October 17, 2016

Why Are Interest Rates So Low? Causes and Implications

Vice Chairman Stanley Fischer

At the Economic Club of New York, New York, New York

I am grateful to the Economic Club of New York for inviting me to speak today. My subject is the historically low level of interest rates, a topic not far from the minds of many in this audience and of many others in the United States and all over the world.1

Notwithstanding the increase in the federal funds rate last December, the federal funds rate remains at a very low level. Policy rates of many other major central banks are lower still--even negative in some cases, even in countries long famous for their conservative monetary policies. Long-term interest rates in many countries are also remarkably low, suggesting that participants in financial markets expect policy rates to remain depressed for years to come. My main objective today will be to present a quantitative assessment of some possible factors behind low interest rates--and also of factors that could contribute to higher interest rates in the future.

Now, I am sure that the reaction of many of you may be, "Well, if you and your Fed colleagues dislike low interest rates, why not just go ahead and raise them? You are the Federal Reserve, after all." One of my goals today is to convince you that it is not that simple, and that changes in factors over which the Federal Reserve has little influence--such as technological innovation and demographics--are important factors contributing to both short- and long-term interest rates being so low at present.

There are at least three reasons why we should be concerned about such low interest rates. First, and most worrying, is the possibility that low long-term interest rates are a signal that the economy's long-run growth prospects are dim. Later, I will go into more detail on the link between economic growth and interest rates. One theme that will emerge is that depressed long-term growth prospects put sustained downward pressure on interest rates. To the extent that low long-term interest rates tell us that the outlook for economic growth is poor, all of us should be very concerned, for--as we all know--economic growth lies at the heart of our nation's, and the world's, future prosperity.

A second concern is that low interest rates make the economy more vulnerable to adverse shocks that can put it in a recession. That is the problem of what used to be called the zero lower bound on interest rates. In light of several countries currently operating with negative interest rates, we now refer not to the zero lower bound, but to the effective lower bound, a number that is close to zero but negative. Operating close to the effective lower bound limits the room for central banks to combat recessions using their conventional interest rate tool--that is, by cutting the policy interest rate. And while unconventional monetary policies--such as asset purchases, balance sheet policies, and forward guidance--can provide additional accommodation, it is reasonable to think these alternatives are not perfect substitutes for conventional policy. The limitation on monetary policy imposed by low trend interest rates could therefore lead to longer and deeper recessions when the economy is hit by negative shocks.

And the third concern is that low interest rates may also threaten financial stability as some investors reach for yield and compressed net interest margins make it harder for some financial institutions to build up capital buffers. I should say that while this is a reason for concern and bears continual monitoring, the evidence so far does not suggest a heightened threat of financial instability in the post-financial-crisis United States stemming from ultralow interest rates. However, I note that a year ago the Fed did issue warnings--successful warnings--about the dangers of excessive leveraged lending, and concerns about financial stability are clearly on the minds of some members of the Federal Open Market Committee, FOMC.

Those are three powerful reasons to prefer interest rates that are higher than current rates. But, of course, Fed interest rates are kept very low at the moment because of the need to maintain aggregate demand at levels that will support the attainment of our dual policy goals of maximum sustainable employment and price stability, defined as the rate of inflation in the price level of personal consumption expenditures (or PCE) being at our target level of 2 percent.

That the actual federal funds rate has to be so low for the Fed to meet its objectives suggests that the equilibrium interest rate--that is, the federal funds rate that will prevail in the longer run, once cyclical and other transitory factors have played out--has fallen.2 Let me turn now to my main focus, namely an assessment of why the equilibrium interest rate is so low.

To frame this discussion, it is useful to think about the real interest rate as the price that equilibrates the economy's supply of saving with the economy's demand for investment. To explain why interest rates are low, we look for factors that are boosting saving, depressing investment, or both.3 For those of you lucky enough to remember the economics you learned many years ago, we are looking at a point that is on the IS curve--the investment-equals-saving curve. And because we are considering the long-run equilibrium interest rate, we are looking at the interest rate that equilibrates investment and saving when the economy is at full employment, as it is assumed to be in the long run.

