FEDS Notes

February 05, 2019

Living at Home Ain't Such a Drag (on Spending): Young Adults' Spending In and Out of Their Parents' Home

Aditya Aladangady, Laura Feiveson, and Andrew Paciorek

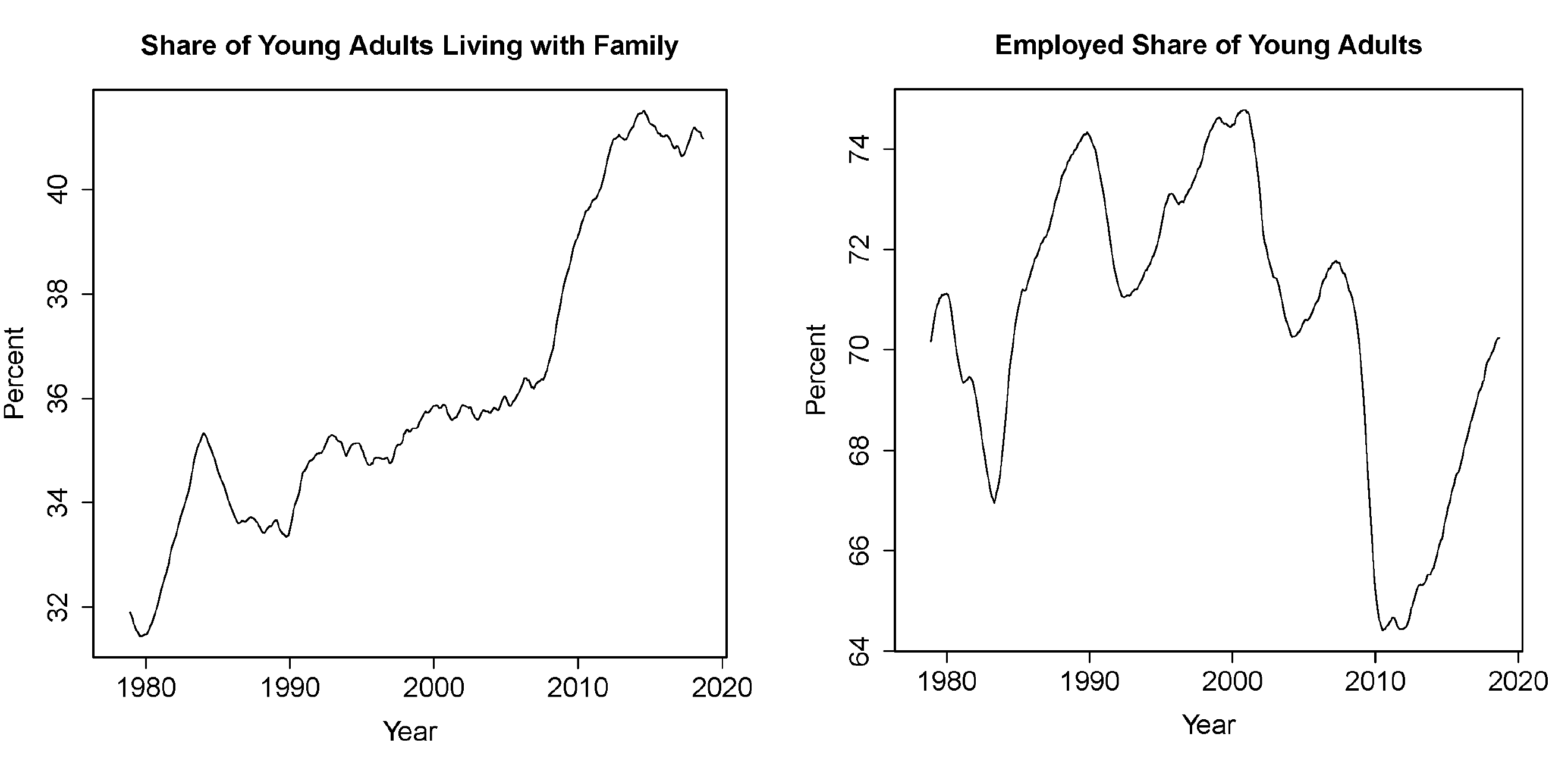

In the wake of the Great Recession, the share of young adults living with their parents increased sharply, and it has remained elevated since (figure 1a). Many young adults likely moved back in with their parents, or never left home in the first place, because they could not find a job paying enough money to allow them to live alone. But the increased rate of living at home has persisted even as per capita income has recovered and the employment rate among young adults has returned to pre-recession levels (figure 1b). There is a growing literature attributing this pattern to a range of possible factors, including lower perceived job stability or income growth expectations, a shift in social interactions towards video games and social media, a cultural shift in the acceptability of living at home, and increased housing costs.1 Regardless of the underlying cause, however, this shift in behavior has important implications for household consumption.

