FEDS Notes

October 02, 2020

Implementing Monetary Policy in an “Ample-Reserves” Regime: When in Crisis (Note 3 of 3)1

Jane Ihrig, Zeynep Senyuz, and Gretchen C. Weinbach

The Federal Reserve's response to this extraordinary period has been guided by our mandate to promote maximum employment and stable prices for the American people, along with our responsibilities to promote stability of the financial system.

Jerome Powell, Chair of the Federal Reserve

https://www.federalreserve.gov/newsevents/testimony/powell20200519a.htm

Note 1 and Note 2 in this three-part series described how the Federal Reserve (or Fed) implements monetary policy in normal times, with an ample quantity of reserves in the banking system.2 In this third and final Note in our series, we take a detour in light of current circumstances and describe how the Fed operates amid a crisis—when facing severely strained economic or financial circumstances, or both. To make the discussion concrete, we describe the Fed's extraordinary response to the COVID-19 pandemic, which acutely disrupted key financial markets and severely weakened economic activity in the United States and around the world.

When faced with a crisis, the Fed takes extraordinary steps to mitigate harm to the economy and financial markets. As a result, the amount of reserves in the banking system tends to rise substantially. Regardless of how elevated reserve balances become or how large the Fed's balance sheet gets, an ample-reserves regime remains an efficient and effective approach to implementing monetary policy, by design, providing flexibility to the Fed in its crisis response.

What does a "crisis" look like?

In the United States, each of the last two crises hit financial markets and the economy very hard but arose in very different ways. The Global Financial Crisis of 2007-09 was triggered by the prospect of significant losses on some types of residential mortgage loans and related securities, leading to severe strains in financial markets. The stresses cumulated as they spread among interconnected financial markets and entities, and they spilled over to weigh heavily on economic activity, causing the Great Recession that followed in their wake.3 In contrast, the COVID-19 pandemic, currently still evolving, is fundamentally a global public health crisis. The coronavirus, as well as measures taken to limit its spread and protect public health, including social distancing, triggered deep disruptions in economic activity and financial markets around the globe.

Although crisis episodes such as these can arise in different ways, some of their interrelated effects on the economy and in financial markets are similar. When a severe crisis hits, no matter the source, the outlook for economic activity and employment tends to become highly uncertain. When the fundamental strength of the economy and its likely evolution are in question, the pricing of various financial instruments can become more difficult, resulting in significant volatility in markets. A sustained period of large and more frequent changes in the prices of financial assets can lead investors to adjust their portfolios, generally reducing holdings of riskier or less-liquid assets in favor of safer, more-liquid assets. Such adjustments can be very sizable in aggregate, and the functioning of key financial markets can become strained. In addition, entities that extend credit can become more cautious in doing so. When the prospects for employment and income cloud, and the ability of businesses and households to consistently access credit declines, they tend to pull back from spending, resulting in further deterioration in economic activity, higher uncertainty regarding the outlook for such activity, and perhaps also additional pressures in key financial markets.

The Fed's policy responses to severe crises also have some things in common. When crises arise, the Fed typically takes actions that are more forceful than in normal times—both swifter and larger—calibrated to the extent and pace of harm that could otherwise befall the economy. In addition, because crises can emerge in significantly different ways, the Fed works to understand the origins of the adverse pressures on financial markets and economic activity and tailor its actions to best mitigate the harm. Moreover, the Fed taps its toolkit. The Fed's toolkit contains a wide range of possible actions; we sort them into three broad categories, each corresponding to a particular purpose. In the remainder of this Note, we describe each of these toolkit categories and how the Fed has deployed it during the first few months of the COVID-19 pandemic. Table 1 lists all of the Fed's many pandemic-related actions, all of which ultimately aim to help the Fed achieve its dual mandate.

Table 1: Summary of Fed Actions in Response to COVID-19 Pandemic

| Fed action | Short description | Initial purpose | Tapped in 2007-09 GFC | ||

|---|---|---|---|---|---|

| Lower interest rates | Support smooth market functioning | Support credit flow more directly | |||

| Adjust policy rate | Lower target range for policy rate to near zero | Yes | Yes | ||

| Forward guidance | FOMC says policy rate will stay low | Yes | Yes | ||

| Repo operations | Temporarily provide cash in large quantities to primary dealers on overnight and term basis in exchange for sound collateral | Yes | |||

| Securities purchases* | Purchase large quantities of Treasury securities and agency MBS | Yes | Yes | ||

