January 07, 2017

Low Interest Rates and the Financial System

At the 77th Annual Meeting of the American Finance Association, Chicago, Illinois

Thank you for this invitation to discuss low interest rates and the financial system. The framing of this topic raises the question of whether low interest rates have somehow undermined the stability and functioning of the financial system. I will argue that "low for long" interest rates have supported slow but steady progress to full employment and stable prices, which has in turn supported financial stability. Indeed, by many measures the U.S. financial system is much stronger than before the crisis. That said, there are difficult tradeoffs to manage. Over time, low rates can put pressure on the business models of financial institutions. And low rates can lead to excessive leverage and broadly unsustainable asset prices--things that we watch carefully for and do not observe at this point. I will begin by focusing briefly on the macroeconomic effects of low interest rates. I will then turn to the condition of the financial system--in particular, its interplay with low rates. As always, the views I express here today are mine alone.

Highly Accommodative Monetary Policy

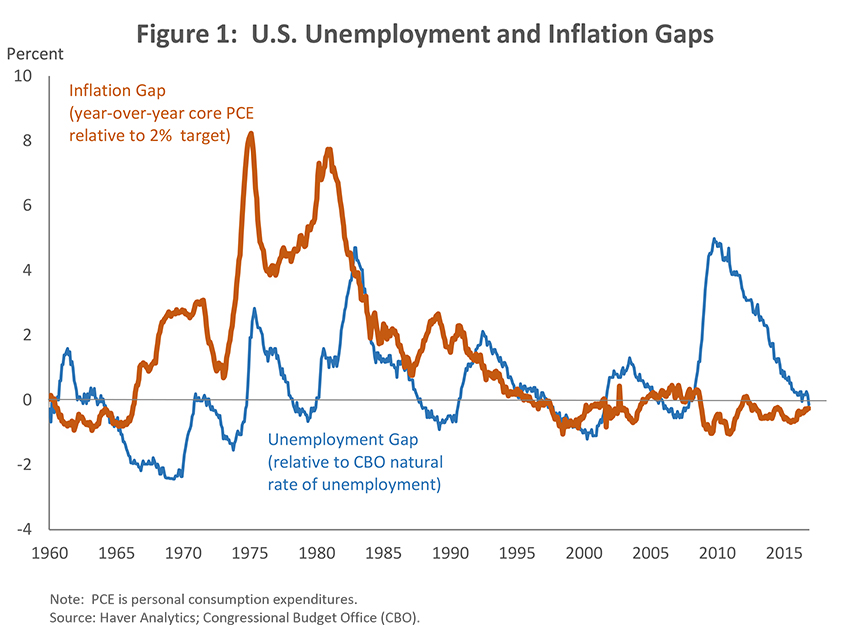

The financial crisis and the Great Recession posed the most significant macroeconomic challenges for the United States in a half-century, leaving behind high unemployment and below-target inflation and calling for highly accommodative monetary policies. Isolating the effects of these policies is challenging, but studies generally show that they lowered rates across the curve and moved other asset prices as well.1 It is even more challenging to evaluate their effects on aggregate demand. Low rates and higher asset prices should support household and business spending and investment through various channels. But low rates may also perversely induce some households to save more in order to meet their targets for retirement. And low rates have clearly not produced a boom in corporate investment, although standard accelerator models suggest that investment has largely been consistent with the weak pace of economic growth. Nonetheless, there is good reason to think that low rates have provided significant support for demand, and my view is that they have done so.2 As you can see in slide 1, we are now close to meeting our dual mandate--a reasonable summary statistic for the effects of policy. While growth has been frustratingly slow, employment gains have been solid. This is a reasonably good outcome considering the scope of the crisis and the relatively poorer performance of other major advanced economies.