Figure 1: The Recent Experience of Young Adults

Source: Current Population Survey, 12-month moving average. "Young adults" include ages 18 to 32. "Family" includes parents but also grandparents, older siblings, and others.

By living together, young adults and their parents may jointly save on a variety of costs relative to maintaining multiple households (Kaplan 2012). In addition to the obvious savings on rent and utilities, home production activities may have some returns to scale. Cleaning and cooking, for example, may be more efficiently done in a single household as opposed to two separate ones. These efficiencies could imply more overall saving by the members of the household, or the amount saved could be redistributed toward spending in other areas. In this note, we quantify the net change in annual spending--both in total and within various categories--by a young adult who has just moved out of her parents' home, holding income constant.2

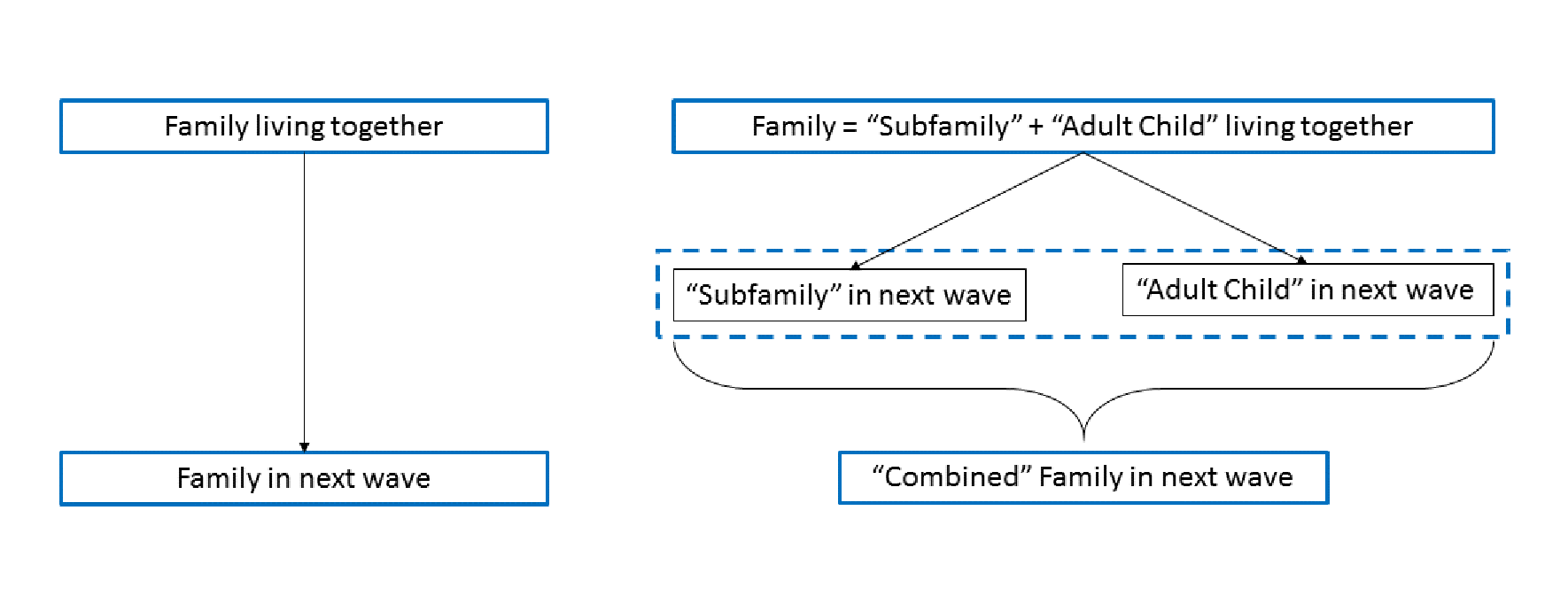

To explore this spending behavior, we use data from the Panel Study of Income Dynamics (PSID). Because it follows families over time, the PSID allows us to directly compare the spending of a family with a young adult living at home to the spending of the same family members when the young adult moves out. In particular, as shown in figure 2 below, we can track changes in spending and income of families between two waves of the survey, both for families that continued to live together (left side of flow chart) and for families where an "adult child" splits off to form a new household (right side).3