| Discount window | Lend cash to depository institutions in sound condition | Yes | Yes | ||

| Central bank liquidity swaps | Standing swap lines provide foreign central banks with U.S. dollars in exchange for local currency; dollars may be on-lent to institutions in local jurisdictions | Yes | Yes | ||

| Temporary Foreign and International Monetary Authorities (FIMA) Repo Facility | Fed does repo with FIMA account holders (foreign central banks)—Fed takes Treasury securities in exchange for dollars, which may then be on-lent in local jurisdictions | Yes | |||

| Commercial Paper Funding Facility (CPFF) | Purchase highly rated 3-month CP from businesses, municipals, and issuers of asset-backed CP | Yes | Yes | ||

| Money Market Mutual Fund Liquidity Facility (MMLF) | Lend to eligible financial institutions secured by high-quality assets purchased from select money market mutual funds | Yes | Yes | ||

| Primary Dealer Credit Facility (PDCF) | Lend cash to primary dealers, key financial intermediaries, in exchange for sound collateral | Yes | Yes | ||

| Paycheck Protection Program Liquidity Facility (PPPLF) | Lend to eligible financial institutions who originate or purchase PPP loans from the Small Business Association | Yes | |||

| Main Street Lending Program (MSLP) | Purchase large share of loans originated by eligible lenders to small and medium-sized businesses (and soon, nonprofits) | Yes | |||

| Term Asset-Backed Securities Loan Facility (TALF) | Lend to eligible investors who purchase certain top-rated securities backed by consumer and business loans or other assets | Yes | Yes | ||

| Primary and Secondary Market Corporate Credit Facilities (PMCCF, SMCCF) | Primarily purchase bonds issued by qualified, large corporations | Yes | |||

| Municipal Liquidity Facility (MLF) | Purchase short-term notes from U.S. states and other municipalities | Yes | |||

| Supervisory and regulatory actions | Various statements, guidance, and rules to support financial institutions and the economy | Yes | Yes | ||

Category 1: Lower interest rates

During times of crisis, faced with the prospect of pervasive weakness in economic activity, severe strains in financial markets, or both, the Federal Open Market Committee (FOMC) typically lowers the target range for its policy interest rate, the federal fund rate. Since the policy rate transmits to other funding rates, lowering it helps reduce the cost of credit for businesses and households, and may lower some existing debt burdens. And, among other things, lowering the policy rate affects decisions about asset allocations, spending, and saving, and thus influences financial conditions more generally. Overall, this policy action stimulates economic activity over time by providing incentives for households and businesses to increase their consumption and investment.

The FOMC may also use forward guidance—words—to communicate an intention to leave the policy rate low. If the public believes the policy rate will stay low, this expectation becomes built into longer-term interest rates and feeds through to financial conditions more broadly. This tool can be especially important when the policy rate nears, or is at, zero (its effective lower bound). For forward guidance to achieve its intended goal, the FOMC's inherent or explicit commitment must be credible. Credibility may in part be achieved by conditioning the commitment on some observable marker. Some markers, such as a particular future date (calendar-based forward guidance), are more observable than others, such as a specific economic outcome (state-based forward guidance), and there are trade-offs and other considerations that are important in choosing a particular marker.

In March 2020, in the wake of the COVID-19 pandemic and a severely deteriorating economic outlook, the FOMC quickly lowered the target range for its policy rate. Over two unscheduled meetings, the Committee cut the target range for the federal funds rate a total of 150 basis points, bringing it down to a range of 0 to 25 basis points. The FOMC also issued forward guidance, communicating that it "expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals."4 These actions—all of which aimed to lower interest rates—are shown in the first block of (unshaded) entries in Table 1.

Category 2: Support smooth market functioning

Well-functioning financial markets are foundational to a well-functioning economy. The Fed relies on financial markets to implement monetary policy effectively and efficiently; that is, to ensure its desired policy rate settings in fact take initial hold in financial markets. In addition, the Fed relies on financial markets for effective and efficient monetary transmission—to ensure its policy rate settings not only take initial hold, but also propagate widely through the economy, affecting longer-term interest rates and financial conditions more broadly. And, more generally, stable financial markets are needed to facilitate the flow of credit through the economy. So when financial markets become severely strained, the Fed must step in to help stabilize them.