{kind=link}

Other Factors Are Holding Down Rates

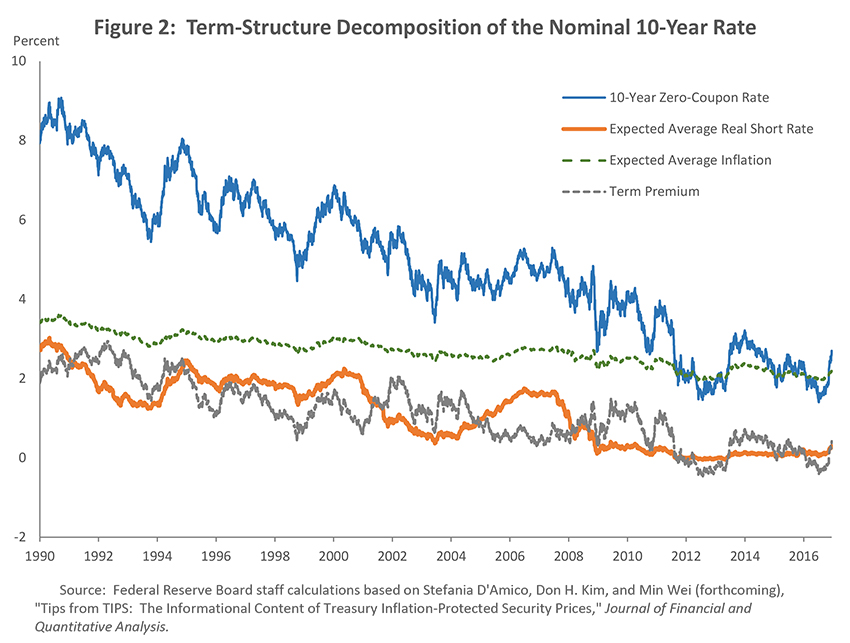

There are also many factors other than monetary policy that are holding down long-term interest rates. Long-term nominal and real rates have been declining for over 30 years. The next slide decomposes long-term nominal yields into expected future short-term real rates, expected future inflation, and a term premium. These estimates are based on one of the Board's workhorse term structure models.3 All three components have contributed to the downward trend in long-term nominal yields.