I will look at four major forces that have affected the balance between saving and investment in recent years and then consider some that may be amenable to the influence of economic policy.

The economy's growth prospects must be at the top of the list. Among the factors affecting economic growth, gains in productivity and growth of the labor force are particularly important. Second, an increase in the average age of the population is likely pushing up household saving in the U.S. economy. Third, investment has been weak in recent years, especially given the low levels of interest rates. Fourth and finally, developments abroad, notably a slowing in the trend pace of foreign economic growth, may be affecting U.S. interest rates.

To assess the empirical importance of these factors in explaining low long-run equilibrium interest rates, I will rely heavily on simulations that the Board of Governors' staff have run with one of our main econometric models, the FRB/US model. This model, which is used extensively in policy analyses at the Fed, has many advantages, including its firm empirical grounding, and the fact that it is detailed enough to make it possible to consider a wide range of factors within its structure.

Going through the four major forces I just mentioned, I will look first at the effect that slower trend economic growth, both on account of the decline in productivity growth as well as lower labor force growth, may be having on interest rates. Starting with productivity, gains in labor productivity have been meager in recent years. One broad measure of business-sector productivity has risen only 1-1/4 percent per year over the past 10 years in the United States and only 1/2 percent, on average, over the past 5 years. By contrast, over the 30 years from 1976 to 2005, productivity rose a bit more than 2 percent per year. Although the jury is still out on what is behind the latest slowdown in productivity gains, prominent scholars such as Robert Gordon and John Fernald suggest that smaller increases in productivity are the result of a slowdown in innovation that is likely to persist for some time.4

Lower long-run trend productivity growth, and thus lower trend output growth, affects the balance between saving and investment through a variety of channels. A slower pace of innovation means that there will be fewer profitable opportunities in which to invest, which will tend to push down investment demand. Lower productivity growth also reduces the future income prospects of households, lowering their consumption spending today and boosting their demand for savings. Thus, slower productivity growth implies both lower investment and higher savings, both of which tend to push down interest rates.5

In addition to a slower pace of innovation, it is also likely that demographic changes will weigh on U.S. economic growth in the years ahead, as they have in the recent past. In particular, a rising fraction of the population is entering retirement. According to some estimates, the effects of this population aging will trim about 1/4 percentage point from labor force growth in coming years.6

Lower trend increases in productivity and slower labor force growth imply lower overall economic growth in the years ahead. This view is consistent with the most recent Summary of Economic Projections of the FOMC, in which the median value for the rate of growth in real gross domestic product (GDP) in the longer run is just 1-3/4 percent, compared with an average growth rate from 1990 to 2005 of around 3 percent.7

We can use simulations of the FRB/US model to infer the consequences of such a slowdown in longer-run GDP growth for the equilibrium federal funds rate. Those simulations suggest that the slowdown to the 1-3/4 percent pace anticipated in the Summary of Economic Projections would eventually trim about 120 basis points from the longer-run equilibrium federal funds rate.8

Let me move now to the second major development on my list. In addition to its effects on labor force growth, the aging of the population is likely to boost aggregate household saving. This increase is because the ranks of those approaching retirement in the United States (and in other advanced economies) are growing, and that group typically has above-average saving rates.9 One recent study by Federal Reserve economists suggests that population aging--through its effects on saving--could be pushing down the longer-run equilibrium federal funds rate relative to its level in the 1980s by as much as 75 basis points.10

In addition to slower growth and demographic changes, a third factor that may be pushing down interest rates in the United States is weak investment. Analysis with the FRB/US model suggests that, given how low interest rates have been in recent years, investment should have been considerably higher in the past couple of years. According to the model, this shortfall in investment has depressed the long-run equilibrium federal funds rate by about 60 basis points.

Investment may be low for a number of reasons. One is that greater perceived uncertainty could also make firms more hesitant to invest. Another possibility is that the economy is simply less capital intensive than it was in earlier decades.11

Fourth on my list are developments abroad: Many of the factors depressing U.S. interest rates have also been working to lower foreign interest rates. To take just one example, many advanced foreign economies face a slowdown in longer-term growth prospects that is similar to that in the United States, with similar implications for equilibrium interest rates in the longer run. In the FRB/US model, lower interest rates abroad put upward pressure on the foreign exchange value of the dollar and thus lower net exports. FRB/US simulations suggest that a reduction in the equilibrium federal funds rate of about 30 basis points would be required to offset the effects in the United States of a reduction in foreign growth prospects similar to what we have seen in the United States.

