FEDS Notes

May 17, 2024

Why is the U.S. GDP recovering faster than other advanced economies?

Francois de Soyres, Joaquin Garcia-Cabo Herrero, Nils Goernemann, Sharon Jeon, Grace Lofstrom, and Dylan Moore1

On May 23, 2024, this Note was updated with an additional footnote (footnote 4) and reference (“Brooks, Robin, on X…”).

Economic performance since the onset of the COVID-19 pandemic has been very heterogenous across countries. While real GDP in the U.S. has already returned to its pre-pandemic trend, advanced foreign economies (AFEs) experienced a much weaker recovery, both relative to the U.S. and to their own pre-pandemic trend.2 In some countries, the gap between real GDP and its pre-pandemic trend has kept widening, suggesting continued scarring from the crisis as well as some new headwinds.

In this note, we investigate possible drivers explaining the stark difference in economic performance between the U.S. and AFEs over the past few years, considering both cyclical factors, such as fiscal and monetary policies, as well more structural factors, such as labor market flexibility and business dynamism. We also recognize the role of large shocks that particularly affected certain regions such as the economic shocks resulting from Russia's invasion of Ukraine that had an outsized effect in Europe. Although a precise quantification of each channel is left for future research, we argue that structural factors play a role in the way different economies responded to cyclical policies.3 In addition, we caution against interpreting recent productivity developments as only reflecting permanent shifts across economies.

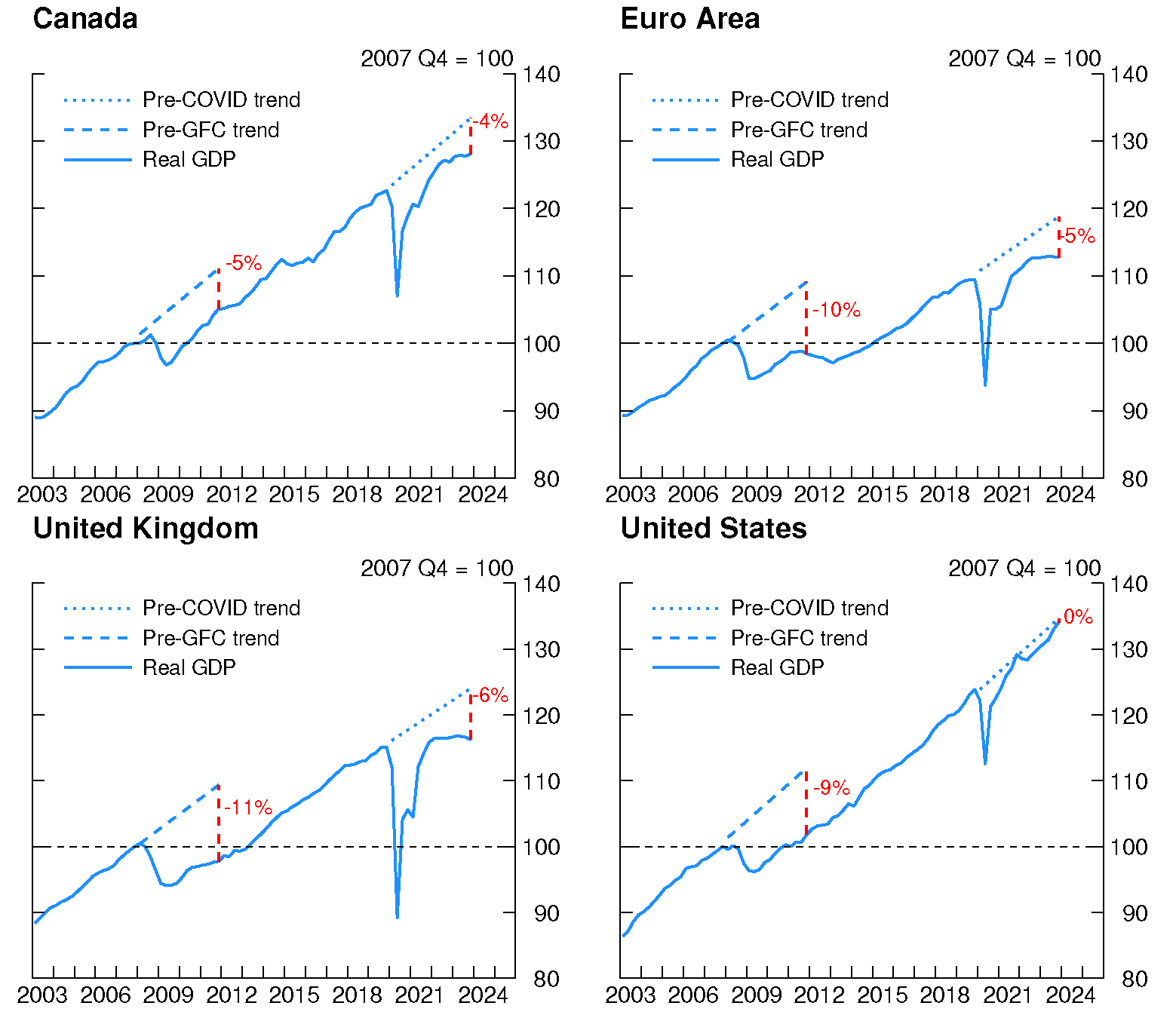

An overview of growth differentials.

