FEDS Notes

September 13, 2018

A Wealthless Recovery? Asset Ownership and the Uneven Recovery from the Great Recession

Lisa Dettling, Joanne Hsu and Elizabeth Llanes

Aggregate measures of household wealth have broadly followed the business cycle. Between 2007 and 2009, American households as a whole lost 20 percent of their wealth.1 Household wealth increased during the economic recovery from its nadir in the Great Recession, and by late 2012, aggregate household net worth surpassed its previous 2007 peak, and continued to grow through 2016.

These aggregate patterns obscure the extent to which gains from the recovery are shared across the population. Wealth is highly concentrated--as of 2016, 80 percent of aggregate wealth was held by only 10 percent of households (Bricker et al., 2017)--which suggests that aggregate wealth measures may insufficiently describe how most households fared financially in the recent economic recovery.2 Such an analysis requires detailed microdata on the wealth of households, including enough coverage of the top of the wealth distribution to differentiate their experiences from those of the rest of the population.

In this Note, we turn to data from the Federal Reserve Board's triennial Survey of Consumer Finances (SCF) to examine trends in the distribution of household wealth during the Great Recession and subsequent recovery. The SCF is ideally suited for our purposes because it includes an oversample of wealthy families and a weighting scheme that allows for comparisons across the entire distribution of wealth, including the very top. The SCF also allows us to construct a broad measure of household wealth that includes financial assets and liabilities (including IRAs and retirement accounts), the value of vehicles less any debt against them, the value of any homes or other properties owned less their debt, and the net value of any businesses.3

Trends in the distribution of household wealth during the Great Recession and recovery

We examine the evolution of wealth for different types of families, where families are grouped according to their reported "usual income." Usual income is a measure of family resources that smooths away temporary fluctuations in income, such as an unexpected bonus or a temporary unemployment spell. We divide the usual income distribution into four groups. First, given the well-documented concentration of wealth at the top, we separately examine the top 10 percent of families by usual income (the "Top 10"). Then, we split the other 90 percent of the distribution (the "Bottom 90") into three equal-sized groups: the "Bottom 30" (the bottom 30 percent), "Middle 30" (the 31st to 60th percentile), and the "Next 30" (61st to 90th percentile). We restrict our analysis to working-age households, defined as those headed by individuals between the ages of 25 and 64, to facilitate comparisons over time.4

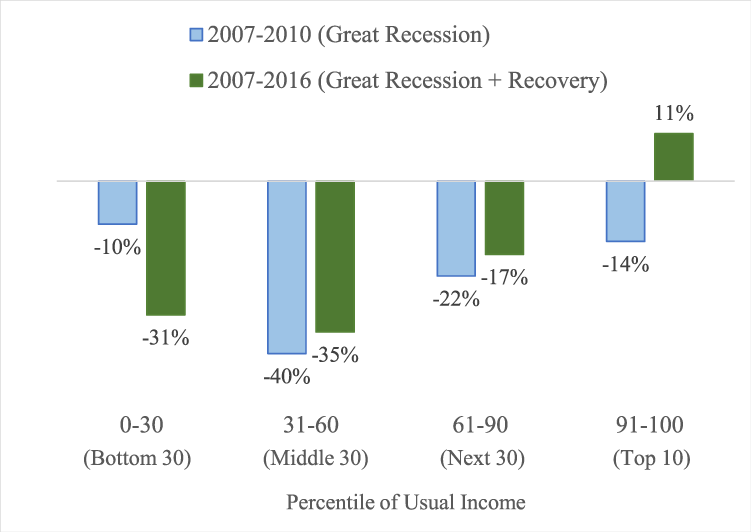

Figure 1 displays changes in real mean wealth for the four income groups during the Great Recession and recovery, as captured in the triennial SCF.5 The bars show changes in wealth since the 2007 SCF, or just before the onset of the Great Recession. The blue bars show changes in wealth through 2010--roughly the end of the Great Recession as captured in the triennial SCF. And the green bars show changes in wealth through 2016--the most recent survey year. This time period includes both the recession and a substantial portion of the recovery.

Source: Survey of Consumer Finances 2007-2016.