The specific actions the Fed takes to support the smooth functioning of financial markets depend on which markets are strained and the particular conditions and pressures they are exhibiting. One particular market problem the Fed is well designed to address is insufficient liquidity—a situation in which cash in the financial system is either in unusually high demand (beyond what financial markets themselves can supply), unusually low supply (because markets are impaired from normal provisioning), or both. In this situation, the Fed can step in to provide a backstop source of liquidity in targeted financial markets. Doing so helps restore market functioning as well as confidence in their steady operation going forward. The Fed has a number of ways in which it can serve as a backstop source of liquidity; it can use its standard tools as well as its emergency lending authority.

In March 2020, with the COVID-19 pandemic underway, financial markets became strained as cash was in very high demand. It had become clear that the pandemic would cause severe disruptions in business activity, including substantial job losses, and would also disrupt other areas of the economy.5 With many businesses' cash receipts slowing or ceased, and investors preferring safe, liquid assets in these circumstances, many market participants simultaneously sought to raise cash, in part by selling less-liquid assets and pulling back from some routine investments. These actions contributed to a severe deterioration in the functioning of a number of markets, including those for Treasury securities and agency MBS that are central to short-term funding.6 The Fed needed to urgently step in to provide liquidity to financial market participants and help restore the functioning of these and other key markets.

The Fed addressed the extraordinary demands for liquidity in March 2020 in a number of ways. Table 1 lists these actions—all of which aimed to stabilize short-term funding markets—in the second, shaded block of entries. The Fed immediately increased the size and frequency of its offers to conduct repurchase agreements (repo), a transaction in which the Fed temporarily lends cash in exchange for Treasury and other government-backed securities as collateral. Reflecting the severe strains in short-term funding markets at the time, take-up of the Fed's repo operations was initially quite large, peaking near $500 billion in mid-March. This take-up subsequently declined as market functioning improved, and it dropped to near-zero in early July.

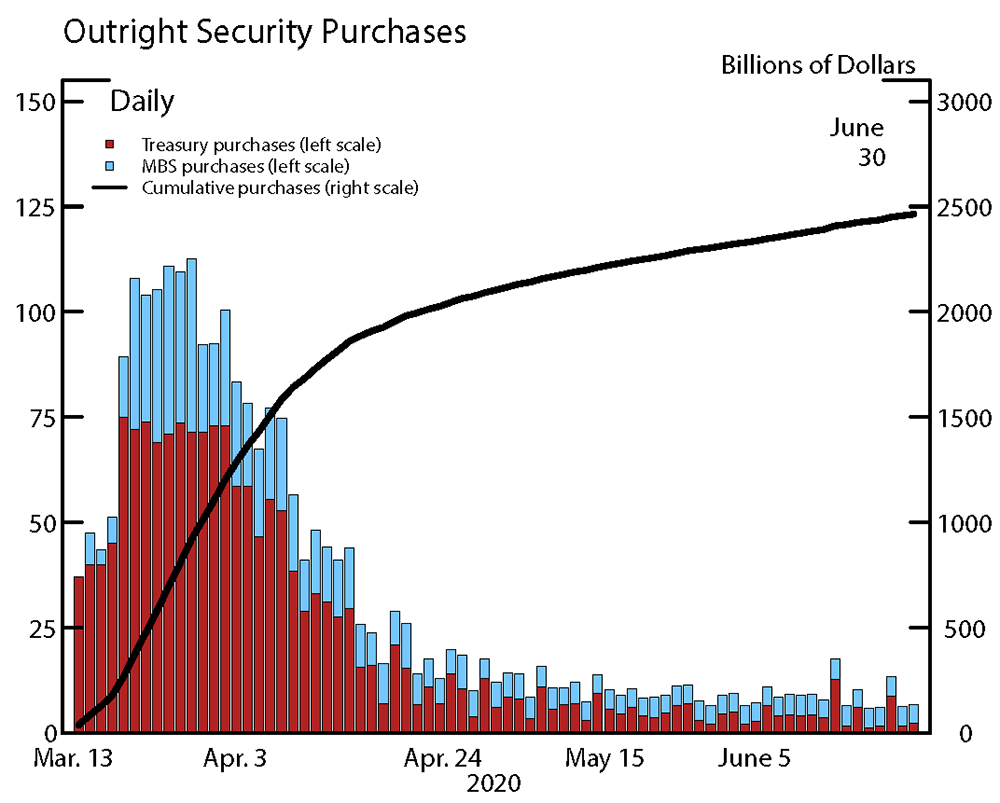

Shortly after beginning these sizable repo operations, the Fed announced that it would substantially increase its purchases of Treasury securities and agency MBS.7 Given the severe dysfunction in these markets, the Fed quickly ramped up its daily purchases of these securities to an unprecedented level, one that exceeded $100 billion a day for several days in late March (see the red and blue bars in Figure 1). In early April, market functioning began to improve, and the Fed started to slow its pace of purchases. Overall, between mid-March 2020 and the end of June, the Fed purchased a total of about $2 1/2 trillion of these securities (see the black line in Figure 1).8

Note: Cumulative purchases are from March 13.

