September 26, 2016

Next Steps in the Evolution of Stress Testing

Governor Daniel K. Tarullo

At the Yale University School of Management Leaders Forum, New Haven, Connecticut

Supervisory stress testing has become a cornerstone of post-crisis prudential regulation. Stress testing, unlike traditional capital requirements, provides a forward-looking assessment of losses that would be suffered under adverse economic scenarios. The simultaneous testing of the largest firms lends a perspective on a large part of the banking system and facilitates identification of common exposures and risks.

During the financial crisis, the success of an ad hoc stress test in assessing the capital needs of, and restoring confidence in, the nation's largest financial institutions encouraged Congress to make stress testing a required and regular feature of large firm prudential regulation.1 The Federal Reserve has, in the succeeding years, substantially refined its supervisory stress test. Moreover, the stress test has been integrated into our Comprehensive Capital Analysis and Review (CCAR), which both ties the results of the test into the banks' capital distribution practices and evaluates their risk management and capital planning capacities.

Today I want to share with you the results of an extensive review of the statutory stress test and CCAR programs, which we began following the end of the 2015 cycle. Before turning to the reasons for that review and some ideas for changing these programs that have arisen from it, I will take a few moments to summarize the characteristics and purposes of the programs as they have evolved to this point.

Stress Testing and CCAR Today

As we have implemented the requirement mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) for stress testing--which the Federal Reserve denominates as the Dodd-Frank Act Stress Test (DFAST)--that exercise includes four main steps.2 (1) The firms subject to DFAST provide the Federal Reserve with detailed, significantly standardized data on their loans, securities holdings, trading positions, counterparty exposures, revenue, expenses, and balance sheets. (2) The Federal Reserve specifies hypothetical macroeconomic and financial market scenarios--including an "adverse" and a "severely adverse" scenario. (3) The Federal Reserve inputs the data from the firms into its own supervisory models to project each firm's losses, revenues, and capital over a nine-quarter planning horizon under the specified scenarios. (4) The results of the exercise, including the capital positions of the firms following the hypothesized stress scenarios, are disclosed to the public.

As DFAST has evolved, it has become an increasingly valuable tool for evaluating whether the largest financial firms are holding sufficient capital to continue providing credit in the event of significant macroeconomic and financial stress. However, in itself DFAST does not set any capital ratios or limit any capital actions by the firms. Those functions are implemented through the CCAR program, which was created through the regulatory process by the Federal Reserve.3 In CCAR, the Federal Reserve assesses the overall capital adequacy of the firms--including evaluations of whether each firm's capital provides an adequate buffer for the losses that would be incurred during the stress scenarios, whether its risk management and capital planning processes are appropriately well-developed and governed, and how its plans to distribute capital through dividends or share repurchases could affect its ability to remain a viable financial intermediary in the hypothesized scenarios. Given how central these considerations are to effective risk management and the soundness of these firms, we are progressively integrating the qualitative elements of CCAR into our year-round supervisory program for the largest banking organizations.

Under CCAR, the Federal Reserve may object to a firm's capital plan on either quantitative or qualitative grounds. A quantitative objection is made when the stress test reveals that a firm would not be able to maintain its post-stress capital ratios above the regulatory minimum levels over the planning horizon, taking into account its planned capital distributions. We have taken planned distributions into account because, as the run-up to the financial crisis revealed, firms may be reluctant to cut their distributions--particularly dividends--even in a period of growing stress. Thus, CCAR included what has been called a "pre-funding" requirement.

The Federal Reserve may object on qualitative grounds if it finds that the firm's capital planning processes are not sufficiently reliable. The qualitative assessment includes the assumptions and analyses underlying each firm's capital plan, its controls and governance processes, and whether previously identified weaknesses in management and operations have been corrected. If the Federal Reserve objects on quantitative or qualitative grounds, the firm may not make any capital distributions without our permission. In practice, in the case of a qualitative objection, we have generally permitted distributions at the previous year's level but no increases. This practice, however, has been in the context of distributions rising from generally low levels coming out of the crisis; there has been no guarantee that a similar practice would prevail as distributions continue rising.

The quantitative component of CCAR, based as it is on the DFAST stress tests, has contributed to the continued strengthening of the capital levels of the largest financial institutions that began after the original stress test in the winter of 2009.4 While, understandably, many focus on the quantitative side and its implications for capital distributions, the importance of the qualitative component has been perhaps underappreciated. We saw during the 2009 stress test that many large financial institutions were unable to marshal the data necessary to gauge their own exposures accurately or to project the adverse effects they would suffer in a tail event, as opposed to a more ordinary cyclical downturn. CCAR has required the firms to steadily improve their risk management and capital planning processes. Indeed, some of the firms--particularly the less complex banks within the CCAR cohort--are now meeting, or are close to meeting, our supervisory expectations across a range of risk management and capital planning processes.