During the Great Recession, wealth fell for all usual income groups, although some groups lost more wealth than others (Figure 1, blue bars). The Middle 30 experienced the largest percentage losses in wealth from $214,000 to $128,000. The Next 30 also faced substantial wealth losses, from $510,000 to $395,000. For the Bottom 30, wealth fell from $83,000 to $75,000. The Top 10's wealth dropped from $3.7 million to $3.2 million.

In 2016--well into the recovery--wealth remained below 2007 levels for all three subgroups in the Bottom 90, but the Top 10 had more wealth than in 2007 (Figure 1, green bars). In 2016, average wealth was $57,000 for the Bottom 30, $139,000 for the Middle 30, and $424,000 for the Next 30; all of these values were below 2007 levels. On the other hand, the Top 10's 2016 mean wealth was $4.1 million, well above the 2007 value.6

The Bottom 90 and Top 10 alike lost wealth during the Great Recession (figure 1, blue bars). However, the changes in wealth during the cumulative Great Recession and recovery period (figure 1, green bars) illustrate that the Bottom 90 and the Top 10 had vastly different experiences during the recovery. The Bottom 90 experienced little to no wealth gains, whereas the Top 10 experienced outsized gains. The remainder of this note will unpack some determinants and implications of families' varied experiences in the Great Recession and subsequent recovery.

Why did some families experience larger wealth losses 2007-2010?

Between 2007 and 2010, house prices fell 23 percent and stock prices fell 21 percent, but these changes affected household wealth differently for the Bottom 90 and Top 10.7 The first reason for this differential effect stems from variation in families' portfolios before the Great Recession. In 2007, the primary residence represented more than a third of wealth of the Bottom 90, compared with 15 percent for the Top 10, making the Bottom 90's total wealth relatively more sensitive to changes in house prices (Table 1). Furthermore, families in the Bottom 90 also stored a non-negligible share of their wealth in stocks, making them sensitive to changes in stock prices as well. In contrast, families in the Top 10 held a relatively larger proportion of their wealth outside of these two types of assets, making their wealth less sensitive to changes in home and stock prices.

Table 1: Wealth concentration and leverage in 2007

| Bottom 30 (0-30) |

Middle 30 (31-60) |

Next 30 (61-90) |

Top 10 (91-100) |

|

|---|---|---|---|---|

| Share of wealth in... | ||||

| ...housing | 45% | 41% | 33% | 15% |

| ...stocks | 11% | 15% | 21% | 24% |

| ...other | 44% | 44% | 46% | 61% |

| Share of homeowners with mortgage LTV over 80 percent | 13% | 22% | 16% | 6% |

Note: Stock wealth includes stocks held directly and indirectly. Housing wealth and debt includes the primary residence only.

Source: Survey of Consumer Finances.

A second reason for the differential effect of price declines in the Great Recession is differences in leverage. In particular, the Bottom 90 were more leveraged on their homes before the Great Recession and thus suffered larger proportional declines in wealth when house prices fell. Families in the Middle 30 were the most leveraged group: 22 percent of owners had mortgage LTVs of more than 80 percent (Table 1) and thus would have had their housing wealth erased by the 23 percent decline in home prices that occurred in the Great Recession. Because families in the Top 10 were considerably less leveraged on their homes than other families, their total wealth was more insulated from the house prices declines.

Why has the recovery been weak for the Bottom 90?

The patterns above can explain why families in the Bottom 90 experienced larger proportional losses during the Great Recession than the Top 10, but not why their recovery has also been weaker. By 2016, house prices had increased by 26 percent from their trough, and stock prices had risen by more than 160 percent: so why haven't families in the Bottom 90 shared in those gains?

One reason the Bottom 90 experienced little to no recovery is their homeownership rate declined between 2007 and 2016 (Table 2). Families who do not own a home will not experience an increase in housing wealth when house prices rise.

Table 2: Homeownership rates and decomposition of increase in renter share

| Bottom 30 (0-30) |

Middle 30 (31-60) |

Next 30 (61-90) |

Top 10 (91-100) |

|

|---|---|---|---|---|

| Share of families that are homeowners... | ||||

| ...in 2007 | 41% | 71% | 89% | 91% |

| ...in 2016 | 33% | 59% | 81% | 92% |

| Change in renter share 2007-2016*... | 7% | 12% | 8% | 0% |

| ...previously owned a home | -1% | 3% | 3% | 0% |

| ...never owned a home | 9% | 9% | 5% | 0% |

* May not sum due to rounding.