For selected advanced economies, we compute output losses since the start of the COVID crisis by comparing each country's real GDP to its pre-pandemic trend. In Figure 1, we depict output losses in Canada, the euro area, the U.K., and the U.S. For each quarter, we define the output loss as the difference between the projected level of GDP based on its pre-pandemic linear trend, and the realized level of GDP. The projection is based on the five years before the COVID recession, and the red numbers labeled in Figure 1 reflect the output loss approximately four years after the onset of the recession. This measure of the output loss is one gauge for understanding the scarring effect of the pandemic on GDP, and, to provide context, we also provide the output loss for the Great Financial Crisis (GFC).

Note: The data extend through 2023:Q4. Trend lines are linear trends based on the 5 years before the recessionary episode. Red numbers show the difference between real GDP and the trend value.

Source: Haver Analytics; FRB staff calculations.

As Figure 1 shows, all regions experienced a significant output loss after the GFC, ranging from 5 percent in Canada to 11 percent in the U.K.4 The charts make clear that output losses from the GFC era were not temporary; rather, these regions saw permanent downward level GDP shifts, and although the growth rate of GDP returned to its original trend in some countries, the levels ended up permanently below the pre-crisis trend. The COVID shock also induced significant output losses in these jurisdictions, but with two key differences compared to the GFC. First, the U.S. has completely offset its output loss as of 2023: Q4, meaning that its level has returned to its pre-pandemic trend. The GDP effects of the pandemic appear to have been temporary, without any longer-run scarring. Second, Canada, the U.K., and the euro area have not returned to their projected pre-pandemic levels, and so far, their current trends appear somewhat flatter – implying that real GDP is growing at a slower pace than before the pandemic. In these countries, real GDP may be on track to be permanently below their projected pre-pandemic trends and, so far, their total output losses have only increased over time.

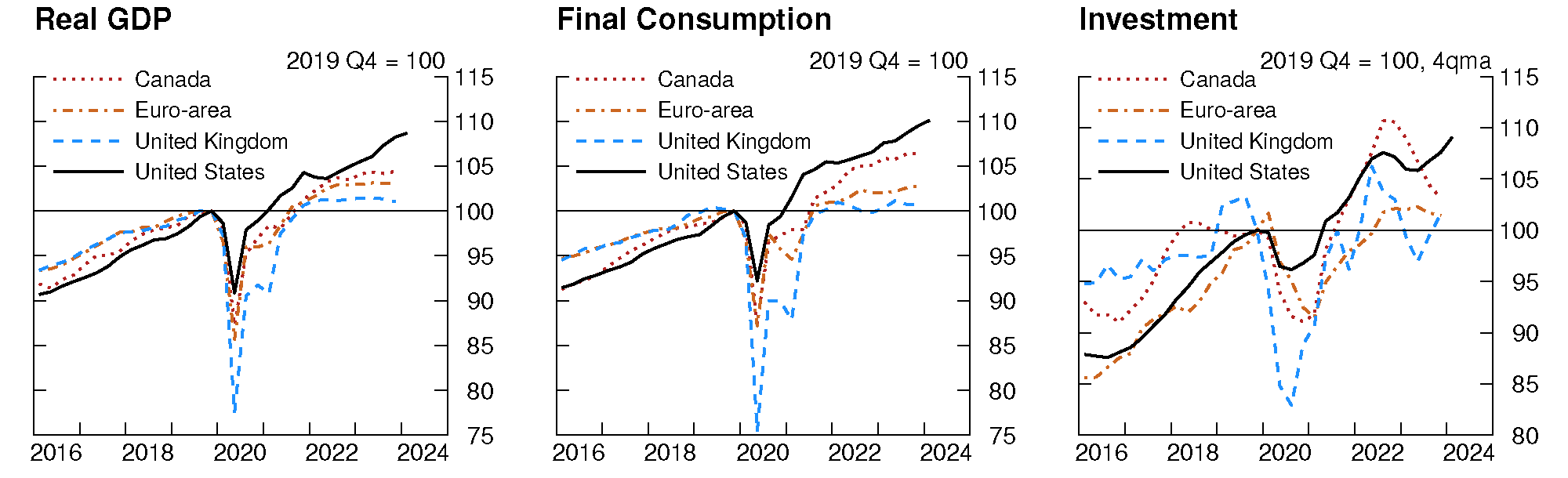

Taking a purely accounting perspective, Figure 2 looks at the demand-side component of real GDP and shows that the outperformance of the U.S. is largely due to strong final consumption and strong domestic investment. There are a variety of potential reasons why consumption and investment have been stronger in the U.S. than AFEs. As we will argue in the next few sections, the reasons underlying observed growth differences are broad-based, including differences in fiscal and monetary policies as well as more structural differences in the design of labor market institutions that shape how economies responded to shocks throughout the recent crisis.

Note: The data extend through 2023:Q4.

Source: Haver Analytics; FRB staff calculations.