The CCAR Review

Clearly, then, we regard the stress testing and CCAR programs to have made substantial contributions to protecting the safety and soundness of the nation's largest financial firms and to promoting the stability of the financial system as a whole. But, equally clearly, if a stress testing regime is to continue to play this role, it must be dynamic. The hypothesized scenarios must change to take account of new economic and financial risks. The supervisory model may, in some circumstances, need to be changed to take account of evolving economic conditions and bank portfolio characteristics. Additionally, we have been refining the stress testing and CCAR processes in what is, of course, still a relatively new regulatory and supervisory tool. Changes of all these kinds have been, and will continue to be, made from year to year.

After five years of post-crisis stress testing, however, we believed it was important for us to conduct a more thorough assessment of the program. Taking advantage of the shift in timing of the annual stress tests following the 2015 cycle, we undertook an overall review.5 We knew there were several areas to which attention was needed. These included the imperfect alignment of CCAR with the regulatory capital requirements as they had evolved since we began stress testing, the desire for additional macroprudential elements in the stress test, and the qualitative component of CCAR as it applied to less complex firms.

But we also wanted to hear what others thought. Accordingly, we met with bank officials, debt and equity-side market analysts, public interest groups, and academics--both to solicit their views on the topics I noted a moment ago and to hear their overall evaluation of, and recommendations for, our stress testing and CCAR exercises. As you can imagine, we received a wide range of suggestions, at least some of which were inconsistent with one another. In the main, though, these discussions reflected strong support for stress testing, reinforced our going-in view of the key issues for consideration, and presented us with some other areas for possible change. Before describing the package of potential changes that is emerging from our review, let me explain a bit more about each of the key topics.

First is the fact that CCAR has been adjusted to align with some, but not all, of the important changes made in our regulatory capital rules over the past six years.6 One might decide that the regulatory capital rules and CCAR should be different, complementary capital measures, roughly the way that a leverage ratio requirement and risk-weighted capital requirements are complementary. In some particulars, though, CCAR sits a bit uneasily alongside the ongoing capital requirements. The most notable example is that CCAR assumes that a firm will continue to make its planned capital distributions during a stress period even though the regulatory capital rules now include a capital conservation buffer to limit such distributions. Another is that, to this point, CCAR has not reflected the firm-specific capital surcharge we have adopted for global systemically important banks (GSIBs).

Our second key topic was the macroprudential dimension of the stress testing and CCAR regimes. One of the most important lessons of the financial crisis was that prudential regulation, including capital regulation, had been dominantly microprudential in nature, even for the largest firms. That is, the regulation was designed and applied with a view mostly to the idiosyncratic risks faced by a bank in isolation, without regard to the interaction of the bank and the financial system as a whole. Thus, for example, capital regulation did not take account of fire sale effects--the reduction in portfolio values for one bank by other banks selling certain types of assets in order to enhance their own solvency or to counter a reduction in funding availability. Similarly, microprudential capital regulation allows a bank to meet its capital ratios by reducing lending--that is, by reducing the denominator of its ratio--as well as by increasing capital. If many banks were to follow this strategy, even creditworthy borrowers would be adversely affected, thereby exacerbating an economic downturn.

Our stress testing and CCAR regimes do have some macroprudential elements, which have been modestly enhanced over the past few years. By conducting the stress tests for all large banks at the same time under common scenarios, we can evaluate the collective losses that may be borne by a major part of the industry in the stress scenario. We vary scenario design to take account of a variety of risks to the financial system and in a way that reduces procyclical effects.7 We vary the market shock over time to reduce the incentive for firms to correlate their asset holdings or adopt correlated hedging strategies that are treated relatively favorably under one particular market shock scenario. And we do not allow firms to plan on a reduction in their balance sheets as a way to meet capital ratio requirements under stress.

Still, as currently conceived and implemented, our stress testing regime emphasizes the direct risks to bank capital from a severe recession and associated market dislocation via the usual channels of reduced operating revenues combined with credit, market, counterparty, and operational losses. However, as noted by some academics and policy analysts, a fully developed macroprudential dimension to stress testing would incorporate indirect risks to bank capital through channels such as market-wide funding and liquidity disruptions, fire sales, and so on.8 These amplification effects are obviously particularly important for firms that have relatively larger trading books or that rely relatively more on short-term funding, or both. Indeed, many of the academics with whom we discussed stress testing during our review emphasized the importance of building out the macroprudential elements of our stress testing program.

The third topic we had identified for review was the nature of the qualitative assessment as it applied to the relatively smaller, less complex firms within the CCAR exercise. While we had always explicitly differentiated our risk management and capital planning expectations for these firms, our supervisors had observed that many such firms seemed uncertain of whether they would nonetheless be held to the more stringent standards intended for the largest, most complex firms. In the course of our review, comments from these smaller, less complex firms confirmed this observation. Officials from these banks expressed the view that the CCAR qualitative assessment was unduly burdensome because it created pressure to develop complex processes, extensive documentation, and sophisticated stress test models that mirrored those in use at the largest, most complex firms, in order to avoid the possibility of a public objection to their capital plan. Since our intention had never been to create an incentive for firms with a relatively small systemic footprint to invest in stress testing processes appropriate only for larger or more complex firms, we knew we needed to address this problem.