{kind=link}

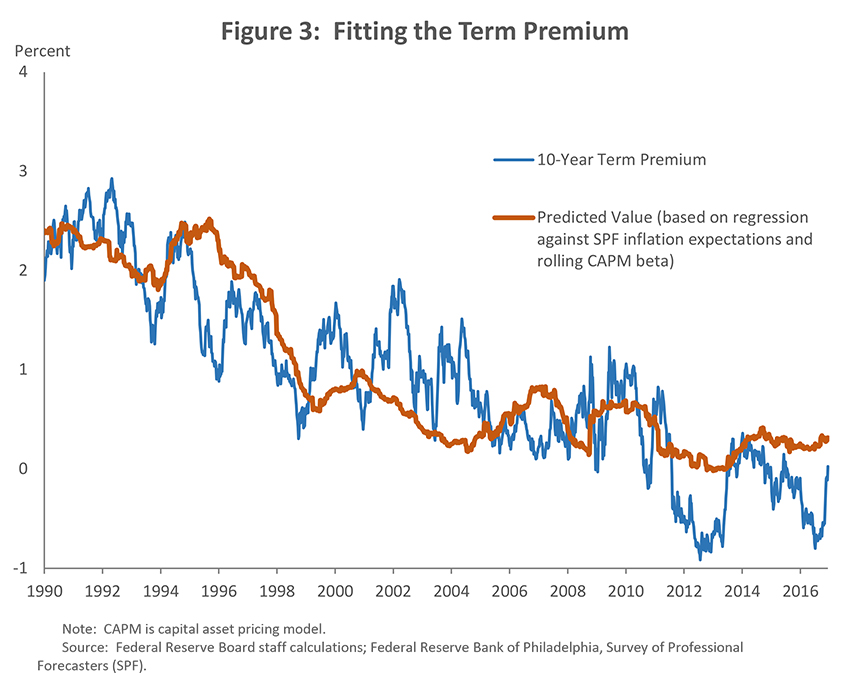

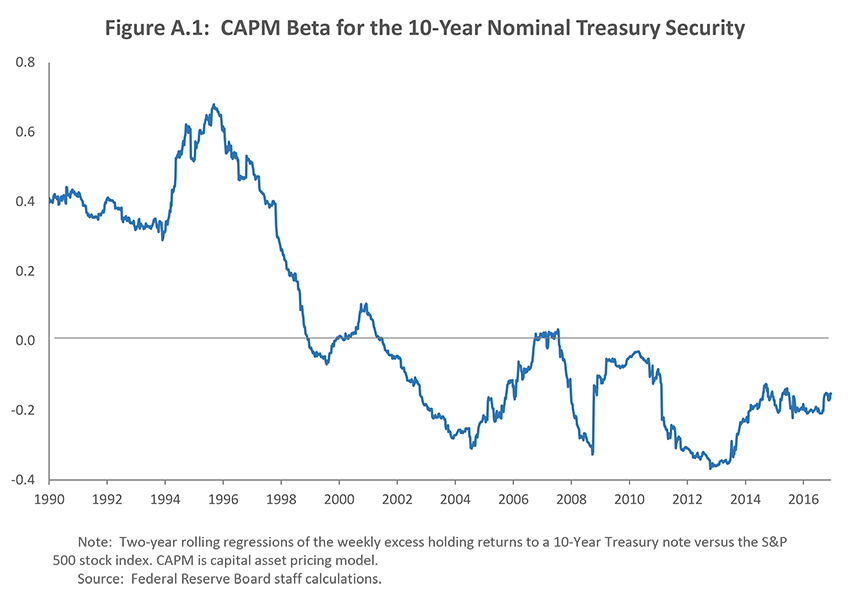

The downward trend in nominal term premiums likely reflects both lower inflation risk and the fact that, with inflation expectations anchored, nominal bonds have become an increasingly good hedge against market risk. That has made bonds a more attractive investment and reduced the term premium.4 As shown in the next slide, a regression of the 10-year term premium on measures of 10-year inflation expectations and a rolling beta of Treasury returns with respect to equity returns (to proxy for the hedging value of bonds) shows that these two factors can account for a large part of the decline in the term premium.

{kind=link}

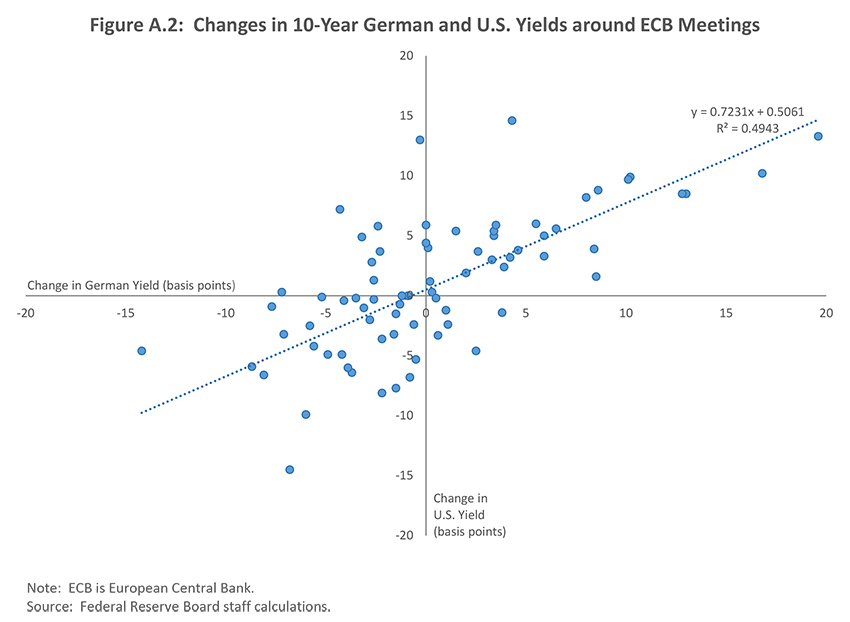

Regulations now require many financial institutions to hold more safe, high-quality liquid assets, which likely has pushed down term premiums further. Global factors may have put downward pressure on term premiums because of anxiety about the foreign outlook, which may have increased demand for U.S. assets, or because low rates abroad have depressed U.S. term premiums through a global portfolio balance channel.5 And real rates are quite low globally, reflecting the step-down of productivity growth over the past 10 years as well as shifts in savings and investment demand due to demographic change.6

The Core of the Financial System Is Much Stronger

Before turning to the interplay between low rates and the financial system, I will simply point out that both improved risk management at the largest, most systemically important financial institutions (SIFIs) and stronger regulation have made the core of the system much stronger and more resilient than before the crisis.7 The SIFIs have more stable funding, hold much more capital and liquidity, are more conscious of their risks, and are far more resolvable should they fail. Many aspects of our financial market infrastructure, including the triparty repurchase agreement (or repo) market, central counterparties (CCPs), and money market funds are more robust as well.