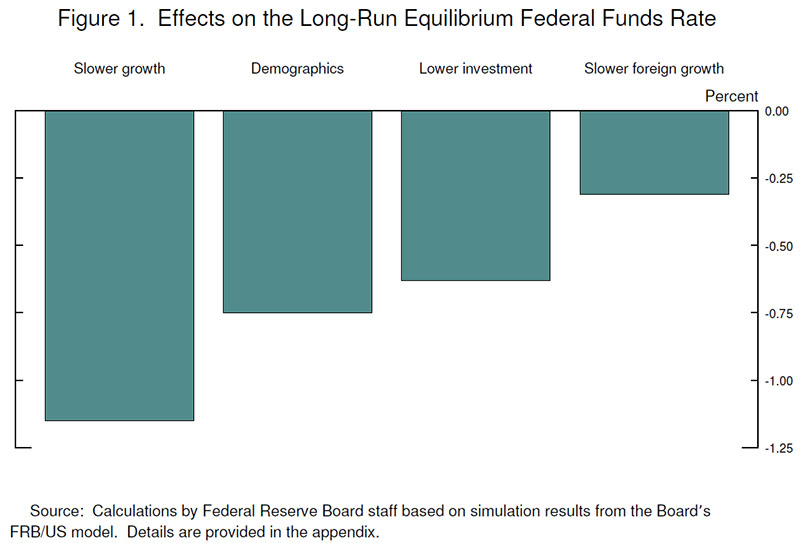

The first figure shows the effects of these four factors. You will see that each factor is considered separately; there is no attempt to add them together. That is because the broad factors we are considering here could well overlap--particularly the link between slower growth and the remaining three factors. Still, the comparison gives us a notion of the relative importance of some of the leading explanations for the decline in interest rates.

I started by noting the costs of low interest rates, including the limits on the ability of monetary policy to respond to recessions, and possible risks to financial stability. Now that we have some notion of where lower interest rates might be coming from, I want to turn to the question of what might contribute to raising longer-run equilibrium interest rates.12

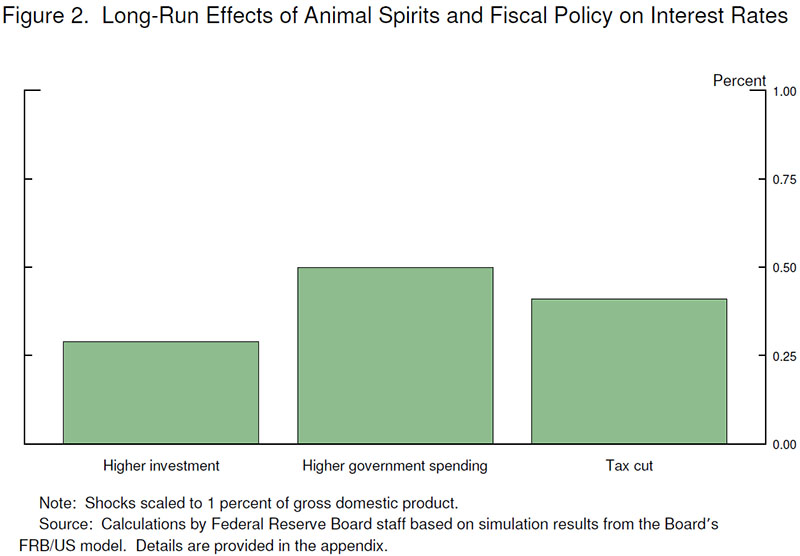

One development that would boost the equilibrium interest rate would be a further waning in the investor precaution that seems to have been holding back investment--in Keynesian terms, an improvement in animal spirits. The first bar in the second slide illustrates the effects on the longer-run equilibrium federal funds rate of an increase in business-sector investment equal to 1 percent of GDP. As can be seen, such a rebound in investment would raise the equilibrium funds rate by 30 basis points, according to the FRB/US model. In addition, higher investment would improve the longer-run growth prospects of the U.S. economy, although the effects in this particular case are fairly small, with real GDP growth about 0.1 percentage point higher on account of the higher investment.