Source: Federal Reserve Bank of New York.

(Treasury securities purchase amounts (red bars): https://www.newyorkfed.org/markets/domestic-market-operations/monetary-policy-implementation/treasury-securities/treasury-securities-operational-details#monthly-details. MBS purchase amounts (blue bars): https://www.newyorkfed.org/markets/ambs/ambs_schedule accessed week of June 30, 2020.

During this time, borrowing from the Fed's standing discount window also increased following the combination of policymakers' public communications encouraging its use and changes to the program to offer more favorable loan terms. In addition, to address strains in global dollar funding markets, the Fed announced an expansion of its dollar liquidity swap lines with foreign central banks and introduced a temporary Foreign and International Monetary Authorities (FIMA) Repo Facility to make it easier for foreign and international monetary authorities to access dollar funding. With direct access to U.S. dollar funding, these monetary authorities become better positioned to meet demands for U.S. dollars in their local jurisdictions.

Moreover, as the COVID-19 pandemic had caused "unusual and exigent circumstances," the Fed, with approval of the Secretary of the Treasury, invoked its authority granted under section 13(3) of the Federal Reserve Act to establish broad-based lending facilities.9 Some of these facilities were established to stabilize short-term funding markets, a step that ultimately supports the flow of credit to households, businesses, and communities. In particular, and as also listed in the second (shaded) block of items in Table 1, the Fed launched the Commercial Paper Funding Facility (CPFF) to encourage investors to engage in term lending to corporations; the Money Market Liquidity Facility (MMLF) to help stem rapid outflows from some money market funds; and the Primary Dealer Credit Facility (PDCF) to provide loans to these key financial intermediaries in exchange for sound collateral. These facilities provided important backstops for particular segments of the financial system that had become impaired and thus, indirectly, contributed to a broader improvement in the flow of credit in the economy. Sometimes such improvement can occur without much usage of a given Fed facility because, by setting up the facility as a backstop, the Fed restores confidence in the market among its participants.