Fiscal policy

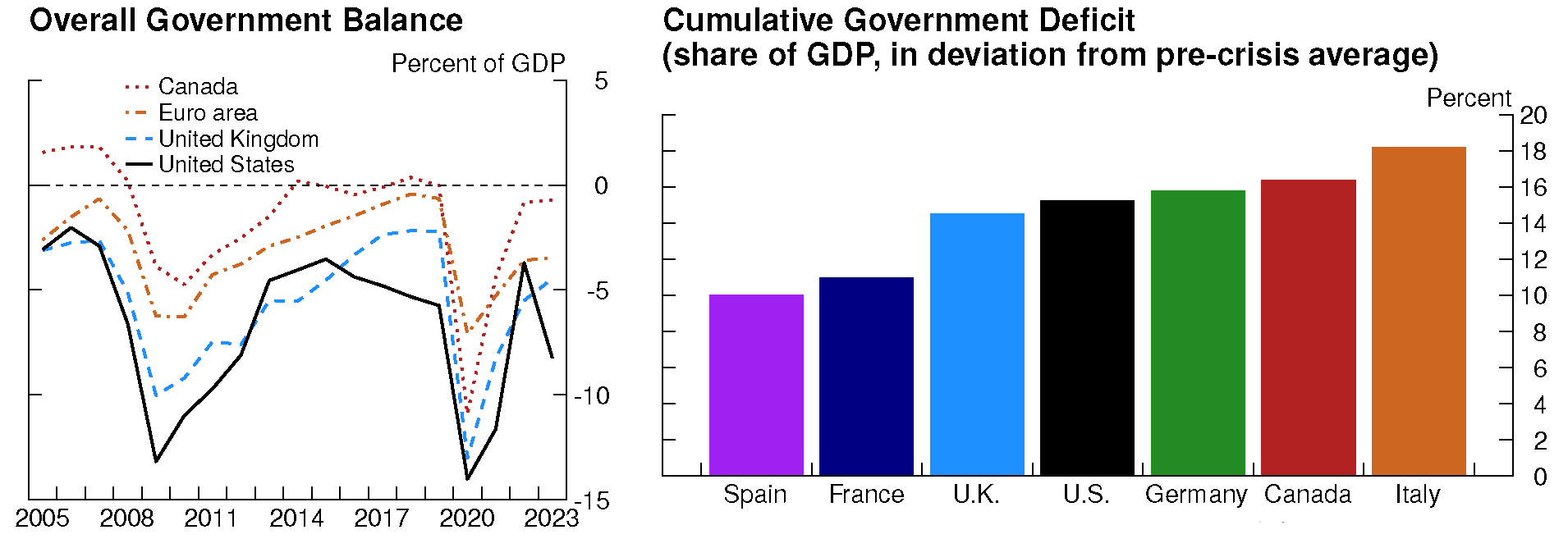

We begin our exploration of contributors to the divergence of post-pandemic growth with differences in fiscal policy-a factor whose exact role turns out hard to pin down. As a first pass, one can look at overall government balances, a metric which measures the difference between public revenue collected from taxes and government spending. The left panel in Figure 3 shows that the deficit in the U.S. was larger than in other featured regions. Interestingly, this stronger support happened not only during the Covid-19 crisis in 2020 and 2021, but also in 2023 as the economy recovered from the pandemic-shock. However, the U.S. does not stand out when computing changes in government deficit from pre-pandemic levels. In the right panel in Figure 3, the cumulative fiscal impulse from 2020 to 2023, expressed as deficit in deviation of its pre-pandemic average, puts the U.S. on par with the other AFEs. Such observation illustrates the difficulty of finding an appropriate proxy for fiscal stimulus.5

Left panel:

Source: International Monetary Fund.

Right panel:

Note: Calculated as the difference between primary government balance and the 2015-19 average.

Source: Haver Analytics; FRB staff calculations.