Low Rates Can Mean Tradeoffs

So far, I have argued that low rates have supported aggregate demand and brought us very close to full employment and 2 percent inflation; that forces other than monetary policy have been pushing rates lower for more than 30 years; and that the core of the financial system is now much stronger and more resilient than before the crisis. All of that said, I would also agree that monetary policy may sometimes face tradeoffs between macroeconomic objectives and financial stability. Indeed, it would be a divine coincidence if that were not the case. There are times when all of these objectives are aligned. For example, the Fed's initial unconventional policies supported both market functioning and aggregate demand. More broadly, post-crisis monetary policy supported asset values, reduced interest payments, and increased both employment and income. All of these effects are likely to have limited defaults and foreclosures and bolstered the balance sheets of households, businesses, and financial intermediaries, leaving the system more robust.

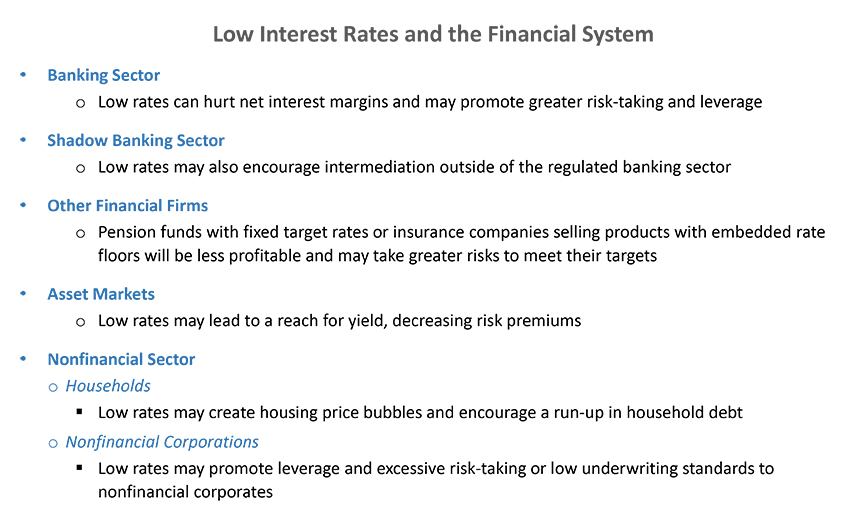

But at times there will be tradeoffs. Low-for-long interest rates can have adverse effects on financial institutions and markets through a number of plausible channels, as listed on the next slide.8 After all, low interest rates are intended to encourage some risk-taking.9The question is whether low rates have encouraged excessive risk-taking through the buildup of leverage or unsustainably high asset prices or through misallocation of capital. That question is particularly important today. Historically, recessions often occurred when the Fed tightened to control inflation. More recently, with inflation under control, overheating has shown up in the form of financial excess. Core PCE inflation remained close to or below 2 percent during both the late-1990s stock market bubble and the mid-2000s housing bubble that led to the financial crisis. Real short- and long-term rates were relatively high in the late-1990s, so financial excess can also arise without a low-rate environment. Nonetheless, the current extended period of very low nominal rates calls for a high degree of vigilance against the buildup of risks to the stability of the financial system.

{kind=link}

If we look at the channels listed here, the picture is mixed, but the bottom line is that there has not been an excessive buildup of leverage, maturity transformation, or broadly unsustainable asset prices.