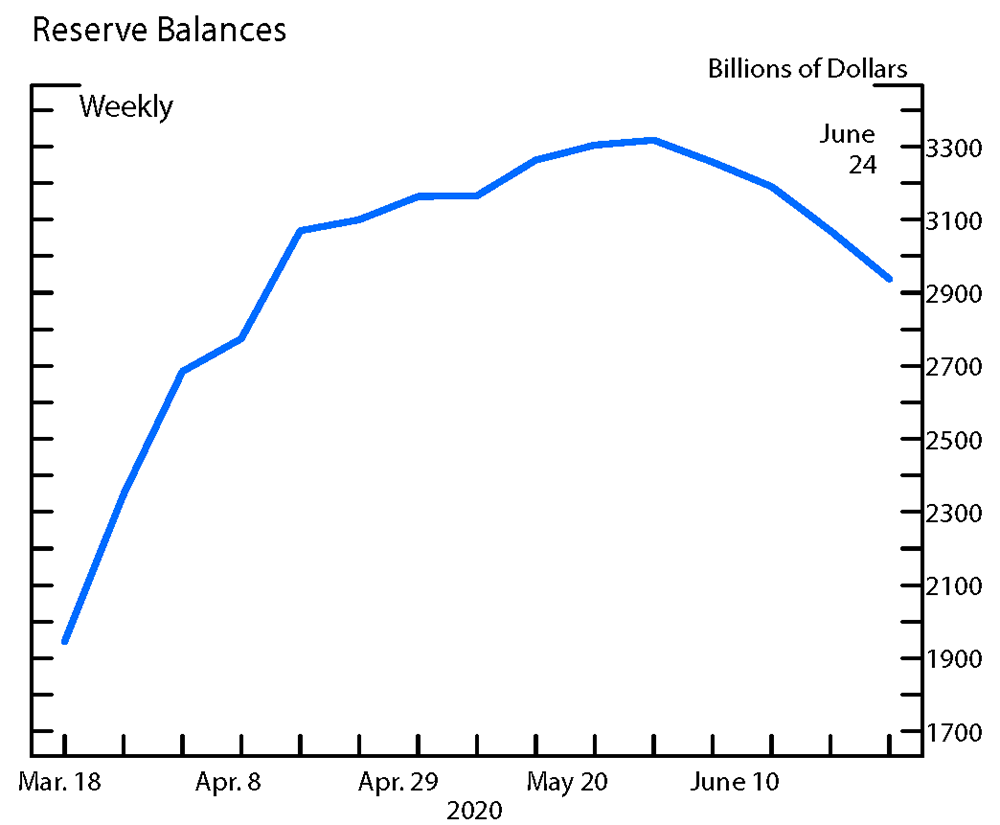

As a result of these various actions to support the smooth functioning of short-term funding markets, between mid-March and June 2020, the size of the Fed's balance sheet expanded substantially. The sizable increase reflected the fact that banks' reserve balances increase one-for-one with each dollar the Fed "invests" in securities purchases and also with each dollar of take-up of the Fed's crisis liquidity facilities.10 At the end of June, the level of reserves in the banking system stood at just under $3 trillion, about $1 trillion higher than it had in mid-March, on net (see Figure 2).

Note: The values shown are utilization amounts.

Source: Federal Reserve Bank (2020). H.4.1 Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks. https://www.federalreserve.gov/releases/h41/ (Table 1, column 1 for Primary Credit, PDCF, MMLF, and PPPLF; Table 4, column 2 for CPFF, SMCCF, MLF, and TALF; accessed week of June 24, 2020).

Action 3: Support credit flow more directly

When a crisis hits the economy, the Fed may also take steps to support more directly the flow of credit to households, businesses, and communities. When financial markets or the economy, or both, are strained, market participants may be reluctant to intermediate the flow of credit from lenders to borrowers, and some lenders may even temporarily exit certain credit markets altogether. The Fed's actions on this front can serve as a backstop in credit markets, and form an important component of the Fed's overall support of economic activity.

When the COVID-19 pandemic set in, the Fed created several temporary facilities to help restore the flow of credit in various sectors of the economy. The facilities, whose terms in some cases were revised over time in response to the public's feedback, aimed to improve the supply of credit to households, businesses, municipal governments, and nonprofit organizations. These facilities are shown in the third (unshaded) block of entries in Table 1. Many of these credit facilities took some time to become operational, but once in place, they also contributed to the rise in the level of reserves in the banking system seen in Figure 2.

Here we provide very brief descriptions of these facilities.11 The Paycheck Protection Program Liquidity Facility (PPPLF) was designed to help small businesses keep employees on payroll by supporting the related Paycheck Protection Program created by the CARES Act and administered by the Small Business Association; the Main Street Lending Program (MSLP; a set of five facilities) was established to support lending to both small and midsized businesses, and later also to nonprofit organizations; the Term Asset-Backed Securities Loan Facility (TALF) aimed to support lending to both businesses and consumers by facilitating the issuance of loans that are subsequently bundled into securities and sold to investors; two facilities—the Primary and Secondary Market Corporate Credit Facilities (PMCCF and SMCCF)—aimed to support the employment and spending of investment-grade businesses; and the Municipal Liquidity Facility (MLF) aimed to help state and local governments manage their needs for cash and serve their communities.

The Fed also took several steps on the supervisory and regulatory fronts to support bank intermediation, and thus ultimately the flow of credit in the economy. These actions included providing temporary relief from certain regulatory requirements, granting additional time to phase in new regulations, accelerating some previously planned adjustments to some regulations, and issuing supervisory statements encouraging banks to support those affected by COVID-19.12