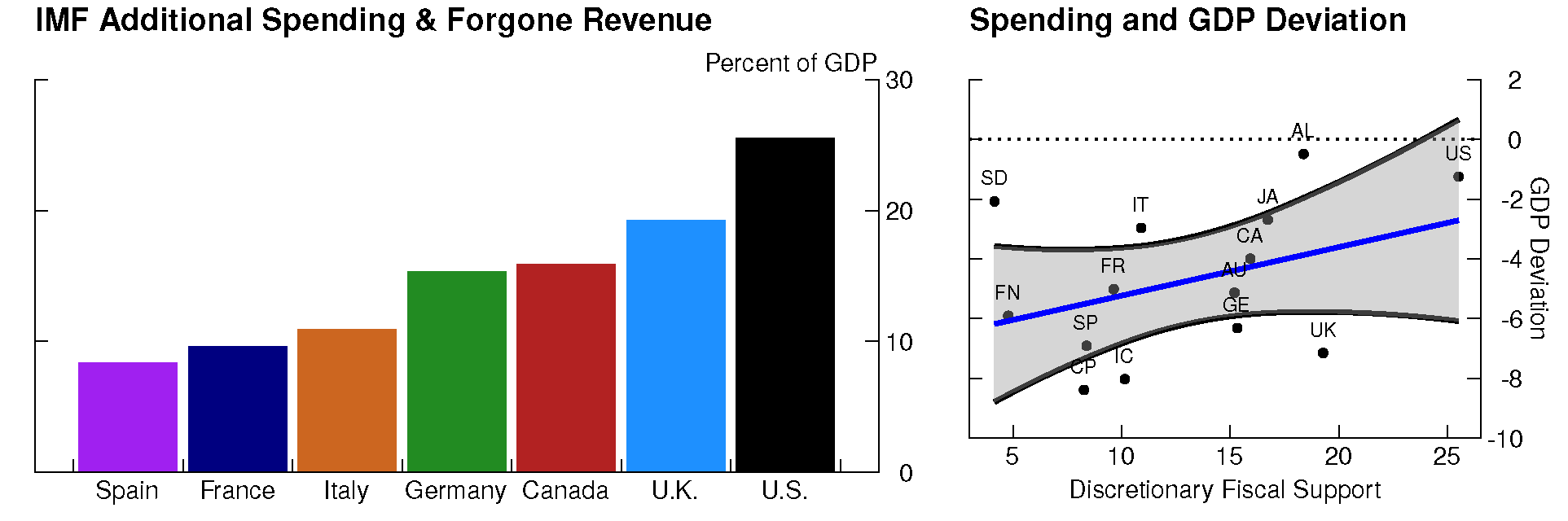

To investigate this issue further, we turn to data from the International Monetary Fund (IMF, 2021), which captures "fiscal measures governments have announced or taken in selected economies in response to the COVID-19 pandemic" from January 2020 to September 2021. The left panel in Figure 4 shows that according to this metric, the U.S. provided more fiscal support than AFEs. Using this data, we observe a positive association between government discretionary spending and the GDP loss metric defined above as the deviation from pre-pandemic trend. The right panel in Figure 4 shows that discretionary spending early in the pandemic, ranging from 8 percent of GDP in France to 25 percent of GDP in the U.S., is positively associated with our GDP loss metric at the end of 2023. This means that greater fiscal spending is correlated with lower amounts of GDP loss.6 That said, the association is weak overall, hinting that other elements are also at play in explaining the divergence in economic performance. Further, as highlighted in de Soyres et al. (2024), fiscal support led to a disproportionate increase in demand for tradeable goods, with effects that propagated internationally through global value chains. As such, since fiscal stimulus in one country likely boosted production not only domestically but also abroad, one should take country-specific analysis with caution.

Left panel:

Note: Estimates from Jan. 2020 to Sept. 2021. Numbers in US dollars and percent of GDP are based on October 2021 World Economic Outlook'.

Source: IMF; FRB staff calculations.

Right panel:

Note: GDP loss is calculated the deviation of 2023 GDP from the 2015-2019 average. Spending is calculated as the additional spending and forgone revenue from January 2020 to September 2021.

Source: IMF; FRB staff calculations.