Results of the Review

After more than a year of discussions and analysis, we have developed ideas for changes to the stress testing and CCAR regimes that would address these three key issues, along with some related matters that arose during the course of our review. Some of these changes would need to be pursued through rulemakings, including the usual notice-and-comment process. Others can be implemented through nonregulatory changes, though some will need further elaboration in moving from idea to concrete practice. Thus, there is a necessarily provisional character to the package set forth here. Except for the relief from the qualitative requirements for smaller, less complex CCAR firms--which I will describe a bit later--we do not contemplate proposing regulations to implement these ideas until early next year. Thus, any such changes would not apply to the coming 2017 DFAST/CCAR cycle.

Better Alignment of CCAR with the new regulatory capital rules

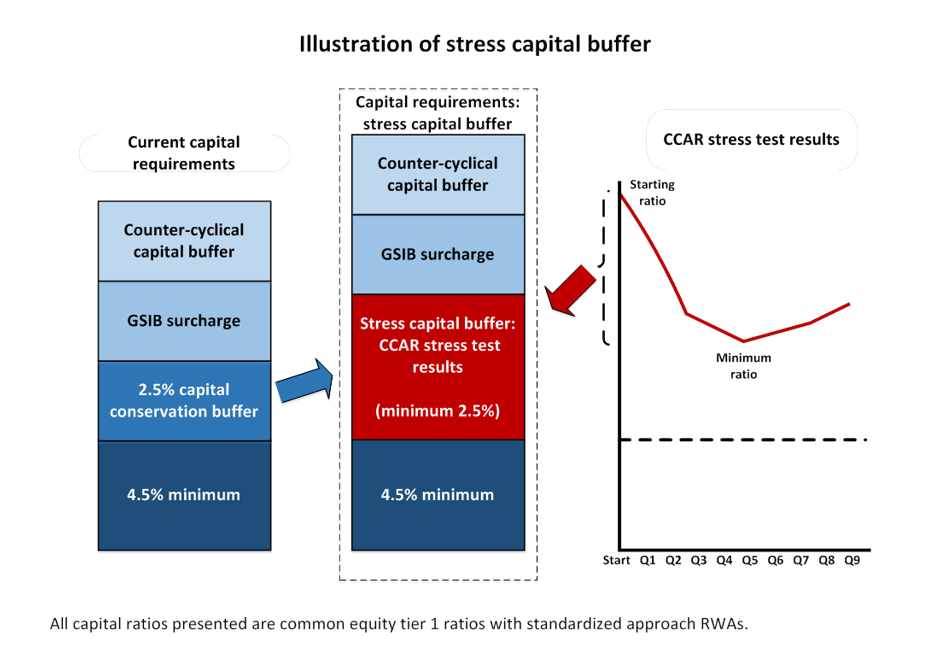

As I noted earlier, there have been significant additions to regulatory capital requirements since the first CCAR exercise began in late 2010. While some--such as revised risk-weighted asset calculation methodologies and definitions of capital--have been integrated into the stress testing program, other important additions have not. Most significant are the various capital buffer requirements that sit atop the regulatory minimum levels. These include a uniform 2.5-percent capital conservation buffer (CCB), the GSIB surcharge, and a countercyclical buffer that can expand the CCB for a broad range of firms in times of increasing financial vulnerabilities.9 Firms that do not hold capital sufficient to meet or exceed this combined buffer level are subject to restrictions on their capital distributions and bonus payments to executives, which become progressively stricter as their capital level falls deeper into the buffer.

To better align CCAR with the regulatory capital rules as they now stand, we will be considering adoption of a "stress capital buffer" (SCB) approach to setting post-stress capital requirements that would further integrate our capital rules with our stress test and CCAR frameworks. The simplest way to describe it is that the SCB would replace the existing 2.5 percent CCB as a component in each CCAR firm's point-in-time capital requirements. The SCB would be risk-sensitive and vary across firms, based on the results of the annual stress test. Specifically, it would be set equal to the maximum decline in a firm's common equity tier 1 capital ratio under the severely adverse scenario of the supervisory stress test before the inclusion of the firm's planned capital distributions, a simplification from the current practice of calculating the capital positions of the firm separately for each quarter in the scenario horizon.

As is now the case with the CCB and other applicable capital buffers, a firm would be subject to restrictions on its capital distributions whenever its capital levels fall below the combined regulatory minima and buffers. Although it is likely that the stress test losses will continue to exceed 2.5 percent of risk-weighted assets for most GSIBs, the SCB would have a specified floor at this current CCB level to avoid any reduction in the stringency of the regulatory capital rules. A firm's buffer requirement would be recalculated after each year's stress test, and its capital plan would not be approved in CCAR if the plan indicated that the firm would fall into the buffer under the stress test's baseline projections.