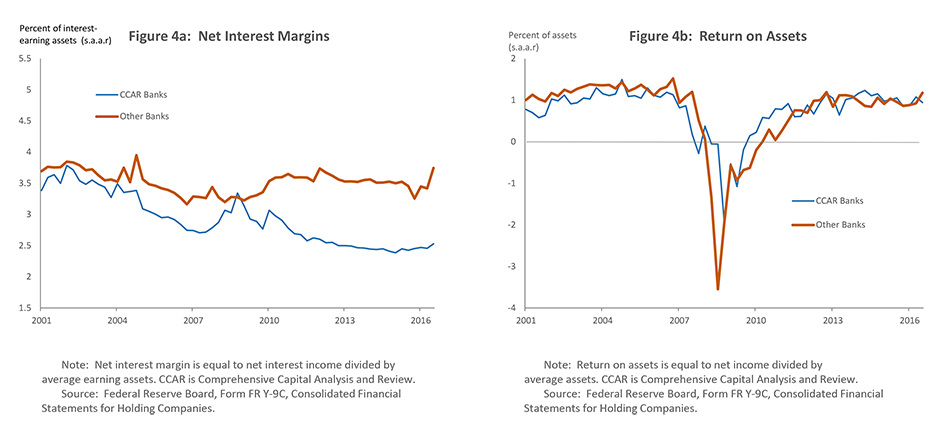

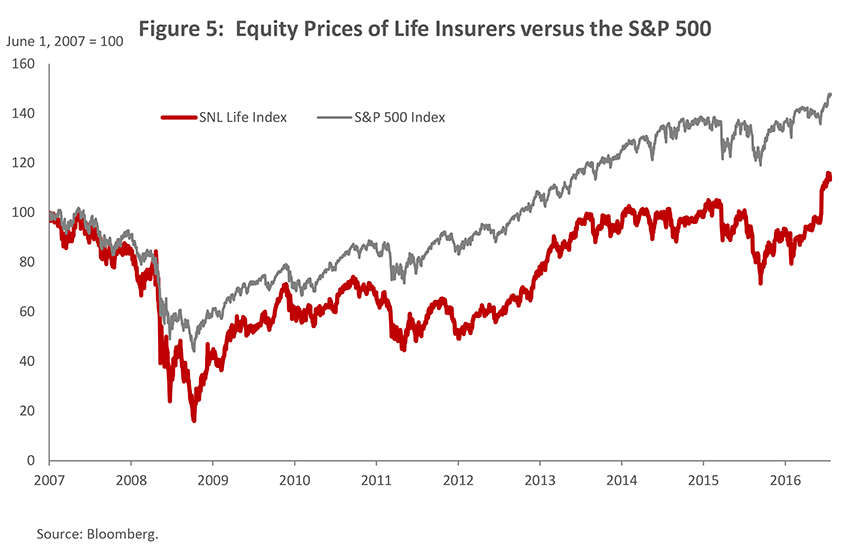

Low long-term interest rates have weighed on profitability in the financial sector, although firms have so far coped with those pressures. As shown in the next slide, net interest margins (NIMs) for most banks have held up surprisingly well. NIMs have moved down for the largest banks. Return on assets, shown to the right for both groups, has recovered but remains below pre-crisis levels. Life insurers have substantially underperformed the broader equity market since 2007, suggesting that investors see the low-rate environment as a drag on profitability for the industry. Even so, data on asset portfolios do not suggest that life insurers have increased risk-taking. The same is true for banks. Both the regulatory environment and banks' own attitudes toward risk following the financial crisis have helped ensure that the largest banks have not taken on excessive credit or duration risks relative to their capital cushions.

{kind=link}

{kind=link}

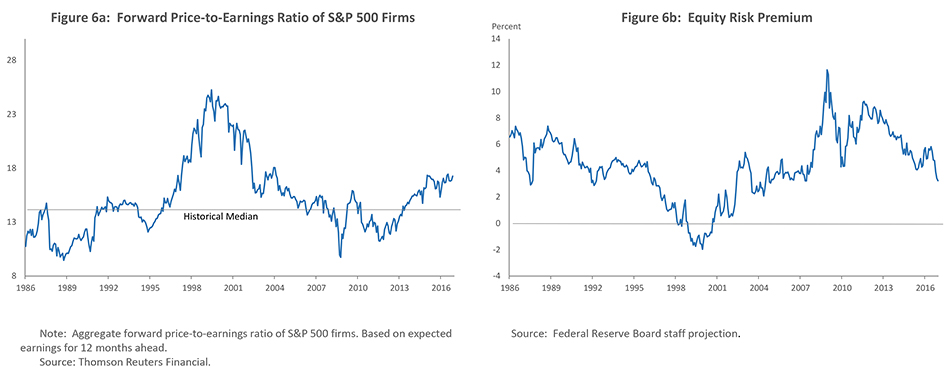

Low rates have provided support for asset valuations--indeed, that is part of their design. But I do not see valuations as significantly out of line with historical experience. Equity prices have recently increased considerably, pushing the forward price-earnings ratio further above its historical median (slide). And equity premiums (right)--the expected return above the risk-free rate for taking equity risk-- have declined, but are not out of line with historical experience.