Over the years, many economists--some of them textbook authors--have noted that expansionary fiscal policy could raise equilibrium interest rates.13 To illustrate this possibility, the next two bars on the slide show the estimated effect on interest rates of two possible expansionary fiscal policies, one that boosts government spending by 1 percent of GDP and another that cuts taxes by a similar amount. According to the FRB/US model, both policies, if sustained, would lead to a substantial increase in the equilibrium federal funds rate. Higher spending of this amount would raise equilibrium interest rates by about 50 basis points; lower taxes would raise equilibrium rates by 40 basis points. I should note that the FRB/US model does not contain a great deal of detail about taxes and government spending. These are thus the effects of very broad changes in income taxes and government spending, and not those of any specific, detailed, policy measures.

It is important to emphasize that these estimates are from just one model and other models may give different results. Still, I think these implications of fiscal policy measures are qualitatively correct--they are a standard result in many models, including the simplest textbook IS-LM model.

Stimulative fiscal policies such as these could be beneficial if the economy confronted a recession. Of course, it would be important to ensure that any fiscal policy changes during a recession did not compromise long-run fiscal sustainability.

Government policies that boost the economy's long-run growth rate would be an even better means of raising the equilibrium interest rate. This is a point I have also made in the past.14 While there is disagreement about what the most effective policies would be, some combination of more encouragement for private investment, improved public infrastructure, better education, and more effective regulation is likely to promote faster growth of productivity and living standards--and also to reduce the probability that the economy and, particularly, the central bank will in the future have to contend with the effective lower bound.

In summary, a variety of factors have been holding down interest rates and may continue to do so for some time. But economic policy can help offset the forces driving down longer-run equilibrium interest rates. Some of these policies may also help boost the economy's growth potential.

References

Aaronson, Stephanie, Tomaz Cajner, Bruce Fallick, Felix Galbis-Reig, Christopher Smith, and William Wascher (2014), "Labor Force Participation: Recent Developments and Future Prospects (PDF)," Brookings Papers on Economic Activity (Fall), pp. 197-255.

Board of Governors of the Federal Reserve System (2016), "Federal Reserve Board and Federal Open Market Committee Release Economic Projections from the September 20-21 FOMC Meeting," press release, September 21.

Carvalho, Carlos, Andrea Ferrero, and Fernanda Nechio (2016). "Demographics and Real Interest Rates: Inspecting the Mechanism (PDF)," Working Paper Series 2016-05. San Francisco: Federal Reserve Bank of San Francisco, April.

Fernald, John, and Bing Wang (2015). "The Recent Rise and Fall of Rapid Productivity Growth (PDF)," FRBSF Economic Letter 2015-04. San Francisco: Federal Reserve Bank of San Francisco, February.

Fischer, Stanley (2016). "Remarks on the U.S. Economy," speech delivered at "Program on the World Economy," a conference sponsored by The Aspen Institute, Aspen, Colo., August 21.

Gagnon, Etienne, Benjamin K. Johannsen, and David Lopez-Salido (2016). "Understanding the New Normal: The Role of Demographics (PDF)," Finance and Economics Discussion Series 2016-080. Washington: Board of Governors of the Federal Reserve System, October.

Gordon, Robert J. (2016). The Rise and Fall of American Growth: The U.S. Standard of Living since the Civil War. Princeton, N.J.: Princeton University Press.

Hamilton, James D., Ethan S. Harris, Jan Hatzius, and Kenneth D. West (2015). "The Equilibrium Real Funds Rate: Past, Present, and Future (PDF)" NBER Working Paper no. 21476 (August).

Hilsenrath, Jon and Bob Davis (2016). "Tech Boom Creates Too Few Jobs," Wall Street Journal, vol. 168, no. 88 (October 13, 2016), p. 1.