By combining families in this way, we can estimate the difference in how spending changes for a family that had an adult child move out compared to a control family that continues living together. Specifically, we estimate the following regression for combined family spending growth:

$$$$ \Delta c^{combined}_{it} = \beta_1 {SPLITOFF}_{it} + \beta_2 X_{it} + \delta_t + \delta_i + \varepsilon_{it} $$$$

In the regression, the change in spending of a combined family ($$ \Delta c^{combined}_{it} $$) is simply the change in family spending for a household that continued living together (figure 2, left panel). For a family where an adult child moves out into a new household, $$ \Delta c^{combined}_{it} $$ is the change in combined spending of the young adult and any family members with whom they were living previously (figure 2, right panel). The variable $$ {SPLITOFF}_{it} $$ is an indicator that takes the value of one for a young adult that split off from their parent household to form their own household or zero otherwise. We also include time ($$\delta_t$$) and household ($$\delta_i$$) fixed effects, as well as a set of controls $$X_{it}$$ that include the level and change in combined income and family size. Given estimates from this regression, we can see how much more the combined family spends when the child moves out of the house controlling for income and family size. We run the regression with both changes in the dollar value of consumption and in the log value of consumption on the left hand side.

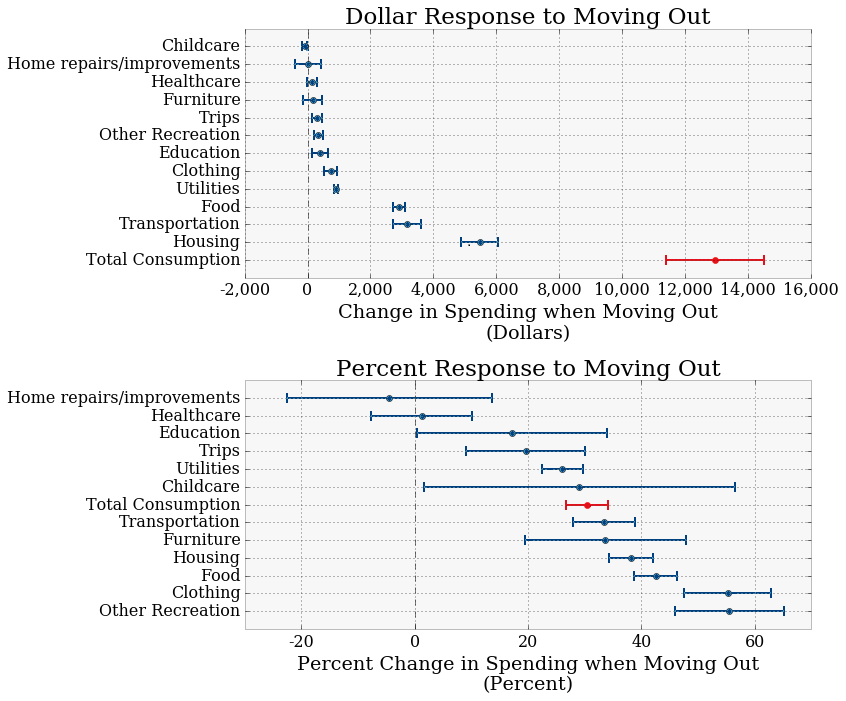

The results of these exercises are shown in figure 3 below, where the top panel shows estimates of the absolute dollar value of changes and the bottom panel shows the percentage changes implied by the log value regression. Categories of spending are broken out in blue, with the red marker denoting total spending in all measured categories.

Note: Whiskers show 95 percent confidence bands around the point estimates represented by the dots.

We find that adult children who move out spend roughly $13,000 more annually than their counterparts who continue living with their parents, as indicated by the red dot in the top panel of figure 3.4 Not surprisingly, much of the effect--about $6,400 per year--comes from increased spending on housing and utilities expenses. The results also suggest that movers spend more on certain other components like food and transportation (which includes car purchases) where there may be returns to scale within a household. Another category in which we may expect returns to scale is furniture. Expenditures on furniture--which make up less than one percent of total spending on average--are not significantly different for those moving out in dollar terms, but do appear large and significant when estimated and expressed as a percent of total furniture spending (see the bottom panel of figure 3).