A quick adding up of the Fed's COVID response

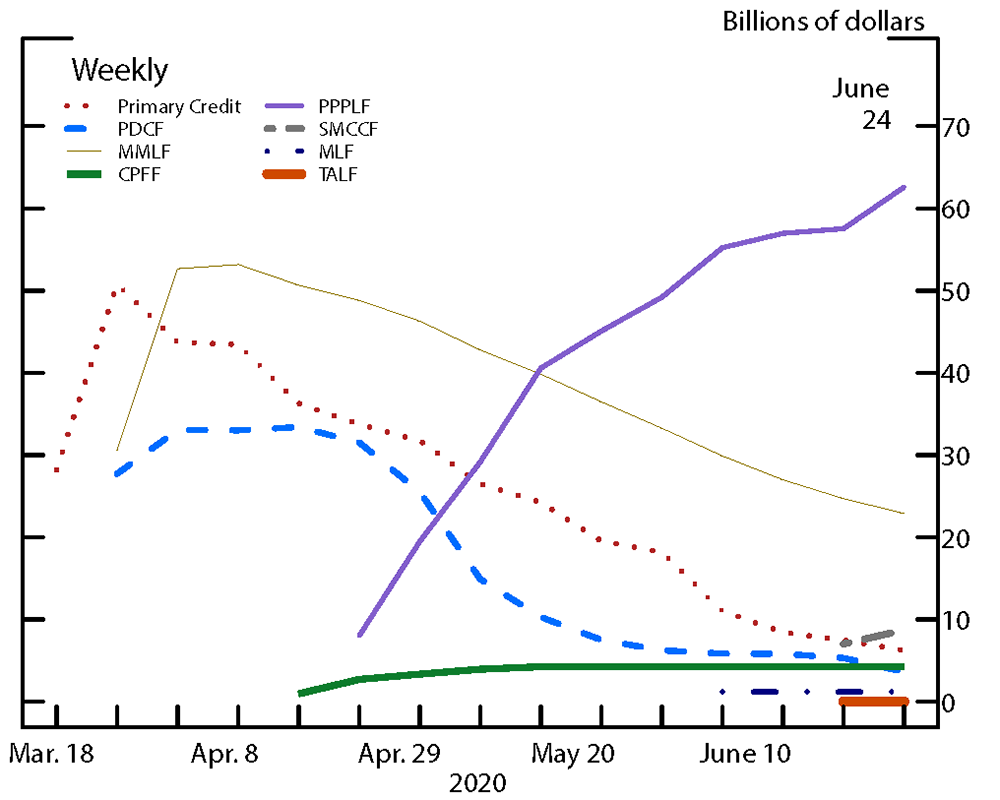

Figure 3 shows the take-up at several of the Fed's individual liquidity and credit facilities through the end of June 2020, including the volume of banks' discount window borrowing ("primary credit" on the chart; the red-dotted line). Here we highlight a few aspects of the use of these facilities.

As shown on the left side of the chart, the Fed's post-COVID liquidity facilities were made operational very quickly; they had all been used before, during the Global Financial Crisis. And, as discussed above, take-up at these facilities was generally swift, and concentrated around the time when market turbulence was at its peak, in mid-March 2020. Since then, take-up at these facilities has generally ebbed, in conjunction with the calming in financial markets.

Source: Federal Reserve Bank (2020). H.4.1 Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks. https://www.federalreserve.gov/releases/h41/ (accessed week of June 24, 2020).

In contrast, as shown in the middle and the right portions of the chart, other facilities, such as the PPPLF (purple line), took a bit more time to establish and, at this facility, take-up continues to rise. Other credit facilities, such as the MLF (the dark blue, broken-dotted line) and the SMCCF (the grey broken line) began operating in June, with modest take-up through the end of that month.13