Holston, Kathryn, Thomas Laubach, and John C. Williams (forthcoming). "Measuring the Natural Rate of Interest: International Trends and Determinants," in Richard Clarida and Lucrezia Reichlin, organizers, NBER International Seminar on Macroeconomics 2016. Amsterdam: Journal of International Economics (Elsevier).

Johannsen, Benjamin K., and Elmar Mertens (2016). "The Expected Real Interest Rate in the Long Run: Time Series Evidence with the Effective Lower Bound," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, February 9.

Kiley, Michael T. (2015). "What Can the Data Tell Us about the Equilibrium Real Interest Rate? (PDF)" Finance and Economics Discussion Series 2015-077. Washington: Board of Governors of the Federal Reserve System, September.

Kocherlakota, Narayana (2015). "Public Debt and the Long-Run Neutral Real Interest Rate," speech delivered at Northwestern University, Evanston, Ill., September 8.

-------- (2016). "Write Your Congressperson! (If You Want Higher Interest Rates)," Kocherlakota's Thoughts on Policy (blog), January 19, https://sites.google.com/site/kocherlakota009/home/policy/thoughts-on-policy/1-19-16.

Laubach, Thomas, and John C. Williams (2003). "Measuring the Natural Rate of Interest," Review of Economics and Statistics, vol. 85 (November), pp. 1063-70.

Rachel, Lukasz, and Thomas D. Smith (2015). "Secular Drivers of the Global Real Interest Rate (PDF)," Staff Working Paper 571. London: Bank of England, December.

Summers, Lawrence H. (2014). "U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bound," Business Economics, vol. 49 (April), pp. 65-73.

-------- (2015). "Demand Side Secular Stagnation," American Economic Review, vol. 105 (May), pp 60-65.

-------- (2016). "The Age of Secular Stagnation: What It Is and What to Do about It," Foreign Affairs, vol. 95 (March/April), pp. 2-9, https://www.foreignaffairs.com/articles/united-states/2016-02-15/age-secular-stagnation.

1. I am grateful to John Roberts and Robert Tetlow of the Federal Reserve Board staff for their assistance. Views expressed are mine and are not necessarily those of the Federal Reserve Board or the Federal Open Market Committee. Return to text

2. More formally, my Federal Reserve colleagues Thomas Laubach and John Williams (2003) have developed a statistical procedure that decomposes the movement in interest rates into the contribution of long-run and short-run factors. They conclude that the long-run component of the level of the real federal funds rate is currently very low--around 1/4 percent--compared with a pre-2000 average of 2-1/2 percent. Other assessments have reached similar conclusions. See Holston, Laubach, and Williams (forthcoming); Johannsen and Mertens (2016); and Kiley (2015). However, it is important to note that there is a great deal of statistical uncertainty around all of these estimates. Return to text

3. While the analysis that follows relates to interest rates in the long run, these factors are also important determinants of interest rates in the short run. Return to text

4. See Gordon (2016) and Fernald and Wang (2015). Return to text

5. These effects are what we would expect from our textbook models; they are also at work in the FRB/US model being used here. The empirical evidence on the link between trend growth and long-run equilibrium interest rates is mixed. Laubach and Williams (2003) find evidence of a link that is consistent with the predictions of models such as FRB/US. However, in their well-known paper, Hamilton et al. (2016) conclude that while "the theoretical presumption that there is a link between aggregate growth and real rates is very strong," the empirical link between the real equilibrium interest rate and real GDP growth is weak. As stressed by Hamilton et al. there a great deal of uncertainty over the relationship between growth and interest rates, likely, in part because of the multitude of shocks to which the economy is subject. A structural model, such as FRB/US, provides one method of estimating the link between growth and interest rates by examining the reaction of the interest rate to a clearly defined shock to the trend growth rate. However, this reaction occurs within the model economy, and is therefore subject to the particular structure and assumptions of the FRB/US model. Return to text

6. See, for example, Aaronson et al (2014). Return to text

7. See Board of Governors of the Federal Reserve System (2016). Return to text

8. Details of the simulations are included in an Appendix to the speech. Return to text

9. See Gagnon, Johannsen, and Lopez-Salido (2016); Rachel and Smith (2015); and Carvalho, Ferrero, and Necchio (2016). Return to text