Importantly, our results imply that, on average, adult children living at home do not spend the money saved on rent and food on other items. In fact, they save additional money by spending less than their counterparts who move out in other categories where there are unlikely to be returns to scale in home production, such as clothing and other recreation. These findings suggest the decision to live at home may partly reflect factors that are generally holding down spending among young adults like job instability or high housing costs.

Nevertheless, if we make the (perhaps unrealistic) assumption that the young adults living at home would spend like their counterparts that are living on their own, we find that there could be substantial effects on aggregate spending if they moved out. Relative to the period before the recession, we estimate that there are currently 3 1/4 million "excess" young adults living at home.5 Given our estimate that each of these young adults, on average, spends $13,000 less than they would living away from home, aggregate spending would rise by about $40 billion (or roughly 0.3 percent of national personal consumption expenditures) if they increased their spending by that amount. This would push the aggregate saving rate down by about 1/4 percentage point.

Of course, expenditures are not equivalent to welfare, and there are good reasons that some young adults prefer to live with their parents. First, the quality of shared housing might be higher than the housing an individual could afford on her own, conditional on the cost. Second, even reduced per-person expenditures may provide a higher benefit when there are returns to scale--for instance, home-cooked meals may be tastier and healthier, even while less expensive, than takeout meals.6 Finally, the increased saving rates among young adults living at home might lead them to be better prepared for the financing of future household purchases, their children's educations, or their retirement.

Bibliography

Aguiar, Mark, Mark Bils, Kerwin Kofi Charles, and Erik Hurst (2017). "Leisure Luxuries and the Labor Supply of Young Men," NBER Working Paper No. 23552.

Benmelech, Efraim, Adam Guren, and Brian Melzer (2017). "Making the House a Home: The Stimulative Effect of Home Purchases on Consumption and Investment," NBER Working Paper No. 23570.

Dettling, Lisa, and Joanne Hsu (2018). “Returning to the nest: Debt and parental co-residence among young adults,” Labour Economics 54, pp 225-236.*

Kaplan, Greg (2012). "Moving Back Home: Insurance against Labor Market Risk," Journal of Political Economy 120:3, pp 446-512.

Lee, Kwan Ok, and Gary Painter (2013). "What Happens to Household Formation in a Recession?" Journal of Urban Economics 76, pp 93-109.

Paciorek, Andrew (2013). "The Long and the Short of Household Formation," Real Estate Economics 44:1, pp 7-40.

Panel Study of Income Dynamics, public use dataset (2018). Produced and distributed by the Survey Research Center, Institute for Social Research, University of Michigan, Ann Arbor, MI.

Tiwari, Arpita, Anju Aggarwal, Wesley Tang, and Adam Drewnowski (2017). "Cooking at Home: A Strategy to Comply with U.S. Dietary Guidelines at No Extra Cost," American Journal of Preventive Medicine 52:5, pp 616-624.

1. See Dettling and Hsu (2018), Aguiar et al. (2017), Paciorek (2013), and Lee and Painter (2013), as well as citations therein.* Return to text

2. See also Benmelech et al. (2017), who examine the implications of home purchases for household consumption and investment. Return to text

3. In the PSID sample, we restrict "young adult living at home" to be any adult living in the household who is not a student, is between the ages of 18 and 32, and is not the head of the household in the survey or spouse of the head. This is most often a child of the head or spouse, but could also be another relation. Roommates or those paying rent are not included. Return to text

4. In addition to the PSID, we use the Consumer Expenditure Survey (CEX) to validate these findings. Because the CEX does not follow families over long periods, we match households living with an adult child at home with a young adult living separately and a sub-family with a similar structure, as well as similar income, age, and family characteristics. The results suggest households living separately spend approximately $13,000 more per year. The composition of this difference is similar to our PSID results, as well. Return to text

5. We calculate this number by multiplying the total number of young adults by the difference between the current share of young adults living at home and the share that did so in 2006. Return to text

6. Tiwari et al (2017). Return to text

*On February 6, 2019, footnote 1 and the bibliography were updated.

Aladangady, Aditya, Laura Feiveson, and Andrew Paciorek (2019). "Living at Home Ain't Such a Drag (on Spending): Young Adults' Spending In and Out of Their Parents' Home," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, February 5, 2019, https://doi.org/10.17016/2380-7172.2301.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.