{kind=link}

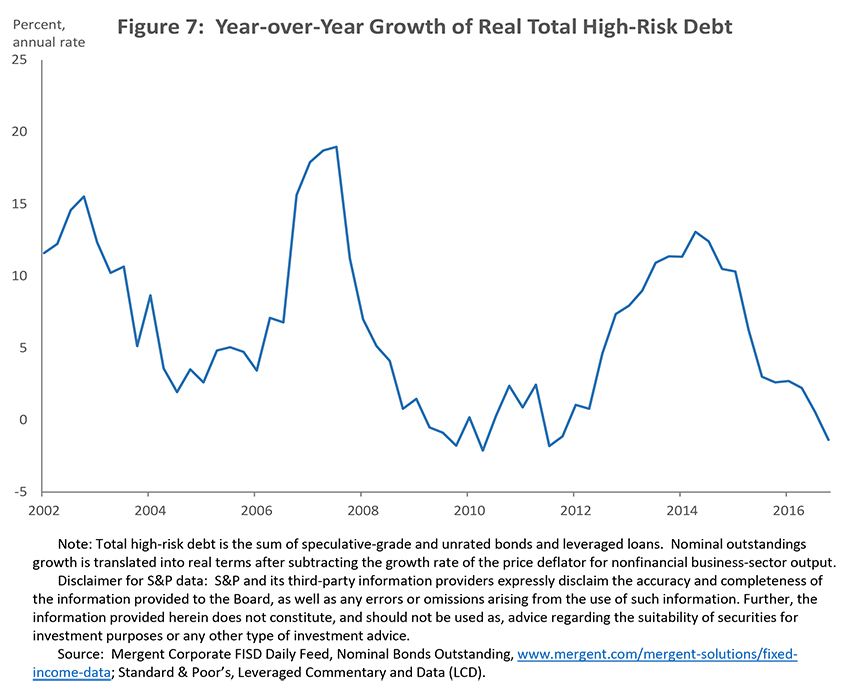

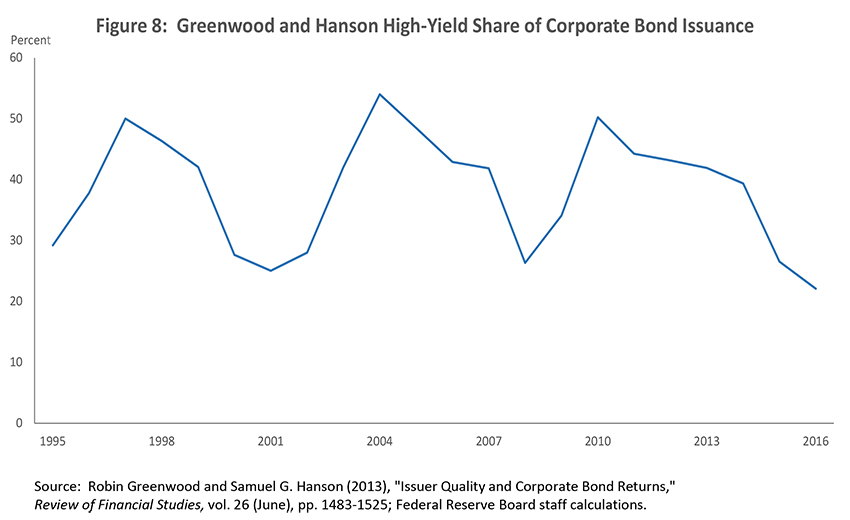

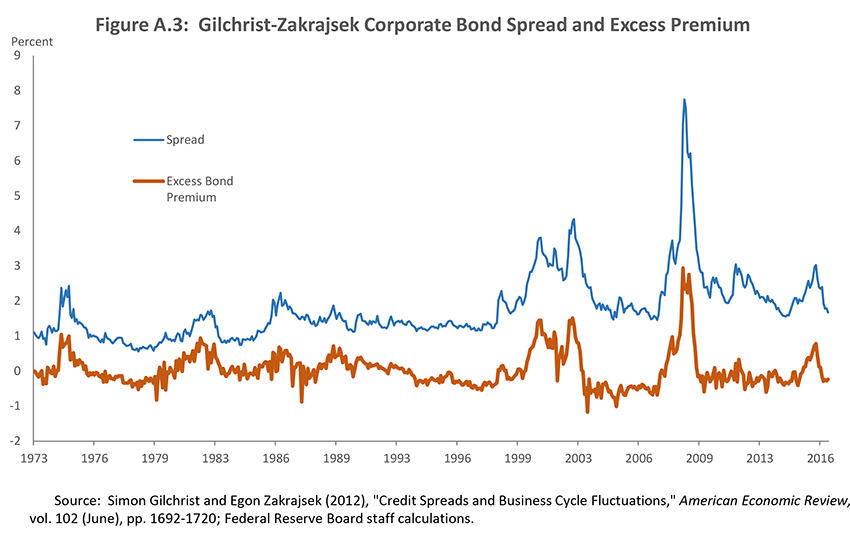

In the nonfinancial sector, valuation pressures are most concerning when leverage is high, particularly in real estate markets. Residential real estate valuations have been in line with rents and household incomes in recent years, and the ratio of mortgage debt to income is well below its pre-crisis peak and still declining. In contrast, valuations in commercial real estate are high in some markets.10 And in the nonfinancial corporate sector, gross leverage is high by historical standards. Low long-term rates have encouraged corporate debt issuance at the same time that some regulations, particularly the Volcker rule, have discouraged banks from holding and making markets in such debt. High-risk corporate debt (the sum of high-yield bonds and leveraged loans) grew rapidly in 2013 and 2014 (slide), although growth has declined sharply since then.11 However, firms also are holding high levels of liquid assets, so net leverage is not elevated. Firms have also lengthened their maturity profiles, and interest coverage ratios are high. As the next slide shows, Greenwood and Hanson's measure of the share of high-yield debt in overall issuance is at a relatively low level.12 And this debt is now held more by unlevered investors. Overall, I do not see leveraged finance markets as posing undue financial stability risks. And if risk-taking does not threaten financial stability, it is not the Fed's job to stop people from losing (or making) money.

{kind=link}

{kind=link}

As I said, a mixed picture. Low interest rates have encouraged risk-taking and higher leverage in some sectors and have weighed on profitability in others, but the areas where there are signs of excess are isolated.

Conclusion