10. See Gagnon, Johannsen, and Lopez-Salido (2016), figure 12. Return to text

11. See Summers (2014, 2015, 2016). See also Hilsenrath and Davis (2016). Return to text

12. By emphasizing "longer-run equilibrium" interest rates, I am excluding monetary policy (which is unlikely to have major effects on the equilibrium real interest rate), and thereby also relating to concerns about monetary policy being the only game in town. Return to text

13. See, for example, Kocherlakota (2015, 2016) and Summers (2016). Return to text

14. For instance, in Fischer, 2016. Return to text

Appendix

Here we review the simulations that underlie the estimates of the effects of various economic disturbances for their implications for the long-run equilibrium real federal funds rate, using simulations of the staff's FRB/US model. We first provide background on the methodology we use. We then review the nature of the shocks that are discussed in the speech and show the effects of those shocks on the long-run federal funds rate. Finally, we provide details about the results shown in the figures.

1. Background

Our point of departure is a definition of the equilibrium interest rate that corresponds with the neutral rate of interest. In particular, we use the definition of the neutral rate of interest that Chair Yellen used in a 2015 speech: "the real rate consistent with the economy achieving maximum employment and price stability over the medium term," which, in an elaboration in a footnote, is said to be "usually thought of as independent of the cyclical disturbances that routinely buffet the economy...[that] fade away after a few years."1 The sort of disturbances being captured under the rubric of shifts in r* are thus rarer and more persistent than the usual business cycle phenomena and are associated with the "various adjustment processes that are unusually drawn out by historical standards...[and have] slow-moving influences on both aggregate demand and supply."2 This definition corresponds reasonably closely with the (possibly time-varying) intercept of a Taylor-type rule in that the standard arguments of the Taylor (1999) rule--the output gap and the deviation of inflation from target--can be thought of as capturing the influence of the drivers of monetary policy at business cycle frequencies, with the longer-lasting (lower-frequency) determinants of the level of the policy rate being subsumed into movements in r*.3

Using this definition of r*, we identify several economic disturbances that have long-lasting consequences for the savings-investment balance of the U.S. economy. We shock the FRB/US model with each of these disturbances and compute what long-lasting (but not necessarily permanent) shift in the intercept of the Taylor (1999) rule is the best perturbation to the rule.

The thought experiment behind the simulations is as follows. We assume that the public views the Taylor (1999) rule as a good approximation of the conduct of monetary policy, and, accordingly, they price assets and formulate expenditure decisions on the expectation that this policy will prevail. Then policymakers identify that the economy is encountering a shock with durable implications for the savings-investment balance of the economy. At this point, policymakers communicate to the public a long-lasting shift to the intercept of the rule. Private-sector agents are assumed to understand this communication, and find it credible, and thus adjust their expectations accordingly.

2. The shocks

All simulations were carried out using the database from the public release of the FRB/US model, starting in 2036:Q1, at which time the economy is in steady state.4 Accordingly, the effective lower bound on nominal interest rates is never a binding constraint under these circumstances. Consistent with the definition of a steady state, at the start of the simulations, the output gap is closed, the unemployment rate is equal to its natural rate of 4.8 percent, inflation is 2 percent, the nominal federal funds rate is 3 percent, the 10-year Treasury bond rate is 3.5 percent, and potential output growth is 2 percent. Except as otherwise noted, tax rates are held fixed at their baseline levels for four years, after which fiscal policy is allowed to respond by gradually adjusting the federal personal income tax rate to stabilize the ratio of federal government fiscal deficits to gross domestic product (GDP) at its assumed baseline target level. In all instances, monetary policy is assumed to be governed by the (non-inertial) Taylor (1999) rule, with an intercept shift where applicable.

Table A.1 summarizes the effects of several shocks on the long-run equilibrium real federal funds rate in the FRB/US model. The details of how these shocks were implemented follow.

Labor force. The growth rate of the U.S. population (variable N16 in the FRB/US model) is assumed to climb over the course of a year to a pace that is 1 percentage point faster than in the baseline, with commensurate effects on the labor force, employment, potential output, and actual output. The elevated pace of population growth lasts for 20years before returning to baseline rates over the succeeding 5 years.