Let me use a hypothetical example to illustrate how the SCB would work. Assuming that a firm's common equity tier 1 capital ratio declines in CCAR's severely adverse scenario from 13 percent to 8 percent, that firm's SCB would be the greater of 2.5 percent or the 5 percent decline--thus, 5 percent. Assuming further that this firm is a GSIB with a surcharge of 3 percent and that the countercyclical buffer is not in effect, the firm would be constrained in making capital distributions that would bring its common equity tier 1 capital ratio under 12.5 percent. The 12.5 percent figure is the sum of the 4.5 percent minimum common equity tier 1 risk-weighted capital requirement, the 3 percent surcharge, and the 5 percent stress loss as calculated in annual stress test.10

Because the GSIB capital surcharge already exists as an additional buffer requirement in the regulatory capital rules, the stress capital buffer approach would effectively add the GSIB capital surcharge to our estimates of the amount of capital needed under stress. This would generally result in a significant increase in capital requirements applicable to the GSIBs, for most of which CCAR has been their binding capital constraint. But having both the stress loss buffer and the capital surcharge included in our capital requirements is wholly consistent with the reasons for having a capital surcharge in the first place. Indeed, not having the two together has actually been an anomaly that arose from the sequencing of the various capital strengthening measures we have undertaken.

The Board adopted the GSIB surcharge requirement as part of its implementation of section 165 of the Dodd-Frank Act, which established the important macroprudential principle that financial firms should be subject to increasingly stringent regulation as their systemic importance increases. As explained in more detail in the white paper that accompanied the Board's final GSIB risk-based capital surcharge rule,11 the material distress or failure of a GSIB would have an adverse impact on the financial system as a whole that is far greater than the impact on the financial system of the distress or failure of a non-GSIB banking firm. Accordingly, GSIBs should face capital surcharges to compel internalization of those external costs. This should reduce the probability of a GSIB's failure enough below that of a non-GSIB that the expected impact on the system of a GSIB and a non-GSIB failure are more comparable.

Because the difference in the external costs of the distress or failure of a GSIB as compared to a non-GSIB is likely to be at least as high during times of macroeconomic and financial market stress as during ordinary times, there is no reason why the GSIB surcharge should not be a part of the post-stress capital regime. A complementary point is that the extra buffer required by the GSIB surcharge also reflects the fact that even the best-conceived annual stress scenarios cannot capture all tail risks in the financial system. The integration of capital rules and the stress test thus advances our second aim in initiating our CCAR review--the incorporation of more macroprudential elements.

As some of you may know, Chair Yellen and I have, on a number of occasions over the past year or so, indicated publicly that we would be considering the effective incorporation of the surcharge into post-stress capital expectations. Some industry representatives have subsequently argued that this step is not warranted. While we will of course address these and other comments as our rulemaking process moves forward, I want to comment now on a couple of arguments, since they seem to reflect a misunderstanding of our stress testing program or of the regulatory structure established by the Dodd-Frank Act.

One such argument is that it is duplicative to include both the anticipated losses under stress and the GSIB surcharge in a firm's capital requirement because two elements of our current stress test, the global market shock and the counterparty default shock, only apply to GSIB firms. However, these additional scenario components capture direct losses to which any firm engaged in material trading activity is exposed. The market shock measures the trading mark-to-market losses associated with sudden changes in asset prices. The large counterparty default measures the losses associated with repricing counterparty exposures based on the market shock, and then assuming the default of the counterparty that represents the largest net exposure. These components of the stress test do not capture the adverse impact of a GSIB failure on the financial system as a whole--the risks that are the basis for the GSIB surcharge.

These components of our stress test currently apply only to GSIBs because GSIBs are the only firms currently in CCAR for which these exposures are material. Non-GSIBs currently do not have material trading activities and so would suffer only small direct trading losses as a result of severely stressed market conditions or the failure of a major derivatives or repurchase agreement (repo) counterparty. As the U.S. intermediate holding companies of foreign banks with more material trading businesses in their U.S. operations are added to CCAR, we intend to revisit whether the global market shock and counterparty default component should be applied to firms beyond the U.S. GSIBs.

Another argument offered against inclusion of the surcharge as an element of post-stress capital expectations is that the material distress or failure of a GSIB no longer poses a significant threat to financial stability due to the regulations and supervisory programs that are designed to improve GSIB resolvability. These measures include, among others, the proposed total loss absorbing capacity (TLAC) rule, the proposed qualifying financial contracts early termination rule and related International Swap and Derivatives Association (ISDA) protocols, and efforts to ensure firms engage in strong recovery and resolution planning.

It is true that these efforts have improved GSIB resolvability in recent years. But these efforts are ongoing, rather than complete. More importantly, while there is certainly a relationship between the goals of strengthening the resiliency of the most systemically important firms and making them more readily resolvable should they nonetheless fail, those are still separate regulatory aims. The demise of a very large financial institution would cause substantial damage to the economy and the financial system even if it was not so disorderly as to threaten the system entirely. Note, in this regard, that the Dodd-Frank Act requires both more stringent prudential standards for systemically important firms and a process for promoting the orderly resolution of these same firms. While the complementarity of these and other elements of a regulatory program always warrant consideration, and while adjustments in all aspects of the program should be made as conditions and practices evolve, current work on orderly resolution is surely no argument against the promotion of systemic stability and macroprudential aims by integrating the surcharge requirement with CCAR.