Monetary policy

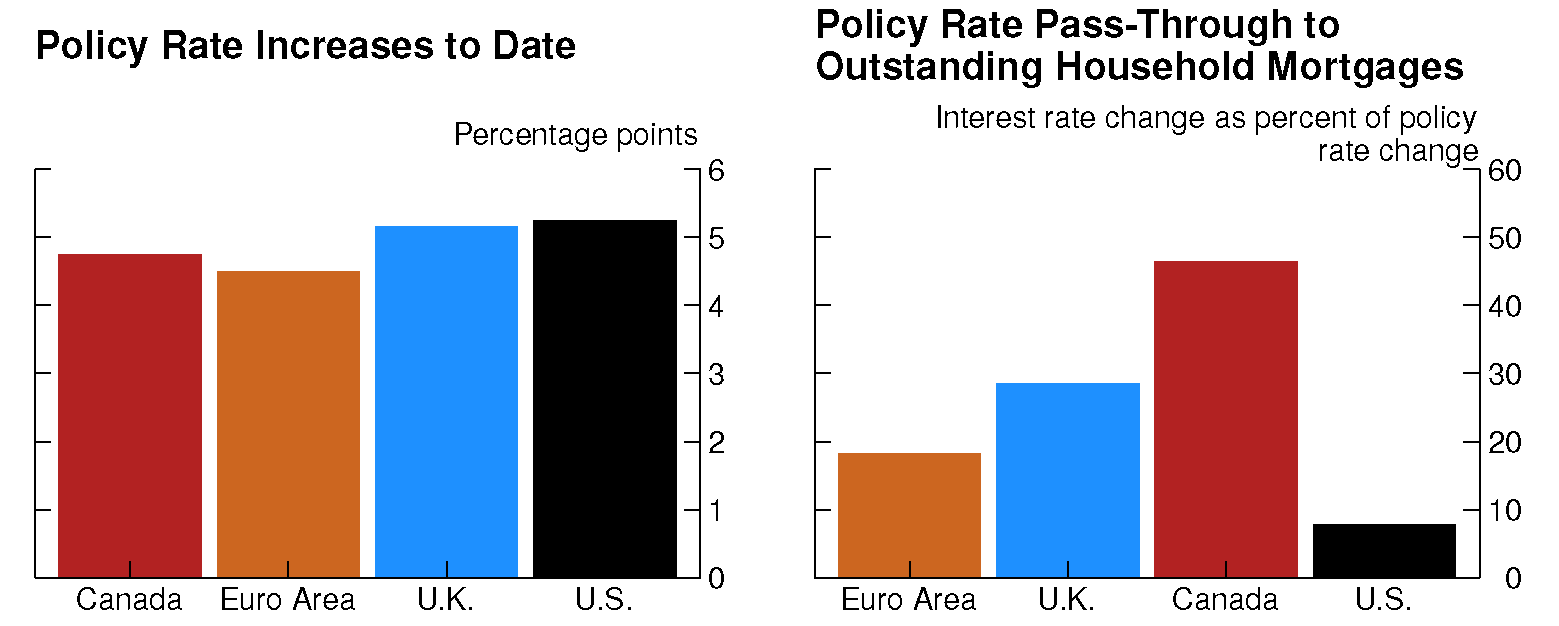

We turn now to monetary policy and its effects on borrowing costs. As shown in the left chart of Figure 6, cumulative policy rate increases since 2022 are roughly comparable, with the U.S. tightening slightly more than AFEs. However, the pass-through to outstanding consumer and firm loan rates was significantly lower in the U.S., especially compared to Canada.

As the right chart of Figure 5 shows, Canadian pass-through of policy rates to outstanding household mortgages, measured as the ratio of change in outstanding mortgage rates to change in policy rates, is more than four times that of the U.S. pass-through. Pass-through for the Euro-area and the U.K. are also considerably higher than for the U.S. It is not surprising that borrowing costs increased more significantly and more rapidly abroad than in the U.S.: the U.S. has higher shares of fixed-rate mortgages and corporate debt being termed out at fixed rates, and U.S. firms are also overall less reliant on the banking system. These elements generate important differences in the pass-through of monetary policy to borrowing cost and ultimately to economic activity.

Left Panel:

Note: Cumulative policy rate increase from the beginning of the hiking episode to present.

Source: Haver Analytics; FRB staff calculations.

Right Panel:

Note: Pass-through to outstanding household mortgage rates calculated as of January 2024 for the euro area U.K., Canada, and December 2023 for the U.S. The mortgage rates are the weighted average rates of oustanding, household mortgages among banks except for the U.S. where it is calculated as the effective mortgage interest rate on residential housing. The euro-area mortgage rate is the monetary financial institutions (MFIs) harmonized interest rate.

Source: S&P Capital IQ; mortgages: U.S. Bureau of Economic Analysis; national central banks.

Left Panel:

Note: Output per hour is GDP divided by total hours worked Employment is all employed persons in the euro area and U.S., those aged 15 years or older in Canada, and those aged 16 years or older in the U.K.. Hours per employee is the total number of hours worked divided by employment.

Source: Haver Analytics; FRB staff calculations.

Middle Panel:

Note: Latest values are February for Canada and the U.S., January for the euro area, and the U.K. is 3-month moving average with January as the end point.

Source: Haver Analytics; FRB staff calculations.

Right Panel:

Note: The reallocation index is calculated using year-over-year growth rates of employment from SIC industry classification.

Source: Statistical Office of European Communities, Bureau of Labor Statistics via Haver Analytics, FRB staff calculations.

Euro-area pass-through of policy rates to outstanding household mortgages is the most like that of the U.S., yet euro-area growth remains substantially lower than in the U.S. This is partly due to differences in labor market responses, as discussed in the next section.

Labor markets

Differences in fiscal policy, monetary policy, and pass-through can be exacerbated by structural factors that shape how the economy reacts to these stimuli. In this section, we focus on labor market dynamics and highlight important differences between the U.S. and AFEs.

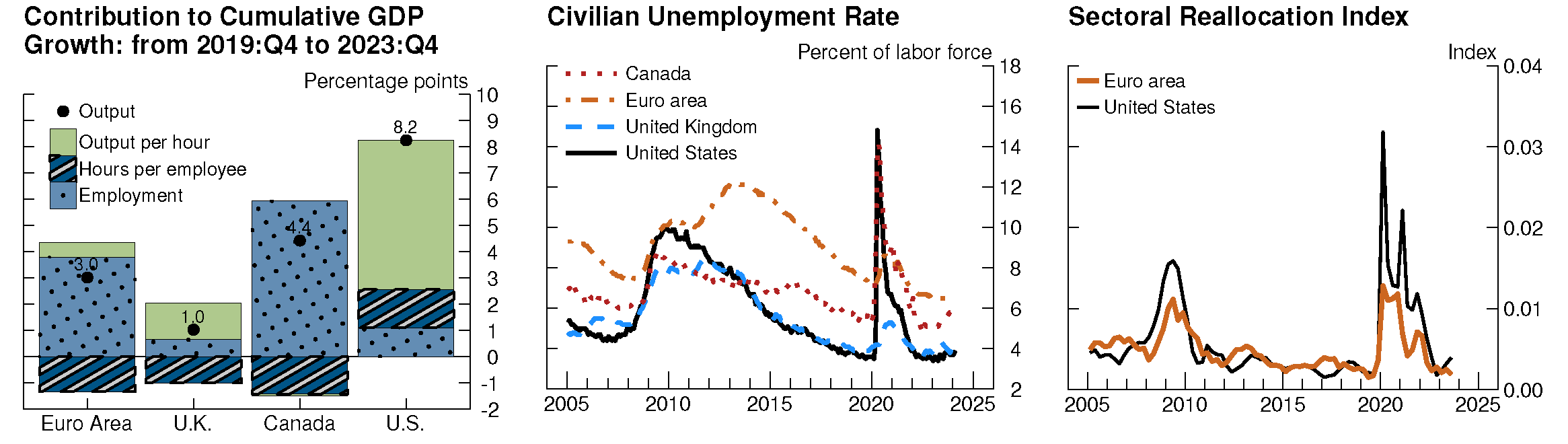

In the left panel of Figure 6, we show the change in the level of GDP since 2019:Q4. The change is decomposed into the contributions of labor productivity, hours worked per employee, and employment. We find that the gap in output performance between the U.S. and AFEs can be traced to a divergence in labor productivity, and, to a lesser degree, the number of hours worked per employee.