Productivity. The growth rate of total factor productivity (HMFPT) is increased 0.7 percentage point, which implies an acceleration in labor productivity (output per worker hour) of 1.0 percentage point. The shock lasts for 40 years before fading out at a moderate pace.

Investment. Sequences of shocks to the FRB/US model's three equations for business fixed investment--producer durables (EPD), intellectual property (EPI), and nonresidential structures (EPS)--are constructed such that the total increase in gross fixed capital investment equals 1 percent of GDP for 25 years. Thereafter, the shocks fade at a moderate rate over time. The shocks are scaled such that the split between the three components is about equal to their relative shares of GDP since 2001.

Cost of capital. Relative to its average over the period from 2000 to 2007, the financial cost of capital (RPD) has declined by about two percentage points, according to the FRB/US model database. That should have produced a boom in investment, which seems not to have happened. This shock computes the magnitude of this "missing effect" by simulating the effect of an increase in the financial cost of capital. RPD affects the user cost of capital for the model's four investment categories: equipment, intellectual property, nonresidential structures and inventories. Those, in turn, influence target rates of investment, all else equal. The shock lasts for 20 years before fading out at a moderate pace.

Foreign interest rates. The equilibrium real interest rate in (trade-weighted) foreign economies (FRSTAR) is assumed to decline by 1 percentage point for an indefinite period. This decline has the effect of reducing both foreign long- and short-term interest rates by a comparable amount.

Government spending. An increase in the level of federal expenditures on goods (EGFO) equal to 1 percent of GDP is sustained for 25 years and then phased out at a moderate pace thereafter. All other components of government spending are held at their baseline levels. The federal personal income tax rate is held at baseline for 10 years, and then the model's fiscal policy reaction function is allowed to adjust the tax rate so as to return the ratio of federal deficits to GDP to its previous target level. The government-debt-to-GDP ratio is therefore allowed to permanently increase.

Tax cut. The model's fiscal policy reaction function is suspended for 10 years, similar to the case of the government spending shock described previously. A sequence of shocks to the FRB/US model's equation for the average federal personal income tax rate (TRFP) is constructed such that the resulting decrease in taxes increases the federal budget deficit very similarly to the government spending shock described previously, in order to make the two simulations of comparable magnitude. After 10 years, the personal federal tax rate is allowed to adjust to bring the ratio of government deficits to GDP back to the baseline target level. The government-debt-to-GDP ratio is permanently increased.

Table A.1. Summary of Shocks Affecting the Neutral Rate of Interest

| Shock | FRB/US Mnemonic | Specification of shock | Δrr* |

|---|---|---|---|

| 1 Population growth | N16 | 1 ppt, 20 years | 1.15 |

| 2 Productivity growth | HMFPT | 1 ppt, 40 years | 0.85 |

| 3 Investment | EPD, EPS, EPI | 1 pct of GDP, 25 years | 0.29 |

| 4 Cost of capital | RPD | 2 ppts, 20 years | 0.63 |

| 5 Foreign interest rates | FRSTAR | 1 ppt, indefinitely | 0.27 |

| 6 Government spending | EGFO | 1 pct of GDP, 25 years | 0.50 |

| 7 Tax cut | TRFP | Deficits as in line 6 | 0.41 |

* In the current context, rr* is defined as the intercept of the Taylor (1999) rule.

3. Calculations for figures

Figure 1: Effects on the long-run equilibrium federal funds rate

{kind=link}

Slower growth. The slower growth of 1-1/4 percentage points in this scenario assumes that labor force growth is 1/4 percentage point lower and that labor productivity growth is 1 percentage point lower. According to table A.1, an increase of 1 percentage point in labor force growth would raise the equilibrium real federal funds rate by 1.15 percentage points. The contribution of the slower labor force growth to the equilibrium federal funds rate is therefore negative 0.25 x 1.15, or negative 30 basis points. Similarly, the contribution of slower productivity growth is negative 1.00 x 0.85 = negative 85 basis points, for a total effect of negative 115 basis points.