Source: Survey of Consumer Finances 2007, 2016.

Further inspection of the data indicates that the decline in homeownership for the Bottom 90 can be explained by a decline in first-time home buying. Between 2007 and 2016, the share of families in the Bottom 90 who have never owned a home (e.g., families who would become first-time buyers if they did purchase homes) increased, while the share of renters who used to own a home (perhaps due to a previous foreclosure) fell or increased only modestly (Table 2).

What explains this decline in first time home-buying among the Bottom 90? Several recent papers indicate that a reduction in mortgage credit availability is a likely culprit (Acolin et al, 2016; Bhutta, 2015). Also, the SCF shows that rent-to-income ratios rose between 2 and 9 percentage points for renters in the Bottom 90 during this time period, which would have reduced renter families' ability to save for a down payment.8

A second reason the Bottom 90 has not experienced a stronger recovery is that stock market participation has declined since 2007. Between 2007 and 2016, stock market participation--defined as holding stocks directly or indirectly, such as through a pooled investment fund or a defined contribution retirement account like a 401 (k) or IRA--fell for the Bottom 30 and Middle 30, but increased slightly or was unchanged for the Next 30 and Top 10 (Table 3).

Table 3: Stock Market Participation and the availability of employer-sponsored retirement plans

| Bottom 30 (0-30) |

Middle 30 (31-60) |

Next 30 (61-90) |

Top 10 (91-100) |

|

|---|---|---|---|---|

| Share of families that participate in stock market.... | ||||

| ...in 2007 | 24% | 56% | 80% | 93% |

| ...in 2016 | 20% | 50% | 80% | 95% |

| Change in share of families that do not participate in stock market 2007-2016*... | 4% | 6% | -1% | -2% |

| ...employer plan available, but does not participate | -2% | 1% | 0% | 0% |

| ...employer plan not available... | 6% | 5% | 0% | -2% |

| ...part-time at main job(s) | 7% | 2% | 0% | -1% |

| ...full-time at main job(s) | -4% | 0% | 0% | -1% |

| ...not working | 3% | 2% | 0% | 0% |

* May not sum due to rounding.

Data source: Survey of Consumer Finances 2007, 2016.

Why did stock market participation decline among the Bottom 30 and Middle 30, but not the Next 30 or Top 10? Table 3 reveals differential declines in retirement plan eligibility across groups. Most families in the Bottom 90 only hold stocks through defined contribution retirement accounts, such as 401(k)s or IRAs. Between 2007 and 2016, the share of families in the Bottom 30 and Middle 30 with access to retirement plans through an employer dropped by 5 to 6 percentage points. Most of this decline in plan availability appears to stem from changes in work patterns between 2007 and 2016: families in the Bottom and Middle 30 were more likely to work part-time at the their main job, or not work at all (due to declining participation rates and elevated unemployment rates), which would typically make those families ineligible to participate in employer-sponsored plans (Table 3). These changes in plan eligibility also appear related to the increase in contract work and the gig-economy, since those jobs are often part-time and typically do not offer plans (GAO, 2015; Katz and Krueger, 2016).

What would the recovery look like for the Bottom 90 if homeownership and stock market participation had not declined between 2007 and 2016? We can conduct a counterfactual exercise where we assume group-level homeownership and stock market participation rates had remained at their 2007 level and allow each group's wealth to be affected by changes in home and stock prices that occurred between 2007 and 2016.9 The results of this experiment reveal that the changes in asset ownership described in this Note played a key role in generating a "wealthless recovery": Bottom 90 wealth would be 50-60 percent higher in 2016 if home ownership and stock market participation rates had not fallen (Table 4).

Table 4: Counterfactual change in Bottom 90 wealth 2007-2016 assuming 2007 home and stock ownership rates

| Bottom 30 (0-30) |

Middle 30 (31-60) |

Next 30 (61-90) |

||

|---|---|---|---|---|

| Change in wealth 2007-2016 | ||||

| ...actual | -31% | -35% | -17% | |

| ...assuming 2007 ownership rates | -12% | -20% | -9% | |

Source: Survey of Consumer Finances 2007-2016.