To understand these latest labor productivity developments, it is useful to note that many advanced foreign economies (AFEs) are traditionally considered to have more rigid labor markets, with more stringent employment protection as well as higher unemployment rates.7 During the Covid-19 pandemic, faced with an unprecedented shock, some AFEs aimed to maintain the firm-employee link and thus to prevent spikes in unemployment, which in previous recessions had proven to be very persistent. While such policies mitigated staggering unemployment rates towards the beginning of the pandemic in the euro area and the U.K., they also restricted the ability of the economy to adapt through sectoral reallocation. In the middle panel of Figure 6, we see that the unemployment rate increased several times more in the U.S. than in the euro area or the U.K. Moreover, the right panel in Figure 6 presents an index of sectoral reallocation as shown in Garcia-Cabo et al. (2023) for the U.S. and the euro area, based on a methodology proposed by Chodorow-Reich and Wieland (2020). We can see that that during the pandemic recession, there has been three times more sectoral reallocation of workers in the U.S. than in the euro area.

Importantly, one should note that the low labor productivity in AFEs likely comes from the fact that labor is under-utilized within firms. Indeed, policies preserving the firm-employee link in some AFEs led to adjustments along the intensive margin, with hours worked per employee decreasing somewhat – though the small decrease in hours worked does not necessarily reflect the full extent to which workers reduced their activity. In this sense, subdued labor productivity could be the mechanical consequence of weak aggregate demand, as firms retain employees without producing goods and services up to their full potential. Hence, as aggregate demand recovers, one might see a mechanical increase in labor productivity in advanced foreign economies, as firms are able to produce more without a comparable increase in their labor force. Again, this would mean that lower labor productivity in AFEs is not entirely a structural problem but can be partially explained by the response to weak aggregate demand. Lower AFE business dynamism, the topic of our next section, could also help to prolong the effects of recent shocks. These frictions might also explain why we see AFEs' GDP weakness show up mainly in contributions from hours worked and much less in contributions from employment.