Changes to the treatment of planned dividends and share repurchases

The shift to a stress capital buffer approach would provide a mechanism for addressing two issues related to capital distribution limitations under CCAR. The first is the arguable inconsistency between, on the one hand, the existing CCAR assumption that all planned dividends and share repurchases would proceed during the two-year planning horizon, regardless of how much stress the bank was under and, on the other, the concept of a capital conservation buffer above minimum capital requirements as it has been added to the capital rules. The second is a soft limitation on dividends put in place by the Board at the inception of CCAR. Both of these features of CCAR reflected supervisory concerns with the fact that, even as the financial crisis was clearly unfolding, some of the largest banks continued to repurchase shares and pay dividends to shareholders and, thereby, depleted capital that proved to be needed later.12

The SCB approach addresses the first of these issues by providing a continuous constraint on any planned distributions that would bring capital levels below the sum of the minimum 4.5 percent of risk-weighted assets plus the firm-specific SCB, plus any applicable GSIB surcharge.13 However, because declines in observed and reported capital levels usually occur with a lag, and the historical evidence that dividends are less likely to be curtailed than share repurchases,14 we would assume a firm will maintain its dividends for one year while reducing its repurchases. This would have the effect of requiring a firm to hold capital to meet its stress losses and fund its planned dividends over the next year.

The switch to an SCB approach would also give us an opportunity to address a second issue, the soft limit on dividends in CCAR. Since its inception, our policy statements on CCAR have indicated that a capital plan with a planned dividend payout ratio above 30 percent would be subjected to particularly close scrutiny. When this policy was adopted in late 2010, we expected that it would be a useful guideline during a period when most of the CCAR banks would need to continue increasing capital levels for some time but also recognized that at some point we would need to revisit it.

Since the new approach of adding one year's planned dividends to a firm's capital buffer should act as a disincentive for imprudent or unsustainable levels of dividends, the notion of extra scrutiny on planned dividends may no longer be useful. And we would, in any case, be reluctant to substitute a higher payout ratio for the original 30 percent ratio because it may end up being an implicit target for banks to try to reach. However, firms planning higher dividends should be aware that the operation of the SCB is such that, if a firm planned to pay out all of its earnings in the form of dividends and things did not go as well as expected for the firm, it could end up having to cut its dividend.

Balance sheet and risk-weighted asset assumptions

Beyond requiring that large banks have the resiliency to weather a period of serious financial stress, an important macroprudential aim of stress testing is to ensure that they can provide credit to households and businesses that remain creditworthy even in such a period. If banks maintain their capital ratios under stress by reducing their balance sheets through asset sales, or reductions in new lending, this crucial intermediation function will be compromised across the economy. The result could be a credit crunch, likely resulting in a more severe or longer-lasting recession. In the first few years of CCAR, we used the banks' own projections where many banks planned on balance sheet declines as part of their strategy for remaining sufficiently capitalized.15 In the 2014 CCAR cycle, we replaced banks' projections with our own model, adding a requirement that banks would not restrict the supply of loans during the severely adverse scenario.

To date, the model has actually operated to project an increase in the balance sheets of the CCAR banks during the severely adverse scenario, with varying impacts on different portfolios. This assumption, and its somewhat complicated implementation, was designed to be fairly conservative, in a manner not dissimilar to the assumptions about capital distributions. Numerous banks have attempted to show why some of these portfolios or business lines would not be increasing under any reasonable assumptions, and thus that even macroprudential goals do not justify ignoring the likelihood that those portfolios would decline. During our review of CCAR, some banks proposed ways to distinguish among business lines so as to relax what they argued to be an unrealistic assumption, even one with a macroprudential purpose.

The complexities of trying to differentiate across idiosyncratic business lines seem to us considerable. We are instead considering replacing this feature of our model with a simple assumption that balance sheets and risk-weighted assets remain constant over the severely adverse scenario horizon. Given that some decline in demand by creditworthy borrowers for loans is inevitable in a serious recession, this simpler assumption would still achieve the macroprudential policy objective that any such decline in lending during a recession is attributable to the impact of the recession, rather than to capital constraints at the large banks. This change would also make the treatment of balance sheets and risk-weighted assets simpler and more transparent.

Toward a more macroprudential stress testing regime

The second major objective in our stress testing review was to integrate more macroprudential elements into the program. Of course, combining the GSIB surcharge with the SCB approach promotes an important macroprudential aim, since the surcharges are calibrated to force large, interconnected banks to internalize the additional costs their distress would impose on the financial system. The surcharges are thus at least a partial surrogate for inclusion of various macroprudential features in the stress test.

We are also considering a couple of relatively modest revisions we are considering to the Board's "Policy Statement on the Scenario Design Framework for Stress Testing"16 that are motivated by the macroprudential consideration of reducing procyclicality. The first would be to make the severity of the change in the unemployment rate less severe during downturns. The second would be to replace the current judgmental approach to setting the hypothesized path of house prices by tying this variable to disposable personal income. The result would be a more countercyclical path of house prices and increased transparency into how we determine the severity of this very important element of the scenario.