To sum up, low interest rates have supported economic activity and gradually brought us back to full employment and 2 percent inflation. Better regulation and risk management have so far minimized the tradeoffs between our macroeconomic objectives, on the one hand, and financial stability, on the other. Still, a period of low rates for a long time could present significant challenges for monetary policy. It could also put pressure on the business models of some financial institutions. Ultimately, the only way to get sustainably higher interest rates is to improve the broader environment for growth, by adopting policies designed to increase productivity and potential output over the long term--policies that are mainly outside the scope of our work at the Federal Reserve.13

References

Adrian, Tobias, and Nellie Liang (2014). "Monetary Policy, Financial Conditions, and Financial Stability," Federal Reserve Bank of New York Staff Reports 690. New York: Federal Reserve Bank of New York, September (revised December 2016).

Bekaert, Geert, Marie Hoerova, and Marco Lo Duca (2013). "Risk, Uncertainty and Monetary Policy," Journal of Monetary Economics, vol. 60 (October), pp. 771-88.

D'Amico, Stefania, Don H. Kim, and Min Wei (forthcoming). "Tips from TIPS: The Informational Content of Treasury Inflation-Protected Security Prices," Journal of Financial and Quantitative Analysis.

Dell'Ariccia, Giovanni, Luc Laeven, and Gustavo A. Suarez (forthcoming). "Bank Leverage and Monetary Policy's Risk-Taking Channel: Evidence from the United States," Journal of Finance.

Engen, Eric M., Thomas Laubach, and David Reifschneider (2015). "The Macroeconomic Effects of the Federal Reserve's Unconventional Monetary Policies (PDF)," Finance and Economics Discussion Series 2015-005. Washington: Board of Governors of the Federal Reserve System, January.

Gagnon, Etienne, Benjamin K. Johannsen, and David Lopez-Salido (2016). "Understanding the New Normal: The Role of Demographics (PDF)," Finance and Economics Discussion Series 2016-80. Washington: Board of Governors of the Federal Reserve System, October.

Gilchrist, Simon, and Egon Zakrajšek (2012). "Credit Spreads and Business Cycle Fluctuations," American Economic Review, vol. 102 (June), pp. 1692-1720.