Business dynamism

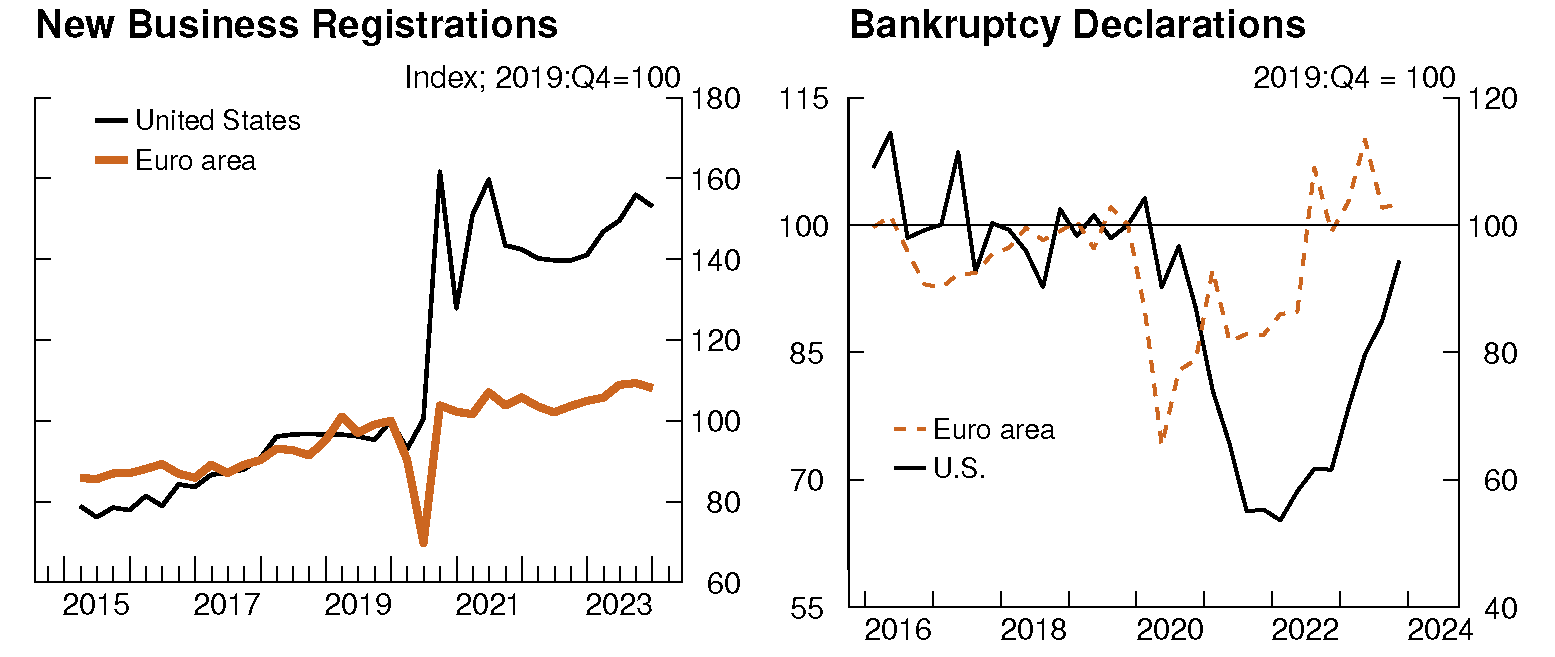

Another aspect worth highlighting, which is more structural in nature, is the stark difference in business dynamisms. Looking at new business registration in the left panel of Figure 7, we see that the U.S. has experienced an impressive increase in new firms' formation since the second half of 2020. Together with the high increase in unemployment discussed above, this surge in firms' creation likely supported the strong rebound in U.S. aggregate activity.

Left Panel:

Note: Data extend through 2023:Q4.

Source: Haver Analytics.

Right Panel:

Note: The data extend through 2023:Q4.

Source: Haver Analytics; FRB staff calculations.

Importantly, this trend is not reversing, as latest data shows that new businesses are still being formed at unprecedented levels. In contrast, business formation in the euro area is simply back at its pre-pandemic trend, without any make-up for the lost generation of firms that were not formed in 2020:H1 (the pandemic's first wave). Overall, the strength of new business creation depends on each country's regulations and processes, but also depends on the cyclical policies put in place by governments. In the U.S., strong fiscal policy, lower pass-through from monetary policy, and more a flexible labor market may have all contributed to supporting a new wave of firm creation over the past three years.

Turning to bankruptcy declarations, presented in the right panel in Figure 7, two messages emerge. First, while in the U.S. bankruptcies remained roughly at their pre-crisis levels until late in 2020, the euro area experienced an earlier decrease in bankruptcies – signaling that support to firms happened earlier in Europe. That said, bankruptcies in the U.S. remained notably lower than pre-crisis for a more prolonged period. With less bankruptcies over the past three years and more new firm creation, the U.S. stand out from the euro area in terms of overall business dynamism.

Other important considerations

Finally, our investigation of the growth divergence between the U.S. and AFEs would not be complete without a discussion of region or country-specific shocks.

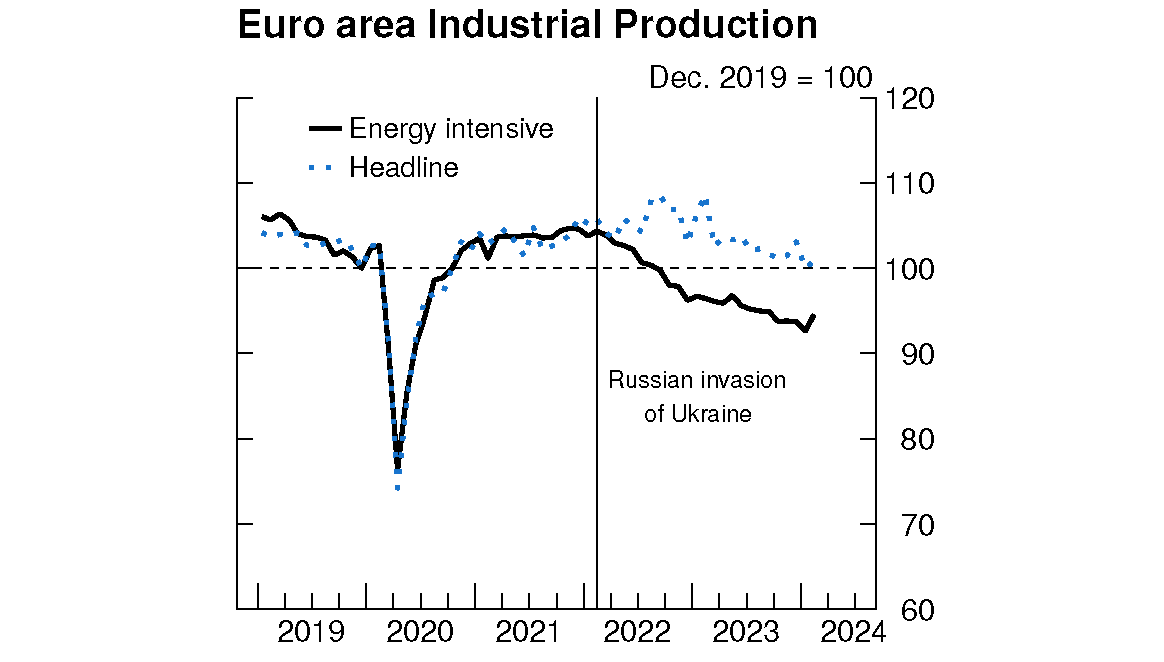

First and foremost, the large effects of the war in Ukraine on European economies must be acknowledged. The natural gas supply shock had a particularly strong effect on real incomes and energy-intensive industries. As can be seen in Figure 8, energy-intensive industries in the euro area are still reeling from the energy shock of 2022. In particular, private firms responded by substitution and reallocation of production, the details of which likely will weigh for a long time on productivity of some countries, notably Germany. In addition to the natural gas shock, declining sentiment related to the war weighed on aggregate demand and input-output linkages were disrupted.