Demographics. As explained in the text, the effect of demographics on the equilibrium federal funds rate is based on the study of Gagnon, Johannsen, and Lopez-Salido (2016), who emphasize that demographic changes since the 1980s would imply a reduction of 125 basis points in the equilibrium federal funds rate. However, this number includes the effects of demographics on the labor force, which have already been included in the growth effect. As suggested by figure 12 of Gagnon, Johannsen, and Lopez-Salido (2016), adjusting for the effects of employment would trim about 50 basis points from the total effect (the distance between the solid-blue and dashed-green lines as of 2015). Thus, in Gagnon, Johannsen, and Lopez-Salido (2016), the effects excluding those via labor force growth are about negative 75 basis points.

Lower investment. This experiment corresponds to the cost of capital shock discussed in section 2, with the sign reversed. As can be seen in line 4 of table A.1, the "missing effects" of a 2 percentage point decrease in the financial cost of capital would have lowered the equilibrium real funds rate by 63 basis points.

Slower foreign growth. Here, we assume that foreign trend GDP growth has fallen as much as U.S. trend GDP growth and thus has had a similar effect on interest rates--namely, 115 basis points. That assumption would imply a reduction in the (U.S.) equilibrium federal funds rate of negative 1.15 x 0.27, or negative 30 basis points.

Figure 2: Long-run effects of animal spirits and fiscal policy on interest rates

{kind=link}

This figure shows the effects of shocks that lead to 1 percentage point shifts in each of the variables indicated. These simulations can be found directly in table A.1. Thus, the animal spirits shock in figure 2 corresponds to the investment shock shown in line 3 of table A.1. And the government spending and tax cut simulations shown in figure 2 line up with the simulations shown in lines 6 and 7 of table A.1.

References

Board of Governors of the Federal Reserve System (2016). "FRB/US Model," webpage, Board of Governors.

Gagnon, Etienne, Benjamin K. Johannsen, and David Lopez-Salido (2016). "Understanding the New Normal: The Role of Demographics (PDF)," Finance and Economics Discussion Series 2016-080. Washington: Board of Governors of the Federal Reserve System, October.

Taylor, John B. (1999). "A Historical Analysis of Monetary Policy Rules," in John B. Taylor, ed., Monetary Policy Rules. Chicago: University of Chicago Press, pp. 319-41.

Williams, John C. (2016). "Monetary Policy in a Low R-Star World," FRBSF Economic Letter 2016-23. San Francisco: Federal Reserve Bank of San Francisco, August.

Yellen, Janet L. (2015a). "Normalizing Monetary Policy: Prospects and Perspectives," speech delivered at "The New Normal Monetary Policy," a research conference sponsored by the Federal Reserve Bank of San Francisco, San Francisco, March 27.

-------- (2015b). "Inflation Dynamics and Monetary Policy," speech delivered at the Philip Gamble Memorial Lecture, University of Massachusetts, Amherst, Mass., September 24.

-------- (2015c). "The Economic Outlook and Monetary Policy," speech delivered at the Economic Club of Washington, Washington, December 2.

-------- (2016). "Current Conditions and the Outlook for the U.S. Economy," speech delivered at the World Affairs Council of Philadelphia, Philadelphia, June 6.

1. See Yellen (2015a), paragraph 15 and footnote 4. Return to text

2. See Yellen (2015a), footnote 4. Other definitions of the neutral rate used by the Chair in her public communications include the short-term real interest rate "that would be neither expansionary nor contractionary if the economy was operating near potential" (Yellen, 2015c, 2016) and the short-term real interest rate "that would be consistent with real GDP expanding in line with potential" (Yellen, 2015b). There may be circumstances in which the nuances of these definitions would matter, but, for our purposes, we can take them as one and the same. Return to text

3. Williams (2016) defines the natural rate of interest as the short-term real rate "that balances monetary policy so that it is neither accommodative nor contractionary in terms of growth and inflation." This description is close to that of the neutral rate (but not the natural rate) in the main text and in note 2 but adds a reference to inflation, which does not appear in definitions of the neutral rate. Return to text

4. See Board of Governors (2016). Return to text