Implications for wealth inequality and future outlook

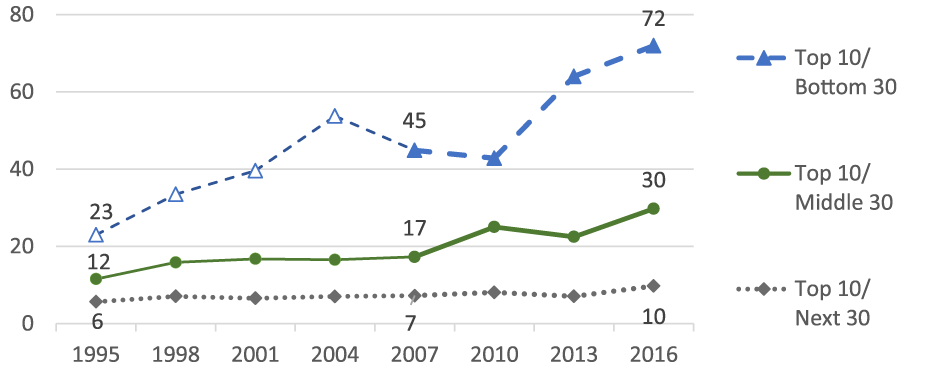

One measure of wealth inequality is the ratio of the mean wealth of the top 10 to mean wealth of each subgroup of the Bottom 90. In 2007, that measure shows that the Top 10 had 45 times as much wealth as the Bottom 30, 17 times as much wealth as the Middle 30, and 7 times as much wealth as the Next 30 (Figure 2, solid markers). By 2016, those rates had increased substantially; the Top 10 had 72 times as much wealth as the Bottom 30, 30 times as much wealth as the Middle 30, and 10 times as much wealth as the Next 30. Furthermore, those ratios are considerably higher than any other time period going back to the mid-1990s (Figure 2, hollow markers).

Source: Survey of Consumer Finances, 1995-2016.

This note has uncovered a divergence between changes in aggregate wealth and most families' wealth in the recovery from the Great Recession. The resulting increase in wealth inequality has important implications for understanding the recovery. For example, it may help explain why the long-standing connection between aggregate wealth and consumption is weaker than it once was, since higher income families tend to consume less out of wealth changes than lower income families (see Aladangady and Feiveson, 2018 for more on recent developments in the consumption-wealth relationship).

Furthermore, because these declines in wealth for the Bottom 90 are driven in part by declines in asset ownership, the outlook for the Bottom 90 as the economic recovery continues will depend on asset ownership rates. Recent data provides little evidence ownership rates have rebounded: for example, as of the second quarter of 2018, the home ownership rate was still below its 2007 level; and although data comparable to the SCF measure of stock market participation is not available, the share of families not participating in a retirement plan, as well as the share working part time, were still elevated relative to 2007.10 This suggests the wealth gaps uncovered in this Note may persist despite the continued economic recovery, as those families will not experience wealth gains from the rise in housing and stock prices since 2016. Data from the next SCF in 2019 will help to further uncover whether this "wealthless recovery" for the Bottom 90 persists.

References

Acolin, Arthur, Jesse Bricker, Paul Calem, and Susan Wachter. 2016. "Borrowing Constraints and Homeownership," American Economic Review: Papers and Proceedings, 106(5): 625-629.

Aladangady, Aditya and Laura Feiveson. 2018. A Not-So-Great Recovery in Consumption: What is Holding Back Household Spending? FEDS Notes, March 8, 2018.

Bhutta, Neil. 2015. "The Ins and Outs of Mortgage Debt during the Housing Boom and Bust," Journal of Monetary Economics, 76: 284-298.

Bricker, Jesse, Alice Henriques, Jacob Krimmel, and John Sabelhaus. 2016. "Measuring Income and Wealth at the Top Using Administrative and Survey Data," Brookings Papers on Economic Activity, Spring, pp. 261-321

Bricker, Jesse, Lisa Dettling, Alice Henriques, Joanne Hsu, Lindsay Jacobs, Kevin B. Moore, Sarah Pack, John Sabelhaus, Jeffrey Thompson, and Richard Windle. 2017. Changes in U.S. Family Finances from 2013 to 2016: Evidence from the Survey of Consumer Finances Federal Reserve Bulletin 103(3).