Source: Haver Analytics; ECB; FRB staff calculations.

Second, the U.K. decision to leave the European Union (Brexit) may continue to weigh on U.K. domestic activity through a variety of channels. Among other effects, Haskel and Martin (2023) suggest that Brexit is at least in part responsible for the U.K.'s particularly poor performance since 2016, with investment about 10 percent lower than it would otherwise have been. Other authors such Springford (2022) estimate that Brexit has reduced U.K. trade in goods by about 13 percent. While considerable uncertainty remains regarding such precise quantifications, the ability of the U.K. economy to emerge from the Covid-19 crisis is likely reduced by the uncertainty and reduced market access that resulted from Brexit.

Third, industrial policy in the U.S., like the IRA and CHIPS acts, seem to have been effective in stimulating investment in key sectors. While similar policies are present in some AFEs, anecdotal evidence points to slower disbursements for various reasons, which might limit the pace at which these policies translate into strong economic effects.

Conclusion

Our analysis points to growth divergence between the U.S. and AFEs being the result of a variety of factors, including differences in monetary and fiscal policies, variations in labor and capital market institutions, and different region-specific shocks. It is currently challenging to judge how much exactly of the divergent performance is explained by each individual element. Overall, our analysis suggests that structural factors play a role in the way different economies responded to cyclical policies, and caution against interpreting recent productivity developments as only reflecting permanent shifts across economies.

References

- Brooks, Robin, on X: "The playbook after the 2008 crisis, https://x.com/robin_j_brooks/status/1769339142242984419.”

- Chodorow-Reich, Gabriel, and Johannes Wieland. 2020. "Secular Labor Reallocation and Business Cycles." Journal of Political Economy 128 (6): 2245-2287.

- de Soyres, François, Ana Maria Santacreu, and Henry Young. 2023."Demand-Supply imbalance during the Covid-19 pandemic: The role of fiscal policy." Federal Reserve Bank of St. Louis Review.

- de Soyres, François, Dylan Moore, and Julio Ortiz (2023). "An update on Excess Savings in Selected Advanced Economies," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, December 15, 2023.

- de Soyres, François, Alexandre Gaillard, Ana Maria Santacreu, and Dylan Moore. 2024. "Supply Disruptions and Fiscal Stimulus: Transmission through Global Value Chains, https://drive.google.com/file/d/1kGpQWfyvt6k30x_kbybcKE_968_O6rPw/view". American Economic Association: Papers and Proceeding, Forthcoming May 2024.

- García-Cabo, Joaquín & Lipińska, Anna & Navarro, Gastón, 2023. "Sectoral shocks, reallocation, and labor market policies, https://www.sciencedirect.com/science/article/pii/S001429212300123X?via%3Dihub". European Economic Review, Elsevier, vol. 156(C).

- Haskel, J and J Martin (2023), "How has Brexit affected business investment in the UK", Economics Observatory, March.

- IMF, 2021. Database of Country Fiscal Measures in Response to the COVID-19 Pandemic.

- Springford, John (2022), "The Cost of Brexit So Far", Centre for European Reform, June.

1. François de Soyres ([email protected]), Joaquin Garcia-Cabo Herrero ([email protected]), Nils Goernemann ([email protected]), Sharon Jeon ([email protected]), Grace Lofstrom ([email protected]) and Dylan Moore ([email protected]) are with the Board of Governors of the Federal Reserve System. The views expressed in this note are our own, and do not represent the views of the Board of Governors of the Federal Reserve, nor any other person associated with the Federal Reserve System. Return to text

2. In this note, the U.S. is taken to be the domestic economy, so AFEs refers to other advanced economies. Return to text

3. For example, lower barriers to entry likely result in a stronger rise in net business formation in response to fiscal measures, resulting in stronger productivity and employment growth in the short to medium term. Return to text

4. Similar charts showing the evolution of real GDP relative to trend have been produced earlier by Robin Brooks (2024). Return to text

5. Relatedly, de Soyres, Moore and Ortiz (2023) investigate the association between government spending (as opposed to deficit) and the accumulation of excess savings. They show that there is a significant positive association between government spending (in deviation from pre-pandemic average) and the stock of excess savings. Return to text

6. In addition, as noted in de Soyres, Santacreu and Young (2023), governments that provided generous fiscal support mitigated the drop in goods consumption in periods of pandemic-related lockdowns, while boosting the recovery of consumption when mobility restrictions loosened. Return to text

7. According to the OECD Employment Protection Legislation Database, the U.S. has the lowest level of employment protection among all OECD countries. Return to text

de Soyres, Francois, Joaquin Garcia-Cabo Herrero, Nils Goernemann, Sharon Jeon, Grace Lofstrom, and Dylan Moore (2024). "Why is the US GDP recovering faster than other advanced economies?," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, May 17, 2024, https://doi.org/10.17016/2380-7172.3495.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.