Beyond these steps, we heard many ideas during our review on how we might pursue our macroprudential objective by adding new features to the stress test, especially from official sector representatives and academics. We also reviewed the growing academic literature on this topic. We concluded that, to this point, even the most conceptually promising of the ideas are a good ways from being realized in specific and well-supported elements of our economic models. Many macroprudential risks involve the spread of stress from one firm or market to others. As such, macroprudential elements of stress tests often must estimate not just first-round losses, but also the knock-on effects, which depend significantly on the vulnerabilities and responses of all other major actors in the financial system, including many that we do not regulate. Modelling these effects requires information about the behavior of those actors that may not be observable either to a firm or to us.

Notwithstanding these and other practical challenges, many of the suggestions we received have focused on important potential risks that bear further inquiry by regulators. Hence we will be undertaking a research program to pursue these ideas in order to better understand the quantitative consequences of new risks and business activities, potential amplification channels such as fire sales by which stress could migrate from the large banks to the rest of the financial system, and important dynamics between capital and liquidity positions. At a minimum, this research should inform scenario design and the overall regulatory and financial stability functions of the Board. And at least some of the ideas might eventually be translated into features of the stress testing regime. Over the medium term we view three related areas as the highest priorities: funding shocks, liquidity shocks, and spillovers from the default of common counterparties.

Funding shocks

Funding stresses are a natural starting point. As banks incur losses and their capital base erodes, some of their creditors will demand additional compensation and bank funding costs will increase. This kind of "direct" funding shock is really microprudential because the resulting losses depend largely on the bank's own decisions about its capital base, asset risk, and reliance on short-term wholesale funding. As such, it should be more straightforward to integrate direct funding shocks into our main stress testing framework than to integrate systemwide effects, and we will consider whether, and how, to do so in the relatively near term.

In a "systemic" funding shock, by contrast, each bank's cost of funds depends on the capital position of the system as a whole. By taking the overall solvency of the system into account, this element captures a key amplification channel evident during the last financial crisis. As the banking system experienced capital losses, the cost of funding increased and some wholesale funding markets shut down even for relatively healthy banks. The potential for this kind of funding shock means that the presence of a poorly capitalized bank might increase funding costs for all banks--a classic kind of macroprudential concern.

Liquidity shocks and fire sale dynamics

As we saw during the last financial crisis, repo and other funding markets can simply close to distressed institutions, which are then unable to access certain kinds of funds at any price. Such a firm may then be forced to make up the funding shortfall by turning to market sources of liquidity by selling assets--both high-quality liquid assets like Treasury securities and less liquid assets. During the financial crisis, distressed firms sold large amounts of securities as quickly as possible. The fire sale price discounts required for such rapid execution in turn imposed mark-to-market losses on other firms with similar holdings. To understand better this channel of financial contagion, we intend to continue our work on the ability of markets to handle large quantities of asset sales under stress, the capacity and willingness of firms to tap their buffers of high-quality assets, and the susceptibility of bank capital to mark-to-market losses from fire sales.

Many commentators have drawn attention to these concerns, and some have advocated an integrated approach to capital and liquidity stress testing. We may or may not be able to achieve this end point. At a minimum, though, research in this area will allow us to move in this direction, perhaps by using the conclusions reached in the annual stress test as a starting point for our annual Comprehensive Liquidity Analysis and Review (CLAR), or vice versa. The results could also shed light on the current calibration of our liquidity rules.

Default of a common counterparty and the reaction of central counterparties

Currently, the annual stress test incorporates a counterparty default scenario component for the eight G-SIBs that measures direct credit loss. However, this component does not consider the potentially large second-round effects of the default of a major financial institution, including an increase in the probability of default of other counterparties as a result of the initial default and requirements for larger margins from derivatives counterparties. Of particular interest is the role of central counterparties (CCPs) in alleviating or transmitting stress from the default of one of their members. By regulatory design, CCPs have increased in prominence in the post-crisis environment because they can lead to greater efficiency and transparency in trading. But this increased role makes it important to understand the impact they may have in stressed conditions. For example, CCPs collect prefunded resources that can mitigate the impact of a default, but also can call on surviving clearing members for additional financial resources if those pre-funded resources are exhausted.

Promoting transparency

Transparency has played an important role in making stress testing such a key part of post-crisis prudential regulation. Transparency of the scenarios and results gives investors and analysts valuable information about the condition of the tested banks, thereby contributing to market discipline. It also allows the public to evaluate the job that the Federal Reserve is doing. For example, analysts can compare our loss estimates for specified portfolios under specified stress conditions with their own evaluations--an exercise that can inform both the analysts and us.