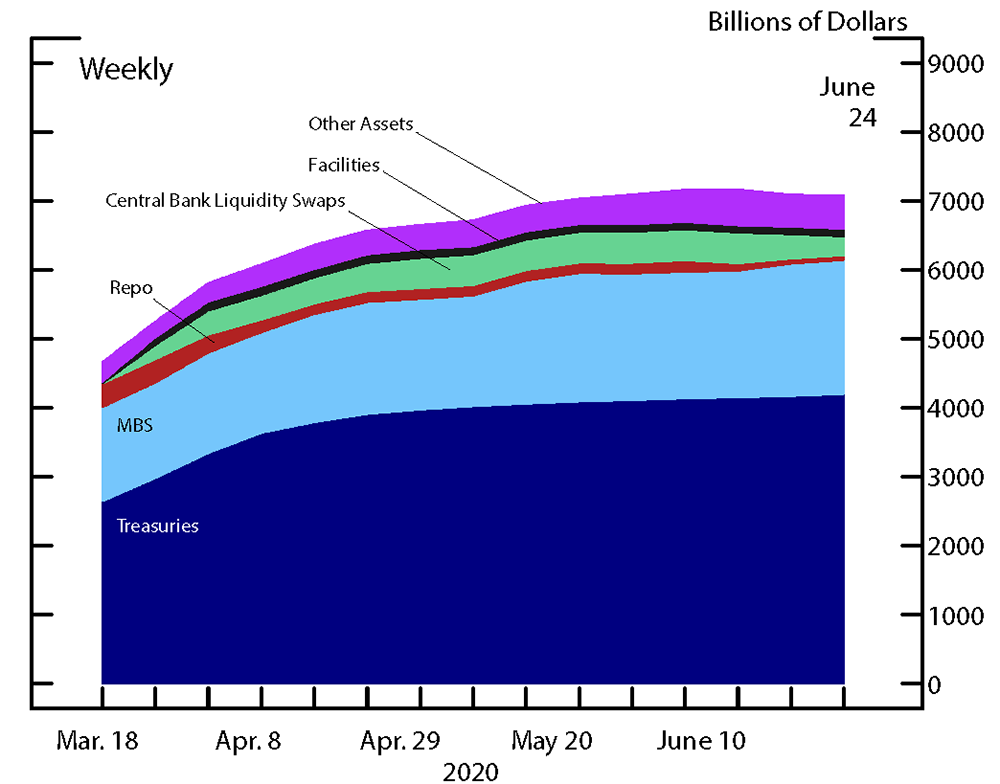

Figure 4 totes up the size of the Fed's balance sheet over the pandemic period between mid-March and June 2020, with the shaded regions showing the various contributions to its growth. Overall, the Fed's balance sheet increased from $4.4 trillion in mid-March to about $7 trillion at the end of June. As shown by the light and dark blue-shaded regions, the Fed action most responsible for the increases in its balance over this period was its securities purchases. In contrast, taken together, the Fed's facilities (in gold) have so far contributed a relatively small share of the growth in the Fed's balance sheet.

Source: Federal Reserve Bank (2020). H.4.1 Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks. https://www.federalreserve.gov/releases/h41/ (accessed week of June 24, 2020).

To sustain, or continue to make, improvements in market functioning and in the flow of credit in the economy more broadly, the Fed may choose to continue to employ a given tool for some time, including after its immediate benefits have been realized. For example, many of the Fed's facilities were scheduled to expire on or around September 30, 2020, and in July, the Fed extended most of these facilities for an additional three months, through the end of the year, with others extended through March 2021. The Fed described its extension as intended to facilitate planning by potential facility participants and provide certainty that the facilities will continue to be available to help the economy recover from the COVID-19 pandemic.14 Looking ahead, the Fed could continue to use its toolkit widely for some time, including by choosing to announce further extensions of its facilities, depending on the performance of financial markets and the economy.

Final thoughts

The Fed has a large toolkit to support the economy and financial markets when needed, including when a severe crisis hits. The Fed used several tools to help mitigate the effects of the Global Financial Crisis of 2007-09, and even more to help alleviate the COVID-19 shock. The COVID pandemic caused extraordinarily swift and severe disruptions to economic activity and financial markets. The Fed responded with unprecedented speed and scale by taking actions in each of three broad categories—it lowered interest rates, supported the smooth functioning of financial markets, and also supported the flow of credit to households, businesses, and communities more directly. All of the Fed's actions ultimately seek to achieve its congressional mandate of maximum employment and stable prices.

Reflecting the forceful actions the Fed took in response to the COVID-19 pandemic, its balance sheet, and reserve balances in particular, expanded at an unprecedented pace. Through all of its extraordinary actions—and through the associated substantial increase in reserve balances—the Fed seamlessly continued to implement monetary policy in the ample-reserves regime. The elevated level of reserves now on the Fed's balance sheet is obviously well above the level that had been considered "ample" before the COVID-19 shock hit, as we defined this concept (see Note 1 in this series). The robustness of the ample-reserves regime to a substantial expansion in reserves ensures that monetary policy implementation and transmission remain effective even when the Fed temporarily needs to carry a very large balance sheet to help achieve its congressional mandate, as is typically the case when a crisis hits the economy.

References

Bernanke, Ben S. "Causes of the Recent Financial and Economic Crisis." Testimony before the Financial Crisis Inquiry Commission, Washington, D.C., September 2, 2010; https://www.federalreserve.gov/newsevents/testimony/bernanke20100902a.htm.

Ihrig, Jane, Lawrence Mize, and Gretchen C. Weinbach (2017). "How does the Fed adjust its Securities Holdings and Who is Affected?," Finance and Economics Discussion Series 2017-099. Washington: Board of Governors of the Federal Reserve System, https://doi.org/10.17016/FEDS.2017.099.

