in the East face. Rural westerners have access to far fewer banks overall than rural easterners, but that understates the disparity when some western counties are the size of Maryland or Massachusetts and many are more than a hundred miles across, so that access to a limited number of banks can be difficult or out of reach.

To provide some perspective on this challenge, let me share what westerners in one small town have to say about their access to banking services. This account is culled from a series of public meetings that the Federal Reserve is convening in communities all around the country, in support of our responsibilities overseeing community banks and promoting community development.

Not quite a month ago, we held one such session in my home state of Utah, in the town of Green River, population 940, located on the eastern side of the state. It is just off an isolated stretch of interstate, and its economy depends on those passersby and tourism related to outdoor recreation. In 2014, Green River lost its only bank, and around that time, banks closed in several nearby communities. As a result, most residents of Green River who need banking services must drive the 52 miles to Moab, Utah. This loss has had a profound effect on households and businesses, essentially turning back the clock in Green River by decades, as far as its access to the banking system. Business owners say their work days have been curtailed by the need to drive two or three times a week to Moab to obtain change and make deposits. Businesses have become banks for many residents, agreeing to cash their checks. Because of this new service to residents, and the long distance to a real bank, retail businesses say they are carrying much larger amounts of cash, which has heightened security concerns and prompted some merchants to invest in new safes. Security is also a concern for residents who no longer have access to safety deposit boxes for valuables and important papers.

Faster and more efficient electronic payments hold some promise to bridge these gaps, eventually, and the Federal Reserve is working hard on this and making significant progress. But one thing that technology cannot do is replace the knowledge and perspective of a local banker who is part of the community. Relationship-based lending that is the hallmark of community banking can stem losses during downturns, since community banks may be able to work with borrowers to avoid losses. Research has shown that small business lending at smaller banks declined less severely than at large banks during the last recession.

Community banks face considerable competition. One of the reasons that community banks continue to succeed in many places is their understanding of their customers' needs and opportunities to invest in families and businesses. The loss of this relationship, for a community, means that needs will go unmet, and opportunities will be lost.

In some communities, of course, this may be unavoidable, if a town has lost a major employer and has no new industry or plan to replace the jobs lost. But let me remind you of the very encouraging data I cited on the growth of small towns in the West. Overall, rural communities are growing at a healthy pace, and growing communities need banks. It is my hope that the opportunity for the future that this population growth suggests will support the local banks that communities need to thrive.

A significant part of the Federal Reserve's recent regulatory focus has been aimed at streamlining regulations and reducing the regulatory burden on smaller and regional banks.

The Fed, along with the other banking agencies, recently proposed a community bank leverage ratio that is designed to simplify significantly the standards banks must abide by for holding capital.11 As a result, qualifying community banks will only need to calculate and meet a single measure of capital adequacy, rather than multiple measures. We have also proposed a reduction in the burden of reporting requirements for community banks, and expect soon to propose an exemption for community banks to the Volcker rule.12 For a subset of the smallest banks--those with less than $5 billion in total assets--we have also lengthened the amount of time between supervisory examinations and expanded eligibility of small bank holding companies that qualify for an exemption to the Federal Reserve's capital rules, a policy that was designed to promote local ownership of small banks and to help maintain banks in rural areas.13

Most recently, the Federal Reserve spearheaded a proposal to tailor regulation that applies to firms that are larger than community banks, but the potential failure of which generally does not pose risks to the financial system.14 These are firms with between $100 billion and $250 billion in total assets. Those changes are designed to reduce unnecessary regulatory burdens on specific institutions without any loss of resiliency for the financial system.

By these steps, I believe the Federal Reserve is helping community banks remain competitive and play the central role they have long played as vital infrastructure for rural communities. The future of community banks in these communities is one reason that I'm optimistic about the economic prospects of small towns in the West, which continue to grow even as the region and the nation overall becomes more urban. That's a good thing, because small towns, and especially their values, have long helped define the West, and I hope will continue to do so.

1. Wallace Stegner, "The American West as Living Space," University of Michigan Press, 1988. Return to text

2. Source: Federal Reserve Board staff calculations were done using data from the following website: "List of states and territories of the United States by population," Wikipedia, last modified November 18, 2018. Return to text

3. Source: "List of states and territories of the United States by population density," Wikipedia, last modified October 12, 2018. Return to text

4. Source: "List of metropolitan statistical areas," Wikipedia, last modified November 29, 2018. Return to text

5. Source: "Urbanization in the United States," Wikipedia, last modified November 10, 2018. Return to text

6. Statistics presented in this paragraph and the next two paragraphs are derived from the following website: "Comparative Economic Indicators: Year vs. Year Analysis of Growth and Change," Regional Economic Analysis Project. Return to text

7. Source: https://www.census.gov/popclock/data_tables.php?component=growth. Return to text

8. Statistics presented in this paragraph and the next two paragraphs are derived from the following website: "The West and South Lead the Way," United States Census Bureau, last modified October 1, 2018. Return to text

9. The source for statistics presented in this paragraph and the next three paragraphs is Federal Reserve Board staff calculations using bank Reports of Condition and Income filed with the Federal Financial Institutions Examination Council, Thrift Financial Reports filed with the Office of Thrift Supervision, and Summary of Deposits filed with the Federal Deposit Insurance Corporation. Return to text

10. Even though state banking restrictions were eliminated in most states decades ago, the differences in the number of banks across states have persisted. Return to text

11. See Board of Governors of the Federal Reserve System, "Agencies propose community bank leverage ratio for qualifying community banking organizations," news releases, November 21, 2018. Return to text

12. See Board of Governors of the Federal Reserve System, "Agencies issue proposal to streamline regulatory reporting for qualifying small institutions," news release, November 7, 2018. Return to text

13. See Board of Governors of the Federal Reserve System, "Agencies issue interim final rules expanding examination cycle for qualifying small banks and U.S. branches of foreign banks," news release, August 23, 2018 and Board of Governors of the Federal Reserve System, "Federal Reserve Board issues interim final rule expanding the applicability of the Board's small bank holding company policy statement," news release, August 28, 2018. Of course, while the holding companies of community banks may be eligible for an exemption from capital rules, the subsidiary banks are still subject to capital requirements. Return to text

14. See Board of Governors of the Federal Reserve System, "Federal Reserve Board invites public comment on framework that would more closely match regulations for large banking organizations with their risk profiles," news release, October 31, 2018. Return to text