There are three areas in which transparency considerations need to be applied. First is the set of scenarios applied in the annual exercise. We release essentially all details of the scenarios and, further, have published a policy statement exploring the aims and factors relevant to development of the scenarios.18

Second is the set of results of the DFAST and CCAR exercises themselves. Right from the start--during the Supervisory Capital Assessment Program (SCAP) in 2009--we adopted what was then the controversial practice of publishing post-stress capital ratio results for each participating firm, along with a breakdown of the projected losses by loan type. Since then, we have substantially increased the breadth of the disclosed results, including a summary of the reasons for any qualitative objection or conditional non-objection to firms' capital plans. During the course of our review, suggestions were made for more granular disclosures, such as providing more details on different components of projected net revenues. We will make this change, and possibly a few others, over the course of the next cycle or two of stress testing.19

The third area for transparency involves the supervisory models used in the stress tests. Banks involved in DFAST/CCAR have regularly requested more disclosures so that they can better understand the likely impact on their firms. One argument has been that banks will have a difficult time in their capital planning if they cannot predict how loss functions and other model features will affect their stress losses. In part to remove the possibility that a bank would receive a quantitative objection to its capital plan because of a large gap between their loss estimates and those produced by the supervisory model, a few years ago we began allowing banks to revise their capital distribution requests following receipt of their DFAST results. Under the SCB approach, a bank could also adjust its planned capital distributions after receiving the stress test results to avoid having its baseline capital distribution projections fall into the buffer.

We have already taken a number of steps to respond to these requests. We currently publish descriptions of all models used in the stress test, including the key risk drivers and scenario variables for each key modeling area. We host an annual conference about modelling practices. We disclose a description of the most material changes to stress test models before each stress test. We are considering further steps, such as disclosing descriptions of changes well in advance of the stress test, and phasing in the most material model changes over two years, so as to smooth somewhat the effects of the changes on projected losses or revenues. Finally, and a bit more tentatively, we are assessing the feasibility of publishing data that represent typical bank portfolios of loans and securities with the losses we would project for those portfolios under various stress scenarios. This kind of information could also help the public trace how changes in risk drivers alter loss projections.

Having said all this, let me now say that we do not intend to publish the full computer code in the supervisory model that is used to project revenues and losses. Full disclosure would permit firms to game the system--that is, to optimize portfolio characteristics based on the parameters of the model and take risks in areas not well-captured by the stress test just to minimize the estimated stress losses. In part for this reason, full disclosure could promote a "model monoculture" in which both supervisors and firms use the same models to evaluate risks. A critical part of the DFAST/CCAR process is that firms use their own models to assess their risks. We do not want them simply to copy the supervisory model and thereby increase the vulnerability of the financial system to the inevitable blind spots in even the best models.

In short, this is not like using a model to develop a regulation that, for example, limits emissions of polluting substances. In such a case, adherence to the precise model output would itself achieve the regulatory purpose. Here, by contrast, the very purpose of the regulatory regime would be undermined. Remember, this is a stress test. The shifts in activities of banks and in the economy create a dynamic set of risks. Effective prudential regulation must be equally dynamic and should try to avoid pushing major financial firms toward measuring all of their risk positions in exactly the same way.

There is, however, one additional consideration. Because the stress tests would be undermined by giving the models to the banks, there are of course limited opportunities for external parties to assess the models. To promote the integrity of the models in these circumstances, we established a Model Validation Group, which is composed of modelling experts who are not involved in the design and application of the stress test models. They make regular assessments and offer suggestions for improvement. We expect to be providing the public greater information on our internal validation processes.

Eliminating the qualitative CCAR exercise for smaller firms

As you can already tell, our responses to the need for better alignment of the stress test with our capital rules and to the desirability of more macroprudential emphasis each required a good bit of explanation. In contrast, our response to the issue of the unnecessary burden on smaller, less complex CCAR firms is both simply stated and simply achieved.

In a notice of proposed rulemaking that the Board is releasing today we are proposing that banks with less than $250 billion in assets that do not have significant international or nonbank activity would no longer be included in the annual CCAR qualitative review. As noted earlier, many of these firms have already met supervisory expectations. We do not intend for less complex firms to invest in stress testing capabilities on par with the most complex firms and, given their profile, we feel these firms can maintain the progress they have made through the normal supervisory process, supplemented with targeted horizontal reviews of discrete aspects of capital planning.

This shift will reduce the intensity of supervision of their capital planning processes, remove any uncertainty as to supervisory expectations for their firms relative to the largest firms, and eliminate the possibility of a public objection to their capital plans on qualitative grounds. They would still be included in the quantitative side of the stress test and the proposed stress capital buffer. But we are also proposing to reduce the amount of data these firms are required to submit for the purpose of running the stress test, on what we call the Y-14 regulatory reports. Unlike the other substantial changes we are contemplating to CCAR and our stress test, we are proposing that these changes would be effective next year, for CCAR 2017.

Conclusion

This set of changes we are considering for our stress testing regime has been motivated by somewhat different considerations, against the backdrop of what we intend to remain a dynamic regulatory instrument whose procedures will be regularly refined and whose substance will be regularly adapted to changing economic conditions and industry practices. Still, in pulling this package of modifications together, we have consciously shaped them in accordance with the principle that financial regulation should be progressively more stringent for firms of greater importance, and thus potential risk, to the financial system. Two features of the package reflect this principle.

First, of course, is the elimination of the qualitative portion of CCAR for nearly all the firms with less than $250 billion in assets, along with some record keeping and reporting requirements.