Katz, Larry and Alan Krueger, 2016 "The Rise and Nature of Alternative Work Arrangements in the United States, 1995-2015" NBER Working Paper #22667

U.S. Government Accountability Office. 2015. "Contingent Workforce: Size, Characteristics, Earnings, and Benefits," retrieved from http://www.gao.gov/assets/670/669766.pdf on April 17, 2018

1. Financial Accounts of the United States, 2007Q2 to 2009Q1, available at www.federalreserve.gov/releases/z1. Return to text

2. See Bricker, et al. (2016) for more on wealth concentration in the Survey of Consumer Finances. Return to text

3. See Bricker, et al. (2017) for more details on the definition of net worth used here to measure household wealth. Return to text

4. We focus on working-age households to ensure that our comparisons are not confounded by time-varying factors that disproportionately affect young and old households. For example, the retirement of the baby boomer cohort might complicate comparisons over time if we were to examine families of all ages, since retired households tend to have low levels of retirement income, but wealth levels that reflect their higher pre-retirement income. Younger households can also complicate the analysis, since college-going tends to increase occurs during a recession and students' income and wealth levels are often low. Return to text

5. All dollar amounts from the SCF for this Note are adjusted to 2016 dollars using the CPI-U-RS. Return to text

6. We choose to focus primarily on mean values because we want to discuss the behavior of the group as whole and because the ability to add together values from subgroups is an important aspect of our analysis. But medians reflect a similar story from 2007 to 2016: median wealth fell from $13,000 to $8,000 for the Bottom 30, $99,000 to $55,000 for the Middle 30, and $318,000 to $195,000 for the Next 30. Additionally median wealth rose from $1.335 million to $1.460 million for the Top 10. Return to text

7. Changes between September 2007 and September 2010 (roughly the median SCF interview dates) were computed using Case-Shiller index and Wilshire index, both inflation-adjusted to 2016 dollars). Return to text

8. Another possibility is that preferences for home ownership declined among the Bottom 90, but there is little empirical evidence to support that notion. For example, surveys show that most renters would prefer to be owners, and crucially, there is very little difference in these preferences across high and low income renters over time, which would be consistent with the home-buying patterns observed in the SCF (Authors calculations from data in the FRBNY Survey of Consumer Expectations https://www.newyorkfed.org/microeconomics/sce). Return to text

9. This counterfactual exercise was conducted by estimating housing wealth, stock wealth and all other wealth for each income groups. Stock wealth is estimated by aging forward the group's 2007 stock wealth using the Wilshire Index. To estimate housing wealth, we first estimate mean mortgage LTVs by housing tenure, where tenure is defined as: owning current home less than 10 years, 10-20 year or 20 or more years. We then estimate 2007 house values by tenure, and age those values forward using the average change in the local FHFA house price index experienced by each group between 2007 and 2016. We combine the house values and mortgage LTVs to construct a weighted mean value of home equity, where the weights are the 2007 tenure distribution. The intuition behind targeting the tenure distribution is to match entry rates into first, second, third, etc. time home buying that was present in 2007. To estimate other wealth, we used mean group-level non-housing, non-stock wealth by housing tenure and stock ownership, and construct a weighted average using the 2007 tenure distribution and stock ownership rate as weights. Return to text

10. As of 2018 Q2 the homeownership rate was 64.3 percent, well below the 2007 Q2 rate of 68.2 percent, and only slightly above the 2016 Q2 rate of 62.9 percent (see https://www.census.gov/housing/hvs/index.html). As of March 2017, the share of persons age 25-64 participating in a pension at work was 26.6 percent, compared to 35.3 percent in 2007 and 27.7 percent in 2016 (Author's calculations based on data from https://www.bls.gov/cps). As of 2018 Q2 the share of adult persons usually working part time was 13.2 percent, up from 12.9 percent in 2007 Q2 and only slightly below the 13.5 percent observed in 2016 Q2 (Authors calculations based on data from https://www.bls.gov/ces). Return to text

Dettling, Lisa J., Joanne W. Hsu, and Elizabeth Llanes (2018). "A Wealthless Recovery? Asset Ownership and the Uneven Recovery from the Great Recession ," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, September 13, 2018, https://doi.org/10.17016/2380-7172.2249.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.