Greenwood, Robin, and Samuel G. Hanson (2013). "Issuer Quality and Corporate Bond Returns," Review of Financial Studies, vol. 26 (June), pp. 1483-1525.

Mian, Atif, Kamalesh Rao, and Amir Sufi (2013). "Household Balance Sheets, Consumption, and the Economic Slump," Quarterly Journal of Economics, vol. 128 (November), pp. 1687-1726.

Powell, Jerome H. (2015). "Financial Institutions, Financial Markets, and Financial Stability," speech delivered at the Stern School of Business, New York University, New York, February 18.

Powell, Jerome H. (2016). "Recent Economic Developments and Longer-Run Challenges," speech delivered at The Economic Club of Indiana, Indianapolis, November 29.

Rachel, Lukasz, and Thomas D. Smith (2015). "Secular Drivers of the Global Real Interest Rate," Bank of England Staff Working Paper 571. London: Bank of England, December.

Williams, John C. (2014). "Monetary Policy at the Zero Lower Bound: Putting Theory into Practice (PDF)," Hutchins Center Working Papers. Washington: Hutchins Center on Fiscal and Monetary Policy, Brookings Institution, January.

Yellen, Janet L. (2016). "The Federal Reserve's Monetary Policy Toolkit: Past, Present, and Future," speech delivered at "Designing Resilient Monetary Policy Frameworks for the Future, a symposium sponsored by the Federal Reserve Bank of Kansas City, held in Jackson Hole, Wyo., August 26.

1. Williams (2014) compiles the results from a range of studies estimating the effect of the Federal Reserve's large-scale asset purchases (LSAPs). While the exact numbers vary and are subject to substantial uncertainty, typical estimates of the effect of a representative $600 billion in Treasury LSAPs on long-term yields are in the range of 15 to 25 basis points, an effect roughly equivalent to that of three or four rate cuts of 25 basis points. Return to text

2. See Engen, Laubach, and Reifschneider (2015). The most interest rate sensitive sectors of the economy, such as consumer durables and residential investment, have exhibited higher growth than other sectors since the second round of quantitative easing by the Federal Reserve. And, for example, Mian, Rao, and Sufi (2013) conclude that the decline in house prices during the recession had a substantial effect on consumption; by the same argument, if low rates supported house prices, then they would have supported consumer spending as well. Return to text

3. See D'Amico, Kim, and Wei (forthcoming). Return to text

4. The changing risk profile of nominal Treasury bonds can be seen from its capital asset pricing model (or CAPM) beta, a measure of the co-movement between returns on longer-term Treasury securities and the equity market. Figure A.1 shows that the estimated rolling beta of the 10-year Treasury note with respect to the S&P 500 turned from positive to negative around 2000, indicating that Treasury bonds are now likely to act as a safe haven, performing well when equity markets do poorly. Return to text

{kind=link}

5. Figure A.2 shows the response in daily changes in 10-year U.S. Treasury yields to changes in 10-year German bund yields around European Central Bank (ECB) monetary policy decisions since 2010. The significantly positive regression coefficient is evidence of substantial spillovers from ECB monetary policy to U.S. long-term yields. Return to text

{kind=link}

6. See Rachel and Smith (2015) and Gagnon, Johannsen, and Lopez-Salido (2016). Return to text

7. See Powell (2015). Return to text

8. See Adrian and Liang (2014). Return to text

9. See Dell'Ariccia, Laeven, and Suarez (forthcoming), which finds evidence for a risk-taking channel of monetary policy based on supervisory ratings of U.S. bank loans. Bekaert, Hoerova, and Lo Duca (2013) find that accommodative monetary policy shocks lead to a decline in the VIX, a measure of implied volatility, by lowering both expected volatility and the risk premium. Return to text

10. The Federal Reserve, along with the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corporation, issued guidance regarding prudent management of risks from loans secured by commercial real estate (CRE) in late 2015. Of course, the annual stress tests typically feature significant declines in CRE prices, suggesting that banks are capitalized against a deterioration in this sector. Return to text

11. Gilchrist and Zakrajšek's (2012) measure of the corporate bond spread, shown in Figure A.3, is at about its average level, but their estimate of the risk premium in this market is low, so, by this measure, at least pricing is rich. Return to text

{kind=link}

12. See Greenwood and Hanson (2013). Return to text

13. See Powell (2016) and Yellen (2016). Return to text