The second key feature is the differential impact the better alignment of CCAR with our capital regulations will have on the roughly 30 firms that are covered. Let me note at the outset that the precise effects on the capital requirements of individual firms cannot be determined because of the very nature of the stress test regime. The scenarios vary from year to year, and the resulting projected effects on losses and revenues may also vary materially depending on the composition of a firm's balance sheet and activities. However, to provide some idea of what the impact may be, we assessed how the various changes I have mentioned would have affected capital requirements in the two most recent CCAR cycles. On average for the eight GSIBs, integration of the surcharge with the post-stress requirements would have been somewhat less than half offset by the simplifying changes in the prefunding of capital distributions and balance sheet assumptions. The impact on capital requirements will likely be greater for firms with larger GSIB surcharges.

For the other CCAR firms, for which there are no capital surcharges, these simplifying assumptions will result in some reduction of post-stress capital requirements. We estimate that the aggregate impact of these changes for the CCAR firms as a whole should be a modest increase in the total amount of required capital. But this increase will be totally due to the impact on the eight GSIB firms, whose increased capital requirements will more than offset the reductions for the other firms.

In short, the GSIBs will see their capital requirements rise. All other CCAR firms will see some reduction in their capital requirements. And firms that have less than $250 billion in assets and do not have extensive international or nontraditional banking activities will also transition to a more tailored set of capital planning expectations outside the CCAR process.

1. Dodd-Frank Act §165(i), 12 U.S.C. §5365(i). Return to text

2. For a more complete description of the Federal Reserve's DFAST and CCAR programs, see www.federalreserve.gov/bankinforeg/stress-tests-capital-planning.htm. As a formal matter, DFAST was implemented beginning in 2013. However, in 2011 and 2012, the Federal Reserve conducted supervisory stress tests as part of its CCAR program, as explained later in the text. Return to text

3. 12 CFR 225.8. Return to text

4. The common equity capital ratio--which compares high-quality capital to risk-weighted assets--of the 33 bank holding companies in the 2016 CCAR has more than doubled from 5.5 percent in the first quarter of 2009 to 12.2 percent in the first quarter of 2016. This reflects an increase of more than $700 billion in common equity capital to a total of $1.2 trillion during the same period. www.federalreserve.gov/newsevents/press/bcreg/20160629a.htm. Return to text

5. The 2016 CCAR cycle started one quarter later than past years' CCAR cycles. Return to text

6. For example, our regulatory capital rules now include a minimum requirement based on common equity, reflecting the fact that common equity provides the best buffer against losses. As a result, the similar common equity requirement that had been included in the early years of CCAR, to meet an additional post-stress target ratio of tier 1 common equity, was removed after CCAR 2015. Other changes that have been integrated into the stress test include modification of the risk-weighted asset calculation methodologies and revised definitions of capital. Return to text

7. Daniel K. Tarullo (2013), "Macroprudential Regulation," speech delivered at the Yale Law School Conference on Challenges in Global Financial Services, New Haven, CT, September 20. Return to text

8. See, for example, David Greenlaw, Anil Kashyap, Kermit Schoenholtz, and Hyun Song Shin (2012), "Stressed Out: Macroprudential Principles for Stress Testing." Chicago Booth Research Paper No. 12-08, Fama-Miller Working Paper (Chicago: University of Chicago Booth School of Business, February 13). Return to text

9. The countercyclical buffer applies to banking organizations with more than $250 billion in assets or $10 billion in on-balance-sheet foreign exposures and to any depository institution subsidiary of such organizations. See 12 CFR Part 217, Appendix A. Return to text

10. Figure 1 further illustrates the stress capital buffer. Return to text

{kind=link}

11. Board of Governors of the Federal Reserve System (2015), "Calibrating the G-SIB Surcharge," white paper (Washington: Board of Governors of the Federal Reserve System, July 20). Return to text

12. See Beverly Hirtle (2014), "Bank Holding Company Dividends and Repurchases during the Financial Crisis (PDF)," Staff Report No. 666 (New York: Federal Reserve Bank of New York, March). Return to text

13. Were a countercyclical capital buffer to be imposed, it would be added to the buffers above the 4.5 percent minimum capital requirement. Return to text

14. During the financial crisis, firms began to curtail share repurchases beginning in 2007 but generally did not cut dividends until late 2008. See Hirtle (2014). Return to text

15. The original stress test undertaken during the crisis did not allow this assumption, precisely because of our aim that the large banks as a group be well-positioned to meet the needs of creditworthy borrowers at that time of great stress. Return to text

16. See 12 CFR part 252, appendix A. Return to text

17. See 12 CFR Part 252, Appendix A. Return to text

18. See 12 CFR 252, appendix A; Board of Governors of the Federal Reserve System (2013), "Policy Statement on the Scenario Design Framework for Stress Testing (PDF)," Final Rule; Policy Statement, November 29. Return to text

19. Quite recently some banks have also suggested disclosing some version of the supervisory letters we send following the annual CCAR to each participating firm detailing our assessment of their capital planning processes. These banks believe that analysts and investors could benefit from knowing more detail on the concerns of the supervisors. We had already been considering how to increase the information provided around qualitative objections or conditional non-objections and will factor these latest observations into this decision. Return to text