Ihrig, Jane, Zeynep Senyuz, and Gretchen Weinbach (2020). "The Fed's "Ample-Reserves" Approach to Implementing Monetary Policy," Finance and Economics Discussion Series 2020-022. Washington: Board of Governors of the Federal Reserve System, https://doi.org/10.17016/FEDS.2020.022.

Ihrig, Jane, Gretchen Weinbach, and Scott Wolla (2020). "How Did the COVID-19 Pandemic Affect the Economy and How Did the Fed Respond?," Page One Economics. St. Louis: Federal Reserve Bank of St. Louis.

Logan, Lorie K. "The Federal Reserve's Market Functioning Purchases: From Supporting to Sustaining." Remarks at SIFMA webinar (as prepared for delivery), July 15, 2020; .

1. We thank Luke Morgan for his assistance with the data and figures, David Bowman, Helen Keil-Losch, Beth Klee, and Ed Nelson for their input on an earlier draft, Michael Palumbo for his input on this Note series, and Julie Carpenter for her assistance with publication. Return to text

2. The first two Notes in this series are based on Ihrig, Senyuz, and Weinbach (2020). Return to text

3. For more discussion, see Bernanke (2010). Return to text

4. See the FOMC's March 15, 2020, post-meeting statement, https://www.federalreserve.gov/monetarypolicy/files/monetary20200315a1.pdf. Return to text

5. For a discussion of the rapid deterioration in economic activity and employment at the onset of the COVID-19 pandemic in the United States, see Ihrig, Weinbach, and Wolla (2020). Return to text

6. See Logan (2020) for more discussion of the stresses in Treasury and MBS markets at this time. Return to text

7. Prior to the Global Financial Crisis of 2007-09, the Fed primarily used asset purchases as a tool for managing the supply of reserves in the banking system. Since then, the Fed's asset purchases have served other purposes as well. For example, to help the economy recover from the Great Recession, the Fed purchased securities to help lower longer-term interest rates after it had already reduced its policy rate to near zero (its effective lower bound). And the securities purchased by the Fed early on in the pandemic were targeted to improve market functioning; the FOMC directed the Open Market Trading Desk at the Federal Reserve Bank of New York to purchase Treasury securities and agency MBS "at a pace appropriate to support the smooth functioning of markets" for those securities (see https://www.federalreserve.gov/newsevents/pressreleases/monetary20200315a1.htm). Return to text

8. After its July 2020 meeting, the FOMC stated that it would continue its securities purchases over coming months to "sustain smooth market functioning." At that time, the Fed's daily purchases of these securities totaled about $9 billion per day. The FOMC's July statement may be found here: https://www.federalreserve.gov/newsevents/pressreleases/monetary20200729a.htm. Return to text

9. In addition to the Federal Reserve Act, the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 also governs this authority. In total, the Fed established thirteen "13(3) facilities." The U.S. Treasury is providing support to certain facilities, using the Exchange Stabilization Fund. (In some cases, Treasury's support was appropriated under section 4027 of the Coronavirus Aid, Relief, and Economic Security (CARES) Act.) For more information about the facilities described in this Note and about such facilities in general, see the Federal Reserve Board's web site: https://www.federalreserve.gov/monetarypolicy/policytools.htm and https://www.federalreserve.gov/newsevents/pressreleases/bcreg20151130a.htm. Return to text

10. See Ihrig, Mize, and Weinbach (2017) for a discussion of how the Fed's securities purchases affect the amount of reserves in the banking system. Return to text

11. For more information about these and other tools, see the Federal Reserve Board's web site: https://www.federalreserve.gov/monetarypolicy/policytools.htm. Return to text

12. The regulatory and supervisory actions taken by the Fed in response to the COVID-19 shock are listed on the Federal Reserve Board's web site: https://www.federalreserve.gov/supervisory-regulatory-action-response-covid-19.htm. Return to text

13. The Fed's Main Street Lending Program became operational on July 6. Return to text

14. For more information, see the announcement on the Federal Reserve Board's web site: https://www.federalreserve.gov/newsevents/pressreleases/monetary20200728a.htm. Return to text

Ihrig, Jane, Zeynep Senyuz, and Gretchen C. Weinbach (2020). "Implementing Monetary Policy in an "Ample-Reserves" Regime: When in Crisis (Note 3 of 3)," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, October 02, 2020, https://doi.org/10.17016/2380-7172.2744.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.